Summary:

- Canoo faces a critical cash situation with only a few quarters of runway left due to consecutive quarters of net losses and cash burn.

- The company has made efforts to raise capital and reduce operational expenses, but the cash burn rate remains high, risking insolvency.

- A reverse stock split will be required to maintain compliance with Nasdaq’s minimum listing rules and to make new stock sales more functional.

Iryna Mylinska/iStock via Getty Images

A zombie firm describes a company that is able to maintain normal business operations despite being fundamentally insolvent. Any such firm is only able to remain a going concern by outside capital. Canoo (NASDAQ:GOEV), two and a half years after being listed on the Nasdaq through a blank check company, now has just a few quarters of cash runway left. The situation is critical with Canoo’s recent fiscal 2023 first-quarter earnings bringing no respite for bulls from the dominant bearish thesis. In this, Canoo’s near-term survivability drops to near-zero on the back of a cash position besieged by consecutive quarters of net losses and cash burn. Canoo’s quarterly operational liabilities, as measured by operating cash outflow, was $67.2 million as of the end of its first quarter. This was set against a cash and equivalents position, including restricted cash, of $12.5 million.

Bulls would be right to state that the company has not been standing still with its capital-raising activities. Canoo was able to raise $48 million through the sales of convertible debentures and the exercise of $15 million worth of warrants. The debentures were issued in April and come with a 1% coupon, they mature in June 2024. Assuming both transactions had closed during the first quarter it would have placed Canoo’s cash position at $69.7 million. The company also has a $150 million ATM facility and a further $150 million pre-paid advance facility with Yorkville Advisors that its management intends to tap to further boost Canoo’s liquidity position.

Zombie Financials And Uncertain Future

Canoo made huge strides in reducing its operational footprint to better preserve cash during the first quarter. Cash burn from operations was down 44% year-over-year with capital expenditure of $18.4 million a decline of 35% over the year-ago comp. However, the decreases simply don’t go far enough. Canoo expects operating expenses to be between $40 million to $60 million during its second quarter with capital expenditure coming in at $10 million to $20 million, both levels that would place its upsized cash position from the post-period end capital raises at significant risk of running out by the end of summer without more capital raises.

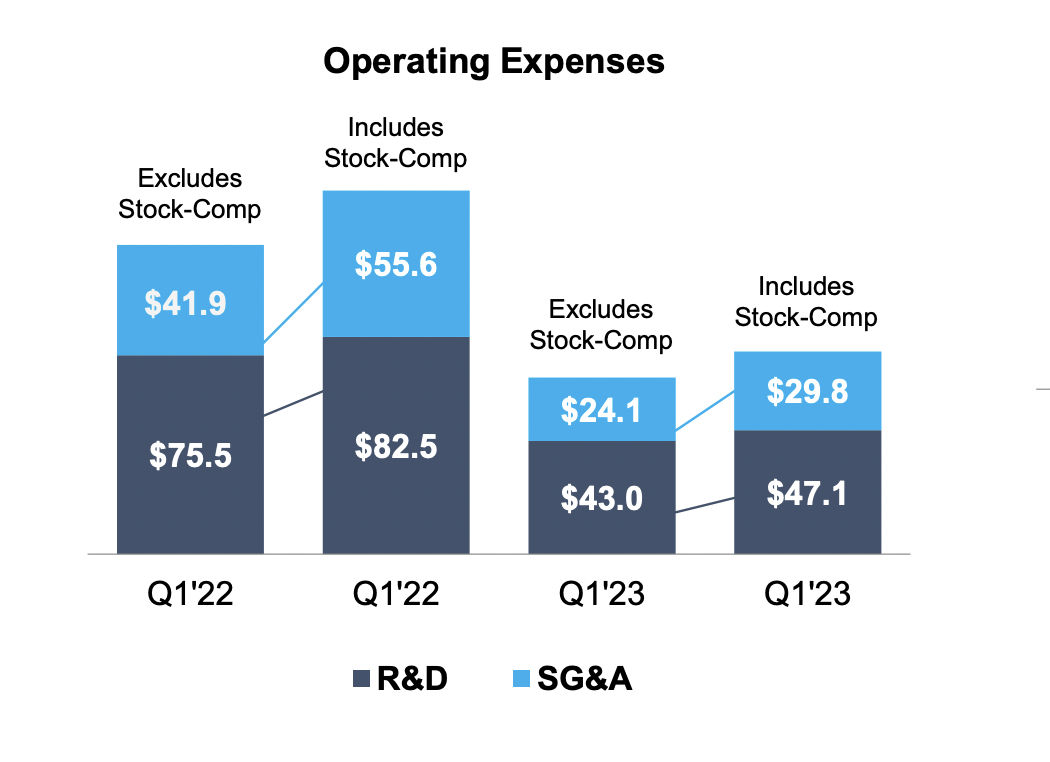

Canoo Fiscal 2023 First Quarter Earnings Presentation

Canoo’s current quarterly cash burn rate including capital expenditure stands at $85.6 million, around $342.4 million annualized. The company does anticipate further cost reductions from its first quarter with R&D expenses which fell 43% year-over-year to $47.1 million and SG&A expenses which fell 46% over the same time frame to $29.8 million in line for further reductions. Overall, Canoo expects a 25% to 30% reduction in annual operating expenses for its fiscal 2023 over 2022, this would imply total operating expenses of $354.2 million, a level that’s still far too high for Canoo to escape zombie status anytime soon. The company’s forecasted cash burn rate through the next four quarters is 4.9x its upsized cash position. Further, if you take an extremely bullish position that the company is able to fully realize the aggregate $300 million in new funding without any headwinds, then current operations would still be on track for a cash runway that’s less than a full year.

A Reverse Stock Split And Dilution

This dire outlook for cash comes against a $2.8 billion order book that saw stage 2 and 3 orders grow by 5% sequentially over the fourth quarter. It also comes against management guidance to exit 2023 with a 20,000 vehicle production run rate, rising to 40,000 in 2024, from their Oklahoma City facility. Critically, reaching production would not stem Canoo’s near-term liquidity needs and its start of production would see new demands on cash that the company simply does not have access to.

To be clear here, Canoo’s current market cap of $277 million is not enough to support its ATM offering with its current stock price also too low. The company will likely engineer a reverse stock split to maintain compliance with Nasdaq’s minimum listing rules in the summer and to raise its stock price to a level where stock sales make more functional sense.

Shares outstanding are up 86% since the summer of 2021 and is inline for further marked increases with a $150 million ATM forming 54% of its current market cap. Whilst the Fed pausing rates at its June 14 FOMC meeting could spark another bull market for currently risk-off stocks, the overall story for Canoo this year looks set to be defined by dilution set against more cash burn. Shares are to be avoided until the company highlights even deeper cost cuts beyond its current guidance range. A Chapter 11 filing is a very real and stark possibility.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.