Summary:

- Block’s Q1 was the company’s best quarter ever.

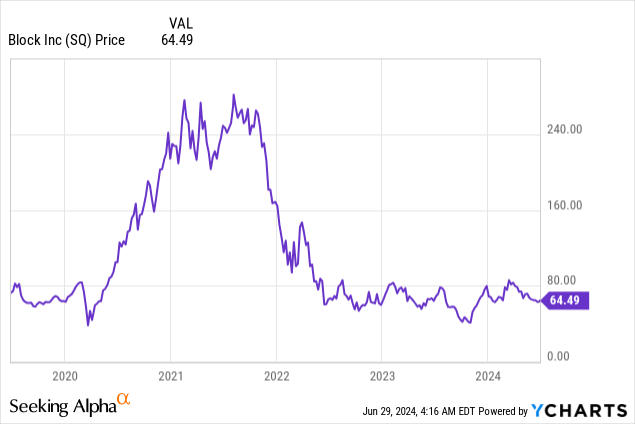

- Yet, the stock is down 11% YTD and 75% from all-time highs — it looks like dead money.

- Despite the negativity, I believe the stock offers long-term investors compelling value.

- I highlight seven reasons why.

sasha85ru

Introduction

Block (NYSE:SQ) — the parent company of Square, Cash App, and Afterpay — is down 11% YTD and 75%+ from its all-time highs of nearly $300.

Just by looking at Block’s price chart, one might think that Block is facing an existential crisis with the stock possibly heading lower and lower over time.

Despite the constant negativity on the stock, I argue that now is one of, if not, the best time to buy Block stock. The company is much larger and more profitable than ever before, and yet, the stock is trading at the same level that it was six years ago.

That said, here are seven reasons why Block stock is a buy today.

As a disclosure, I do not have a position in SQ. However, I have some exposure to the stock through my investment in Marqeta (MQ), which powers the Square Debit Card, Cash App Card, and Afterpay’s BNPL offering.

Reason #1: Square’s Strong Monetization

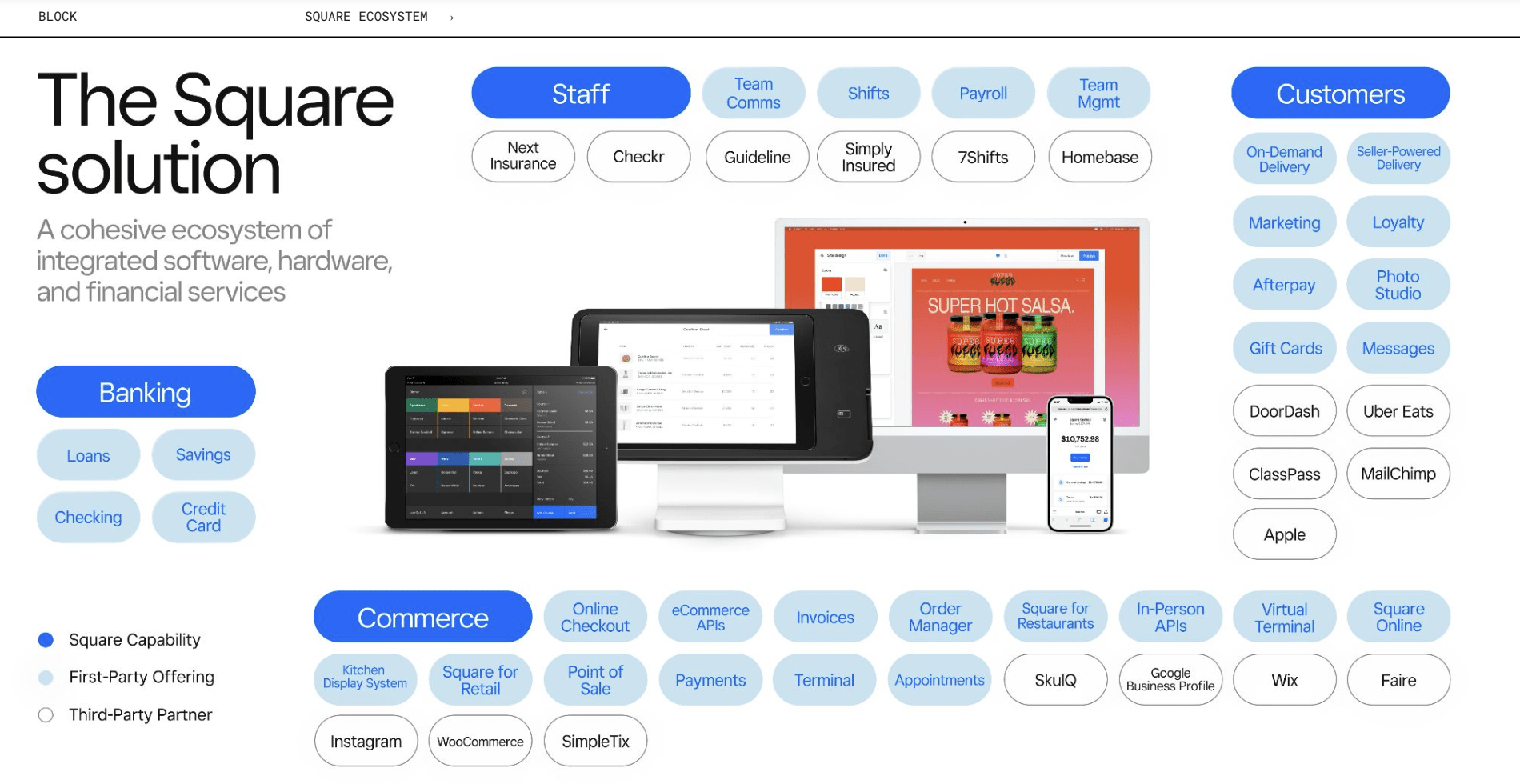

The Square platform is Block’s flagship ecosystem, offering businesses (or Sellers management calls them) payment processing, digital banking, workforce management, customer relationship management, and e-commerce solutions, all in a single platform.

Block FY2024 Q1 Investor Presentation

In Q1, Square generated $1.7B of revenue, up only 11% YoY. For context, growth has stabilized in the 10% to 13% range over the last six quarters as the business matures.

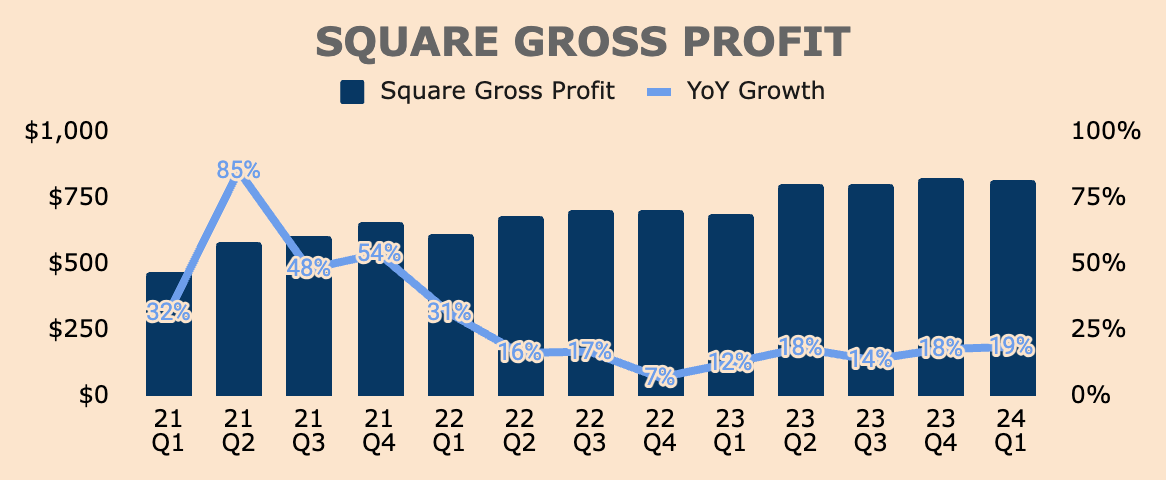

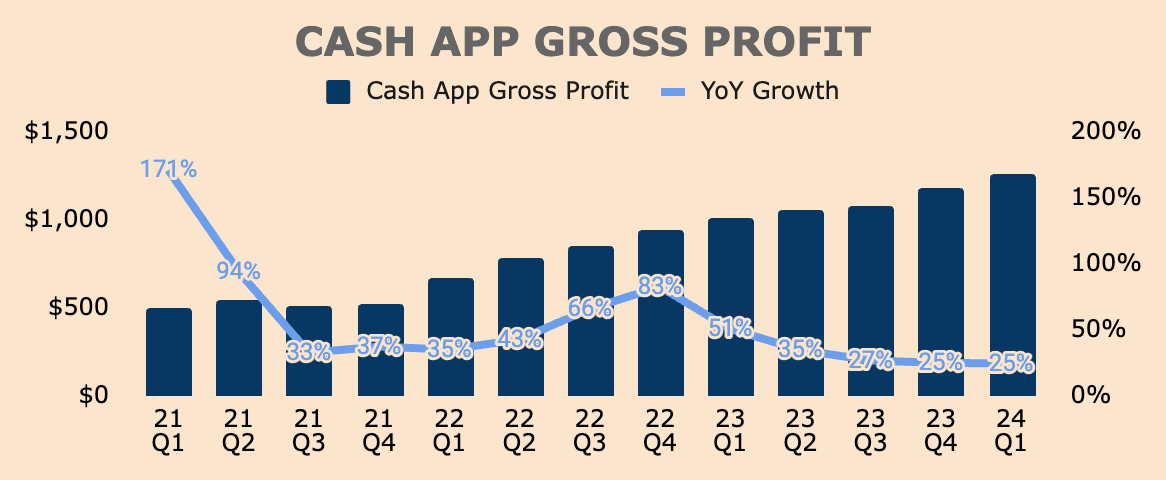

A more important metric to track is Gross Profit, which shows how well Square can extract value from its Sellers. In Q1, Square Gross Profit was $820M, up 19% YoY, significantly higher than Revenue growth.

Author’s Analysis

Not long ago, Square was highly criticized for its inability to monetize its Sellers effectively. For instance, Square saw Gross Profit growth below that of Revenue growth from Q1 of 2022 to Q1 of 2023, implying worsening economics.

However, beginning Q2 of 2023, Square was able to generate higher Gross Profit growth relative to Revenue growth for four consecutive quarters, showing improved monetization. This is important because it shows that Square can extract more value from its Seller base, ultimately leading to higher earnings potential for investors.

Strong Gross Profit growth was mainly driven by:

- a 17% YoY growth in software and integrated payments.

- a 24% YoY growth in vertical point-of-sale solutions (like Square Appointments and Square for Retail).

- a 36% YoY growth in banking products (like Square Loans and Square Debit Card).

- a 38% YoY growth in international Gross Profit with international Gross Payment Volume up 26% YoY.

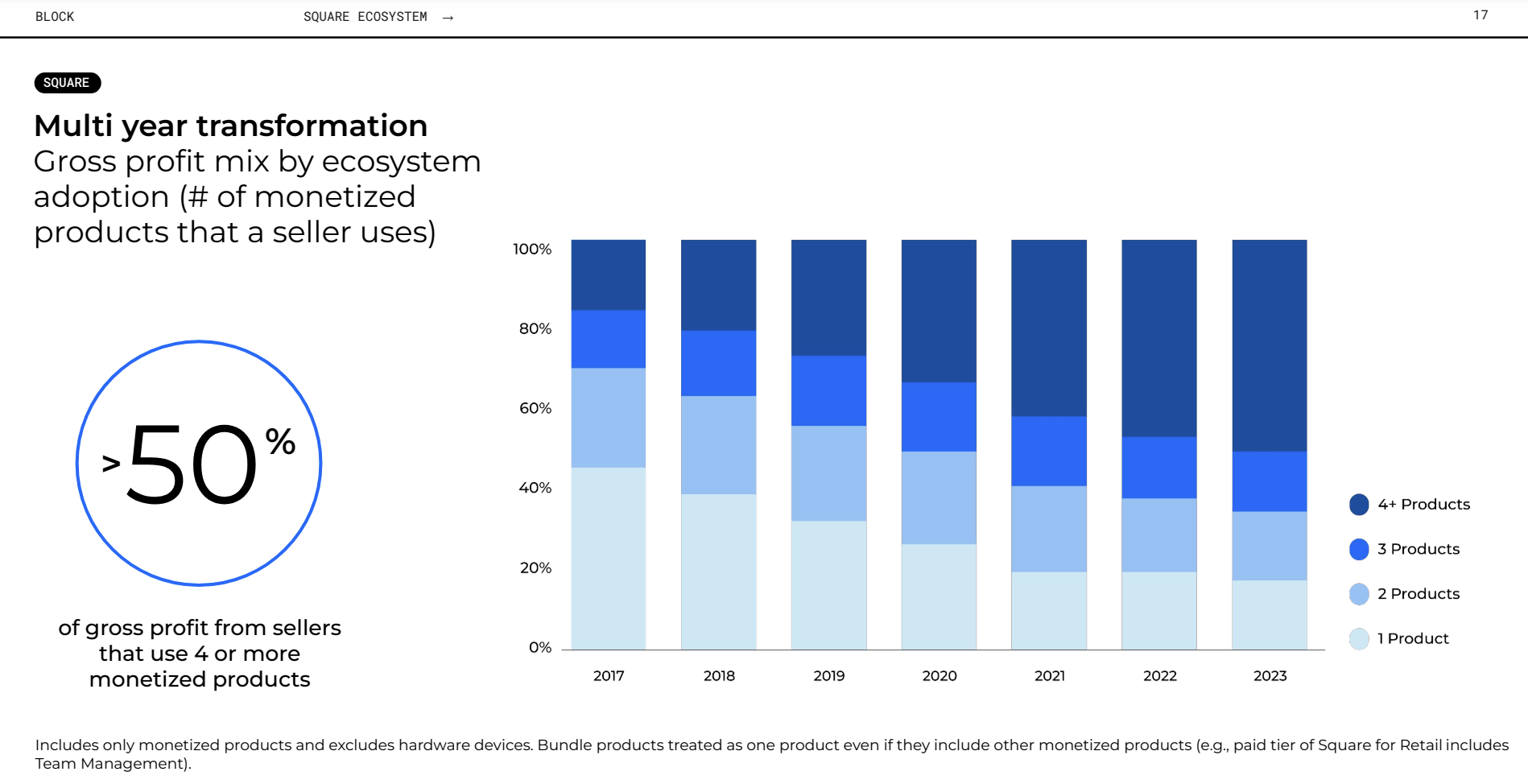

All that said, strong monetization has a hidden benefit for Square. For one, it means that Sellers are increasingly using more of Square’s products, which subsequently amplifies Square’s switching costs moat and Gross Profit retention. As you can see below, more than half of Square’s Gross Profit was generated by Sellers that use 4+ products.

As Square maintains strong monetization, we can expect higher-quality Revenue and earnings moving forward.

Block FY2024 Q1 Investor Presentation

Reason #2: Cash App’s Dominance

On the consumer side of the Block ecosystem, Cash App offers consumers digital financial services such as P2P payments, digital banking, and stock and Bitcoin investing. It is one of, if not, the largest financial app (based on the number of users) in the United States — as of this writing, Cash App is #1 in the Finance category in the Apple App Store.

And it is not done yet.

Block FY2024 Q1 Investor Presentation

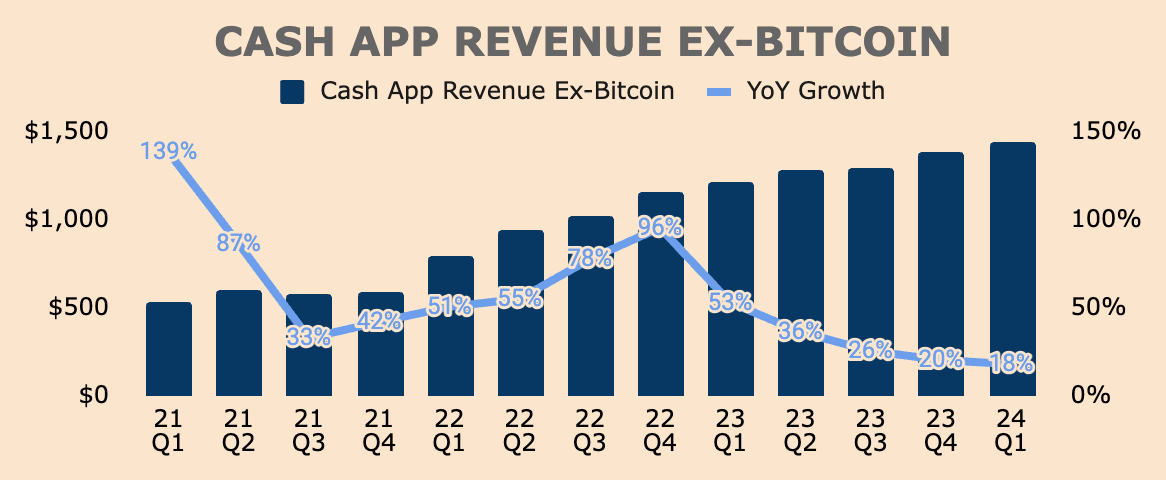

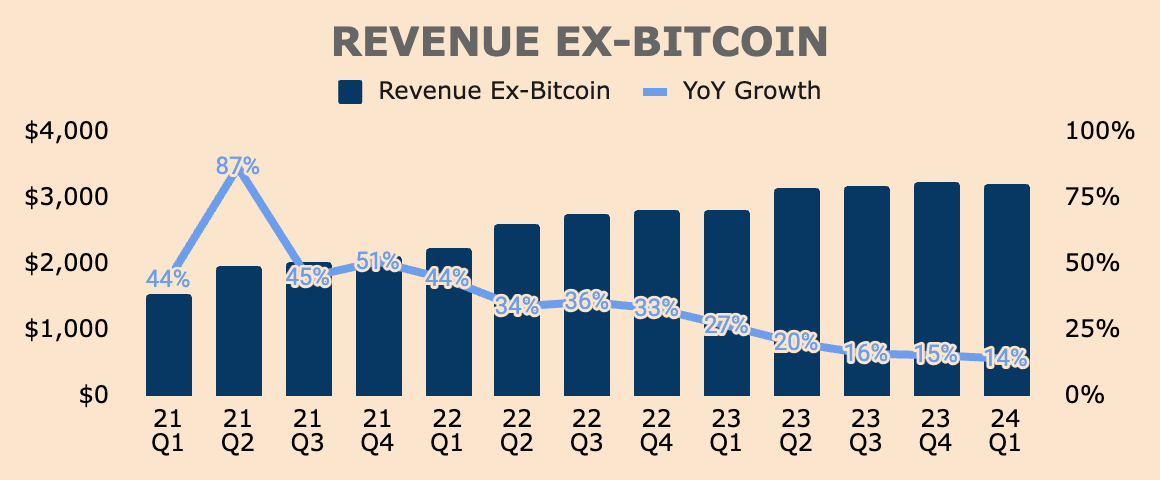

In Q1, Cash App generated $4.2B of Revenue, up 23% YoY. Excluding Bitcoin Revenue, Cash App Revenue Ex-Bitcoin was $1.4B, up 18% YoY.

As you can see, growth has been slowing down over the last few quarters. This is due to the Afterpay acquisition back in Q1 of 2022, which saw a surge in growth rates throughout 2022. Keep in mind that Afterpay Revenue is now fully embedded under Cash App.

Entering 2023, Cash App growth rates declined as it faced tough YoY comps due to the Afterpay acquisition.

Regardless, Cash App Ex-Bitcoin, continues to generate record Revenues, demonstrating its continued virality and dominance.

Author’s Analysis

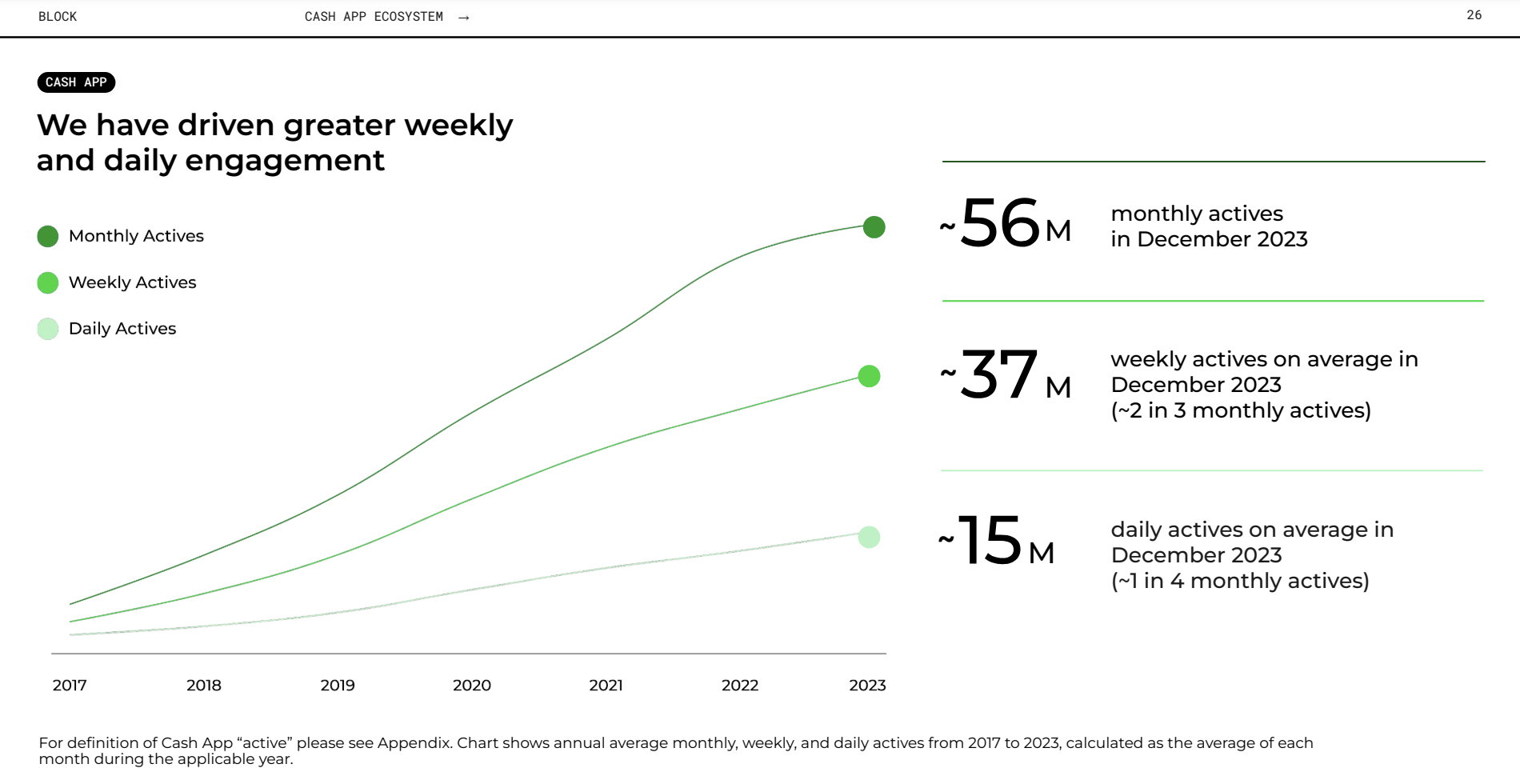

This is further backed by its growing user base with 57M Monthly Actives as of March, up 6% YoY. To put that into perspective, that is about 17% of the US population.

What’s more, Cash App continues to see high — and improving — engagement rates with 37M Weekly Actives and 15M Daily Actives.

Block FY2024 Q1 Investor Presentation

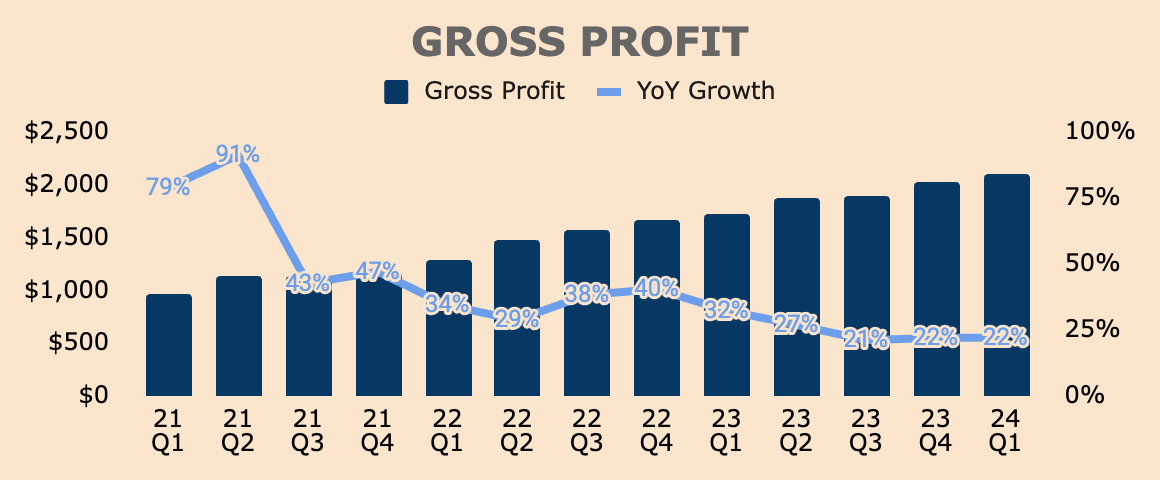

Q1 Overall Inflows were $71B, up 17% YoY and 12% QoQ. Inflows Per Active was $1,255, up 11% YoY and 10% QoQ. As more money flows into the Cash App ecosystem, Cash App has the opportunity to monetize these inflows. As of Q1, Cash App’s Monetization Rate was 1.48%, up 7bps YoY.

As a result of higher Actives, Inflows, and Monetization Rates, Cash App produced $1.3B of Gross Profit in Q1, up 25% YoY, which, if you haven’t noticed, is much higher than Cash App Revenue Ex-Bitcoin growth of 18%.

Author’s Analysis

Similar to the Square ecosystem, this is the third consecutive quarter of higher Cash App Gross Profit growth versus Revenue Ex-Bitcoin growth, implying strong monetization trends.

Strong Cash App Gross Profit growth was driven by:

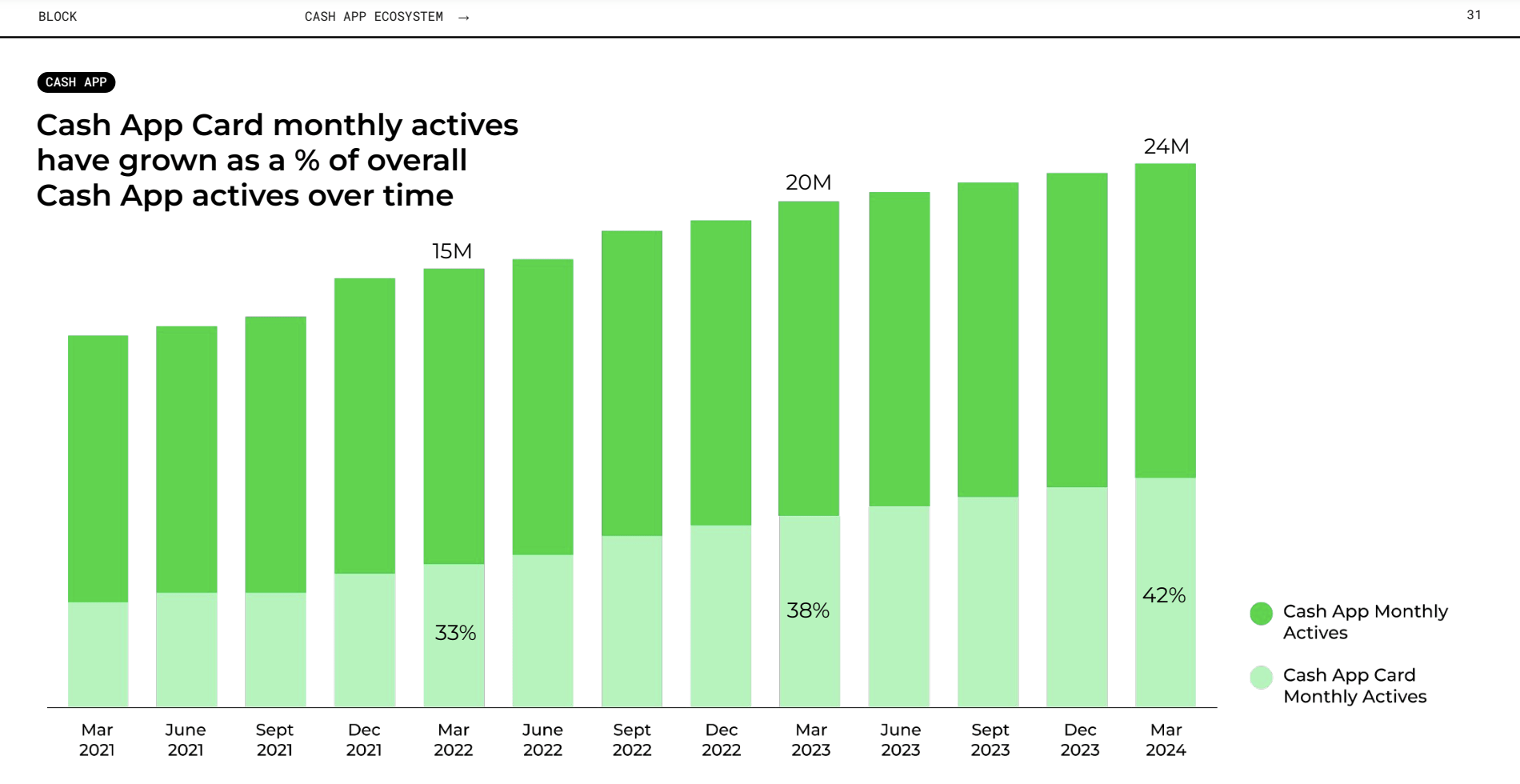

- a 16% YoY increase in Cash App Card monthly actives, to 24M, making up 42% of Cash App monthly actives, up from 38% a year ago.

- a 25% YoY growth in BNPL GMV, to $7B. Management continues to integrate Afterpay into Cash App. For example, management is testing Afterpay’s BNPL offering through the Cash App Card, in exchange for a small fee, which could drive incremental GMV volume and Revenue growth.

- a 59% YoY growth in Bitcoin Gross Profit, to $80M.

- a 40% QoQ growth in Cash App Pay volume.

- higher Cash App Borrow volumes.

Block FY2024 Q1 Investor Presentation

Of important note, Cash App delivered all this growth while cutting Cash App Marketing Expenses by 18% YoY. This just reflects Cash App’s unique value proposition and dominance.

Above all, a growing user base and higher engagement rates present a great opportunity for Cash App to further monetize its ecosystem. By pushing greater product adoption, Cash App will inevitably attract greater inflows, and thus, monetization, which would enhance Cash App’s earnings potential, rewarding shareholders in the long run.

Block FY2024 Q1 Investor Presentation

Reason #3: Low Market Penetration

In Q1, Block Revenue was $6.0B, up 19% YoY, beating analyst estimates by $140M. This included Bitcoin Revenue — Revenue Ex-Bitcoin was $3.2B, up 14% YoY.

Author’s Analysis

Total Gross Profit was $2.1B, up 22% YoY, beating internal guidance by nearly $0.1B.

Author’s Analysis

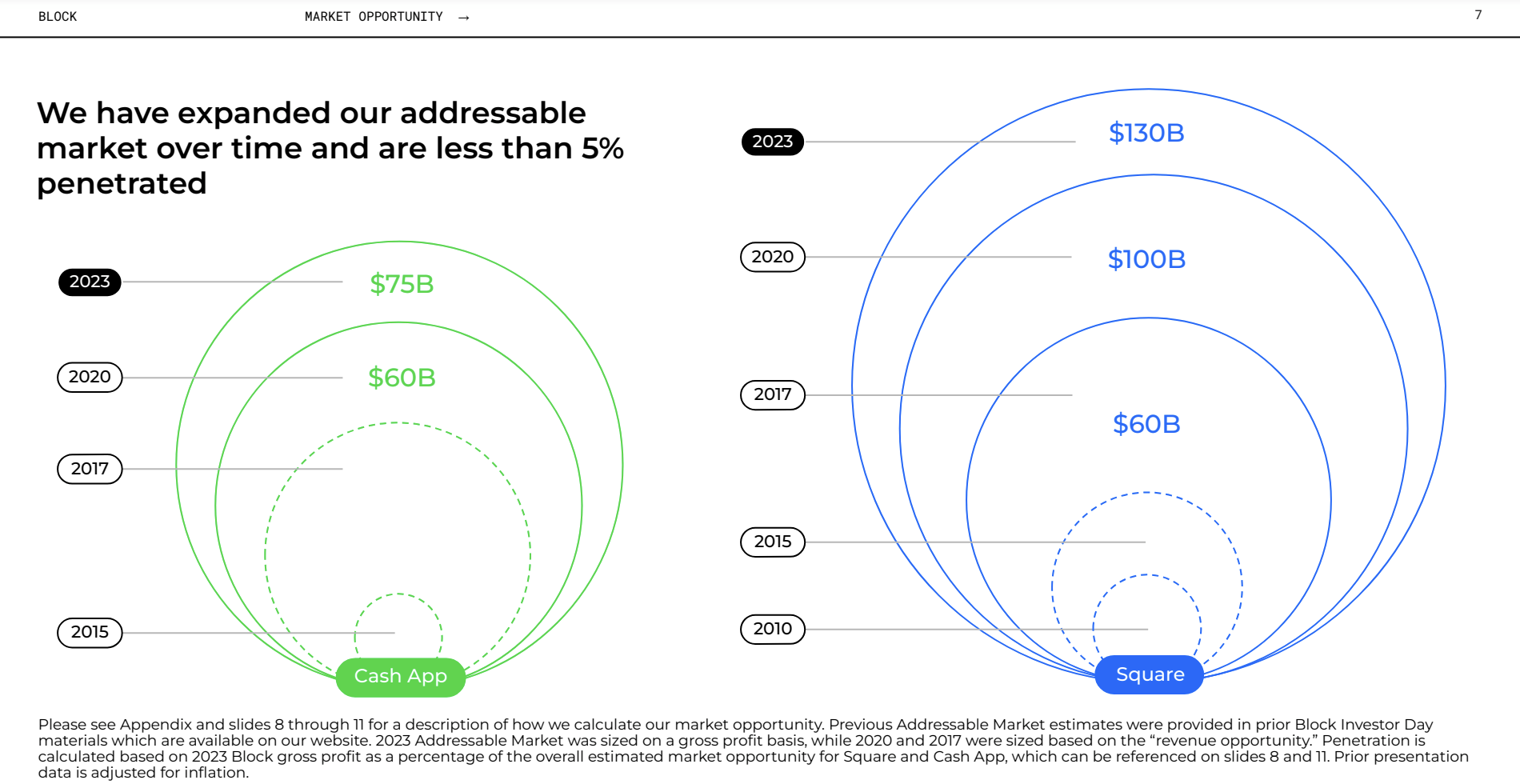

Despite the slowdown in Revenue and Gross Profit growth, Block still has a long growth runway in the emerging fintech industry. As you can see below, Cash App and Square have a total addressable market of $75B and $130B, respectively, with less than 5% market penetration.

The combination of a large TAM and low penetration rate should serve as a tailwind for growth in the next decade or so. This is especially true given Block’s strong brand, large scale, and high switching cost moats.

Block FY2024 Q1 Investor Presentation

Here are some examples that could drive growth in the next few years:

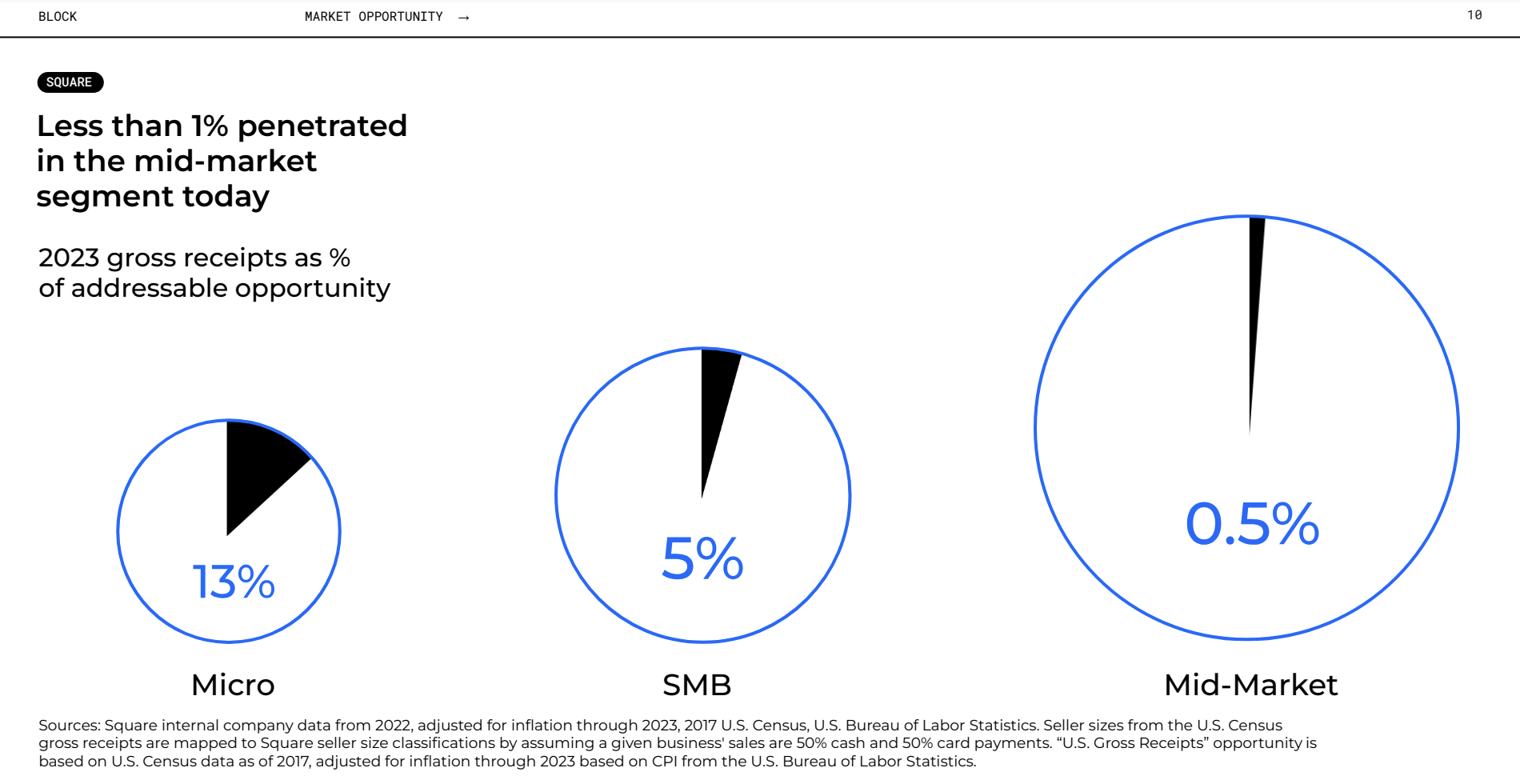

- Block still has a small presence in international markets. For instance, despite growing 38% YoY, Square International Gross Profit only makes up 13% of Block’s Total Gross Profit and is less than 1% penetrated against its TAM.

- Block also has a substantial opportunity in the mid-market segment. As you know, Square is widely used among mom-and-pop stores and SMBs, with a penetration rate of 13% and 5%, respectively. On the other hand, Square only has a 0.5% penetration rate among the mid-market segment.

- Global remittance is an $860B industry with little to no innovation. That is why Block is tapping into this market through its subsidiary, TBD, and is expected to launch its first remittance product in the back half of the year.

Block FY2024 Q1 Investor Presentation

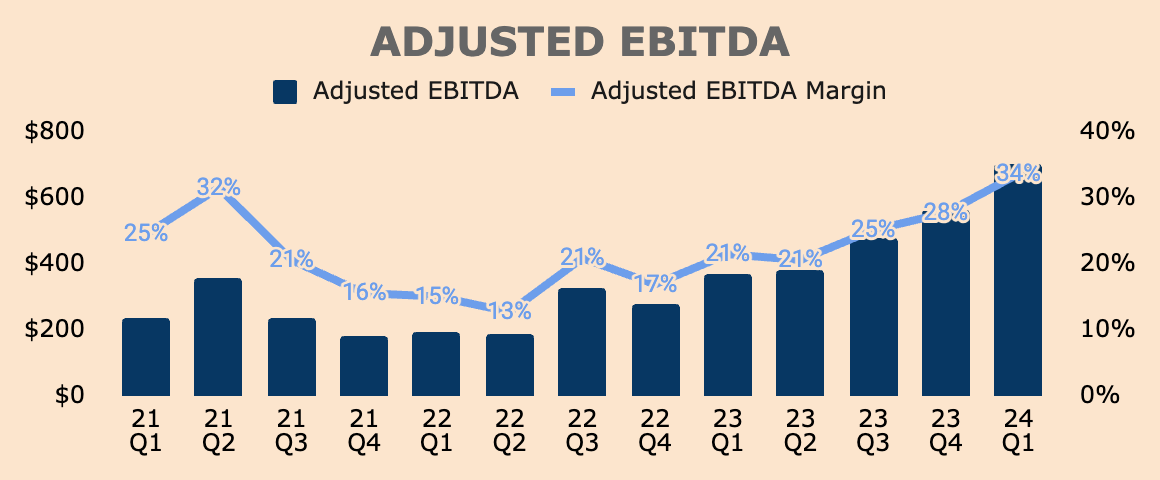

Reason #4: Operating Leverage

In terms of profitability, Block had its best quarter ever, generating record numbers across all profit metrics. Note that, when calculating profit margins, Block uses Gross Profit, instead of Revenue, as the denominator.

- Operating Income was $250M, which is a 12% Margin, expanding 1,200bps YoY.

- Adjusted Operating Income was $364M, which is a 17% Margin, expanding 1,400bps YoY.

- Net Income was $472M, which is a 23% Margin, expanding 1,700bps YoY.

- Adjusted Net Income was $543M, which is a 26% Margin, expanding 1,000bps YoY.

- Adjusted EBITDA was $705M, which is a 34% Margin, expanding 1,300bps YoY.

Author’s Analysis

Without a doubt, Block is demonstrating strong operating leverage across its ecosystem of ecosystems, mainly due to ecosystem growth and its 12,000-employee cap.

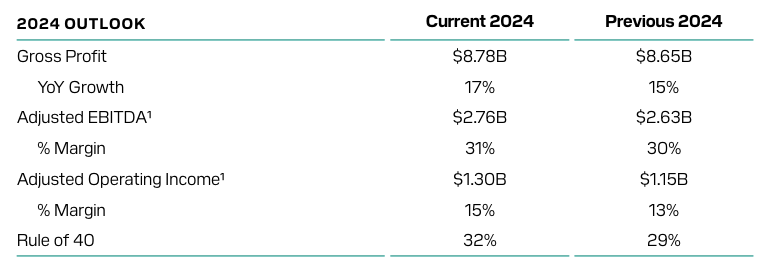

Despite major improvements in profitability, management expects the trend to continue, pointing to higher profit margins over time.

We believe we can continue to drive profitability by leveraging our scale to improve our cost structure across a range of different expense areas, and utilizing AI and automation.

This is also why management is raising their profit guidance for the year. For the full-year 2024, management expects:

- Gross Profit of $8.78B, up 17% YoY, an improvement from 15% YoY growth in its prior guidance.

- Adjusted Operating Income of $1.30B, which is a 15% Margin, up from its prior guidance of 13%.

- Adjusted EBITDA of $2.76B, which is a 31% Margin, up from its prior guidance of 30%.

- This will result a Rule of 32, up from its prior guidance of 29%. Management also reiterated Rule of 40 by 2026.

Raised guidance means a variety of positive things, including high ecosystem engagement, market share expansion, as well as ongoing operating leverage. Such strong business momentum shouldn’t be overlooked.

Block FY2024 Q1 Shareholder Letter

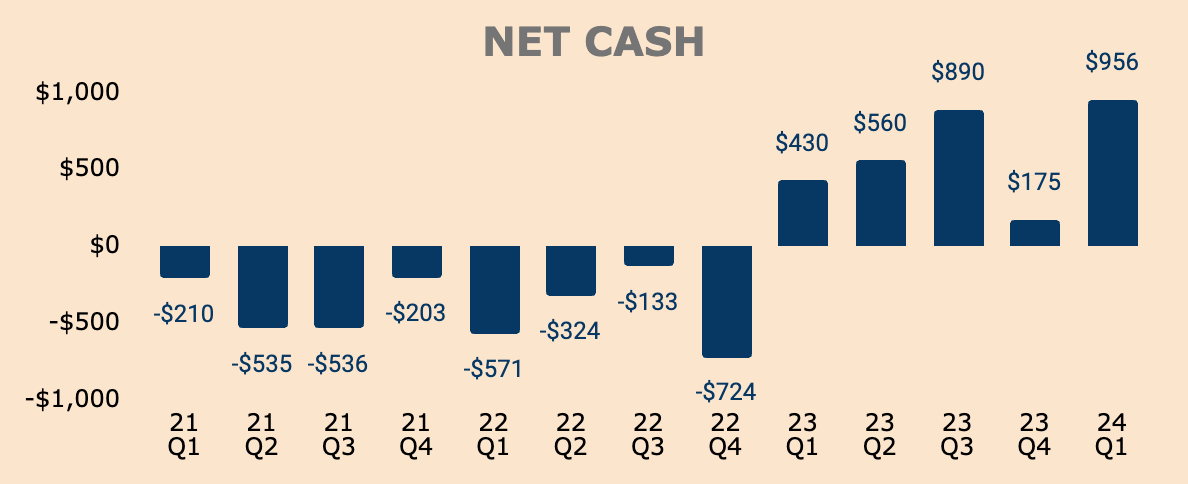

Reason #5: Expanding Balance Sheet

As a result of improving profitability, Block’s balance sheet has also expanded. As of Q1, the company has nearly $1B of Net Cash on its balance sheet, which has improved over the last few quarters.

Author’s Analysis

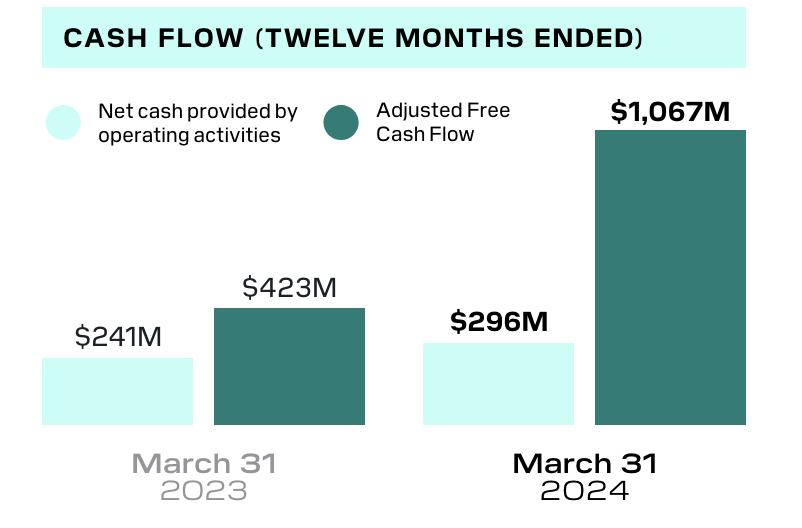

Expect Net Cash to increase moving forward as cash flow continues to improve. Over the last twelve months:

- Cash Flow from Operations was $0.4B, almost doubling YoY.

- Adjusted Free Cash Flow was $1.1B, more than tripling YoY.

Block FY2024 Q1 Shareholder Letter

Robust cash flows enabled Block to buy back its shares on the cheap. Last October, Block launched a $1B buyback program. In Q1, the company repurchased $252M worth of stock, helping to negate the effects of shareholder dilution through stock-based compensation.

As of Q1, Block still has $591M available for repurchases. Given its growth, profitability, and buyback momentum, we can expect a new — and possibly larger — buyback authorization later this year, which could be a catalyst for the stock.

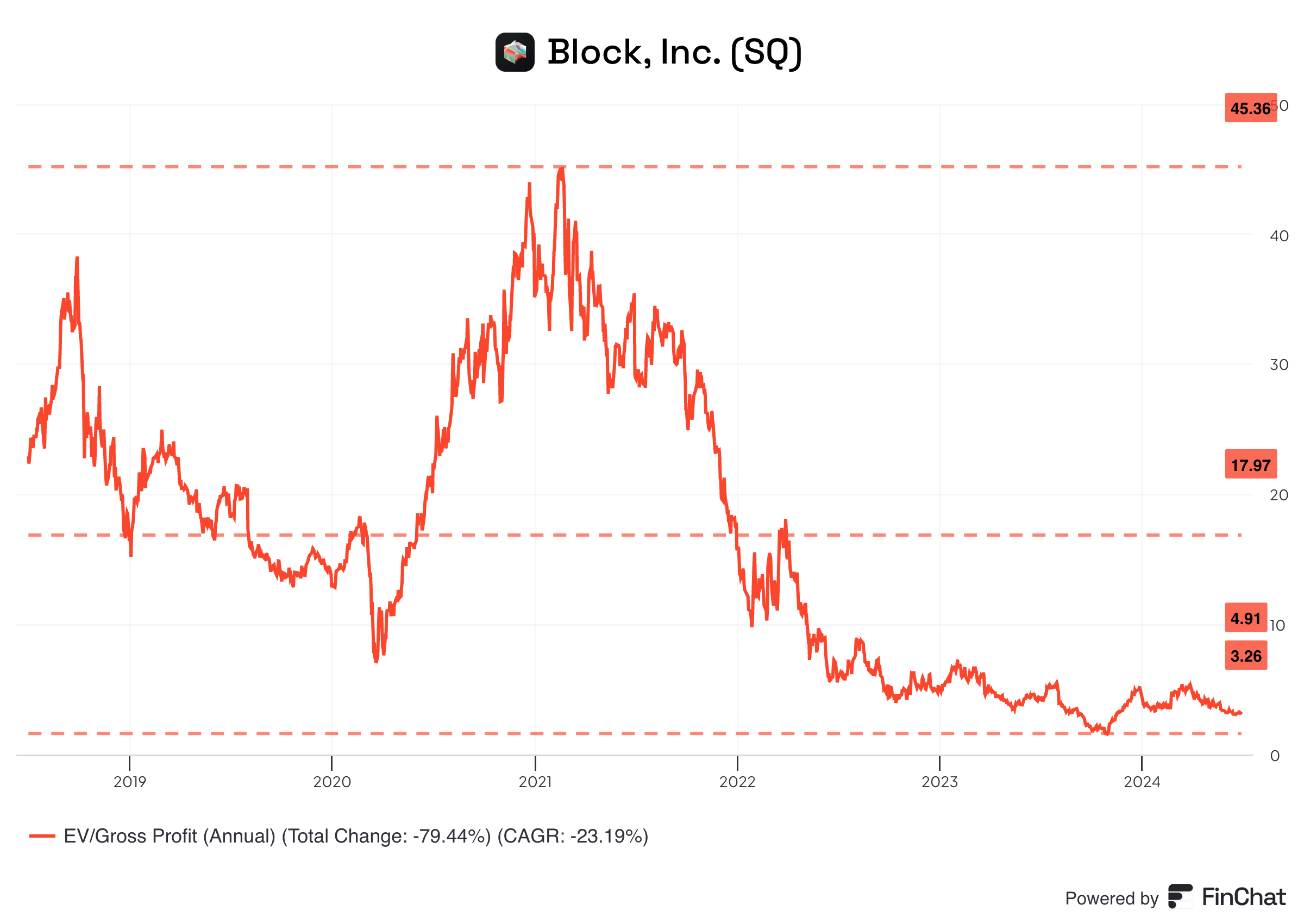

Reason #6: Priced at 2018 Levels

Speaking of which, Block is still trading at depressed valuations, basically at the same price from six years ago. As it stands, Block trades at an EV to Gross Profit multiple of just 4.9x, significantly lower than its peak multiple of 45.4x.

Assuming no Gross Profit growth and a return to its average multiple of 18.0x, we are looking at a 250%+ upside potential for Block stock. Sure, a lower multiple is justified given Block’s slowing growth rate as well as increased competition in the fintech space — but a return to a 10.0x multiple is more than reasonable, which is still a 100% upside from here.

FinChat

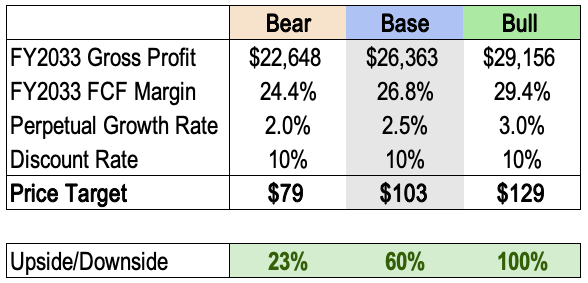

As for me, I have a base-case price target of $103 for Block stock, which is a 60% upside from current prices. This is based on the following assumptions:

- FY2033 Gross Profit of $26.4B, which is just a 13% CAGR.

- FY2033 FCF Margin of 26.8%, which is quite conservative given its current Adjusted EBITDA Margin profile of 30%+.

- Perpetual Growth Rate of 2.5%.

- Discount Rate of 10%.

I have also included my bear and bull cases below.

Author’s Analysis

As you can tell, I believe Block stock is currently undervalued. And considering that the stock is now trading at 2018 levels, I believe Block stock offers investors a wide margin of safety with a decent risk-to-reward profile.

Reason #7: Bitcoin

I’m no crypto enthusiast. But at the same time, I can’t ignore all the positive developments happening with Bitcoin recently. Countries are adopting Bitcoin, institutions are loading up on Bitcoin, and companies are betting on Bitcoin.

Block, as you know, has been investing heavily in Bitcoin. As of Q1, the company has $573M worth of Bitcoin on its balance sheet. Moving forward, the company will also be investing 10% of its Gross Profit from Bitcoin products to buy more Bitcoin.

According to management, Bitcoin products generated 4.2% of Block’s Gross Profit in 2023, with only 0.7% of related expenses. In other words, as Bitcoin product adoption increases, we can expect robust Gross Profit contribution at incrementally lower cost, which should improve Block’s overall cost structure and ultimately, its bottom line.

Furthermore, Block has been introducing more Bitcoin products (such as Bitcoin Round Ups, Paid in Bitcoin, and Bitcoin Conversions), which, over time, should drive higher Bitcoin adoption.

Of course, Bitcoin could be a double-edged sword for Block — we don’t know if Bitcoin will be “the native currency of the internet” or just a fad.

But considering Bitcoin’s 15-year history and price appreciation over that time frame, and given all the positive reception among governments all over the world, it’s safe to say that Bitcoin is here to stay and that it will be a larger part of our lives in the coming years.

Eventually, we may see mass Bitcoin adoption — and when that happens, Block will be one of the main beneficiaries of the Bitcoin standard.

Thesis

Block is one of the most promising fintech companies with strong competitive moats in terms of branding, network size, and switching costs. Not only that but the company has just posted one of, if not, the best quarter in its history as a public company.

While its price action looks like a falling knife to most, I make the argument that Block stock offers compelling value for long-term investors who want exposure in the fintech space. This is driven by seven main reasons:

- Square’s strong monetization trends

- Cash App’s virality and growth

- Massive growth runway in the fintech landscape

- Ongoing operating leverage

- A pristine balance sheet with positive Net Cash

- Stock trading at 2018 levels

- The rise of Bitcoin

Major risks include the potential commoditization of payment processing services, which can destroy Block’s growth and earnings potential. In addition, investors can’t completely write off the likelihood of a Bitcoin bust — such an event would drag Block stock down to the ground.

But these risks are known, and I believe it’s already reflected in Block’s current price. What most investors fail to notice is the potential upside that comes with owning Block stock, propelled by the seven reasons mentioned above.

That being said, I maintain my bullish stance on Block stock.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MQ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.