Summary:

- Unity’s inclusion in Apple’s Vision Pro headset solidifies its position as the go-to platform for developers creating immersive experiences for mixed reality.

- Unity’s revenue growth has been strong, driven by the increasing popularity of real-time 3D content.

- The integration with Apple’s ecosystem could lead to significant financial gains for Unity, including increased revenue from developer seats and a larger addressable ads market.

Justin Sullivan

Unity (NYSE:U), a leading real-time 3D development platform, is poised to become an industry leader with the release of Apple’s (AAPL) Vision Pro headset. The headset will natively include support for Unity-made projects, making it the go-to platform for developers creating immersive experiences for mixed reality.

Given how important spatial computing will likely be to the future of computing in general, this is a key moment for the company to cement itself in the tech stack of tomorrow.

Today, we’ll be exploring why we think Unity’s inclusion in Apple’s ecosystem is such a positive development, along with the potential impact on financials and the stock price.

Financial Results

As always, let’s begin with the financials.

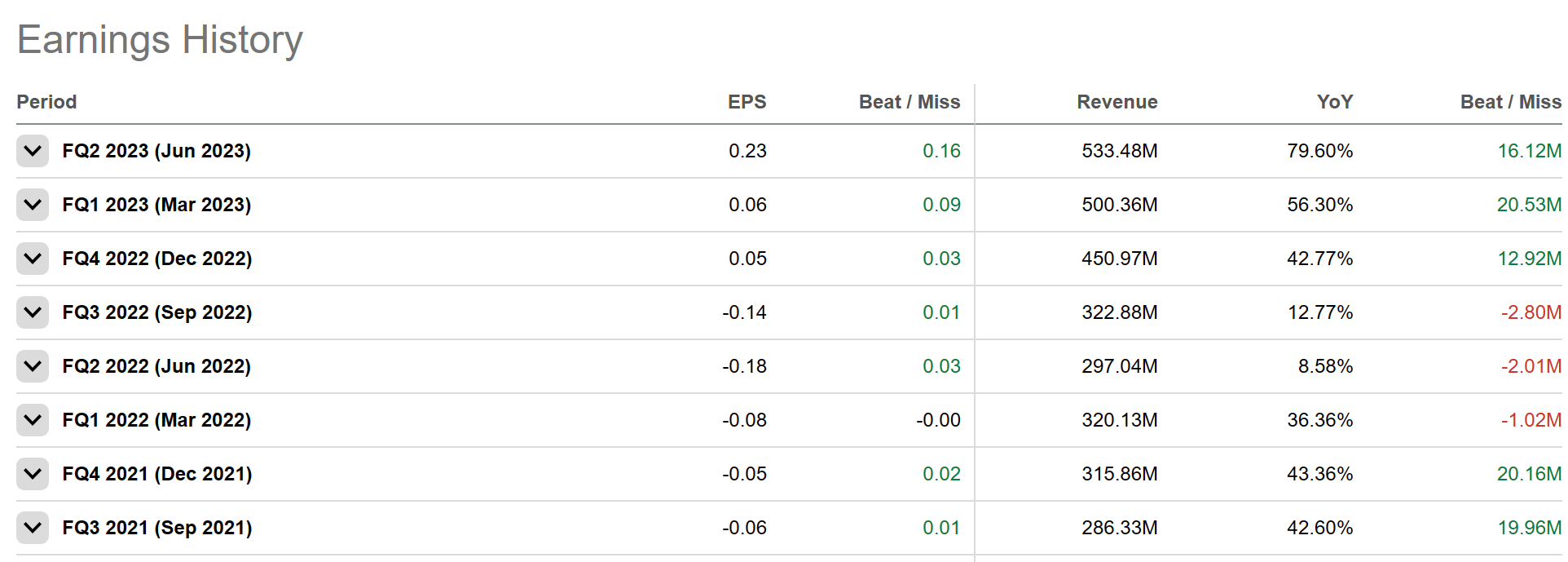

Unity’s revenue growth has been strong in recent quarters. In the second quarter of 2023, the company’s revenue grew 80% year-over-year (!) to $533 million:

Seeking Alpha

This was the company’s highest quarterly revenue ever. For the trailing twelve-month period, Unity’s revenue grew 48% year-over-year to $1.8 billion.

This strong revenue growth is being driven by the increasing popularity of real-time 3D content.

Unity’s platform is used to create games and mixed reality experiences, and the company’s customers include some of the biggest names in the tech industry, such as Google (GOOGL), Microsoft (MSFT), and Amazon (AMZN).

Unity monetizes this trend towards gaming and 3D in a few different ways.

First, the company operates a Grow segment. Grow primarily houses the company’s advertising solutions, and is how they monetize their “free” developer userbase:

We generate Grow Solutions revenue [as our] monetization solutions allow publishers, original equipment manufacturers, and mobile carriers to sell available advertising inventory on their mobile applications or hardware devices to advertisers for in-application or on-device placements. Our revenue represents the amount we retain from the transaction we are facilitating through our Unified Auction and mediation platform.

Second, Unity operates a Create segment, which houses per-seat subscription revenue that game developers pay for advanced features and premium service. This is revenue from the “paid” developer userbase:

We generate Create Solutions revenue primarily through our suite of Create Solutions subscriptions, enterprise support, professional services and cloud and hosting services. Our subscriptions provide customers access to technologies that allow them to edit, run, and iterate interactive, RT3D and 2D experiences that can be created once and deployed to a variety of platforms.

Together, they are growing at a solid clip, with Grow making up a majority of the YoY gains for Unity:

10Q

However, despite its strong revenue growth, Unity has not been profitable since IPO in 2021. In the most recent quarter, the company reported a net loss of $192 million. While this is an improvement from the 4 quarters previous to that which all saw more than $200 million in losses each, many critics have called for the company to improve its cost structure.

Unity’s profitability issues are due to a number of factors, including the high cost of sales and marketing, and the need to invest heavily in research and development. The company is also facing increasing competition from other real-time 3D development platforms, such as Unreal Engine.

However, in our view, things are not as bad as they seem. A majority of the net income losses are from D&A and stock-based compensation, which are non-cash expenses. On a cash basis, Unity is actually in the black, generating more than $351 million in TTM free cash flow.

While this somewhat obscures the situation, as much of the company’s talent only sticks around due to the SBC, the company is really only hurting investors by funding expenses this way.

The liquidity situation of the business is fine, as Unity has more than $1.6 billion in cash, and only around $975 million in current liabilities.

Taken together, and the best way to see Unity is as a high growth powerhouse with profitability issues but no real pressing liquidity concerns.

Unity In Vision Pro

Things improved materially for Unity when Apple announced its Vision Pro product in early June of this year. Mentioned briefly in a blink-and-you-might-miss-it moment of the presentation, Apple confirmed that the new Vision Pro headset would support Unity natively:

Apple

Unity later clarified questions about this integration by saying the following:

Let’s review the ways apps can run on Apple Vision Pro. There are three main approaches to creating spatial experiences on the visionOS platform with Unity.

- Port an existing virtual reality game or create a new fully immersive experience, replacing the player’s surroundings with your own environments.

- Mix content with passthrough to create immersive experiences that blend digital content with the real world.

- Run multiple immersive applications side by side within passthrough while in the Shared Space.

Thus, the integration runs rather deep, and should allow developers to import Unity apps into visionOS, or simply build new things natively using Unity’s Suite of products:

Unity

Network Advantages

To us, this inclusion is a game changer for Unity for three main reasons.

1.) Unity becomes the spatial computing standard.

2.) Unity will own the developer talent pipeline.

3.) Apple’s network effects could drive serious revenue.

Let’s start with the first two, which are more strategic, before finishing with point number 3, which could translate quickly to increased short term performance.

First, in our view, this move of positioning Unity as the only natively supported 3D platform, in what could become one of the largest mixed reality consumer products, effectively positions Unity as a concrete leader in the space. The fact that Apple is one of the world’s most popular brands doesn’t hurt things either. This gives Unity a major advantage over its competitors, such as Unreal Engine and Magic Leap.

Developers who want to create experiences for the mixed reality will have no choice but to use Unity, making it the de facto standard for metaverse / XR development.

There are all sorts of important knock-on effects as well, like our second point – Unity will own the talent developer pipeline.

When it comes to creating a moat around products, one thing that is often under-discussed is how new entrants to a profession end up being trained. If Unity remains the only natively supported 3D development suite for Vision Pro, then all else being equal, new entrants to the game and 3D development fields will make the rational choice and learn Unity first. This leads to custom workflows and assets, which ultimately leads to entrenchment.

Finally, as Made Easy – Finance pointed out in their recent article, even a small portion of Apple’s developer ecosystem moving over to try Unity could have a massive impact on medium term financial performance:

Firstly, AAPL’s partnership gives Unity access to over 34mil registered developers. We think that this is a relatively untapped addressable market for Unity. For instance, if 10% of AAPL’s registered developers subscribe to Unity’s Pro plan (which costs $2,040 per year), this presents Unity with additional $7bn annual revenue from developer seats alone.

AAPL’s new cloud computing platform also introduces an addressable market for Unity’s ads segment (Grow). With more affordable AR/VR/XR headsets planned, we think that the spatial computing platform is on the verge of early majority adoption. More AR/VR/XR users imply a larger addressable ads market.

We expect it’ll take Unity 1.5 years to begin reflecting the growth in developer seats which coincides with the official launch of the Apple Vision Pro. We also expect it’ll take Unity 3-5 years to begin reflecting the growth in ad revenue related to AAPL’s spatial computing platform.

All in all, this Vision Pro integration supercharges what was otherwise a quickly growing company, and with increased adoption, we expect that further revenue growth could translate to net income profitability as well.

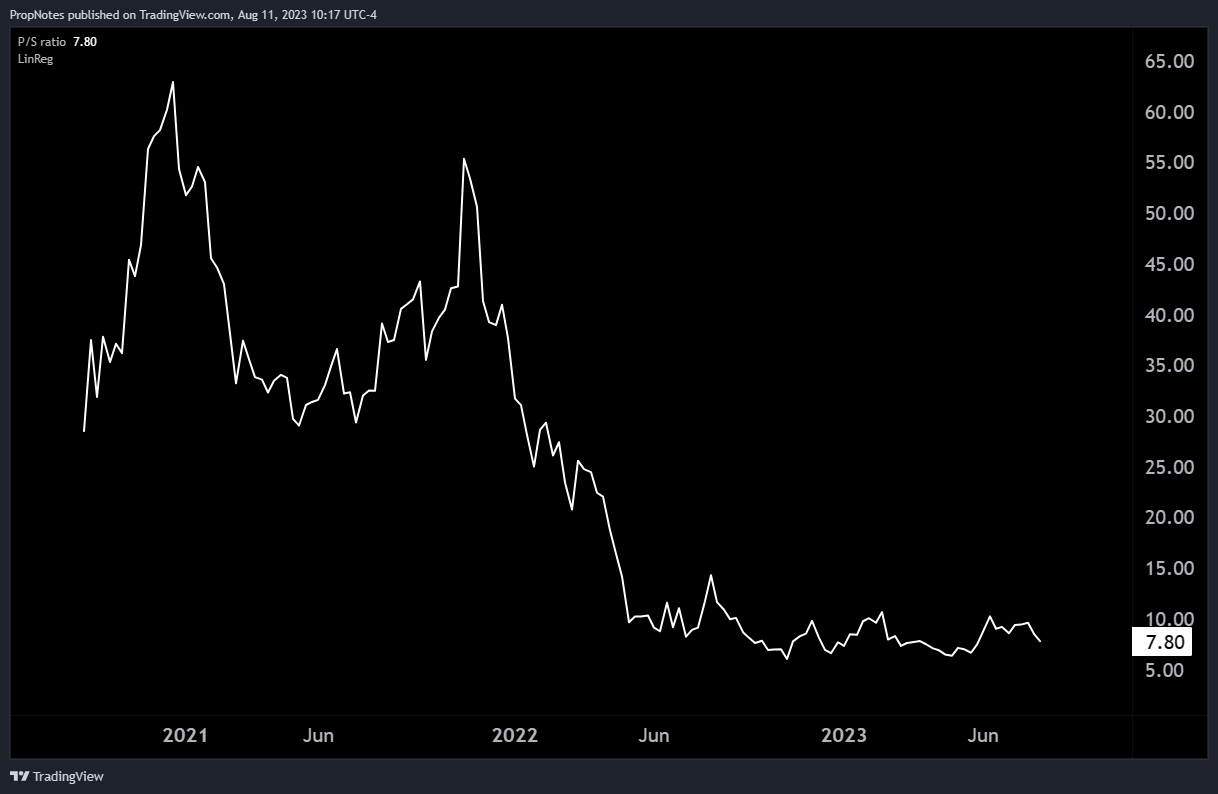

We anticipate that there’s significant room for the share price to move north, especially given the current sales valuation:

TradingView

If Unity even recaptured a quarter of its previous valuation at 60x sales, (15x), then the stock could more than double from here, something we think is highly feasible, especially given the prospect for potential profitability, and the high, triggerable short float.

Risks

The main risk to this story would be Apple supporting another 3D development product, like Unreal Engine, in the Vision Pro at some point in the future.

Right now, Vision Pro is only launching with Unity as a partner, but there’s nothing stopping the company from adding more natively supported engines in the future.

It’s likely that Apple chose Unity instead of Unreal Engine as Unreal Engine is owned and operated by Epic Games, which Apple has been clashing with legally for some time.

That said, if the two companies mend fences, or Godot, another up and coming platform, gets integrated, then the competitive advantage dissipates.

Summary

Unity is poised to become an industry leader in the metaverse. The company’s platform is already the most popular for creating immersive experiences, and its inclusion in the Vision Pro headset will only solidify Unity’s position.

Unity is well-positioned to capitalize on the growth of the mixed reality and become the leader in its industry.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in U over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.