Summary:

- Apple is allocating a significant portion of R&D funds towards generative AI efforts and building AI into every product.

- The company is looking to offset revenue decreases in iPhone, iPad, and Mac businesses with new product launches and improved performance.

- Apple’s services business continues to show growth potential, with over 1 billion subscribers and opportunities to monetize additional users.

Justin Sullivan/Getty Images News

In the last three quarters, Apple (NASDAQ:AAPL) has experienced a Y/Y decline in sales which prompted a lot of investors to raise questions about whether the company has any upside left given the relatively weak performance. Even though Apple’s stock has depreciated in the last month due to the recent mixed earnings report, it’s still hard to justify the business’s current premium valuation when the growth is non-existent. The good news though is that it seems that Apple has a plan to revive growth in the following months, which could undermine the valuation concerns and give its stock an ability to rebound in the short to near-term.

Tackling The Lack Of Growth

Apple reported its Q3 earnings results earlier this month and they showed that the company’s revenues decreased by 1.4% Y/Y to $81.8 billion but were in-line with expectations. This has been the third quarter of consecutive declines in sales that resulted in the depreciation of Apple’s shares in the last few weeks.

Apple’s Stock Performance (Seeking Alpha)

The biggest disappointment for Apple so far was the decrease of iPhone sales which were down 2.5% Y/Y in Q3 to $39.67 billion. The good news though is that we’re likely going to see an improvement in sales in the following months as Apple has been increasing its market share in India and Tim Cook himself noted that sales and services would accelerate in Q4.

In addition to that, we’re months away from the release of iPhone 15 which should give an even greater boost to sales as its starting price would likely be $799 and the phone is expected to have more advanced AI features that could lead to the increased demand for the new device.

At the same time, Apple is looking for ways to offset the revenue decreases for its iPad and Mac businesses which generated $5.79 billion and $6.84 billion in sales in Q3, down 19.8% Y/Y and down 7.3% Y/Y, respectively. Just recently, Bloomberg reported that Apple plans to release a new version of its flagship tablet next year to tackle the sluggish sales, while at the same time, it’s currently testing new M3 chips for its upcoming most powerful MacBook Pro that could be released in late 2023 or early 2024. The idea behind those new launches is to greatly improve the performance of the next generation of its devices so that the customers would be prompted to upgrade their devices, which would offset the lack of growth in recent quarters.

On top of that, even though the wearables business showed a decent growth of 2.5% Y/Y in Q3 and generated $8.28 billion in revenues during the quarter, there are reasons to believe that there’s more growth on the horizon thanks to the release of a Vision Pro headset in early 2024. Back in June, I’ve already highlighted in detail the advantages of the new device and explained why Apple’s pricing strategy should help the company avoid the same mistakes that Meta Platforms (META) made with its metaverse project. The most important thing that needs to be understood is that Vision Pro could help Apple offset the decline in sales of its other product categories and expand the company’s TAM at the same time.

What’s more, is that the services business shows no signs of stagnation and is likely to continue to be one of the biggest drivers of growth for Apple in the future. In Q3, Apple’s services business generated $21.21 billion in revenues, up 8.2% Y/Y, and helped the company finish the quarter with over 1 billion subscribers for the first time in the company’s history. Considering that Apple’s base consisted of 2 billion devices at the end of Q3, the company has more than enough opportunities to monetize up to 1 billion additional users that could generate more sales for the company in years to come.

In addition to that, Apple is also finally experimenting with generative AI in order to not be left behind by its peers. During the latest earnings call, Tim Cook acknowledged the significance of generative AI and indicated that a portion of the company’s R&D this year has been allocated towards the company’s efforts in the generative AI field. At the same time, Bloomberg last month reported that Apple is developing its own ChatGPT-like AI chatbot which engineers call AppleGPT and there are reasons to believe that the company would make a significant AI-related announcement in 2024.

Considering all of those product launches and potential announcements in the following quarters, Apple has a real chance to effectively tackle the latest sales slump and return to growth mode so that its shares would have the ability to rebound in the short to near-term. This should undoubtedly strengthen the bullish case for the stock, especially since the street believes that Apple would be able to grow its sales and profits by over 6% annually in the next two years thanks to those launches. That’s also one of the main reasons why it makes sense to believe that Apple could regain its momentum and its shares still represent an upside at the current levels.

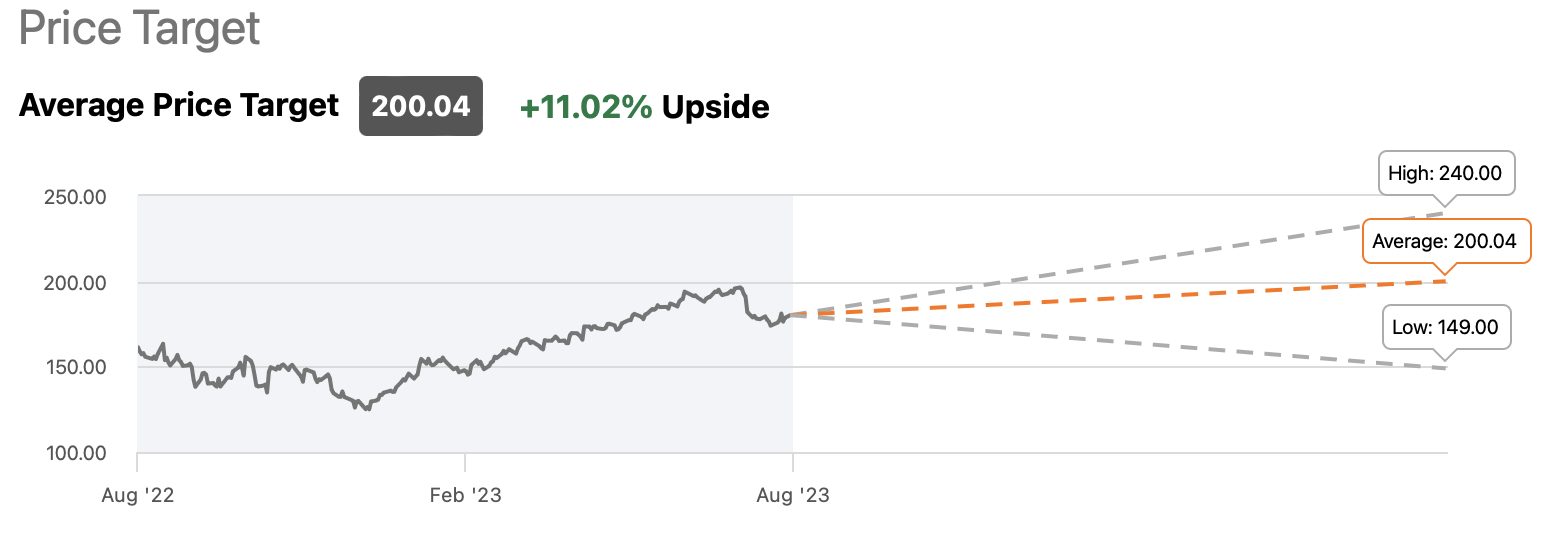

Apple’s Consensus Price Target (Seeking Alpha)

Risks To Consider

Although Apple’s stock is likely to get momentum going for it once the company begins to launch new devices in the following quarters, the geopolitical risks along with the valuation concerns could remain its biggest downsides.

In the last couple of months, Sino-American relations continued to worsen as China first restricted the exports of some materials that are used for chipmaking, then the U.S. officials noted that lifting the tariffs was premature, and then the Biden administration restricted investments in certain parts of the Chinese tech sector. Since Apple’s supply chain continues to be greatly exposed to Chinese-related risks and it’ll likely take eight years to move just 10% of its production capacity out of the mainland, the company’s operations could continue to be under the constant threat of disruption for years to come.

At the same time, after experiencing a decline in sales in the last three quarters, there are questions about whether the current valuation of Apple is justifiable. Even though the company has been underperforming against its Big Tech peers who reported decent returns in recent quarters, Apple continues to have a market capitalization of over $2 trillion and trades at over 7 times its sales and around 30 times its earnings. Considering that the company is not growing at this stage, the valuation for some no longer makes any sense. While the stock could regain its momentum once new products are launched, we might later end up in a situation where the business underperforms again once the excitement from new launches dissipates, and it would be hard to generate alpha when the shares are already in the overvalued territory.

The Bottom Line

There’s no denying that the geopolitical risks will continue to haunt Apple for years to come. However, there’s a possibility that the launch of new products along with its entrance into the generative AI field in the future would be able to help the company mitigate some of the downside caused by the relatively weak performance of some of its product categories in recent quarters. If that’s the case, then Apple’s shares would have the ability to rebound in the short to near-term despite all of the valuation concerns as the company’s ability to monetize various growth opportunities would lead to the change in sentiment and strengthen the bullish case.

As for the long-term, until Apple manages to significantly reduce its exposure to China and grow at a similar rate to its Big Tech peers, the upside of its stock would likely be limited.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Bohdan Kucheriavyi and/or BlackSquare Capital is/are not a financial/investment advisor, broker, or dealer. He's/It's/They're solely sharing personal experience and opinion; therefore, all strategies, tips, suggestions, and recommendations shared are solely for informational purposes. There are risks associated with investing in securities. Investing in stocks, bonds, options, exchange-traded funds, mutual funds, and money market funds involves the risk of loss. Loss of principal is possible. Some high-risk investments may use leverage, which will accentuate gains & losses. Foreign investing involves special risks, including greater volatility and political, economic, and currency risks and differences in accounting methods. A security’s or a firm’s past investment performance is not a guarantee or predictor of future investment performance.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Brave New World Awaits You

The world is in disarray and it’s time to build a portfolio that will weather all the systemic shocks that will come your way. BlackSquare Capital offers you exactly that! No matter whether you are a beginner or a professional investor, this service aims at giving you all the necessary tools and ideas to either build from scratch or expand your own portfolio to tackle the current unpredictability of the markets and minimize the downside that comes with volatility and uncertainty. Sign up for a free 14-day trial today and see if it’s worth it for you!