Summary:

- Disney Plus is now profitable, and Disney currently has a historically low price to sales and price to book ratio.

- Joel Greenblatt highlights that media companies with high intangible assets and goodwill are better evaluated on EBITDA for profitability.

- Despite improving movie quality, setting record box offices, Disney’s stock remains in the doldrums.

HAYKIRDI

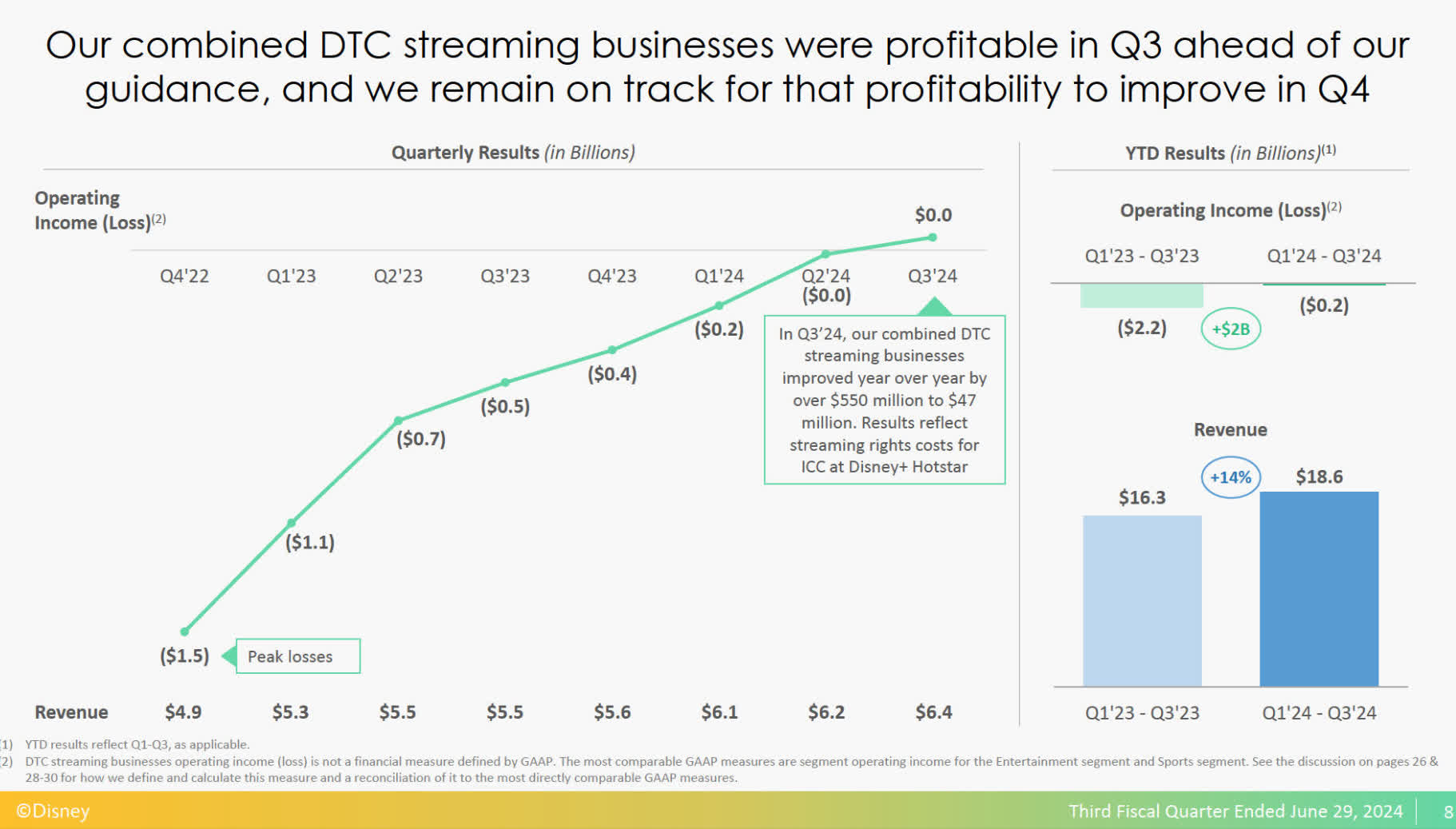

Disney Plus is turning a profit

DisneyQ3 2024 Presentation

Having covered Disney (NYSE:DIS) a few times now:

Disney: Why You Should Buy And Hold Forever

Disney: Forget Disney Plus, The Magic Kingdom Hit My Magic Number

This round trip back to deep-value territory has me adding again. The thesis was built around a modified Graham Number, substituting EBITDA per share for earnings per share while utilizing a Graham Number model to come up with a price target. This model is really only useful when an asset-heavy company is getting such low returns on assets that the market values their company at around 1.5X book value or lower.

In this modern era of Mag 7 tech giants who are asset-light and generate returns out of pure intellectual property creation, the market currently does not have a large appetite for asset-heavy companies. However, we can see above that Disney Plus is finally crossing over break even and has turned a slight profit, now making this a legitimate play divided between an asset-heavy parks and leisure company and one of the challengers to Netflix’s (NFLX) throne in the streaming wars.

Disney is a strong buy at these levels just for the hard asset value alone. Future growth in streaming is just an added “plus”.

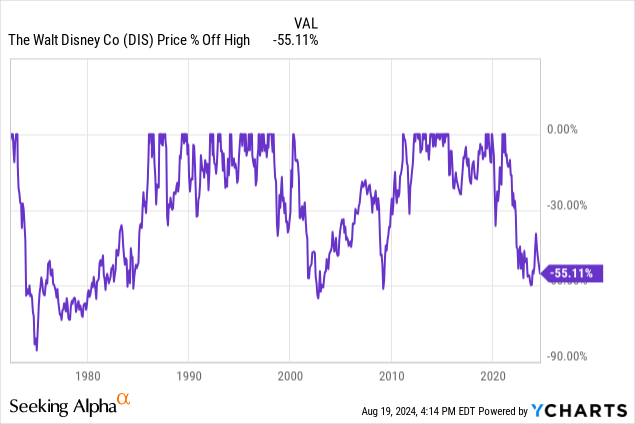

Percent off high

Being not alone as a Dow 30 component thrashed by -50% or more off of the all-time highs, Disney is a stock that bounces higher and then retests this level pretty consistently. Profitability growth is just now making a turn, which will be the key element to send the stock off of these low levels for good. I believe it is on the near horizon, but could take some time. If you’re looking for a quick re-rate higher, this might not be the stock for you. For the patient investor, I believe Disney will pay off handsomely.

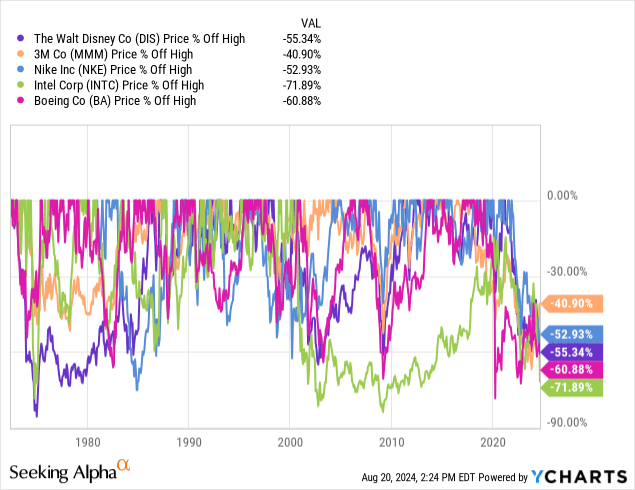

Here is a highlight of some of the worst performers in the Dow 30 over the past few years that I have been adding to:

- The Walt Disney Company: -55.34% off ath

- 3M Co. (MMM) : -40.9% off ath

- Nike Inc. (NKE) : -52.93% off ath

- Intel Corp. (INTC): -71.89% off ath

- Boeing Co. (BA): -60.88% off ath

As one of my investment strategies is to “self-index” the Dow 30 components being that it is the only price-weighted index and the easiest one for the everyday investor to match, I own all 30. I have let off the gas on 3M and of these worst of the worst, I only find Disney, Nike, and Intel compelling from a valuation perspective.

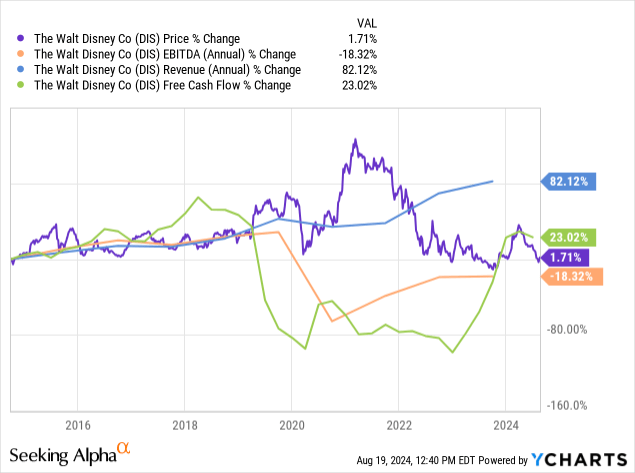

EBITDA to price

Herein lies the flaw in the Disney thesis. Share price growth over 10 years still remains above EBITDA growth, which has cratered due to the cash burn of Disney Plus [which is now self-sustainable] combined with the collapse of DTC cable programming. This is both a new business and a transition away from linear. The great thing is the linear can all be migrated to streaming. The bad news is a lot of this will cause ongoing impairment of assets that hurts GAAP profitability. Therefore, I am solely watching EBITDA during the recovery phase.

There is still a 19% gap between EBITDA crossing over price. I think this will happen quicker than most assume with the aforementioned self-sustainability and growth in Disney Plus. Concern over a looming recession and weaker park numbers are also present, but I am less worried about that cash cow business. The parks are tourist destinations as much for foreign visitors as for domestic markets. They are must-see locations when first visiting any of the major “tier 1” cities where the parks reside.

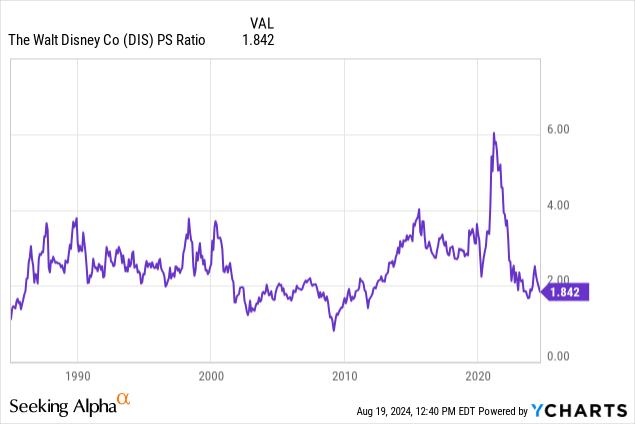

Historical price to sales

I’ve noted in previous articles that price to sales on Disney less than 2 X are historically rare and have only occurred post-tech bubble, the 08-09 GFC, and this current period of company realignment.

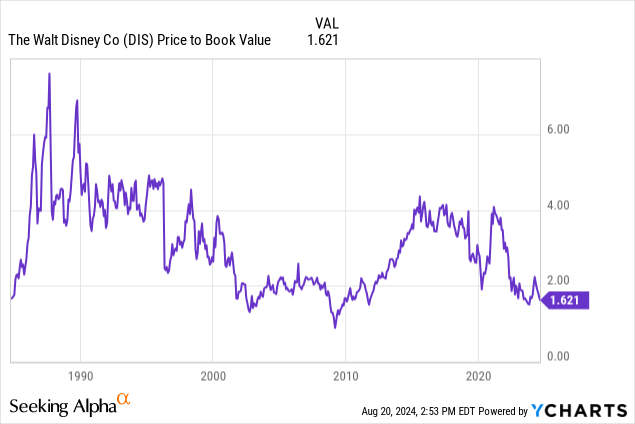

Even more rare is the price to book value. These are also levels we have not seen outside of our prior two financial crises, either.

Remember, most assets on the balance sheet are recorded at cost minus accumulated depreciation [when addressing Disney’s vast real estate empire].

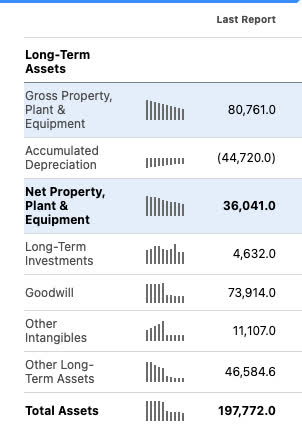

SeekingAlpha

As real estate typically appreciates [especially land], it would not be out of the question to view just the gross PPE line as having a value of 2-3X greater than it currently stands, or about $160-$240 Billion USD. While the PPE is inclusive of equipment, getting fee simple or leasehold estates of acres and acres of contiguous tracts of land put together in the heart of Anaheim, Tokyo, Hong Kong, Paris, or even Orlando at this point wouldn’t be just difficult, it might be impossible.

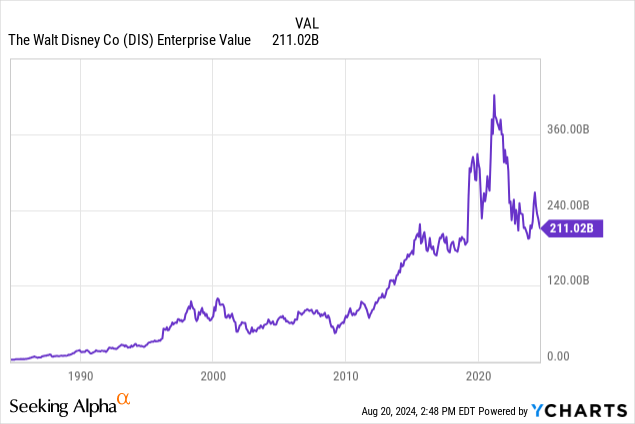

With the enterprise value of Disney [the amount of cash required to take out both the debt and the equity] at $211 Billion USD, I would say a happy theoretical buyer from Saudi Arabia or the UAE would be getting the land at a discount and the streaming and media business for free. Not that it would ever happen, but trading Disney at book values lower than this level seems irrational.

A note on media companies from Joel Greenblatt

As I noted in a previous article regarding Comcast (CMCSA):

Joel Greenblatt pointed out in his book You Can Be A Stock Market Genius, media companies invariably trade on cash flow or EBITDA versus GAAP.

The reason for this is the large amounts of depreciation on equipment and amortization of intangible assets/intellectual property. The non-cash expenses outstrip the depreciation and amortization. A very positive indicator. This was also outlined in the Cap Cities/ABC case studies when Warren Buffett helped arrange the acquisition of ABC. The large non-cash expenses ongoing compared to smaller capex were part of the appeal in the deal.

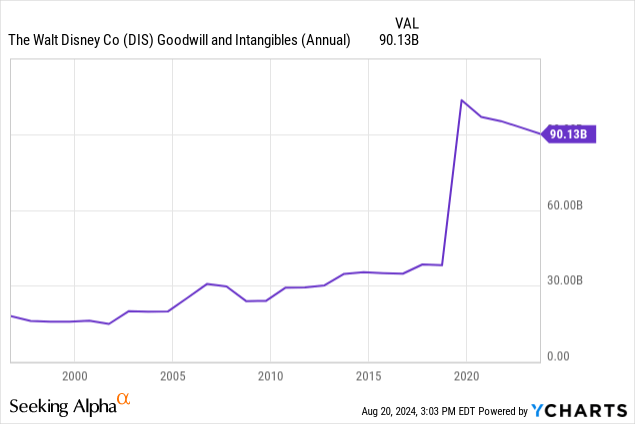

While Disney was more of an organic content creator versus a serial acquirer regarding their media business priorly, we know that story has changed. Marvel 2009, The Star Wars Universe 2012 [Lucasfilm], and The Simpsons are three-storied non-Disney creations that were either fully acquired or licensed. This creates a lot of goodwill to amortize.

We can see Goodwill and Intangibles skyrocket after the pivot to acquisitions took off. Combine this with the depreciation of buildings and equipment, and you have a lot of write-offs to carry forward.

SeekingAlpha

We can see the depreciation line has stayed relatively flat, but amortization has 7X’d since 2015.

SeekingAlpha

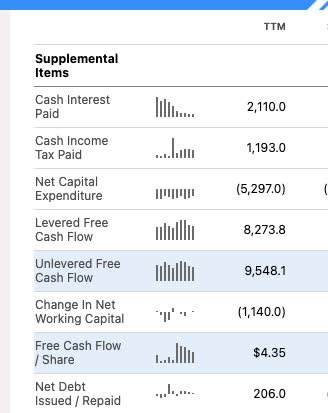

The company is now producing $4.35 of free cash flow per share or a free cash flow yield of 4.8%, well above the current risk-free rate and well poised for growth now that most of the negative CAPEX drag in excess of cash from operations regarding Disney+ is behind us.

The parks do have some big CAPEX on the horizon, as legitimate competition from Comcast’s Universal Studios is keeping them on their toes.

DisneyQ3 2024 Presentation

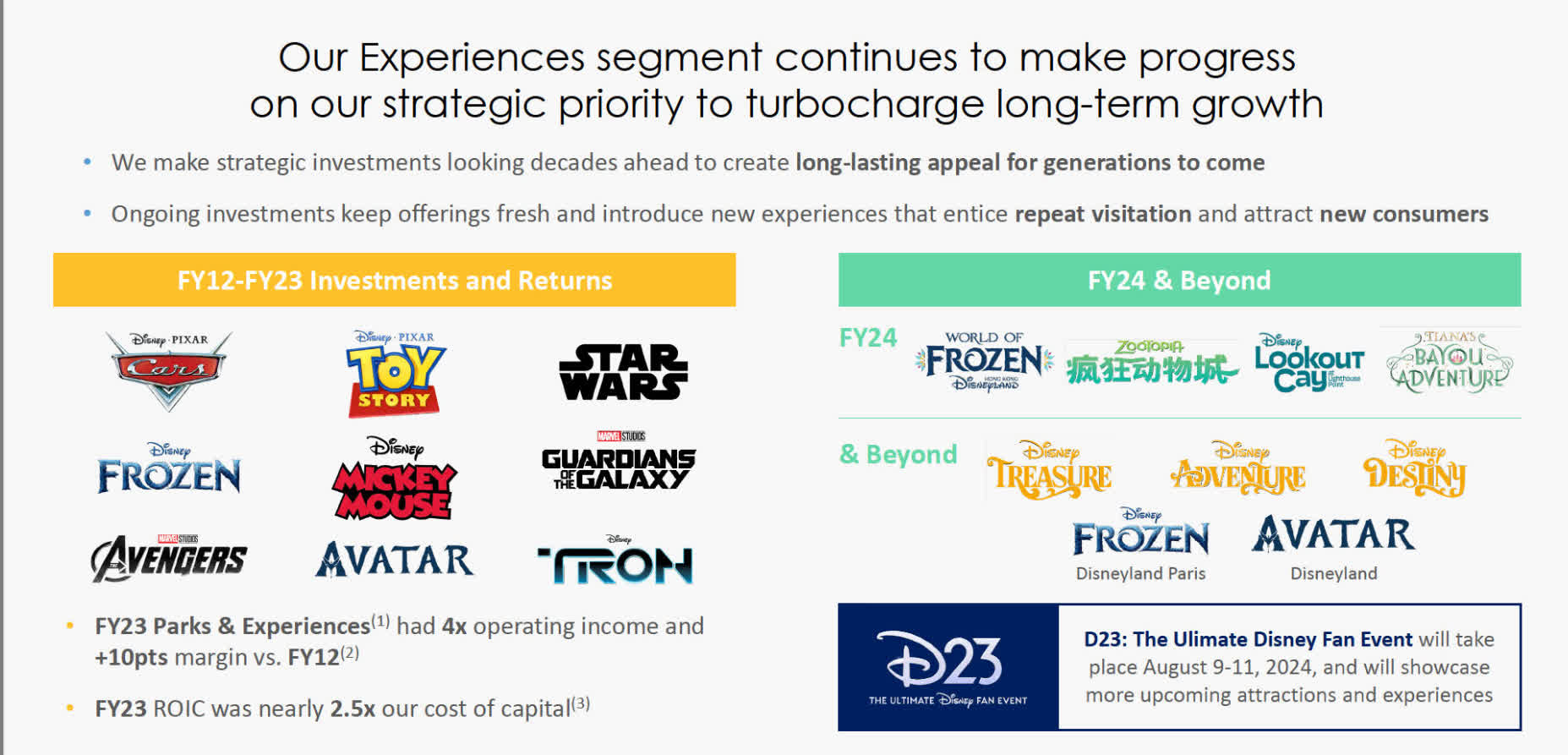

Increased growth CAPEX at parks and now a pivot to more maintenance level CAPEX for streaming should be welcome. If previous numbers for 2023 ROIC of 2.5 X cost of capital for the experiences segment holds up, this should further improve free cash flow numbers.

DisneyQ3 2024 Presentation

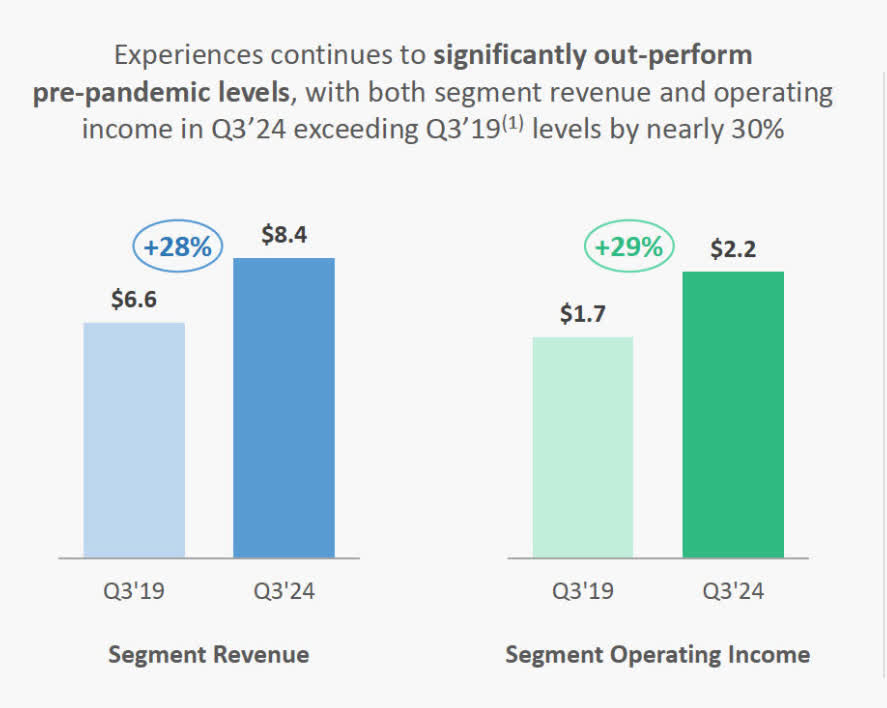

With Disney recently pointing out pre-pandemic revenue and operating income to have increased nearly 30% since 2019, this growth is not just pent-up demand from quarantines, it is organic growth that has tracked inflation and also includes Disney park’s moat-like pricing power. While we should expect waxing and waning from consumer traffic, the long-term trend to track inflation + is promising with continued improvements in park offerings.

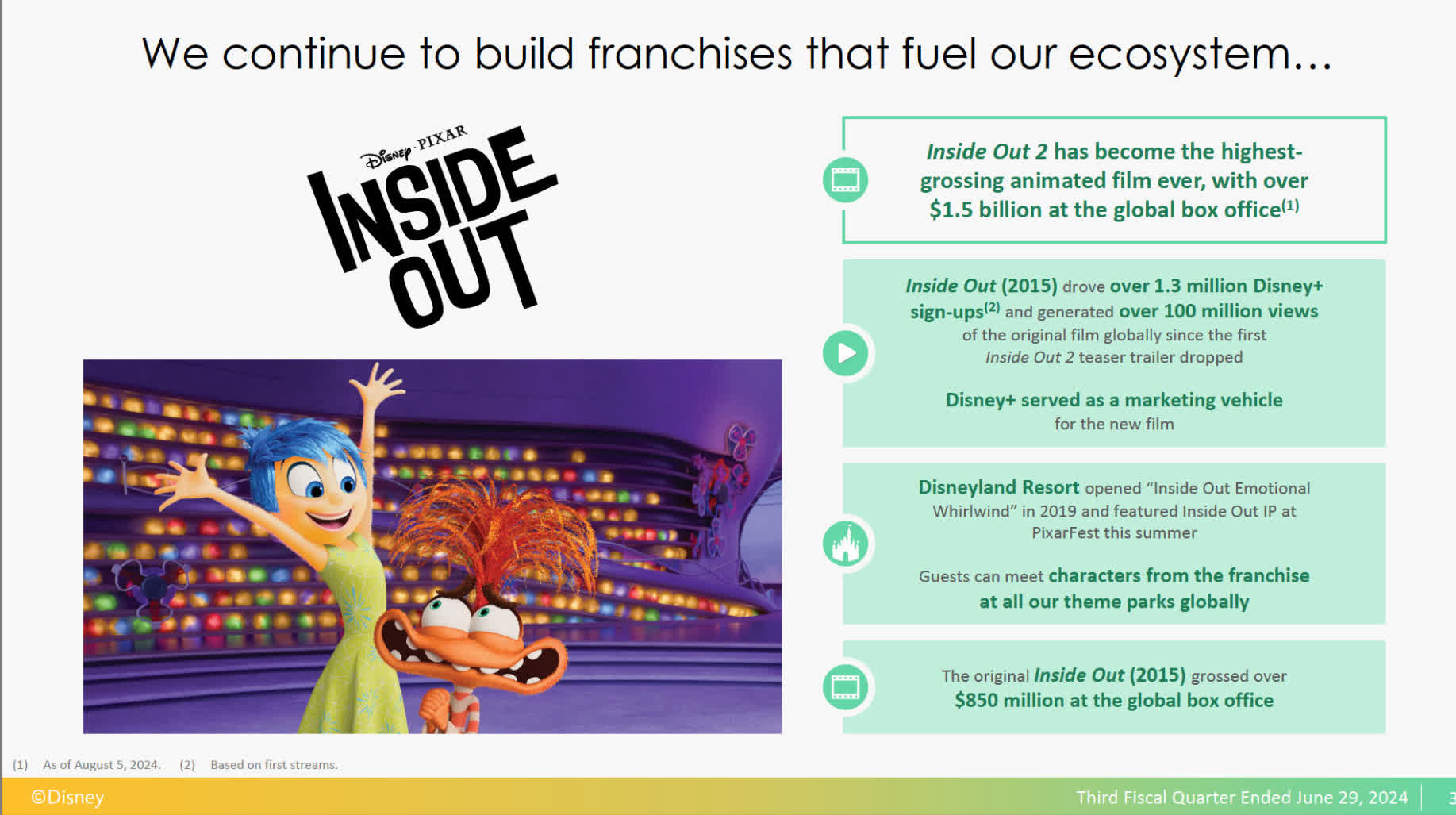

Movie quality is improving

DisneyQ3 2024 Presentation

Disney has now produced a couple of unexpected hits. “Inside Out 2”, just grossed more than any other animated film and is an in-house Disney creation. I did see this film and was pleasantly surprised by how good it was compared to what I’ve seen the past few years out of Disney offerings. There was a nice parent/kid, something for everyone comedic mix that didn’t serve up jokes that fell flat. A lot of it reminded me of “Wreck-It Ralph” in its writing style.

“Deadpool & Wolverine” also became the top R-rated film in movie history, crossing over into the $1Billion club. With CEO Bob Iger having his original background in television and film production, he must be most proud to finally see this segment turn around and produce some bona fide hits.

Update on modified Graham Number Valuation

To reiterate, I believe Disney now qualifies more as a media business than a parks and leisure business due to all the built-up goodwill from acquisitions. As Greenblatt mentioned, these companies are better evaluated on an EBITDA or cash flow basis. The Graham Number is the fair price where the price to book X the price to earnings ratio does not cross a line of 22.5. An example would be P/E 10 * P/B 2.25 would be a 22.5 stock.

In this case, we are substituting EBITDA/share as our profitability measure. To get a price target, we use the formula Square root (22.5*Book value*EBITDA/share).

- TTM Book Value : $55.41

- TTM EBITDA $16.751 Billion/ 1.831 Billion shares= $9.14 EBITDA/share

- Square root ($55.41*$9.14*22.5)=$106.74

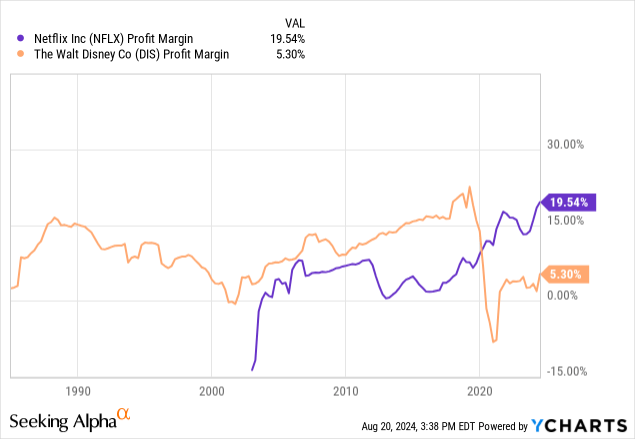

Examination of Netflix margin expansion

With Netflix being the gold standard in streaming execution, the ultimate goal is to hit their margins on a long-term basis for any streamer. If we consider that the streaming business will eventually represent 50% of Disney’s profit, and assuming that Disney+ profit margin is now at break even or 0%, ramping up to Netflix profit margins should eventually tack on another 9.77% in profit margin should experiences remain static [19.54 X 50%= 9.77% if streaming is half of the business]. That would put Disney at right around a 15.07% profit margin if Disney Plus executes to the level of Netflix.

Even if they don’t, and we say Disney conservatively gets to 12% profit margins, that would still result in over $10 Billion in net income when taking into consideration the TTM of $90+ Billion in revenue and growth to come. That would equate to a $5.9/ share EPS or 15.25 X forward GAAP earnings if you believe that Disney can get to 75% of Netflix’s profitability. With ads now integrated as Hulu and ESPN fully accessible in the Disney+ app, I am personally optimistic.

As linear goes away, I expect both Netflix and Disney to actually achieve higher and higher margins as more and more consumers are pigeonholed into streaming as their sole source of television viewing.

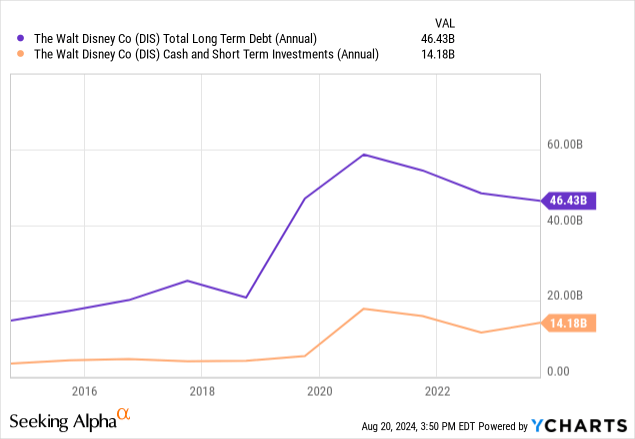

Balance sheet analysis

Disney remains a debt-heavy business but in the near term, is paying down their debt loads from the Covid era Disney+ startup days, and we see an upward trend line in cash and short-term investments. This is another indication of a turnaround execution to where the primary debt aggregator [Disney Plus] is now self-sustainable and excess cash can be used to reduce debt.

Risks and summary

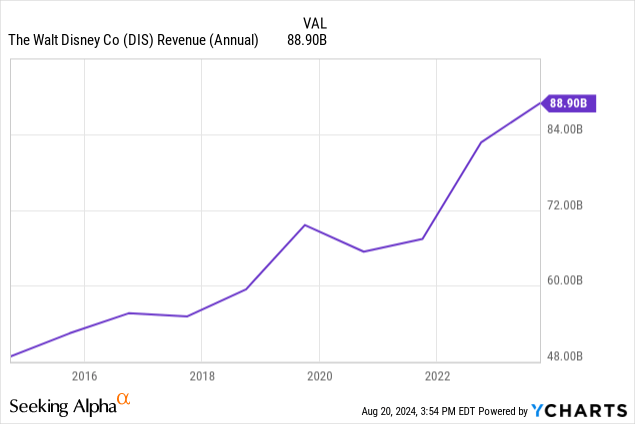

The balance sheet is still debt-heavy, but without Disney+, the company’s DTC business would have been dead in the water. The transition was messy but necessary. The revenue generation from this add now seems to be well worth the wait and debt encumbrance, as we can see, revenue took off with the creation of the streaming business:

Tome, I can see the turnaround in the charts, statistics, and numbers. Disney has a wide enough moat that recessions don’t deter me from investing in a very consumer-discretionary business. The biggest risk in my eyes is global war or tensions that slow down travel or don’t permit as many visitors to enjoy the parks as they normally would have outside of travel advisories.

That risk is one I’m willing to take, as I am ever an optimist that the world will work out its differences, especially the developed nations that rely on each other economically. Disney is a strong buy in the low $90s and under.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DIS, CMCSA, BA, INTC, NKE, MMM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The information provided in this article is for general informational purposes only and should not be considered as financial advice. The author is not a licensed financial advisor, Certified Public Accountant (CPA), or any other financial professional. The content presented in this article is based on the author's personal opinions, research, and experiences, and it may not be suitable for your specific financial situation or needs.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.