Summary:

- The Liberty SiriusXM Group and Sirius XM finally announced a transaction to merge Liberty SiriusXM and Sirius XM.

- Although there are no real surprises in the deal, the stocks involved don’t really get moving in either direction, which simply can’t be right.

- As a result, there is an opportunity for a 50%+ return within 6-9 months.

RichVintage/E+ via Getty Images

Liberty SiriusXM and SiriusXM agree to merge

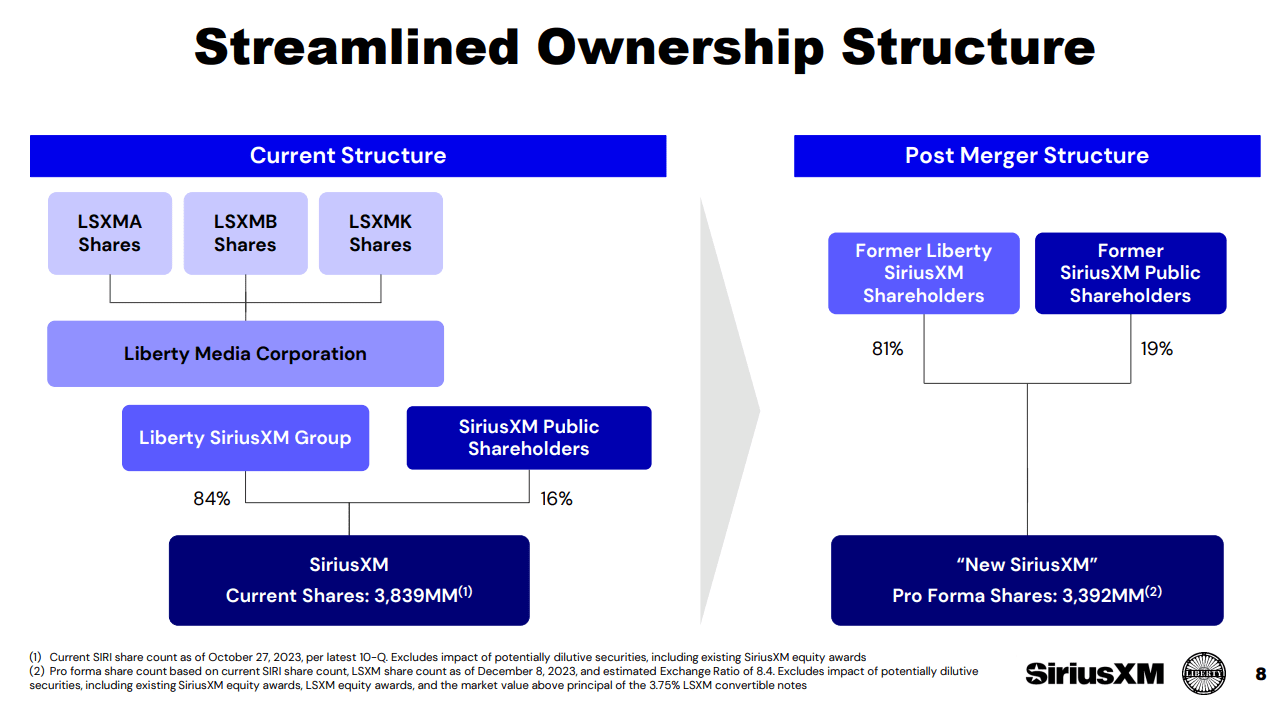

As widely expected (and for far too long), The Liberty SiriusXM Group (NASDAQ:LSXMA) (NASDAQ:LSXMK) (NASDAQ:LSXMB) and Sirius XM Holdings Inc. (NASDAQ:SIRI) have finally agreed to merge. This means about nine months from now Liberty SiriusXM shareholders will receive approximately 8.4 shares of the new SiriusXM, thus owning a total of about 81% of the new company, while the current minority shareholders of Sirius XM Holdings will own the remaining 19%.

The transaction is expected to be tax-free, and there are no potential obstacles to its approval, given that Liberty already owns 84% of SiriusXM and effectively controls the company. Minority shareholders of SiriusXM won’t vote on the deal, while Liberty Media’s shareholders will – but there can’t be any doubt how John Malone with his super-voting B-shares, alongside large owners like Berkshire Hathaway (BRK.B) (BRK.A) and Seth Klarman, will decide: Liberty SiriusXM trades for less than 70% of its underlying value, which means that collapsing the discount is the most accretive thing to do.

The 81/19 ownership split is the result of a months-long bargaining progress, at the beginning of which stood Liberty’s proposal to compensate SiriusXM minorities for the additional debt assumed in a merger via a cash dividend. This solution was not adopted, as it would have burdened SiriusXM with even more debt. Instead, Liberty will give up about 3% of its ownership interest in exchange for minorities assuming more debt.

You can review all the details in today’s slide set.

Liberty Media / SiriusXM presentation

But the NAV discount doesn’t close

What is most interesting about this deal is that, as I write, there remains a huge discrepancy between the intrinsic value of the Liberty SiriusXM tracking stocks and their trading price. As of now, the trackers trade for about $27, while 8.4x Sirius XM’s price of $4.8 would result in a value of more than $40.

So what is wrong here? Is the market just nuts?

For a long time, there has been that idea out there about SIRI being the overvalued stock of the pair, given its massive share repurchases and low liquidity. Instead, the LSXM trackers would have been the fairly and efficiently valued stocks. I personally doubt that theory, but this is what some investors were saying. Today, it certainly looks like nobody wants to bid up the tracking stocks, while SIRI even traded lower after the announcement (after being up 10% yesterday).

It might rally a few minutes from now – who knows? At least this is what SIRI has represented over the past few months: a textbook example of stomach-turning volatility.

Why the NAV discount remain elevated

My personal explanation for the phenomenon is rather short-termism: Given the small trading float of SiriusXM stock, coupled with an outsized short interest (which is probably not mainly due to an assumed overvaluation, but simply to the many arbitrageurs out there that wanted to bet on the closing of Liberty’s trading discount by going long LSXM and shorting SIRI), the stock market has been extremely inefficient for SIRI shareholders for a long time. Frequent brutal selloffs have been followed by massive short squeezes.

Hence, until LSXM shareholders finally get their hands on their SIRI stock and the float increases, there will be a lot of volatility. Technical issues and supply/demand imbalances will have huge impacts, a few of which have been examined in my recent article on the situation.

The stock market will start to price in the exchange ratio of 8.4x between the two classes of stock of the same company over the next few months, and when SIRI suffers from one of its low-float selloffs, LSXM trackers will probably suffer as well. Or not, who knows?

In a nutshell: For anybody looking for short-term results, this is no attractive situation, unless we are talking about ultra-short-term, super-speculative trading. If you own stocks only for minutes, fast movers are great.

Bargain alert for value investors

Long-term oriented folks will need to fasten their seat belts. In the meantime, it should help to have a clear view of what they effectively own: a piece of SiriusXM.

Each share of the Liberty trackers (the K, A and B shares from today will yield exactly the same result, as they will treated as a single class of shares) gives its shareholder a claim on the profits belonging to 8.4 shares of the new SiriusXM, which will likely earn $1.5B of free cash flow, or FCF, within a few years (once the current massive investment phase in new satellites will be done) and have 3.4B shares outstanding, so the FCF belonging to each share of the LSXM trackers will be $3.70 in 2025 or 2026.

Even if FCF stagnated at the current level (unlikely, since it is heavily depressed by this year’s additional investments to the tune of ~$300m), FCF per current LSXM tracker would still be around $3. This means the trackers have a current 11% look-through FCF yield, which is likely to increase over the next few years.

From a purely fundamental point of view, this looks pretty attractive to me, and I certainly won’t sell a single share at these levels and won’t offload my SIRI stock once received as long as it continues to carry an 11% FCF yield.

However, not many fund managers can own such volatile stocks, where basically anything can happen every day. So, the current discount seems a “volatility discount” to me, unrelated to business fundamentals.

The theory that a stock like SIRI with its tiny trading float can still be overvalued while having much of its float sold short sounds implausible to me. Why would SIRI stay stubbornly overvalued while everybody knows that it should fall some 20-30% within a few months and while it is attracting short sellers due to the LSXM/SIRI arbitrage trade?

And even if there was some pressure on the stock close to its merger or right afterward (LSXM shareholders might sell their new SIRI stock right away), the very likely index inclusion of this $19B company with the resulting buying spree by index funds should compensate for that.

If you can stomach the volatility, you will probably be richly compensated. I believe the new SIRI shares will settle around a more common FCF of yield of about 7%, i.e., they should trade for about $43 – and grow from there, as lower capex levels kick in and FCF grows over the subsequent years.

This means current LSXM holders can expect a return of about 50-60% within one year.

Risks are almost negligible

The downside is pretty negligible, in my view. Even at SIRI’s recent multi-year lows of about $3.50, the underlying value of the LSXM trackers would still be $29.40, i.e., about 9% higher than today’s trading price. At that point, the stock would trade for a look-through FCF yield north of 10%.

That said, some readers will question my FCF estimates: Why should FCF grow? After all, SiriusXM enjoyed an extremely low tax rate until recently but has now become a full taxpayer. However, the company is looking to lower its tax rate and will soon come up with some tax optimization, as it stated at a recent conference:

And as we look ahead, we certainly hope that there’ll be some opportunities to reduce taxes and we have some thoughts on that, that we’re not ready to share yet, but I do think there’ll be some improvements in our tax profile going forward as well.

Moreover, despite giving usually rather conservative guidance, the company sounded very confident in being able to grow FCF going forward:

I think as we look beyond next year, because we still have sort of satellite CapEx at a high level, and non-satellite maintenance levels for the new platform at a pretty high level. As you look beyond to ’25 and forward, we would expect free cash flow to grow, and over the next five years for sure.

I believe management in this respect since 2023 saw a $200m capex increase for new satellites (which I consider a growth investment) and a $100m increase in music royalties (which SiriusXM can usually recover by raising subscription fees, albeit with a lag), alongside other smaller investments. The company stated on its Q4/22 call that satellite capex will moderate already in late 2024 and shrink to near zero in 2027, where it will stay for many years.

In Q3/23 SiriusXM guided to $1.15B of FCF for 2023. Excluding 75% of the satellite capex and the one-off increase in music royalties, its steady-state capex should be roughly $250m lower, which means it needs very little growth to deliver the $1.5B of FCF which I expect in 2025 or 2026 at the latest.

In summary, if SiriusXM trades for a reasonable FCF multiple for a slowly growing subscription business with enviable assets, Liberty shareholders will do great in a very short timeframe. And even if SIRI slumps, Liberty shareholders would still not lose much or even gain a little.

And even if I am missing something, I certainly am not missing one safety backstop: Besides serving an attractive, rather affluent customer population, SiriusXM owns a piece of exclusive real estate in 80% (and growing) of all U.S. cars on the road with the possibility to receive audio and video via its own satellites – how could that not be an attractive acquisition target for a tech business seeking to expand into automobiles?

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2024 Long/Short competition, which runs through December 31. With cash prizes, this competition — open to all contributors — is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

Analyst’s Disclosure: I/we have a beneficial long position in the shares of LSXMA, BRK.B either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.