Summary:

- Jony Ive, Apple’s former Chief Design Officer, left the company about 1 year ago.

- As an Apple fan, this article takes a moment away from the daily/quarterly stuff to pay tribute to Ive.

- Ive’s departure was predicted to cause a 10% drop in the stock price. This, of course, did not happen.

- To me, this is a signal that the design-first spirit has been institutionalized at Apple and has become part of its moat.

- Apple now faces new opportunities and challenges, and Tim Cook is leading the company effectively through them, in my view.

Justin Sullivan/Getty Images News

Thesis

About a year ago (on July 13, 2022, to be exact), Jony Ive, the former Chief Design Officer of Apple (NASDAQ:AAPL), officially ended his relationship with the company. In a book entitled “After Steve” by Tripp Mickle, the author predicted that Ive’s departure would be enough to wipe out 10% of AAPL’s stock price. This is not what has happened in the past year. AAPL stock prices went up by almost 20% since Ive’s departure.

Of course, if the stock price did drop, it would be a good testament to Ive’s importance to AAPL. But viewed from a different perspective, the absence of stock price correction could be an even stronger testament to Ive’s legacy. To me, this signals that his design-first approach has become institutionalized at AAPL and a permanent part of its moat.

And this leads me to the thesis of this article (besides paying tribute to Ive as an Apple fan). In the remainder of this article:

- I will analyze how Ive, together with Steve Jobs, has elevated AAPL from a tech business to the most successful luxury brand. Tech enables us to do things faster – a basic human need. That is why tech stock will never be out of fashion. A luxury caters to an even more powerful human: the need to be different. If you think about it, doing things faster is only the means. Not the end. The end is to be different.

- I will then explain this is what I see as AAPL’s true moat and its key differentiator from other tech companies. I will elaborate on this aspect in later sections using a data-driven approach.

- Finally, I will provide an outlook on the new opportunities and challenges that AAPL is facing. I will argue that Tim Cook is leading the company through them effectively. Cook has pushed AAPL further, not only consolidating the luxury brand image Ive and Jobs created but also making it the most efficiently run luxury brand.

Jony Ive and AAPL

For readers not familiar with Ive or AAPL’s history, the next few paragraphs will provide a background to facilitate the subsequent analyses.

Ive’s partnership with AAPL has lasted for about 30 years. During his long career at AAPL, he has either led or had a significant impact on the design of almost every Apple product during that period. Examples included the Newton in 1993 to the Apple Watch and the more recent augmented reality headset.

In the early days, design was not a priority for the company and Ive considered leaving. This changed when Steve Jobs returned to Apple in 1997. Jobs and Ive shared a passion or even an obsession for design. To borrow a cliché, what happened next is history. They worked together and created some of the most iconic products ever made. The first-generation iMac (top panel), released in 1998, is a good example. The translucent shell of the iMac was unlike anything else (bottom panel) on the market at the time. It was an immediate hit, selling over 800,000 units in its first year.

Ive’s work has had a profound impact on Apple’s success. He has helped to create products that are both beautiful and functional. His designs have made AAPL one of the most – if not the most already – valuable brands in the world.

Source: Author

Hardware vs. luxury brand

As aforementioned, technology companies cater to the basic human need of doing things faster – an already powerful and perpetual need. And luxury brands cater to an even deeper and more powerful need: the need to be different. Ultimately, doing things faster is only the means to the end. My bull thesis on Apple is fundamentally anchored on this differentiator. I view it as the only tech company that has successfully transitioned from a tech business into a luxury brand due to the company’s unique combination of design (thanks to Ive), marketing, and technology.

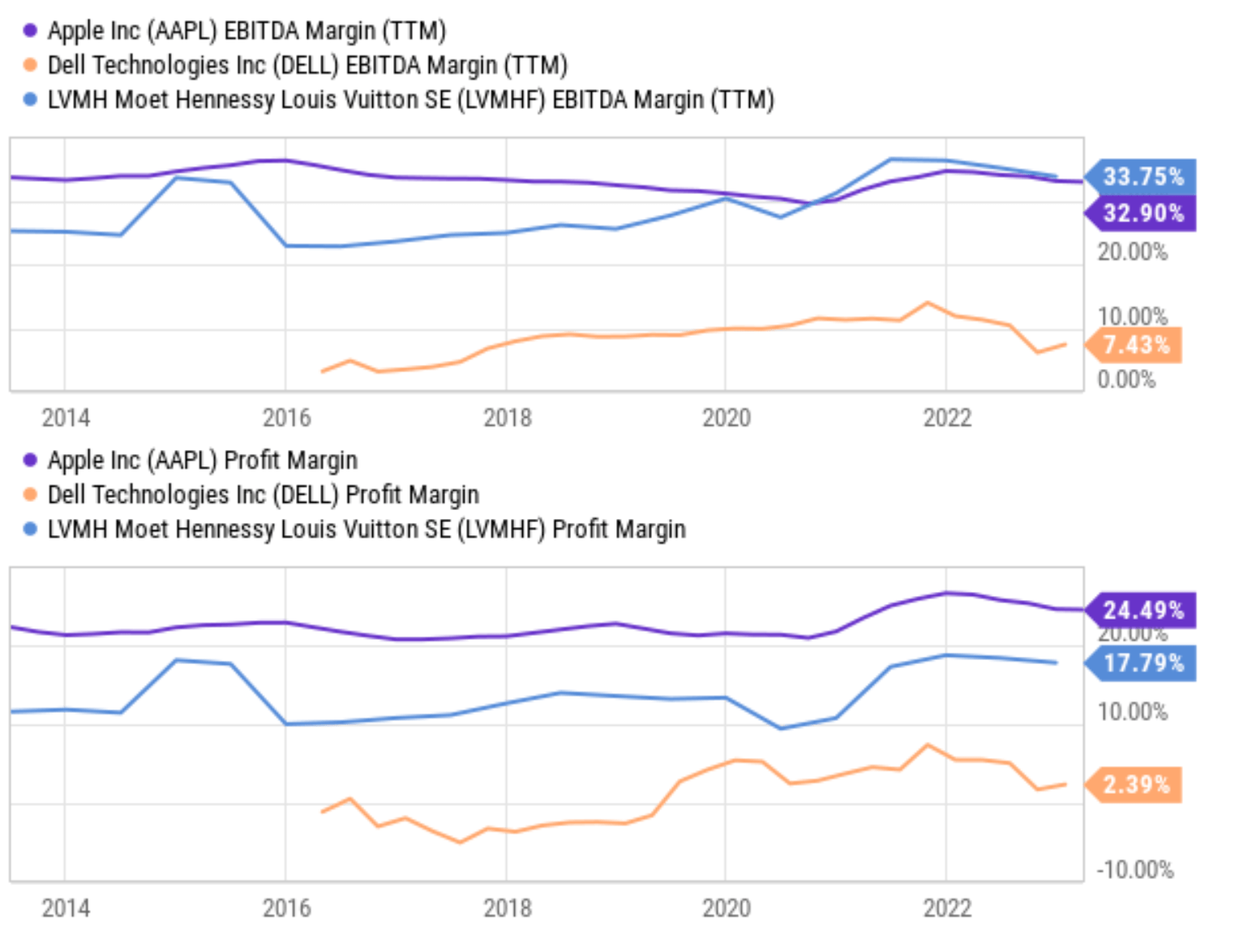

To make my point, the next chart shows AAPL’s margins, in comparison to two other stocks: LVMH Moët Hennessy – Louis Vuitton (OTCPK:LVMHF) and Dell (DELL). This seems to be an orange-to-apple comparison (pun intended). However, the point is to compare Apple’s margins again top luxury brands such as LVMH and a very successful hardware business such as DELL. As seen, AAPL’s EBITDA and net margins are not only far superior to DELL but are also superior to LVMH. To wit, its current EBITDA margins are on par with LVMH but have been historically higher than LVMH consistently. Measured by net margins, it consistently beat LVMH by a whopping 7%~10% over the past decade.

This is even more telling when we zoom in on Apple’s specific product lines. For example, the Mac series captures almost 60% of all the profit in the global laptop market, despite only having 7% of the market share. And consumers are more than happy to pay the premium price to get their Mac. According to this market share analysis, sales of AAPL’s Macs grew at 2x the rate of other PC brands in recent quarters.

Source: Seeking Alpha

Opportunities ahead

Looking ahead, I see more opportunities than challenges in the post-Ive era. And this section will outlook a few of the most important opportunities that I see. And I will leave the challenges that Apple is facing in the next section.

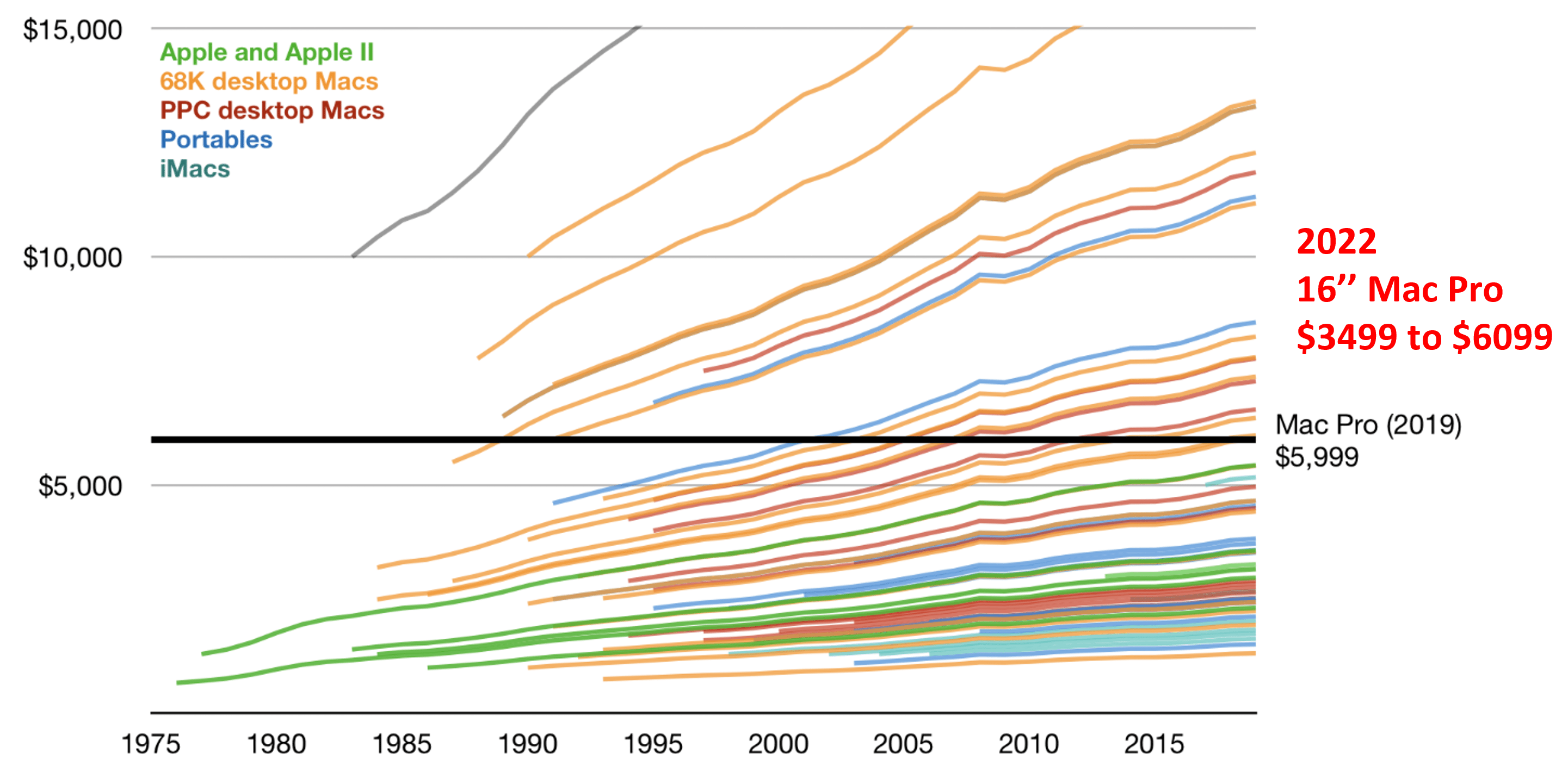

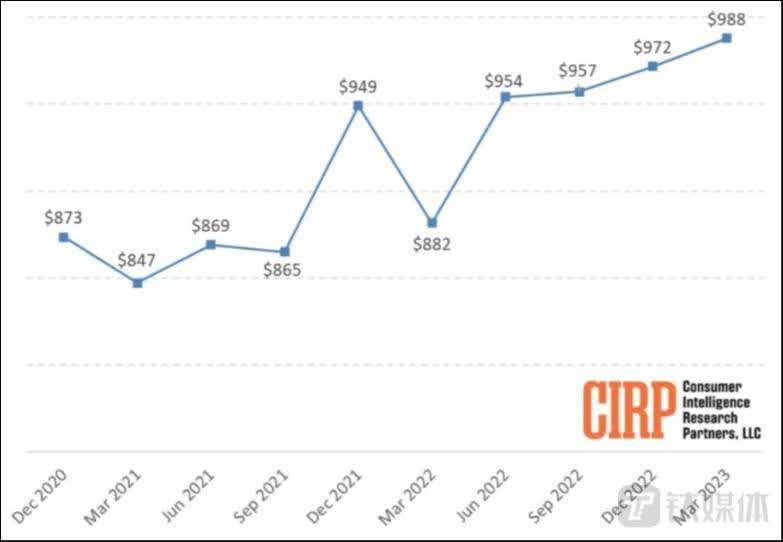

First, AAPL’s brand image offers superb pricing power. Using the Mac Pro as an example (see the next chart). The 2022 Mac Pro starts at $3,499. With upgrades and accessories, the price can easily reach $6,000+ (the price for a second-hand car), and users are still willing to pay – truly the hallmark of a successful luxury brand. Its other products such as the iPhone (see the second chart below) and iPad show exactly the same pattern.

Source: 512 Pixels

Source: Consumer Intelligence Research Partners

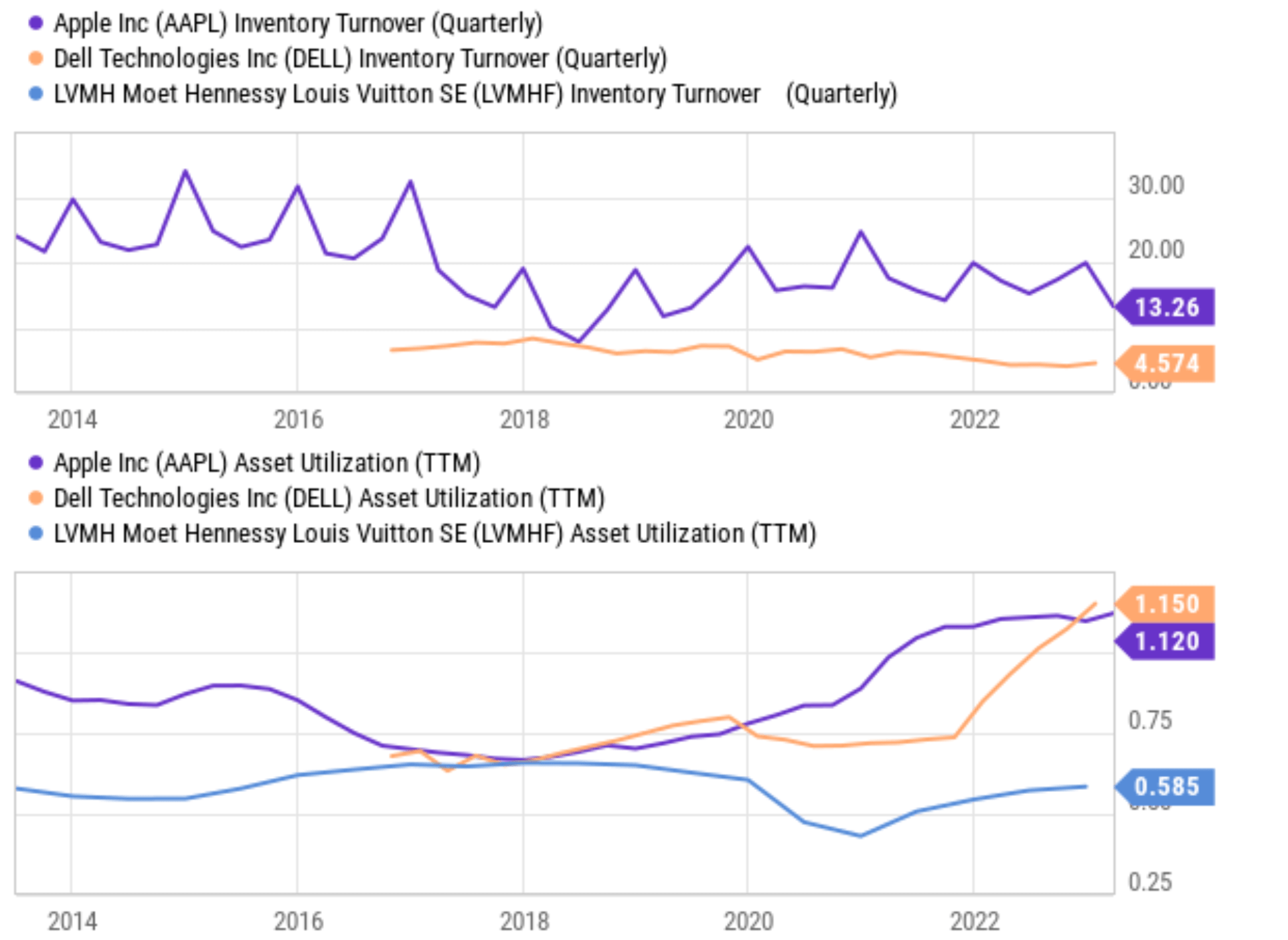

Second, the brand image and efficiency form an overpowered combo. As if a powerful brand name is not enough, Tim Cook then pushed Apple to new heights in operational efficiency. As seen in the next chart, Cook operates as a luxury brand with higher efficiency than a technology company. AAPL outperforms both tech stocks and luxury stocks vastly across all metrics I’ve checked (including inventory turnover, asset turnover, and inventory outstanding, et al). And for the sake of brevity, I’m only showing the charts for its inventory turnover rate and asset turnover rate below. As seen, AAPL’s inventory turnover rates exceed DELL’s by about 300% to 400% on average in recent years, and its asset turnover rates exceed LVMH’s by about 200% currently.

Source: Seeking Alpha

Challenges ahead and final thoughts

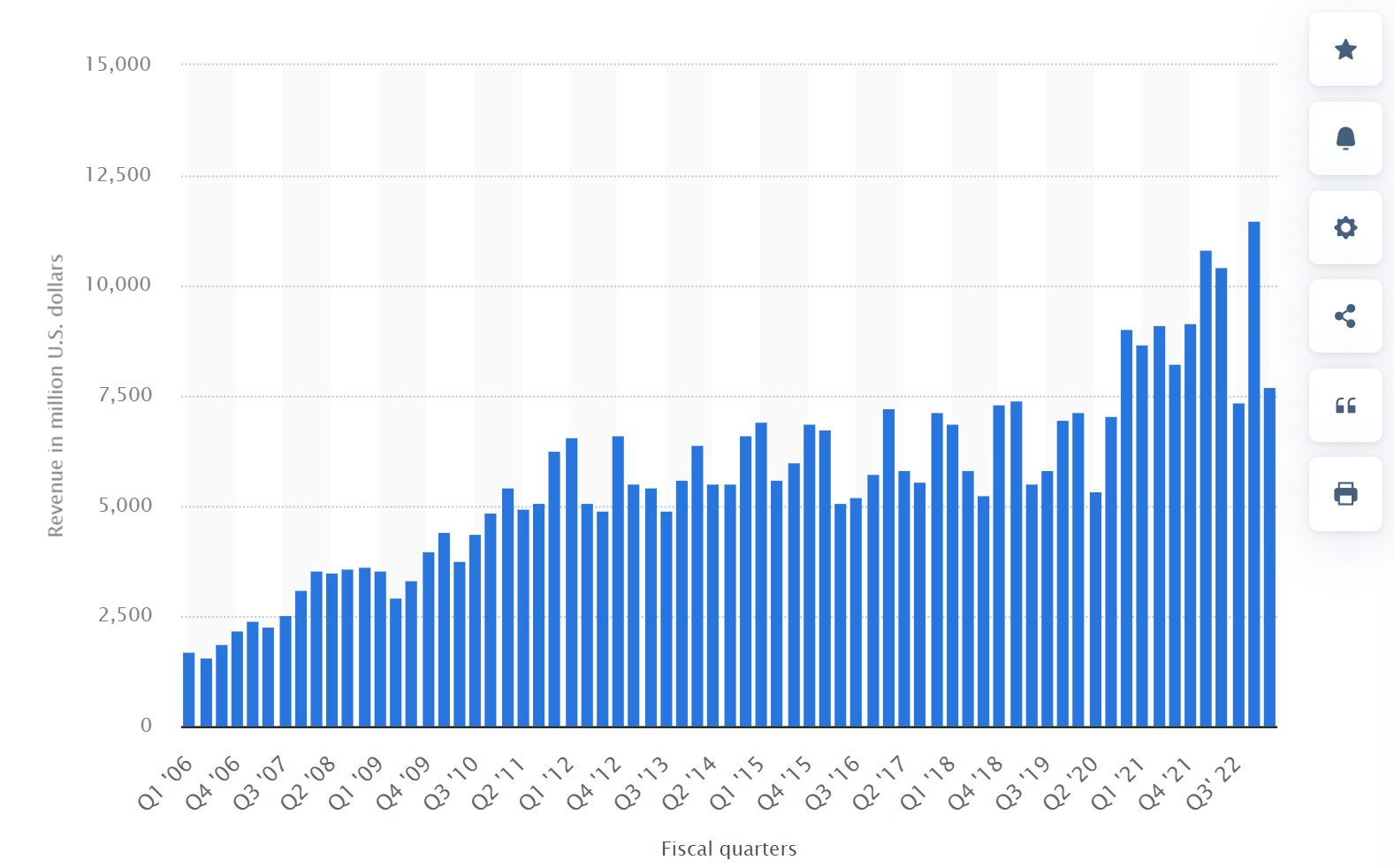

AAPL does face several challenges, both in the long term and immediate term. In the longer term, Apple relies on an intricate web of global suppliers and globalization has been disrupted in recent years by many factors. The factors include trade conflicts, the COVID pandemic (and possibly future ones too), and also the ongoing war in Ukraine. In the nearer term, some of AAPL’s individual products line are facing headwinds. In particular, its Mac revenue in Q1 2023 experienced a significant decline of 31.1% (see the chart below), which was the highest decline among all product lines. The Q1 revenue from Mac dialed in at $7.16 billion, compared to $10.45 billion in the same period last year. Revenue from iPad also declined and fell short of analysts’ expectations.

Source: Apple’s global revenue from Mac computers, statista.com data.

Also, as the Apple empire grows continuously, no single product line can lead to rapid growth anymore (which could be interpreted as good or bad news depending on your perspective). And if you are looking for rapid growth, you will essentially need to bet on a new category, such as AI or something more futuristic and therefore less certain.

All told, I see more opportunities than challenges. Speaking of a new category, as its user base grows, its subscription segment has the potential to be a new category. Sales from its services business reached a record ($20.8 billion) in Q1 2023. Subscriptions could be a very sticky growth driver and amplify the growth of other products (really, all its other products ranging from iPhone to wearables). Furthermore, I view its valuation (29.3x FWD P/E as seen in the chart below) as the more reasonable one among the FAAMG stocks. All around, it is an excellent combination of value, pricing power, superb brand image, and healthy growth prospects.

And most importantly, let’s thank Jony Ive for all the wonderful designs! And I look forward to seeing more creative designs with his new LoveFrom clients!

Source: Seeking Alpha data

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AAPL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.