Summary:

- Chevron is one of the largest integrated players in the global oil and gas industry, which experiences massive secular tailwinds due to a variety of different factors.

- The company has been extremely efficient in absorbing strong tailwinds of recent quarters and now can afford to make a promising megadeal in the Hess Corporation acquisition.

- My valuation suggests that the stock is substantially undervalued.

Nurlan Tastanbekov /iStock Editorial via Getty Images

Investment thesis

Chevron (NYSE:CVX) is a very special company for me because CVX was one of the first foreign investors in my home country, Kazakhstan when it just gained independence from the Soviet Union in 1991. Investing in a young country was a big risk, but I think the investment paid off well since nowadays Tengiz Field, where Chevron owns 50%, is one of the biggest jewels in the company’s crown. However, the strong bond of Chevron with Kazakhstan is not the reason why I am bullish on this company. The company demonstrates strong financial performance and is very efficient in absorbing the current favorable cycle for the oil and gas industry. Softening financial results this year are not a result of the company’s weakness but due to last year’s shocks after the war in Ukraine commencement when oil prices skyrocketed. Chevron was efficient in utilizing last year’s tailwinds and improved its balance sheet significantly, which allowed it to make a solid strategic move with a recently announced acquisition of Hess Corporation (HES). Last but not least, my valuation suggests that the stock is massively undervalued, even under very conservative assumptions. All in all, I assign Chevron’s stock a “Strong Buy” rating.

Company information

Chevron is one of the largest global oil and gas integrated companies. The business is operated via two segments: Upstream and Downstream.

The company’s fiscal year ends on December 31. According to the latest 10-K report, Downstream represented about 73% of the total company’s revenue in FY 2022. More than half of the company’s revenues are generated outside the U.S.

Financials

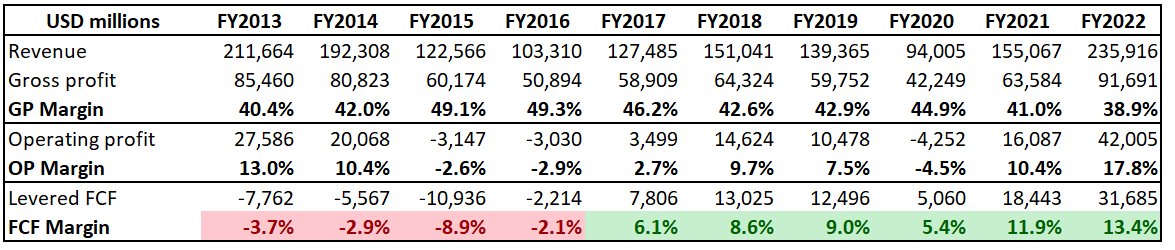

The company’s financial performance over the past decade has been mixed due to substantial volatility in commodity prices over this period. FY 2013 was the last year of the previous oil supercycle, and FY 2022 was the first of the new one. That said, we should take a closer look at a comparison between these two years. The operating margin improved notably from 13% to almost 18%. But the biggest win, I think, is the massive expansion in the free cash flow [FCF] margin. And it relates not only to FY 2022 but all years since 2017. Oil prices were not that high in 2017 and 2018. Still, the company managed to deliver a solid FCF margin.

Author’s calculations

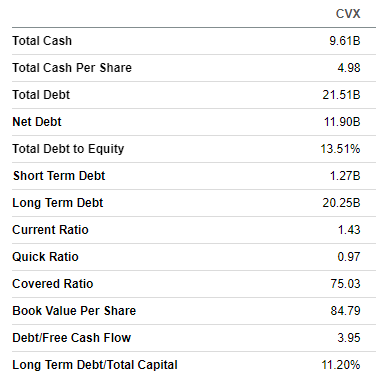

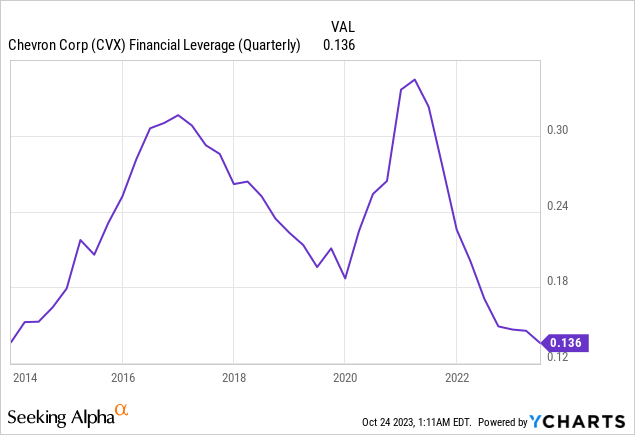

Having a healthy FCF margin over multiple years allowed the company to build a fortress balance sheet. The debt might look massive in absolute terms, but the leverage ratio is insignificant at low double digits. Moreover, I am very comfortable with a 75-covered ratio and the fact that the major part of the debt is long-term. Liquidity metrics are in good shape as well. A wide FCF margin and a solid financial position enable the company to keep shareholders happy with consistent stock buybacks and dividends.

Seeking Alpha

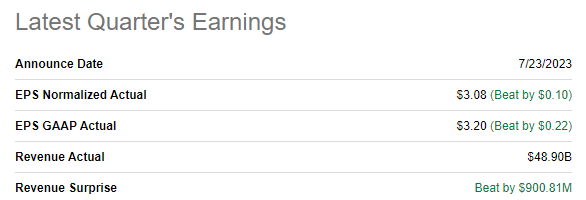

The latest quarterly earnings were released on July 23, when the company topped consensus estimates. It was expected that financial metrics would deteriorate after a massive oil price rally in the first half of 2022 due to the war in Ukraine. Revenue dropped YoY by 29%, and the adjusted EPS followed accordingly by shrinking from $5.82 to $3.08.

Seeking Alpha

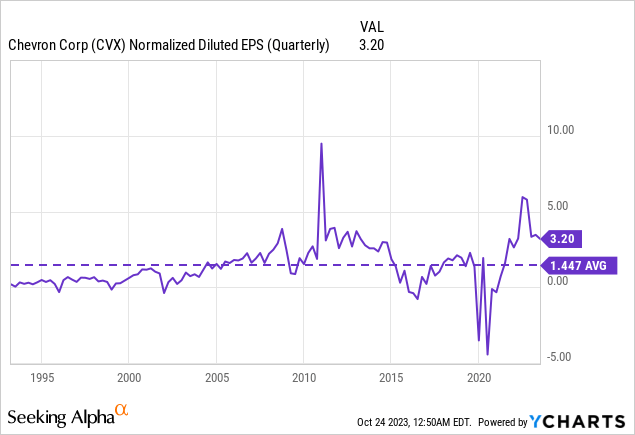

I will not dig deeper into the latest earnings because the upcoming quarter’s earnings are closed and planned for the end of this week. Therefore, I would pay more attention to looking forward. For Q3, consensus estimates forecast revenue at $53 billion, which means about a 20% YoY drop as the spread between this year’s prices and last year’s frenzy is narrowing. The apparent positive sign is that the adjusted EPS is expected to expand sequentially to $3.68, which is far above the historical average and is approximately in line with the previous oil super cycle, which ended in 2013.

I think the management is executing efficiently to absorb the current positive situation in crude oil prices. High profits are distributed in a sound manner between dividend hikes, stock buybacks, and improving the balance sheet. The company historically has been prudent with leverage, and the current indebtedness is at its lowest point over a long time.

The company’s strong balance sheet makes it well-positioned to fuel growth with acquisitions, and that is what the management actually did with the decision to acquire Hess Corporation. Despite the deal being all-stock, I think that Chevron’s strong balance sheet was an important factor for the agreement between the two companies to occur. It looks like the acquisition will give a strong boost to the company’s revenue growth and will help to diversify its assets. The acquisition of Hess is a strong step from Chevron to expand into the most promising blocks in the U.S., including the Permian basin and Bakken assets of Hess. The company’s management is confident the deal will build long-term shareholder value. It was expressed in the official press release stating that there will be an 8% dividend increase in January and post-closing expansion in the stock buyback program by $2.5 billion.

It is also important to underline that HES is a well-executed, high-quality business, and I have high conviction that the deal will indeed add a lot of value to shareholders of both companies. I will not go into deep details about HES here because I already reviewed its future prospects when I covered one of its major assets, Hess Midstream (HESM). The notable passage in the HESM article covers its parent company, Hess Corporation.

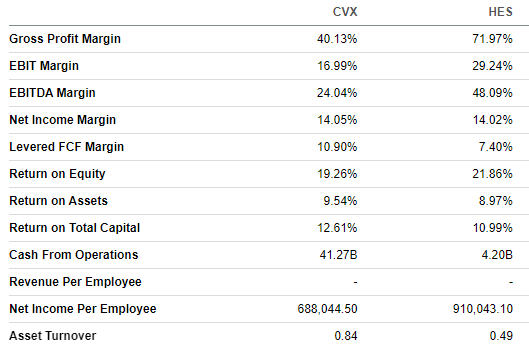

It is difficult to assess how exactly will the business combination affect Chevron’s financial performance in the foreseeable future because there is vast uncertainty regarding potential synergies. But we can make assumptions. In the near future, it is apparent that CVX will face fees related to professional services to support the deal. Still, I expect them to be insignificant compared to the company’s scale. These amounts will definitely pay off because the profitability metrics of HES are substantially higher than CVX’s which means that Chevron will have a more favorable revenue mix. Apparently, HES is a company of much lesser scale compared to CVX, but I expect CVX’s operating profitability to expand as a result of new assets acquired up to a couple of percentage points. The financial performance of HES suggests that the acquisition is also likely to add about $1.5 billion in annual FCF for Chevron. To add context, it is about 6% of CVX’s TTM levered FCF, quite a notable portion.

Seeking Alpha

The substantial underinvestment in the oil and gas industry over the past decade when oil prices were mostly low, together with vast geopolitical uncertainties in oil-rich regions are two more positive catalysts for oil prices in the foreseeable future. The ongoing war in Ukraine, together with the isolation of the Russian economy due to sanctions, is another factor indicating that oil prices are likely to stay higher for longer.

Valuation

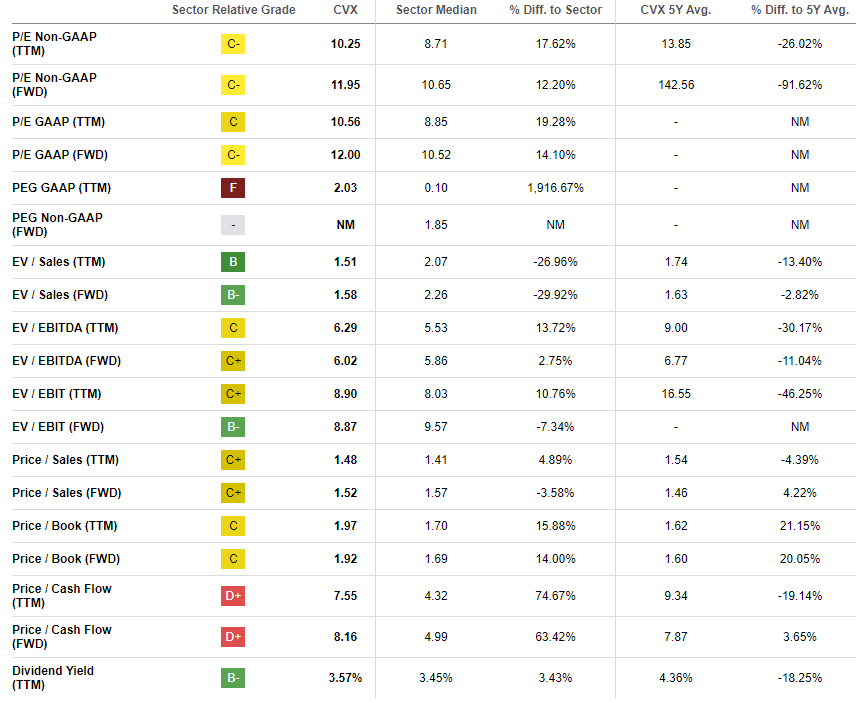

The stock price declined by almost 8% year-to-date, significantly underperforming the broader U.S. market. The stock also lagged behind the Energy sector (XLE), which showed a 5% year-to-date increase. Seeking Alpha Quant assigns CVX an average “C-” valuation grade since ratios analysis demonstrates mixed outcomes. For hyper scalers like Chevron, I prefer to look at historical averages; compared to them, the stock appears to be undervalued.

Seeking Alpha

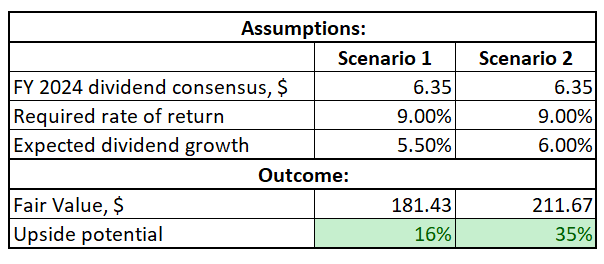

Due to the substantial volatility in commodity prices, I think a discounted cash flow simulation would be less appropriate here. Instead, I prefer to use the dividend discount model, especially given the company’s strong dividend consistency. I use a 9% WACC as a required rate of return. Consensus dividend estimates forecast FY 2024 payout at $6.35. The history of the company’s dividend growth pace has been uneven on different horizons, so I simulate two different scenarios depending on the dividend growth rate.

Author’s calculations

According to my calculations, the stock is very attractively valued even if a very conservative 5.5% dividend growth rate is implemented. I would like to emphasize that over the last five years, with the COVID-19 crisis for the oil industry considered, the dividend CAGR of CVX was at 6.03%.

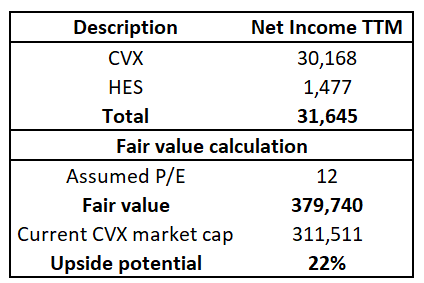

It is also crucial to underline that the DDM valuation analysis does not incorporate the value of assets, which will be added to the company’s balance sheet after the business combination closes. I will try to look at it from the prism of multiples, and P/E looks like a good choice to me. I take the combined TTM net income of the two companies and apply a conservative 12 P/E multiple to calculate the fair value of the combined entity. According to my calculations, the fair value for the combined business is $380 billion, which indicates a 22% upside potential.

Author’s calculations

However, I prefer to stick more to the DDM outcomes because there is still a lot of work to be done for the business combination to close, starting from getting all required regulatory approvals and ending with the complex integration of two large companies’ cultures and processes.

Risks to consider

Operating in the oil and gas industry means that Chevron’s earnings are extremely dependent on energy commodities prices. It is crucial to understand that oil prices are not only on the spot supply-demand equation but also on breaking headlines, rumors, and decisions of a few people from oil-exporting leading countries. And breaking news can go very far from the reality. For example, in October 2023, it might sound ridiculous, but in March 2022, the Russian Energy Minister warned the developed world that oil could hit $300 per barrel if Russian oil gets sanctioned. Nowadays, Russian oil is under sanctions, but the price never got close even to $200 per barrel. It is obvious that over the long term, all prices align with underlying equations, but over the short term, there can be massive overreactions in the oil market. That said, stock prices of all oil and gas companies are very volatile and highly dependent on the sentiment regarding crude oil prices.

It is also important to keep in mind that Chevron generates a substantial portion of its revenues outside the U.S., including countries with developing political institutions and high levels of political uncertainty.

Bottom line

To sum up, Chevron is a “Strong Buy”. The company is very efficient in absorbing strong industry tailwinds and has built up a fortress balance sheet in recent quarters. The FCF margin has expanded notably over recent years and the last news regarding Hess Corporation acquisition is a big strategic move where potential benefits are highly likely to outweigh integration risks. The forward dividend yield is also a good positive factor for potential investors, especially considering the company’s stellar track record of dividend hikes.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.