Summary:

- Broadcom is an expensive but promising semiconductor company with long-term growth potential.

- The global semiconductor industry is expected to reach $1 trillion by 2030, driven by trends in remote working, AI, and electric vehicles.

- The Company’s financial analysis shows strong net income and potential for 15% annual EPS growth, but caution is advised regarding its balance sheet.

- With the current valuation exceedingly high and geopolitical risks surrounding technology companies, my rating for AVGO stock is a Hold.

G0d4ather

Broadcom (NASDAQ:AVGO) is expensive right now, yet as one of the leading semiconductor companies in the world, I think it has a place in technology portfolios. My analysis shows investors are paying a significant premium if buying now, but operations and financials will contribute to continued long-term growth for the firm. As an investor focusing on 10+ year investment horizons, I consider AVGO worth holding for the long term.

Company Overview

For investors already acquainted with Broadcom, please skip ahead to the section ‘Market Drivers.’

Broadcom designs, develops, and supplies semiconductor and software infrastructure. Its customers come from markets including data centers, software, broadband, networking, wireless, and industrials. It was founded in 1991 and became known as Broadcom after a series of acquisitions that began as a division within Hewlett Packard (HPE). In 1999, HP spun off its measurements, components, chemical analysis, and medical businesses into Agilent Technologies. Part of this business, called Avago Technologies, was then acquired by Kohlberg Kravis Roberts & Co. (KKR) and Silver Lake Partners in 2005. In 2015, Avago announced its intention to acquire Broadcom for $37 billion. The deal was finalized in 2016.

GuruFocus

Market Drivers

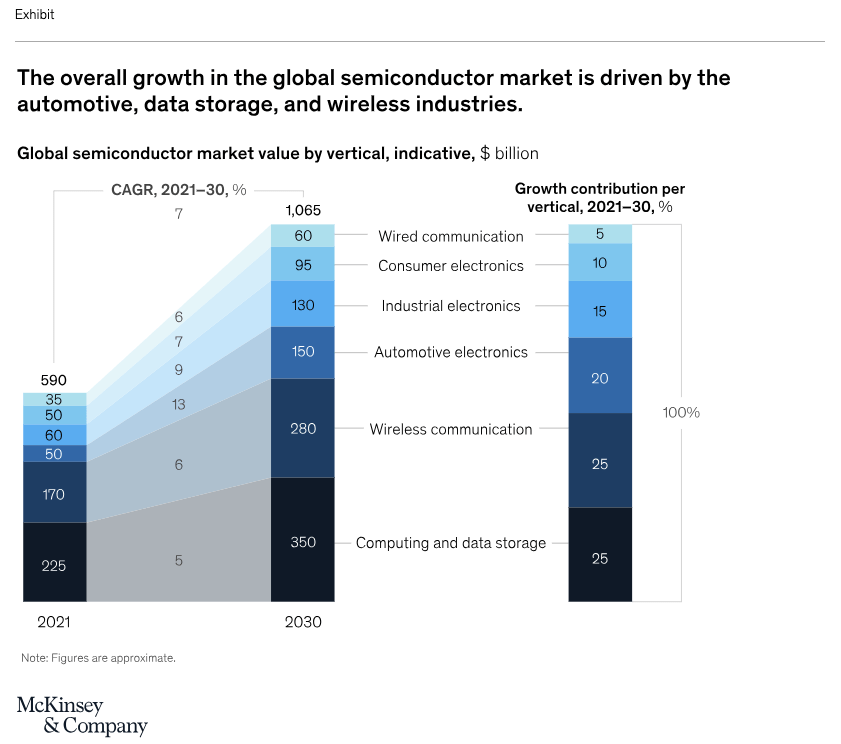

McKinsey has reported that the global semiconductor industry is expected to be worth $1 trillion by 2030. The aggregate annual growth rate is forecasted to average between 6 and 8 percent up until that point. Such growth is driven by massive trends in remote working, the proliferation of AI, and increasing demand for electric vehicles. The research outlines that 70% of the market’s growth could be attributed to the automotive, computation and data storage, and wireless sectors. The automotive industry is particularly anticipated to see higher demand, up to three times present levels, due to progress in autonomous transport and e-mobility.

McKinsey

Fortune Business Insights also reports that the semiconductor market was valued at $527.88 billion in 2021 and is forecasted to grow from $573.44 billion in 2022 to $1,380.79 billion in 2029, indicating a CAGR of 12.2% from 2022-2029. The growth is attributed to the higher use of electronics across the globe and the emergence of AI, Internet of Things, and machine learning.

Fortune Business Insights

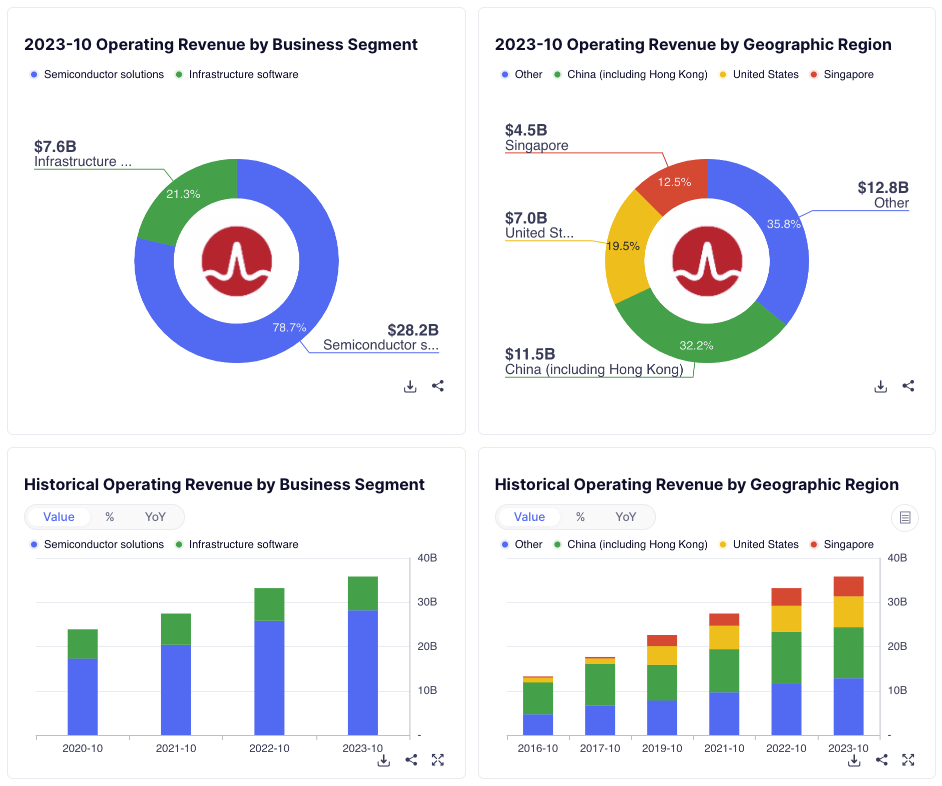

At Broadcom’s 2021 investor day, it outlined its plan to emphasize its business model to focus on strategic customers. Its plan focuses on partnerships with elite, multinational customers, primarily from the Fortune 500, to drive revenue sustainability and foster growth. 70% of its annual revenue comes from these core customers, and 80% are licensed to use five or more Broadcom software solutions.

On November 22, 2023, Broadcom completed its acquisition of VMware, significantly improving its status as a top technology infrastructure firm. This merger should improve its private and hybrid cloud networks, offering higher security. VMware Cloud Foundation should modernize cloud and edge environments, and the deal evidences Broadcom’s acquisition strategy to remain on the cutting edge of technology developments in its field.

Financial Analysis

Compared to major peers, Broadcom has the second-largest net income of the group, including Taiwan Semiconductor Manufacturing Company (TSM), Advanced Micro Devices (AMD) and Texas Instruments (TXN):

Seeking Alpha

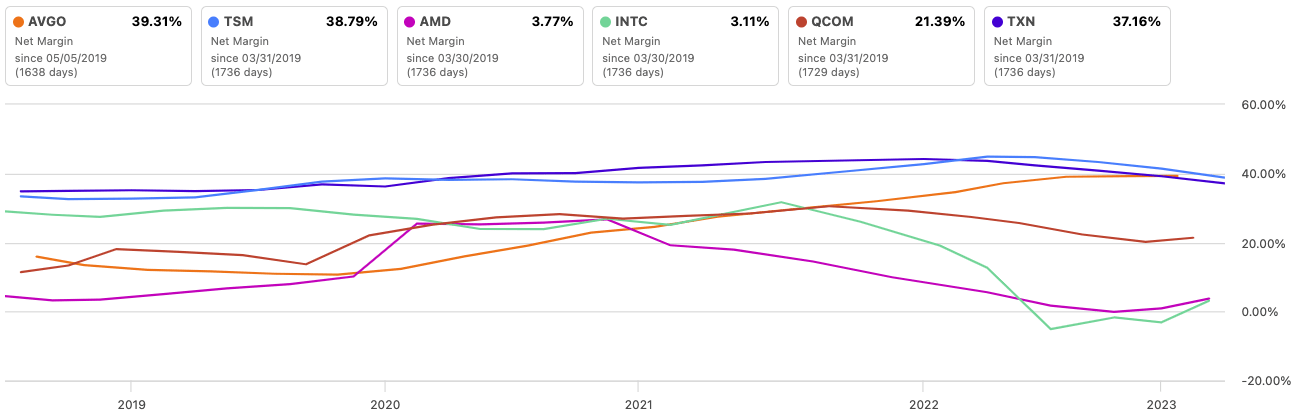

Additionally, it has a net margin that is essentially joint top with TSMC and TXN:

Seeking Alpha

Compared to the sector median net margin of 2.49%, AVGO has a 1,479.66% difference.

Investors would be wise to take caution on the company’s balance sheet, where its equity-to-asset ratio is just 0.33. Compare this to TSMC’s ratio of 0.63 and TXN’s 0.52.

Seeking Alpha

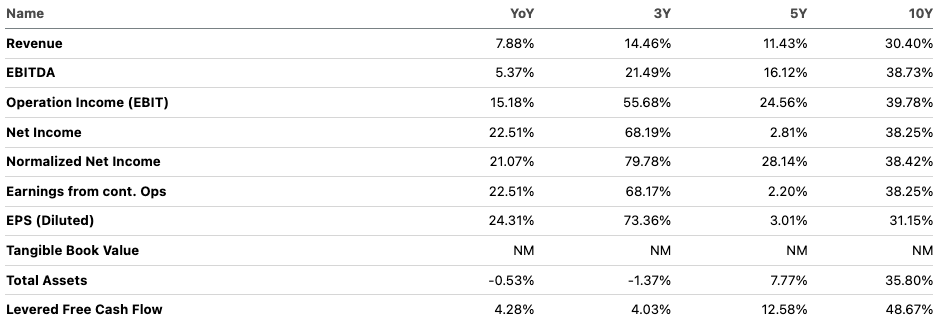

Considering historical growth rates for Broadcom and the massive proliferation in advanced technology currently underway, the future looks positive for the company in terms of earnings growth. It does not seem unreasonable for the firm to hit 15% annual EPS growth as an average over the next 10 years when considering general market CAGRs, but also internal efficiencies that are likely as a result of the implementation of automation driven by AI.

Seeking Alpha

Value Analysis

For my discounted cash flow analysis, I used the forward EPS of $46.83 as my starting point, a 15% annual EPS growth rate, as commented on above, for the next 10 years, a 4% annual EPS growth rate for my 10-year terminal stage following this, and an 11% discount rate. My fair value came to around $1,046, indicating a potential negative 19% margin of safety at this time.

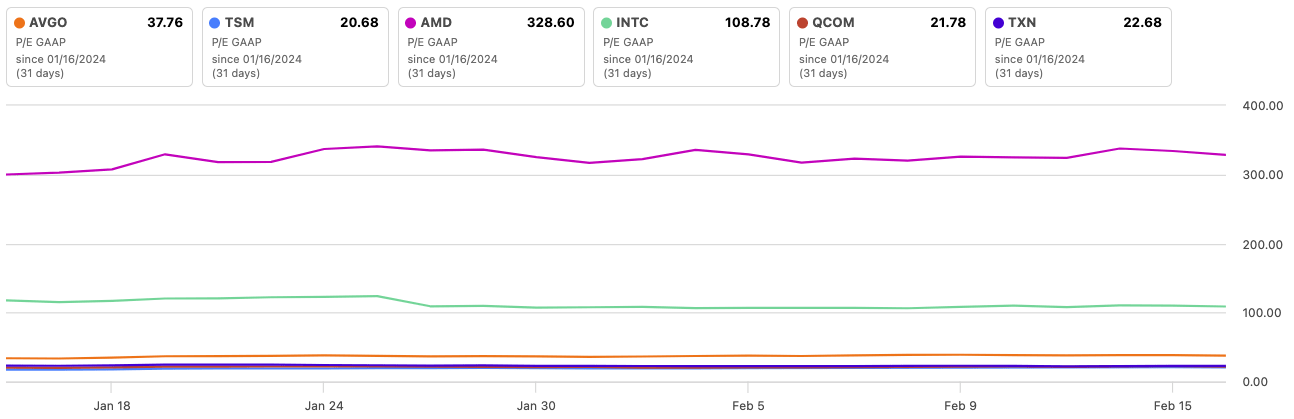

However, also consider its much lower P/E GAAP ratio when compared to AMD and Intel (INTC):

Seeking Alpha

Risks

Broadcom is significantly related to geopolitical risk between the US and China surrounding Taiwan’s TSMC. While any escalation of these tensions would cause significant shocks to most global markets, technology companies would be the first and most negatively affected, without a doubt. As such, allocating too heavily to Broadcom or any of the technology companies aggressively could mean high levels of volatility to come, as this risk does not look accurately priced into present valuations.

Additionally, my above-mentioned 15% EPS growth rate as an annual average over the next 10 years is by no means guaranteed and is higher than some other analyst estimates. My positive future earnings outlook considers internal efficiencies driven by advancements in technology, but the effective execution depends on management’s future decisions relating to employee count, automation, and organizational structure.

Conclusion

Overall, I consider Broadcom a good investment to have. I do not think it is the best company to own for exposure to technology and, specifically, semiconductor operations, but it is a top choice. Investors should be aware of the present geopolitical risks surrounding the technology sector and if they are willing to take on the risk associated with Broadcom, may want to consider investing more heavily in TSMC, which I consider the better investment of the two.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of TSM, TXN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.