Summary:

- Comcast’s upcoming earnings report is expected to show a slight decline in revenues year-over-year, but expect margins to remain or slightly improve.

- The company’s outstanding debt is still not an issue, in my opinion.

- The performance of Peacock TV will be closely watched, with hopes for lower losses and continued subscriber growth.

- A buy recommendation and PT remain the same.

SOPA Images/LightRocket via Getty Images

Investment Thesis

Comcast (NASDAQ:CMCSA) is about to report its FY23 earnings on the 25th of January, so I wanted to take a quick look at how the company’s financials developed since my last coverage and take a look at what to expect from the upcoming report. I’m not expecting any major top-line growth from the company, but I would like to see margin improvements. Peacock TV has a lot of potential but is very far from being a profitable segment. Nevertheless, I believe the company is still undervalued and still has some room to grow if it continues to improve its efficiency and profitability going forward, even with the lack of top-line catalysts.

Update Since the last Coverage

The last time I covered the company was back in April of ´23 when I argued that the CMCSA doesn’t necessarily need robust top-line growth to create value, as long as it can become more efficient by improving its margins. So, let’s take a look at how some of the company’s metrics have evolved over the last few quarters.

As of Q3 ´23, the company accumulated $6.4B in cash and equivalents, against a whopping $94B in long-term debt, which has just gotten slightly worse since April of last year. I don’t think it’s still a problem for three reasons. First, the company’s debt-to-assets ratio is around 0.36, and anything under 0.6 I consider to be not overleveraged. Secondly, the company’s debt-to-equity ratio is 1.15, and anything under 1.5 is acceptable to me. Lastly, and the most important out of the three solvency metrics, is the company’s ability to cover its debt obligations in terms of annual interest expenses. As of nine months ended Sept. 30, the company’s interest coverage ratio stood at around 6, which means that the company can easily cover the expenses with the operating income received, six times over as a matter of fact. As I mentioned in my previous article, many analysts consider a coverage ratio of 2x to be sufficient, and the company passed even my more scrutinizing requirements of at least 5, therefore, CMCSA is not at risk of insolvency.

In terms of revenues, we can see the company’s steady yet slow increase in revenues over the last year, which is as expected. The company doesn’t seem to have any catalysts going for it, so I don’t expect its top line to grow any faster than it does right now.

Revenue growth (SA)

In terms of margins, we can see that the company’s bottom line has improved substantially once the impairment charges went away. Around $8.5B in goodwill and long-lived asset impairments, which led to around 700bps improvement in the bottom line, while gross and EBIT margins stayed relatively stable over the same time.

Margins (SA)

Continuing on efficiency and profitability, we can see that the bottom line improvements helped the company’s ROA and ROE metrics massively. It seems that the management is using the company’s assets and shareholder capital much more efficiently now. Furthermore, the company’s ROTC has seen the same improvement over the last while, which tells me that the company is gaining some sort of a competitive edge.

Efficiency and Profitability (SA)

So, we can see that over the last while, once the company got rid of the impairment charges, the company’s profitability and efficiency substantially improved. Everything is trending upward, which is what I like to see. I do still think that many investors will tend to avoid the company due to its massive debt pile, but as I showed you above, the debt is not that big of a risk, as it looks like it’s manageable.

Upcoming Earnings

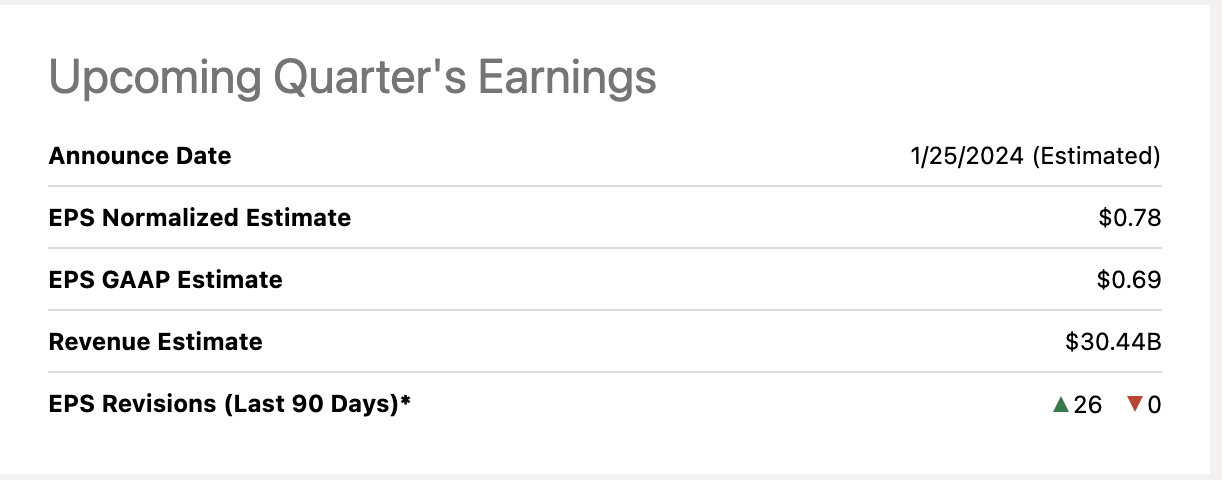

The company is going to announce its Q4 earnings on the 25th of January, so let’s see what the numbers look like.

The company’s EPS GAAP and adjusted are estimated to be $0.69 and $0.78, respectively, while revenues expected to be at around $30.44B, which is an increase of around 1% sequentially and a slight decline year-over-year of around 30bps, so as expected nothing exciting on the top line growth, on thing to note, the company had 26 EPS provisions to the upside in the last 90 days, which may also mean that it may eke out a beat when it reports in a few days.

Earnings estimates (SA)

Speaking of beats, the company managed to beat an estimated 12 out of the last 12 quarters, so it’s likely the company will beat estimates this time around too, unless we see a disastrous report.

Earnings History beats (SA)

Comments on the Outlook

In terms of revenues, I don’t expect to see much growth here. It looks like the company has penetrated all that it can in terms of cable communications and will continue to see subpar growth going forward.

Cord cutting may impact the company’s cable segment and I expect to see slowing subscriber growth in this sector, however, some of it may be offset by higher broadband speeds and data usage.

I’m very eager to see how Peacock’s streaming service develops. The company expects to see lower losses from the service, as the management updated their outlook from $3B in losses to around $2.8B. The service has seen a big growth in subscriber count over the last year, and it doubled in the third quarter from a year ago. I would like to see this momentum continue, and if there’s a substantial slowdown, investors will not take it lightly and I would expect to see a lot of volatility on the day of the announcement. It will take a long while for the company to start making money from the service, however, as I said in my first article, if the company continues to invest heavily in this segment and make the right decisions, it will eventually turn profitable.

I also would like to see the company at least retaining the margins it has right now, however, I wouldn’t be surprised if we do see some deterioration because of increased spending on content in relation to Peacock TV and its traditional cable channels. As long as the increased spending turns into long-term gain in terms of attracting and retaining customers, I’m fine with that.

I’m also eager to hear what the management has to say about the outlook going forward for 2024. I will tune in to hear the earnings call on the 25th and will try to get a feel of the management’s tone about the future developments in the streaming service, its cable segment, and also the theme parks.

Closing Comments

Overall, I believe the company will not surprise us too much on the day of earnings. I do believe we will see a slight beat on all important metrics. However, I’m going to be looking for the management’s guidance and the overall tone of the whole team. Even if the company beats estimates, we could see a meltdown in share price if investors are not going to be happy with the guidance.

My recommendation and PT of around $50 a share remains the same as I believe the company still is rather undervalued and in the long run should be a great investment if the company continues to improve its margins. Furthermore, if the company manages to revitalize its top line growth, that is going to be the cherry on the cake, but I’m not holding my breath on that front.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.