Summary:

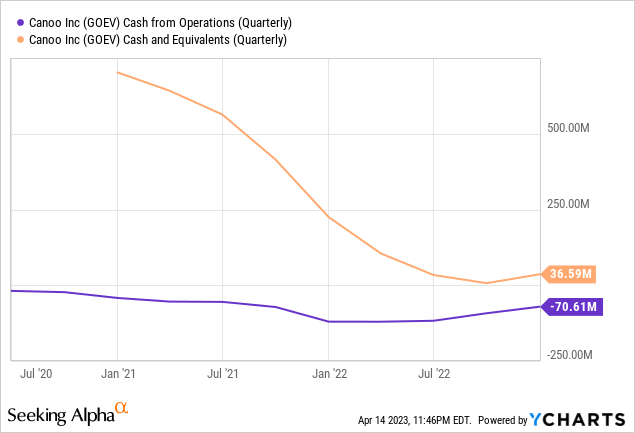

- Canoo’s total cash outflows from operations in 2022 came in at $400 million to push its cash and cash equivalents to $36.6 million as of the end of the year.

- Total operating expenses and capital expenditure for the first quarter of 2023 are expected to not be less than $85 million.

- The subsequent liquidity gap has thrown Canoo’s future into disarray even as large orders have bolstered a fledging sales pipeline.

sefa ozel

There might be too many EV companies. This did not seem like a problem during the pandemic boom years when investors viewed demand for EVs as near-infinite and valued the common shares of EV companies under the lens of euphoria and hope. Canoo’s (NASDAQ:GOEV) 48% year-to-date slide reflects a reality that has now hit several EV companies that also went public just a few years ago on the back of the now-burst blank check company bubble. Electric Last Mile Solutions went bankrupt in the spring of 2022, Faraday Future (FFIE) faces delisting and does not have sufficient capital to bring its flagship to market, Arrival (ARVL) just completed a reverse stock split and is reSPACing after a liquidity collapse placed the EV upstart on a path to bankruptcy.

The EV class of 2021 is fast becoming a requiem for lost dreams and Canoo faces a volatile and highly uncertain near-term future even as demand for EVs looks set to form new sales records every year for the next decade. In the USA, the Inflation Reduction Act is working to boost business demand for EVs. Broader sales of EVs in the US are now expected to grow by a 22.8% compound annual growth rate until 2027 when at least 2.13 million EVs will be sold at a projected market volume of $139 billion. Hence, Canoo faces strong demand even as the company reported cash and equivalents of $36.6 million as of the end of its fiscal 2022 fourth quarter. This was against $70.6 million in cash outflows from operations to set a bleak backdrop for operations in 2023 as the company intends to ramp production of its Lifestyle Vehicle.

The Fiscal 2022 Fourth Quarter Earnings

I’m focused on three metrics when it comes to EV upstarts. Total cash outflows, liquidity, and the sales pipeline. Canoo is still pre-revenue so its liquidity base and outflows are the core determinants of near-term value. With total cash outflows from operating activities of $400.5 million for its fiscal 2022, up around $100 million from $300.8 million in 2021, Canoo’s liquidity position has been placed in peril. Short-term investments and restricted cash help boost total liquidity to $43.7 million but this is still not enough to meet Canoo’s guidance to spend between $85 million and $115 million on operating expenses and capital expenditure during the first quarter of 2023.

I think it’s staggering that Canoo’s outflows have been so material essentially without any sales. The company could be on track to spend at least $340 million through 2023 on a best-case scenario and so would at least need to 10x its current cash and equivalents to meet near-term operating cash demand. Canoo was able to raise around $52.5 million post-period end, but again this is insufficient to meet fiscal 2023 cash demand unless the company materially shrinks outflows. Critically, the February equity raise was completed at a level that was almost double Canoo’s current price per share. To be clear here, Canoo would have to sell almost double the 50 million shares it did at discounted rates earlier this year to raise the same amount of funds in any future capital raise.

A Dark EV Reality

Canoo’s order book as of the end of the fourth quarter was $2.8 billion, a roughly 5% growth sequentially from the third quarter and up around 323% from the year-ago comp on the back of large orders from Walmart and several other businesses for Lifestyle Delivery vehicles. This is as the company targets a 20,000 EV production run rate from its Oklahoma City manufacturing facility.

Hence, a long position in Canoo is now being built on its sales pipeline and other factors outside of total cash outflows and liquidity. I like Canoo’s EV designs and it would not be great for the industry for yet another EV upstart to face the specter of bankruptcy, but the risks could outweigh the rewards here. Canoo’s current market cap at $306 million is set against a marked liquidity gap even after its last fundraising with the company likely to require another capital raise by summer. Bears, who form the 18% short interest in the company, could still be in line for further gains.

Canoo’s market cap is still sufficiently large enough for another equity raise but this will be on the back of shareholders who are faced with the choice of a possible Canoo bankruptcy or material dilution to help management reach their 20,000 vehicles production run rate target. Bulls would of course also highlight Canoo’s sales pipeline even against the competition as a reason to stay enthusiastic about its prospects. A lot of EV companies will likely not survive but Canoo’s sales pipeline likely provides a level of clarity it needs to continue to tap the equity market for dilutive raises in the near term. I continue to be neutral on GOEV stock.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.