Summary:

- Boeing’s preferred stock offers a 5.6% yield with dividends paid quarterly starting January 2025. But mandatory conversion by October 2027 limits long-term income appeal.

- The investment case hinges on Boeing’s common stock price and interest rates, with potential price upside if common stock reaches analyst targets.

- Current preferred stock trades at $53.54, with potential for 50% upside if interest rates drop and common stock hits $238 by 2027.

- While not the best income idea, Boeing’s preferred stock offers opportunities driven by common stock price appreciation and interest rate changes.

JHVEPhoto

As part of the capital raise that I discussed in detail in a separate report, Boeing (NYSE:BA) also issued preferred capital. This report will focus on the Boeing preferred stock as an income idea. So, it will not focus on the prospects of the company or the common stock. The main question I want to answer in this report is whether the Boeing preferred stock (NYSE:BA.PR.A) has any appeal for investors.

About Boeing Preferred Stock

Boeing preferred stock can be purchased through depositary shares, of which $5 billion has been issued and another $750 is available to cover over-allotment. Each depositary share which was priced at $50 represents a 20% interest in 6% Series A Mandatory Convertible Preferred Stock. The stock is mandatory convertible on the 15th of October 2027 if conversion does not happen earlier. The annual dividend is set at $3 per share.

When Will Boeing Pay Dividends?

Boeing will pay preferred dividends four times per year, starting on 15th of January 2025. The dividend dates for the dividend payments are set to occur on Jan. 15, April 15, July 15 and Oct. 15. In principle, the dividends will be paid in cash, but the company also could opt to pay the dividend in common stock or pay the dividends in a combination of cash and common stock.

Boeing Preferred Stock Currently Offers A 5.6% Yield

Dividends.com

Boeing Preferred Stock currently trades at $53.54, which is 7% above the $50 issuing price. At an annual dividend of $3, the current yield is 5.6% and I do believe that’s quite attractive. Particularly in the aerospace and defense industry, we don’t see common stock with a better yield. Apart from Howmet Aerospace (HWM) and Bombardier (OTCQX:BDRBF), I don’t know any other aerospace company that pays a dividend through preferred stock. The Howmet Aerospace preferred dividend yield is 5.9% while Bombardier’s preferred dividend yield is 8.7%, but flexes with the Canadian prime rate. So, Boeing’s preferred dividend yield is not the highest but it’s also not bad.

Boeing Preferred Stock Investment Case Is Complex

There are several things to like and not to like about the dividends on preferred stock. Stating with what I do not like about the dividend is the fact that the stock mandatory converts by October 2027. So, if you’re looking for a long-term income provider Boeing preferred stock is not the right choice, in my view. On the mandatory conversion date, each depositary share will be converted into 0.2914 to 0.3497 shares. Boeing common stock currently trades at $149.58 which would mean that each depositary share would convert into $43.59 to $52.30. At the current prices, in the worst case, it would result in a $9.95 loss, calculated as the difference between the common stock price after conversion and the current price of the preferred stock minus, and in the best case there would be a $1.54 loss. If you add $3 per share in dividends per year, that adds $9 per share, which would limit the loss in the worst case to $0.95 and in the best case it would result in a $7.46 profit, but that would bring the annualized dividend yield after adding the losses to 4.6%. So, there’s a risk of things not working out.

Seeking Alpha Premium

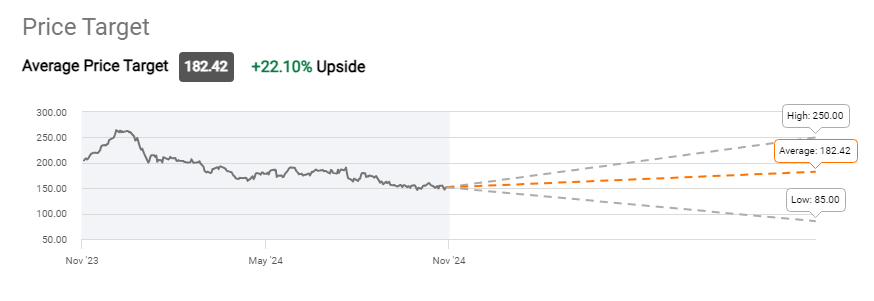

However, the analyst price target for Boeing common stock is $182.42. If that were the stock price at time of conversion in October 2027, it would bring the conversion consideration to $53.16 at the low end and $63.80 at the high end. At the current prices for the preferred stock that would result in a $0.38 loss at the low end and $10.26 gain at the high end excluding dividends. So, I would say that the investment case for Boeing preferred stock stretches beyond the income into the price of Boeing stock and we will likely see the preferred stock price flex with changes in the price of the common stock.

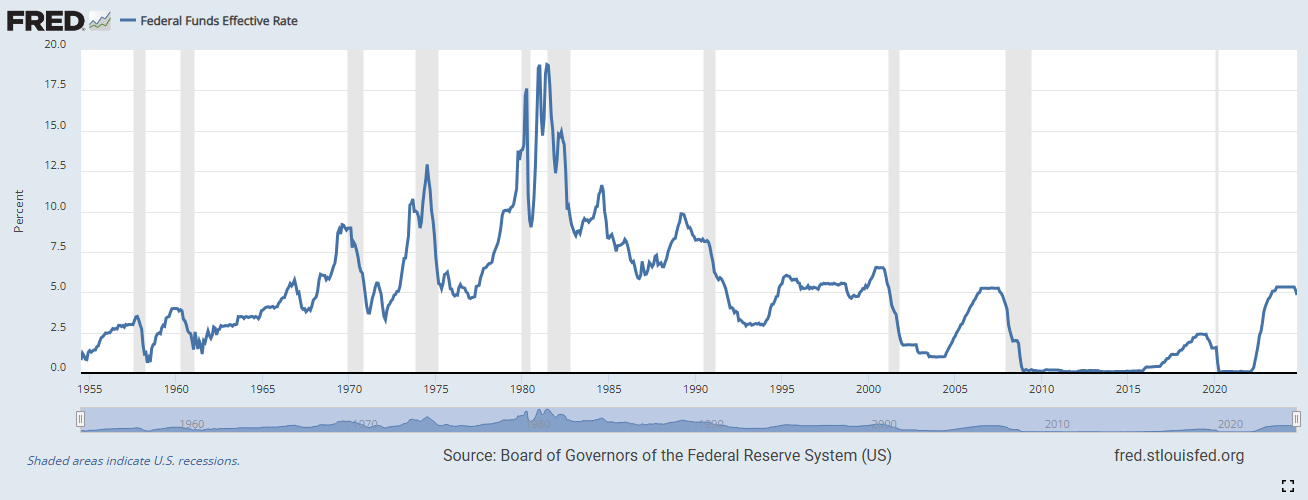

FED

Currently the effective federal funds rate is 4.8%. The expectation is that by December 2025 the Fed will have lowered the rates to 375-400 bps, and by 2027, the rate is expected to be 2.9%. As interest rates decline it’s likely that more investors will start looking at other income ideas. As a result, the Boeing preferred stock price could start increasing. Simultaneously that also implies that the effective yield will come down.

Putting everything together, I do believe that the preferred stock price will increase based on a combination of Boeing’s common stock price and the interest rate. Currently, Boeing’s preferred stock dividend yield is 80 bps above the Fed fund rate. If we were to apply the same premium to 2027, that would imply a 3.7% preferred stock dividend yield and the preferred stock to trade at $81, which represents 50% upside from current levels. However, that price would only be attractive from a conversion point of view if Boeing’s stock price trades between $232 and $278.

Coin Price Forecast puts the 2027 price at around $238, which seems to be more or less validating the price target implied from a yield perspective. Reasoning the other way around from a conversion price perspective, a price of $238 for the common stock would put the shares between $69.35 and $83.23.

Conclusion: Boeing Preferred Stock Is Not The Best Income Idea, But There Are Opportunities

All in all, if you do believe that the common stock will trade higher, I do believe that the preferred stock offers a nice opportunity. Not so much driven by income but driven by upside to the price of the preferred stock as a function of the interest rate environment and the common stock price. As a result, I’m marking the stock a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BA, HWM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

If you want full access to all our reports, data and investing ideas, join The Aerospace Forum, the #1 aerospace, defense and airline investment research service on Seeking Alpha, with access to evoX Data Analytics, our in-house developed data analytics platform.