Summary:

- Chevron Corporation offers $60 billion to acquire Hess Corporation following Exxon Mobil Corporation’s acquisition of Pioneer Natural Resources.

- The Hess acquisition includes a 30% stake in the Stabroek Block off the coast of Guyana, which has significant production potential.

- Chevron’s acquisition is seen as an expensive bet on oil prices, with the long-term success depending on market demands.

DancingMan/iStock via Getty Images

Chevron Corporation (NYSE:CVX) has made its move. The company has responded to Exxon Mobil Corporation’s (XOM) acquisition of Pioneer Natural Resources Company (PXD) with its own, offering $60 billion to purchase Hess Corporation (NYSE:HES), a company we’ve recommended before. As we’ll see throughout this article, this is an important investment for Chevron, but doesn’t alleviate long-term risk.

Transaction Terms

The transaction is a pure equity acquisition, which is something we’re not a fan of. The company is leveraging its equity versus utilizing its cash, leveraging the downside impact to investors.

Chevron Investor Presentation

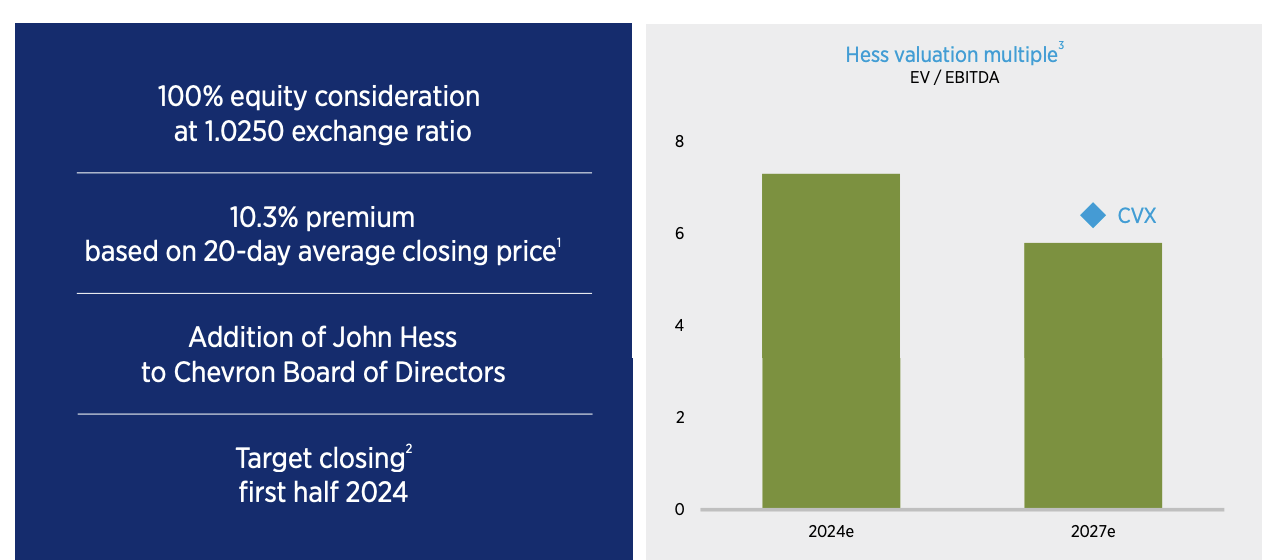

The acquisition is 100% equity at a 1.025 exchange ratio. It’s a 10.3% premium to Hess Corporation’s share price, which is near all-time highs, and as a result, it’s pushed down Chevron’s share price. John Hess, a legend in the industry, will join Chevron’s board and the closing target is 1H 2024. The EV to EBITDA multiple is above Chevron’s current level, but should decline.

It’s definitely an expensive transaction, but it does have some benefits that make Chevron still interesting.

Guyana

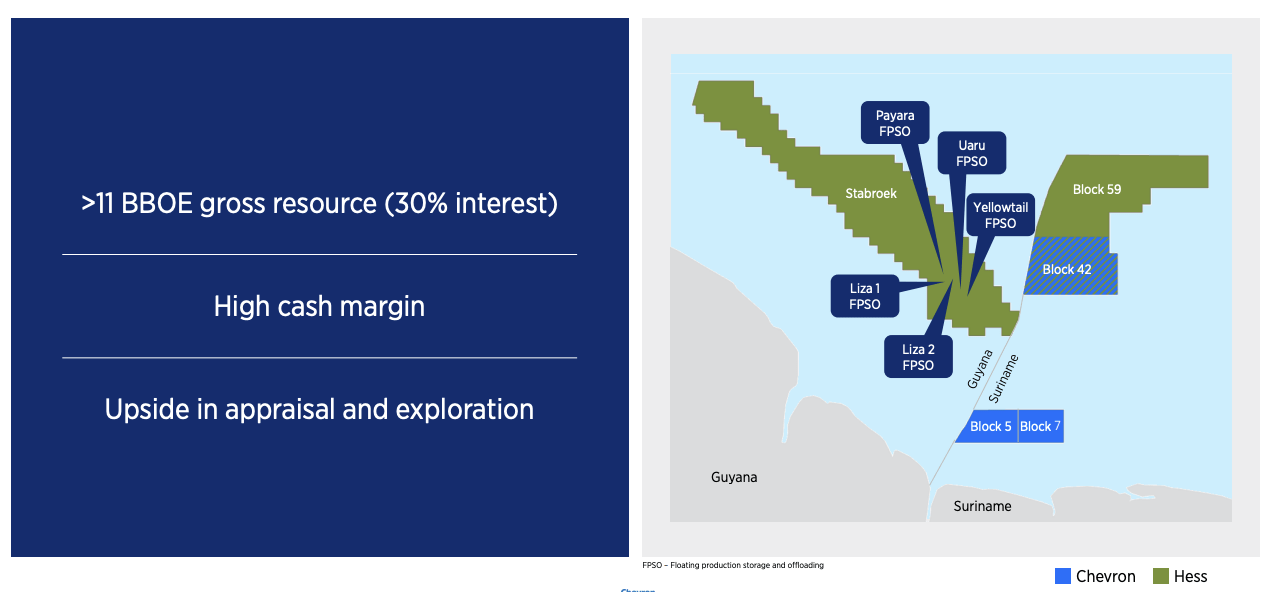

The prime benefit of the acquisition is Hess Corporation’s prior acquisition of part of the Stabroek block from Royal Dutch Shell.

Chevron Investor Presentation

One of the largest discoveries in recent years, the acquisition consists of more than 11 billion barrels in reserves, which Hess Corporation, and now Chevron, will have a 30% stake in. It’s a high cash margin acquisition, with strong upside. Chevron has complimentary assets, but none of Chevron’s assets are at the point where they’re producing.

The Stabroek Block has a path to >2 million barrels / day in production, which means hundreds of thousands of barrels of high margin production for Chevron.

The Other Assets

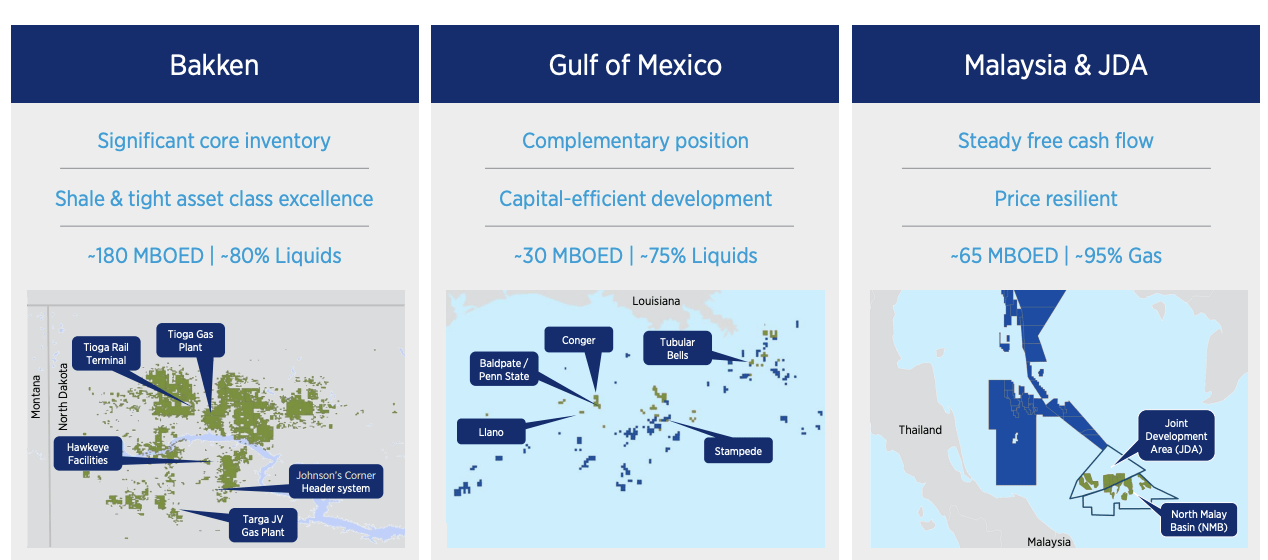

Chevron is also getting a number of other interesting assets.

Chevron Investor Presentation

Most of these assets don’t necessarily have strong growth potential, but they have strong cash flow potential. In the Bakken, the assets mean 180 thousand barrels / day of 80% liquids with strong backing infrastructure. In Malaysia and JDA, it means 65 thousand barrels / day primarily gas with strong contracts to back it up.

In the Gulf of Mexico, there are likely some synergies from acreage close to Chevron’s, which will lower the cost of development, but production is not cheap enough for it to be massively significant.

Forecast

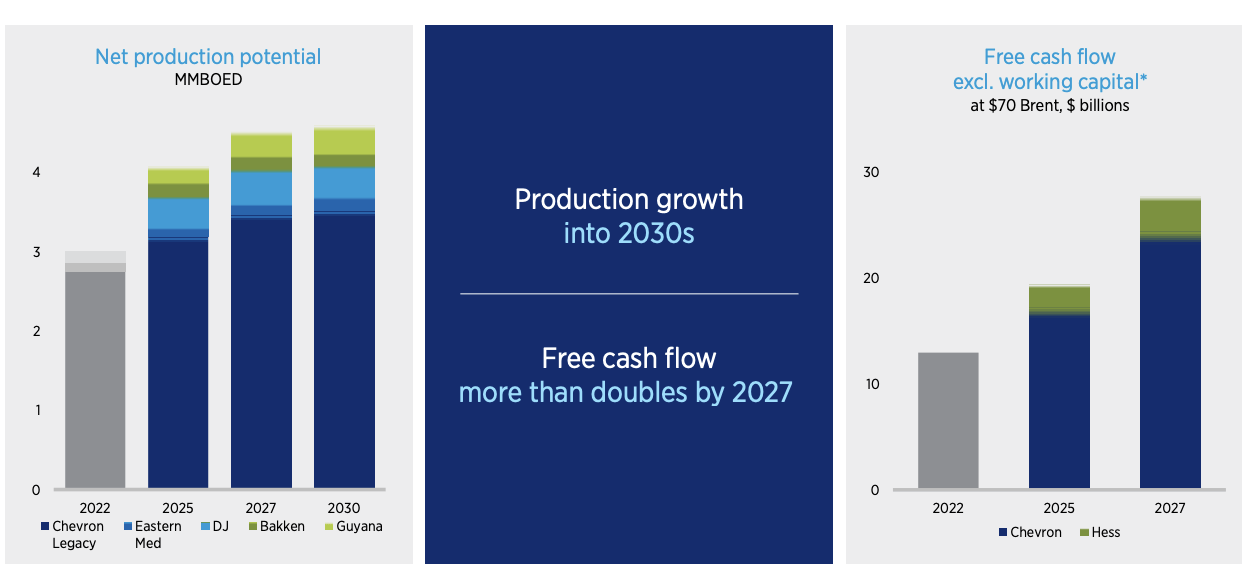

The net result is substantial growth for Chevron, at an expensive cost.

Chevron Investor Presentation

The net production potential comes from growing Guyana production, along with growing DJ basin production. The net forecast is production crossing 4 million barrels in 2025, and continuing to grow into the end of the decade. However, free cash flow (“FCF”) is expected to grow even faster, supported by Hess Corporation, with 2027 FCF estimated to be ~$28 billion.

Versus the combined company valuation of almost $325 billion, and 2027 forecast of almost $30 billion in FCF, that’s an almost double digit FCF yield. More so, the growth doesn’t end in 2027. Guyana will keep growing to the end of the decade, and capital spending will come down as well. We expect that to be reflected in Chevron’s cash flow.

Our View

Chevron clearly had to respond to Exxon Mobil’s acquisition of Pioneer Natural Resources, and they have.

However, we think they made several mistakes.

- An expensive stock-based acquisition makes it harder to drive long-term returns.

- Guyana is a company-maker asset, but the remainder of the assets do not have strong synergies.

- An oil focused acquisition with minimal alternative businesses show Chevron not adopting to the realities of climate change.

Despite all of that, given the raw strength of Guyana, we expect the acquisition to pay-off well for Chevron, especially going into the latter half of the decade. The 2030s will be profitable, but the long-term depends on the demands on the oil market.

Thesis Risk

The largest risk to this thesis is oil prices. Despite Chevron’s claim that the company was thinking about it prior to Exxon Mobil’s mega acquisition of Pioneer Natural Resources, that acquisition likely moved Chevron’s work forward. An expensive stock-based acquisition needs higher oil prices to pay off, and there is no guarantee of that.

The company made a leveraged long-term bet on oil prices, which is worth paying close attention to.

Conclusion

Chevron’s acquisition of Hess Corporation is a big deal. Exxon Mobil acquired Pioneer Natural Resources, and Chevron has responded in a big way. Most importantly, Chevron has purchased a 30% stake in the Stabroek Block off of the coast of Guyana. The company expects to see strong FCF growth in the coming years that continues to the end of the decade.

The FCF yield is expected to move towards 10% by 2027, and synergies should help long-term. Going into the late 2020s what happens remains to be seen, but we recommend paying close attention. At the end of the day, we still see Chevron Corporation stock as a valuable long-term investment. Let us know your thoughts in the comments below.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CVX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

You Only Get 1 Chance To Retire, Join The #1 Retirement Service

The Retirement Forum provides actionable ideals, a high-yield safe retirement portfolio, and macroeconomic outlooks, all to help you maximize your capital and your income. We search the entire market to help you maximize returns.

Recommendations from a top 0.2% TipRanks author!

Retirement is complicated and you only get once chance to do it right. Don’t miss out because you didn’t know what was out there.

We provide:

- Model portfolios to generate high retirement cash flow.

- Deep-dive actionable research.

- Recommendation spreadsheets and option strategies.