Summary:

- Bank of America has reduced its consumer credit card exposure.

- However, Bank of America has significantly increased its exposure to commercial lending.

- It’s time you do appropriate due diligence on banks that are housing your hard-earned money.

MCCAIG

Bank of America (NYSE:BAC) has recently published its 4Q23 results. In the presentation deck, there was a slide on which the bank was showing that it had significantly improved its balance sheet since 4Q09. While some areas were indeed improved, there are a lot of issues that could lead to much worse consequences for BAC, compared to the Great Recession, should a major crisis arise.

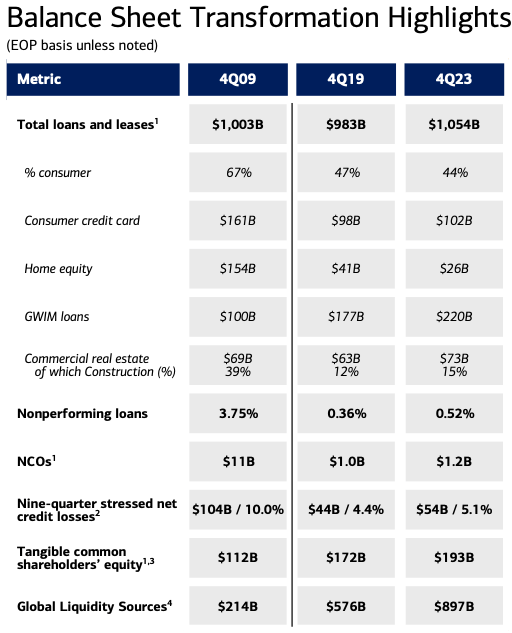

So, here is the slide we are talking about.

Company Data

Debate #1: Does BAC’s credit card business look much better now?

As we can see above, BAC’s consumer credit card portfolio indeed decreased quite significantly, from $161B in 4Q19 to $102B in 4Q23. With that being said, the quality of this lending segment is deteriorating quite rapidly and is likely to become a major issue for BAC soon.

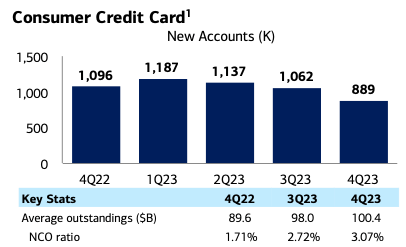

Company Data

The chart above shows that the segment’s NCO (net charge-off) ratio was 3.07% in 4Q23, up from 1.71% in 4Q22. This is quite a notable increase. We have written a lot of articles on unsecured credit space in the U.S., and for those who follow our banking work, it should not be a surprise that this lending segment is in a challenging situation.

For FY 2009, BAC’s NCO ratio was 11.25%. If we apply this ratio to BAC’s current credit card portfolio, that would result in $11B in losses for the bank.

Debate #2: Did a massive increase in commercial lending make BAC’s balance sheet safer?

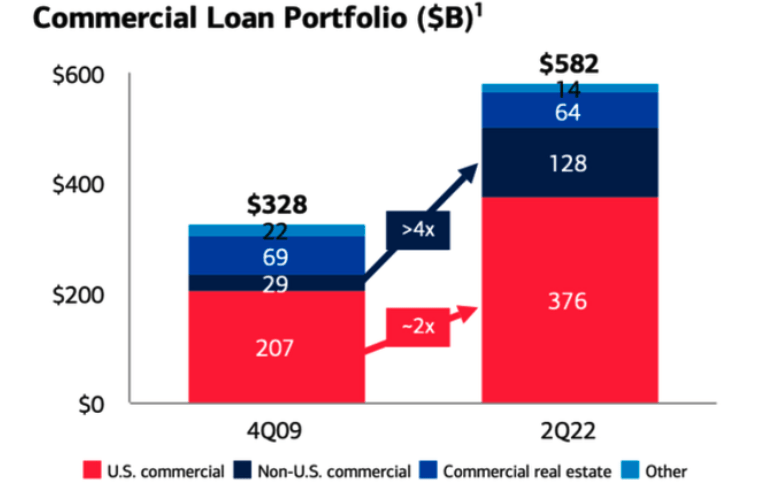

Here’s the chart from one of our previous articles on BAC. As you can see, the bank’s U.S. commercial loan portfolio almost doubled over the period of 4Q09-2Q22.

Company Data

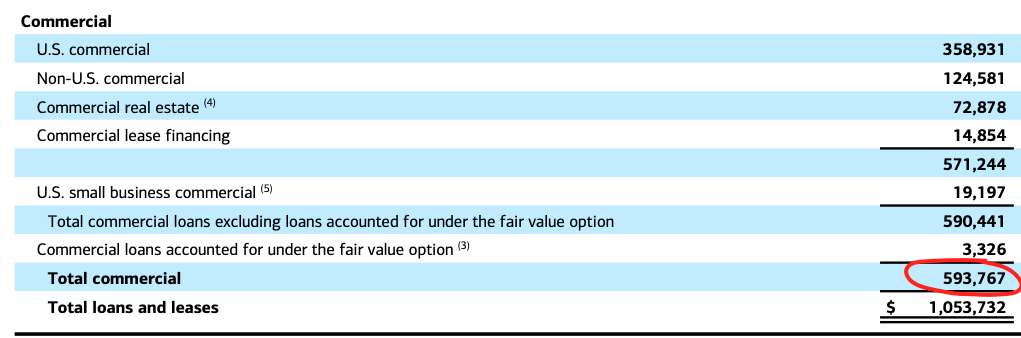

According to the bank’s 4Q23 numbers, its total commercial loan book, including commercial lease financing, has reached almost $594B, which accounts for 56% of the bank’s total outstanding loans.

Company Data

We have been warning about a challenging environment in the commercial lending space for more than 18 months, and the recent data confirms our views.

First, according to Epiq Bankruptcy, a provider of U.S. bankruptcy filing data, commercial Chapter 11 filings increased 72% to 6,569 in 2023 from the previous year’s total of 3,819. The data implies that we’re already seeing a large increase in corporate defaults.

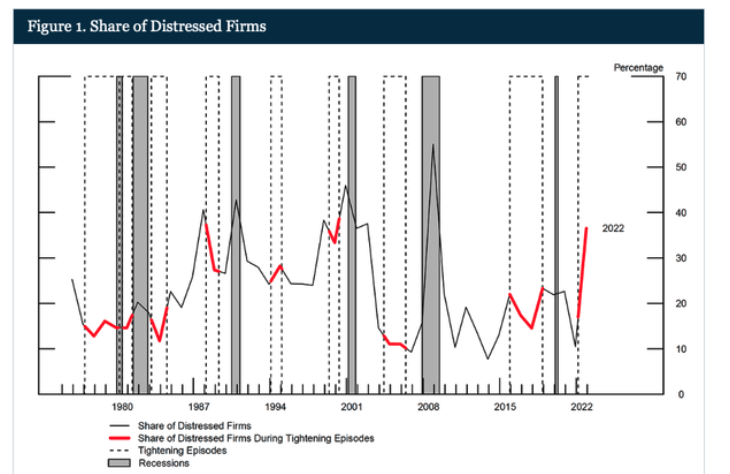

Second, the Fed has recently published a paper saying that the share of non-financial firms in financial distress in the U.S. economy has reached 37%. Importantly, this level is higher than during most previous tightening episodes since the 1970s.

The Fed

Third, the researchers from USC, Columbia, Stanford, and Northwestern have estimated that the U.S. banking industry could face a range of 10% to 20% default rates on CRE loans, i.e., levels that are comparable to or even higher than those seen during the Great Recession. A 20% default rate would result in almost $16B in losses for BAC from its CRE portfolio alone.

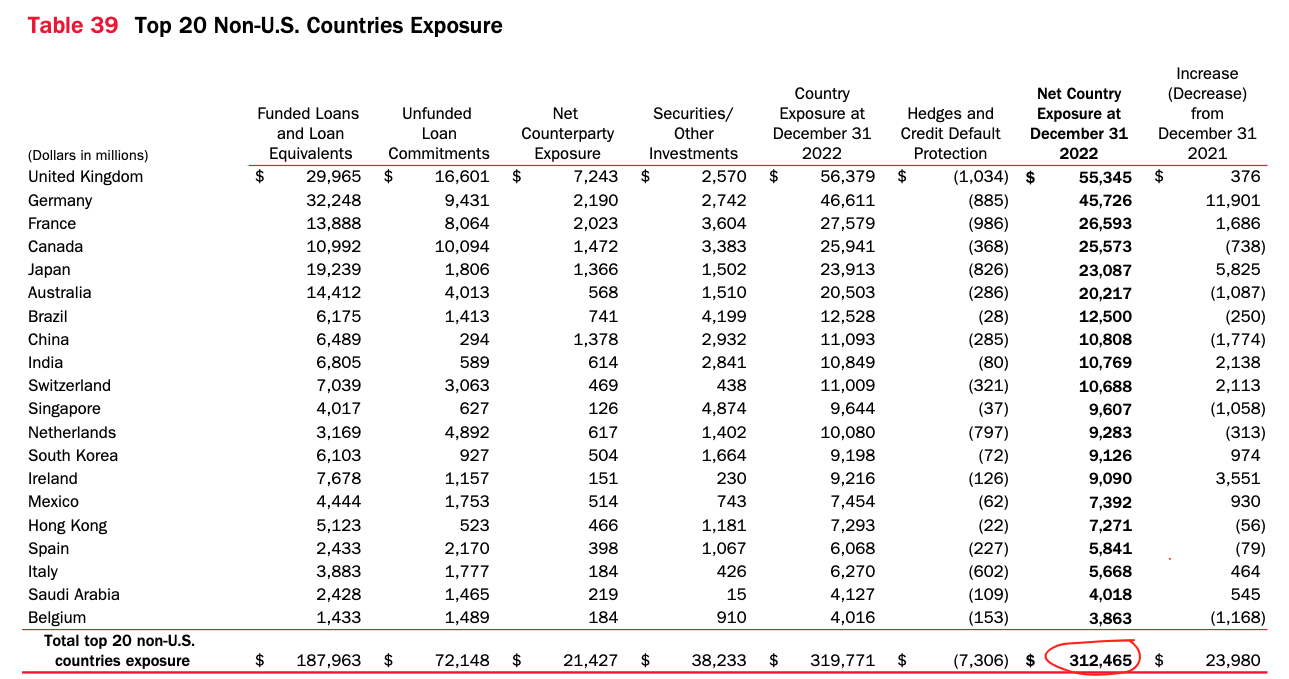

Lastly, it’s important to note that as of FY2023, BAC had $125B of non-US commercial loans. By comparison, it had just $29B of these loans in 4Q09. The bank’s latest 10-K shows that total non-U.S. exposure is much higher at $312B.

Company Data

Here’s what the bank says about its non-U.S. exposure:

Our non-U.S. credit and trading portfolios are subject to country risk. We define country risk as the risk of loss from unfavorable economic and political conditions, currency fluctuations, social instability and changes in government policies…

This suggests that these loans and other commitments are subject to not only credit risks but also FX risks and other sovereign risks as well. The top three non-U.S. country exposure were the UK, Germany, and France. The macroeconomic indicators clearly show that both Britain and Europe are performing worse than the U.S. economy. Importantly, this performance gap is very likely to become wider if a major crisis comes.

To sum up, a massive increase in BAC’s commercial lending does not look like an improvement to the balance sheet. In fact, the bank’s decision to grow its commercial loan book could turn out to be a major strategic mistake.

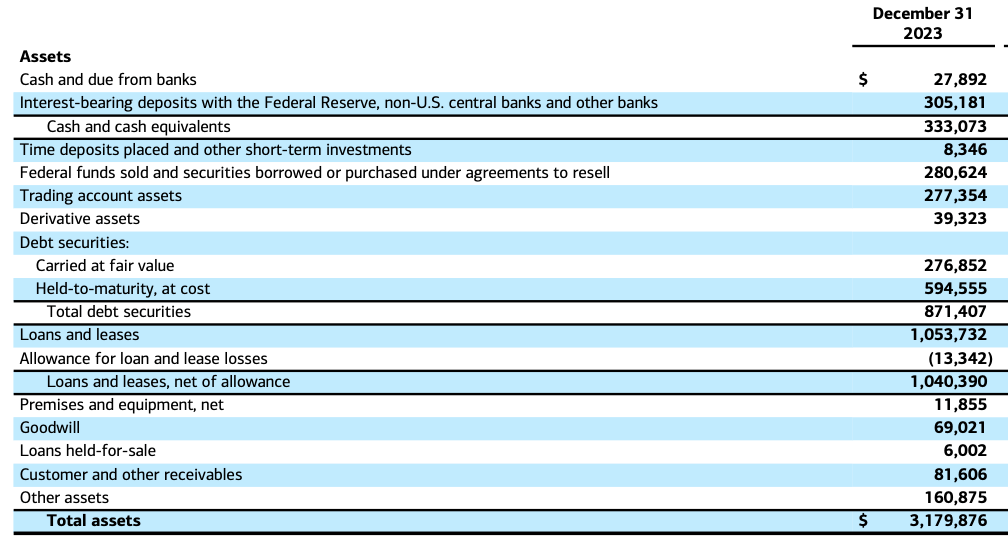

Debate #3: Does BAC really have almost $900B of liquidity on its balance sheet?

In its presentation, BAC says that it has $897B in liquidity sources. At first glance, that does sound really impressive. However, a deeper look at the bank’s balance sheet tells us a different story.

Company Data

The bank’s asset breakdown shows that cash and cash equivalents accounted for $333 billion as of FY2023, which is much less than $897B. That suggests that BAC also includes securities on its balance sheet to liquid assets. However, it’s well known that BAC has securities with very long maturities, and those securities can be sold only at huge losses. The inclusion of long-duration securities in liquid assets looks very questionable, to put it mildly.

Debate #4: Does the Fed’s stress test guarantee that BAC is prepared for a crisis?

We have written a lot about why the Fed’s stress tests do not reflect how the actual financial conditions of U.S. banks would look under a sharp recession scenario. But last year’s tests look really odd.

On July 3, Bank of America issued quite a surprising statement, saying that “Bank of America initiated dialogue with the Federal Reserve to understand differences in Other Comprehensive Income over the 9-quarter stress period between the Federal Reserve’s CCAR results and Bank of America’s Dodd-Frank Act stress test results.”

There were several significant discrepancies between the Fed’s tests and BAC’s own tests. First, BAC’s internal stress test shows that the bank would post a loss of $52.2B under the severely adverse scenario, while the Fed expects the bank to lose only $23.0B. Second, BAC estimates that its other comprehensive income would be $12.5B, while the Fed’s tests show it would be $22.3B. Due to a combination of a bigger loss and lower other comprehensive income, BAC expects its CET1 capital ratio to fall to 8.3%, while the Fed said the ratio would decline to 10.6%.

As we said earlier, it looks odd. This implies that the Fed is much less conservative than the banks that it regulates. Needless to say, a banking regulator should be as conservative as possible in such an important exercise as a stress test. At the end of the day, the results of these tests are used to determine how much capital the banks need.

Obviously, this makes many question the reliability of the Fed’s tests.

The Bottom Line

As our analysis shows, only some areas of BAC’s balance sheet have improved since 4Q09, while others have deteriorated significantly. As such, it’s wrong to say that BAC’s balance sheet and its overall business model are better prepared for a crisis compared to the pre-Great Recession period.

We did not discuss all the problems that BAC has, but even the issues we have mentioned could eat up the bank’s capital quite quickly if a major systemic crisis comes to pass.

I want to take this opportunity to remind you that we have reviewed many larger banks in our public articles. But I must warn you that BAC is not alone regarding major concerning issues sitting on the balance sheets of those banks. The substance of our analysis suggests that the future is not looking too good for the larger banks in the United States, details for which are here.

Moreover, if you believe that the banking issues have been addressed, I’m sorry to inform you that you likely only saw the tip of the iceberg. We were able to identify the exact reasons in our public article which caused SVB to fail, well before anyone even considered these issues. And I can assure you that they have not been resolved. It’s now only a matter of time.

At the end of the day, we’re speaking of protecting your hard-earned money. Therefore, it behooves you to engage in due diligence regarding the banks which currently house your money.

You have a responsibility to yourself and your family to make sure your money resides in only the safest of institutions. And if you’re relying on the FDIC, I suggest you read our prior articles, which outline why such reliance will not be as prudent as you may believe in the coming years.

It’s time for you to do a deep dive on the banks that house your hard-earned money in order to determine whether your bank is truly solid or not. For those looking for a due diligence methodology, our due diligence methodology is outlined here.

Housekeeping Matters

This article, as well as Saferbankingresearch.com, is a combination of efforts between Avi Gilburt and Renaissance Research, which has been covering U.S., European, LatAm, and CEEMEA banking stocks for more than 15 years.

If you would like notifications as to when my new articles are published, please hit the button at the bottom of the page to “Follow” me.

Also, for those that are questioning why all comments (including mine) go through moderation, you can read here: Haters Are Gonna Hate – Until They Learn.

Lastly, I have asked the editors to close the comments section, as I will be out until the 5th of February.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

THE #1 SERVICE FOR MARKET & METALS DIRECTION!

“I enjoy sleeping well at night knowing my money is safe”

“A colleague said “no one saw this issue with the banks.” I just laughed and said that “Avi from EWT was all over it.””

“Thanks for giving a balanced view that so many other services do not. Wish I had joined sooner. You would have saved me a ton of $$.”