Summary:

- Arrival has failed with its attempt to merge with a second blank check firm to raise $238 million.

- The EV upstart has hired advisors for a potential bankruptcy filing. This could come as soon as next month.

- Cash of $130 million as of the end of March has likely been cut in half, with the company faced with a few months of cash runway left.

CASEZY/iStock via Getty Images

Arrival (NASDAQ:ARVL) is likely to file for bankruptcy before the end of astronomical summer, with the EV upstart recently hiring turnaround advisor Alvarez & Marsal to draft contingency plans for a bankruptcy filing as attempts to raise more external capital flounders. A possible filing would add Arrival to a slowly expanding list of EV deSPACs that have collapsed. Proterra was the latest in a tally that includes Lordstown Motors (OTC:RIDEQ) and Electric Last Mile Solutions (OTC:ELMSQ). Further, Arrival’s plan to engineer a second merger with blank check company Kensington Capital Acquisition Corp. V (KCGI) was scrapped. The deal would have been unique if executed and allowed Arrival to access as much as $238 million of cash held in Kensington’s trust.

The failure of the reSPAC transaction and the hiring of external advisors when aggregated with a still difficult macroeconomic backdrop for fundraising and Arrival’s abnormal cash burn profile infer continued near-term headwinds. The best-case scenario, though unlikely, would be for Arrival to be acquired by a larger firm looking to gain access to the company’s unique microfactory concept and IP. However, this is unlikely with Arrival yet to have brought a product to market and against the company’s outsized losses. Critically, the somewhat out-of-the-blue collapse of electric bus maker Proterra has highlighted the difficulty of finding buyers for loss-making EV operations. Proterra, once the poster child for the electrification of the transit bus, spoke to 26 potential buyers but failed to get the backing of a single one.

Modular Microfactory Concept Set To Turn Dark

What’s the key takeaway for current shareholders? That 2023 has seen two EV companies collapse against a Fed funds rate that has just been hiked to a 22-year-high. Arrival has held off on updating its shareholders on its financials in a timely manner with a Form 6-K filed with the SEC in July announcing that Nasdaq had granted the company an extension to the deadline to file its annual report for the fiscal year ended December 31, 2022. The company now has until October 30, 2023, to file its 2022 annual report or face being delisted from the Nasdaq after an earlier 1 for 50 reverse stock split in April brought the company back into compliance with minimum list requirements.

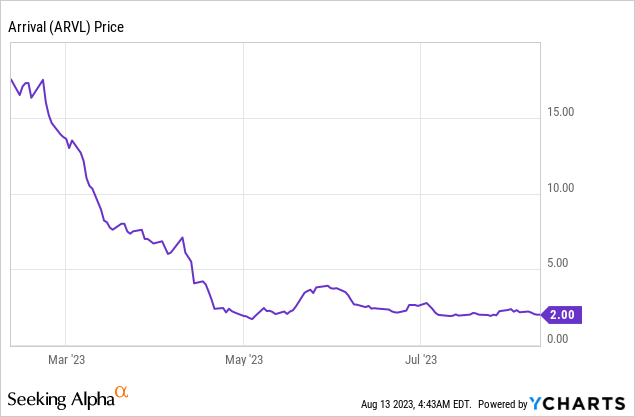

On the back of the hiring of external advisors, it’s unlikely Arrival will be able to maintain operations for the three months until the new deadline date. Hence, the May update on cash and operations could be the last. The company held cash and equivalents of $130 million as of the end of March, a decline from cash and equivalents of $601 million when the company started trading on the Nasdaq back in the spring of 2021 through a combination with CIIG Merger Corp. The company’s microfactories were meant to be a small and low-cost modular approach to EV construction. This should have been reflected as smaller cash outflows and a more constrained operational cost base.

Arrival was aiming to still be able to pump out at least 10,000 of its Class 4 delivery vans annually to sell to a customer base that includes United Parcel Service (UPS). The company has used up 80% of its Spring 2021 cash position, with a monthly cash burn rate running at around $20 million. This figure does not include the burn of other injections of external capital since the company went public. Arrival was able to raise $50 million in equity capital from Antara Capital earlier this year in February. The company has also been exchanging debt held by Antara for equity and most recently swapped $20 million of a 3.50% convertible note due in 2026 for 3.02 million of its ordinary shares.

A Filing Could Be Made Before The End Of The Summer

Arrival has been fighting to remain a going concern. According to LinkedIn it currently employs at least 1,068 employees across its UK and US locations, upping the stakes to find a salvo. Is an eleventh-hour solution possible? I don’t think so. The situation could have been different if capital had not been so expensive. Further, Arrival held debt of at least $300 million as of the end of June. This was all owned by Antara who has been willing to convert it to equity, but Arrival’s current market cap makes any further conversion a more difficult undertaking and would imply a near 10x rate of dilution.

Further, if Antara were to extinguish the debt in a deal to avert bankruptcy, Arrival’s core headwind still remains to find external capital to fund its operations. The company has likely used more than half of its end-of-March 2023 cash position and faces a liquidity position unable to fund another three months of operations. Against this, current shareholders should close out their position, with Arrival likely set to stage a move to over-the-counter trading on a bankruptcy filing.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.