Summary:

- SuperMicro stock dropped 20% in one session after a disappointing announcement, part of a broader decline from overbought levels in March.

- Dell stock has also experienced a considerable pullback, down about 52% from its all-time high, with concerns about profitability and market expectations.

- Both Dell and SuperMicro are currently trading at cheap valuations, with potential for substantial growth in the future. Dell is seen as the safer investment option.

Hispanolistic/E+ via Getty Images

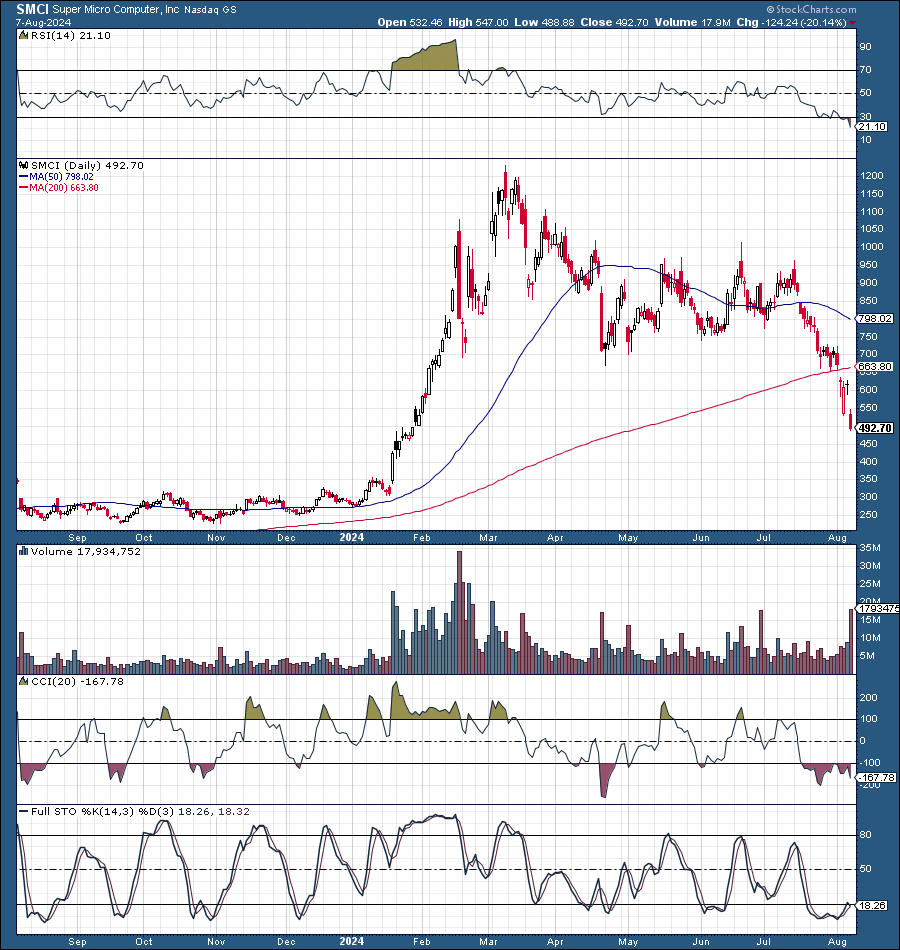

SuperMicro (NASDAQ:SMCI) stock, aka SMCI, dropped by a whopping 20% in one session after reporting a “mixed earnings” announcement. The latest drop is just an extension of a broader decline stemming from the highly overbought levels achieved last March. From peak to trough, SMCI has declined by about 60% from an ATH above $1,200 to below $500 today.

SMCI 1-Year Chart

SMCI (stockcharts.com )

SMCI has returned much of the gains achieved in the massive run-up early in the year. We are seeing a seismic shift. Whereas SMCI was extremely overbought in February, March, and April, SMCI is deeply oversold now. The stock has been in a downtrend for more than four months, and the atmosphere appears filled with panic selling now as the RSI approaches 20, and other technical indicators illustrate that SMCI is highly oversold. Also, it’s more than just SMCI. Dell, another hardware AI leader, has been under significant pressure for months.

Dell 1-Year Chart

DELL (stockcharts.com)

Dell (NYSE:DELL) has experienced a considerable pullback. The stock is down about 52% from its ATH. The drop has been remarkable, and the magnitude of the downturn has been more significant than many imagined. Dell’s stock has been in free fall over the last month, dropping from around $150 to below $90. The RSI is also approaching 20, and the technical conditions are deeply oversold.

What’s Wrong With Dell and SMCI?

What is wrong with stocks like Dell and SMCI? These two companies are supposed to be the AI hardware leaders. Yet, their stocks behave like the good times are about to end. There are concerns that elements surrounding AI are in a bubble. Also, there is uncertainty about whether the recent highly profitable period could persist or if it offers simply a temporary opportunity. Furthermore, the market’s expectations were sky-high, and “mixed results” simply aren’t cutting it.

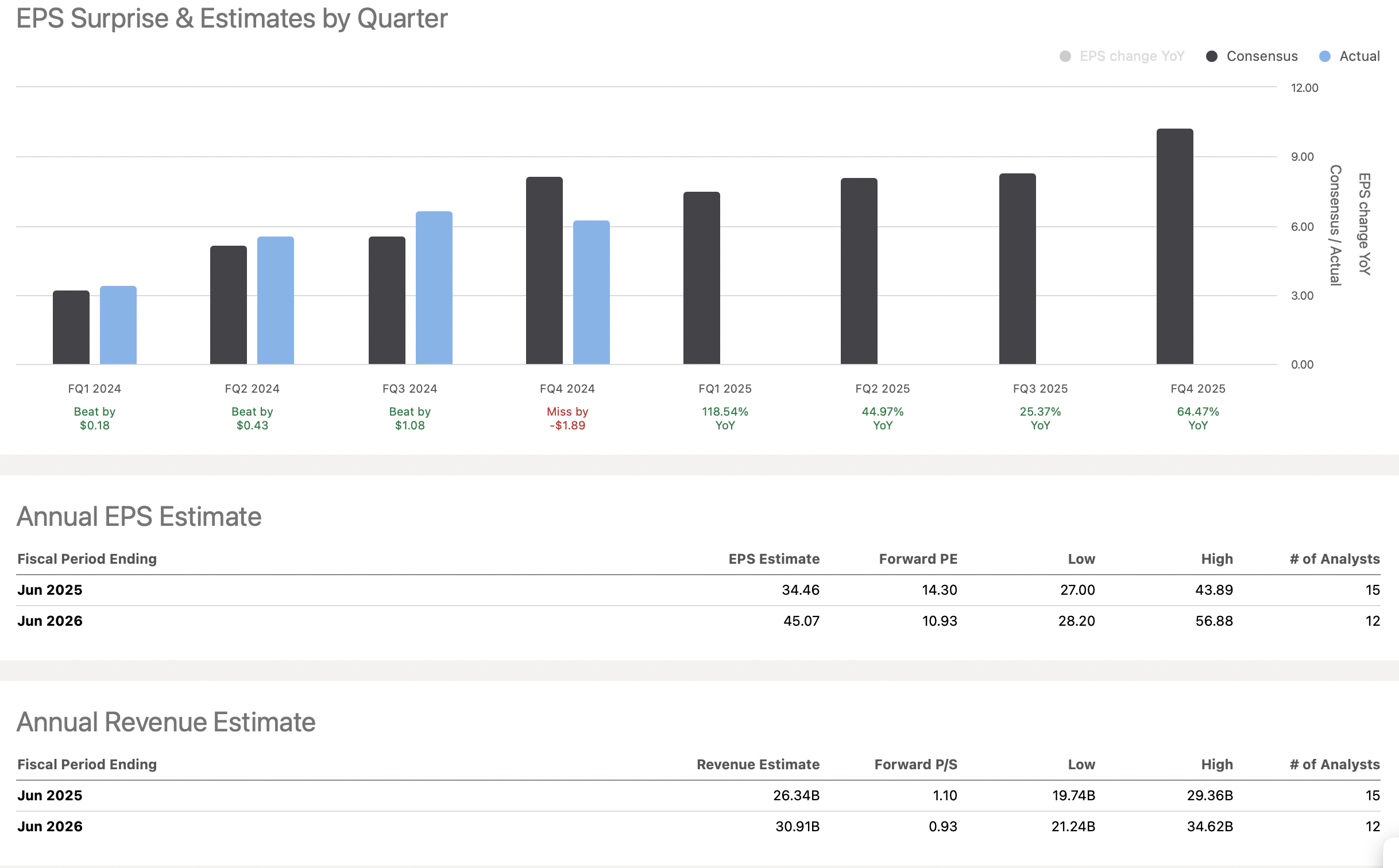

Nonetheless, much of the AI hype has been deflated by the valuations of Dell, SMCI, and other high-quality AI players. For instance, after the drop, SMCI trades around ten times next year’s EPS estimates, which is cheap. Moreover, SMCI trades below one-time forward sales, which is also inexpensive.

SMCI EPS Vs. Estimates

EPS vs estimates (seekingalpha.com )

Consensus estimates are for around $35 in EPS in fiscal 2025 and roughly $45 in EPS in fiscal 2026. This dynamic implies that SMCI trades around ten times forward estimates, but Dell is even cheaper here.

Dell EPS Vs. Estimates

EPS vs estimates (seekingalpha.com )

While the consensus estimate is around $9.36 for next year, Dell could outperform. The consensus estimate may be low, and Dell could deliver $10-$11 in EPS next year. Dell’s stock is below $90 now, suggesting its forward P/E ratio is only 8-9 here, which is dirt cheap. Dell has considerable growth prospects and should not trade at a value trap multiple below 10. Moreover, Dell could improve its profitability with scale and may deserve a 12-15 P/E multiple instead.

Dell Vs. SMCI In The Server Market

Dell is the global leader in the server market, controlling about a 20% market share. The AI server market is expected to grow to around $150B in 2027, much higher than the recent $30B sales figure. Therefore, there is plenty of room for growth for SMCI and Dell here. The excellent news for SMCI is that a much higher portion of its overall revenues come from AI-related server sales. Dell has a massive computer business, and AI servers account for a much smaller share of its revenues.

Still, Dell is a much bigger and more established company that has smartly gotten into the AI game early, making many critical partnerships. Additionally, Dell should benefit from its gigantic position in terms of scale, efficiency, profit stability, and other factors. Dell is the cheaper, safer stock. While SMCI may offer more excitement and higher risk/reward potential, I prefer to own Dell over SMCI, which is why I have a more significant position in Dell.

SMCI’s Mixed Results

SMCI’s mixed results provided less than anticipated profitability, which was the primary explanation for the stock’s poor reaction. SMCI reported GAAP EPS of $6.25, a $1.56 miss. Revenue came in at $5.31B, a 144% increase YoY. For Q1 (fiscal 2025), SMCI expects sales of $6-$7B vs. the consensus estimate of $5.45B. For fiscal 2025, SMCI anticipated $26-$30B in revenues vs. the consensus estimate of about $15B.

The street expected better-than-expected sales guidance figures. However, the negative surprise was lower-than-expected profitability last quarter. There is uncertainty regarding future profitability, and SMCI’s margins may get compressed more than expected. The market has a similar fear about Dell. Given that these are hardware companies, their hardware business margins can decline, mainly due to the increased competition and demand/supply dynamic.

The Takeaway – Likely, we’re witnessing an overreaction, and SMCI’s earnings may improve instead of falling further. SMCI explained that the recent drop in profitability was due to supply chain issues concerning their liquid cooling AI servers and that profitability would rise in future quarters. Also, this may be an SMCI-specific issue, and Dell may be immune from this transitory, less-than-expected profitability effect. Therefore, the market is likely overreacting here and is essentially in panic-selling mode. The truth is that Dell and SMCI are both cheap here, and their stocks have a high probability of moving substantially higher in future years.

Dell Or SMCI – Which Is The Better Buy?

While I like both companies, Dell is a better buy. Both stocks have gotten clobbered in the recent tech rout, but SMCI had a better reason for a significant decline, and it looks like Dell got dragged down for the ride. While SMCI provided excellent sales guidance, it reported worse than anticipated profitability, leading to mounting concern. On the other hand, Dell continues to fire on all cylinders, may not face similar profitability issues as SMCI, and could experience a more substantial rebound in its stock price. After all, an 8-9 forward P/E valuation isn’t just cheap; it’s dirt cheap, and Dell’s valuation likely won’t stay down here for long.

12-Month Price Targets

- Dell: $150-$180

- SMCI: $750-$1,000

Risks to Dell and SMCI

Dell and SMCI are in the hardware space, which typically has lower margins and higher competition than the AI software and services space. Therefore, Dell and SMCI could see margin compression in their industry, leading to lower-than-anticipated EPS growth and profitability. There is also the risk of overall lower demand for AI-related server products. A relatively slow economic environment and high-interest rates could also weigh on sales growth and profitability prospects. Investors should examine these and other risks before investing in Dell and SMCI.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DELL SMCI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I am long a diversified portfolio with hedges.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are You Getting The Returns You Want?

- Invest alongside the Financial Prophet’s All-Weather Portfolio (2023 47% return) and achieve optimal results in any market.

- The Daily Prophet Report provides crucial information before the opening bell rings each morning.

- Implement my Covered Call Dividend Plan and earn 50% on some of your investments.

All-Weather Portfolio vs. The S&P 500

Join The Financial Prophet And Become A Better Investor!

Join The Financial Prophet And Become A Better Investor!

Don’t Hesitate! Take advantage of the 2-week free trial and receive this limited-time 20% discount with your subscription. Sign up now and start beating the market for less than $1 a day!