Disney reported strong third quarter results, beating revenue and earnings estimates, driven by profitability in streaming services.

Despite the improved valuation, concerns remain about the slowdown in experiences.

We go over why we are revising our buy point.

Wirestock/iStock Editorial via Getty Images

On our last coverage of The Walt Disney Company (NYSE:DIS), we remained unimpressed with the relentless rally and suggested investors wait for a better entry point. While the fundamentals were sound, the valuation was anything but. We poured cold water on the bull dreams and gave them a specific entry price point.

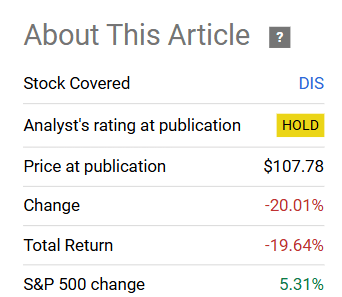

We would look for about 3%-4% annual returns from here. While our previous forecast was in excess of investment-grade bond yields, the current one is not. Investors would do best to avoid the stock and focus on better risk-adjusted opportunities. We rate the stock a hold and would get more constructive under $80.00.

The stock moved a bit higher and then took a turn for the worse.

Seeking Alpha

We look at the recent results and the upgrade cycle to tell you where we stand.

Third Quarter Results

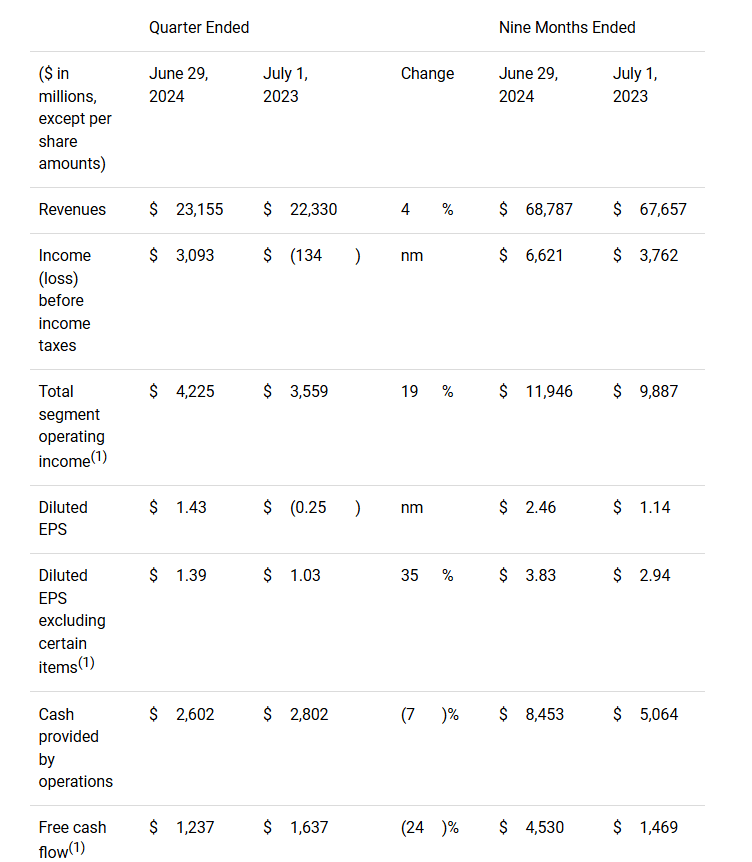

Disney has a fiscal year-end in September, so the reported quarter was the third quarter of the year. The overall numbers looked quite dapper relative to analyst expectations with revenues managing a modest beat. These increased by 4% year-over-year. The real punch line was in the adjusted earnings figure which destroyed all estimates and came in at a $1.39 vs. $1.19 consensus.

Disney Q3 Results

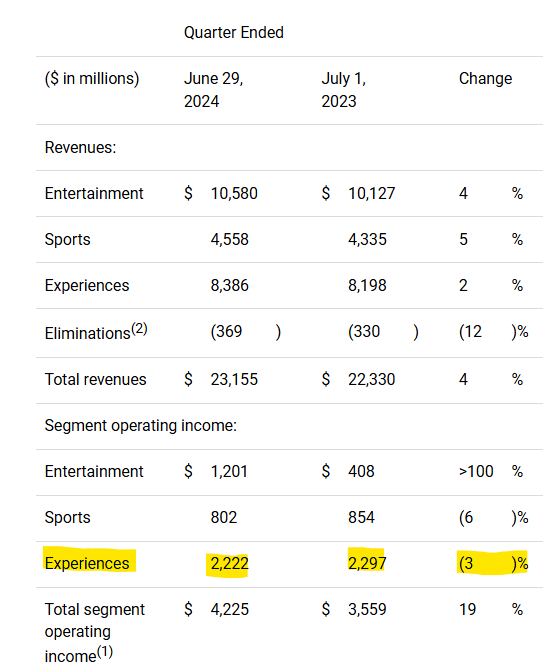

For a stock that was trending down into earnings, one would think that this would energize the bulls and reverse the trend. But the exact opposite happened and the stock slumped further. The devil here was in the “experience” category. The operating income there caught analysts off guard.

Disney Q3 Results

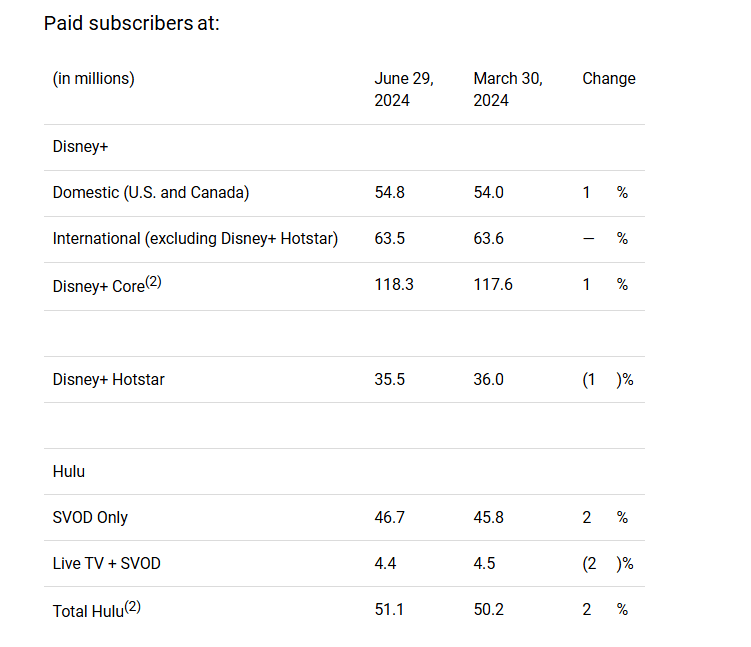

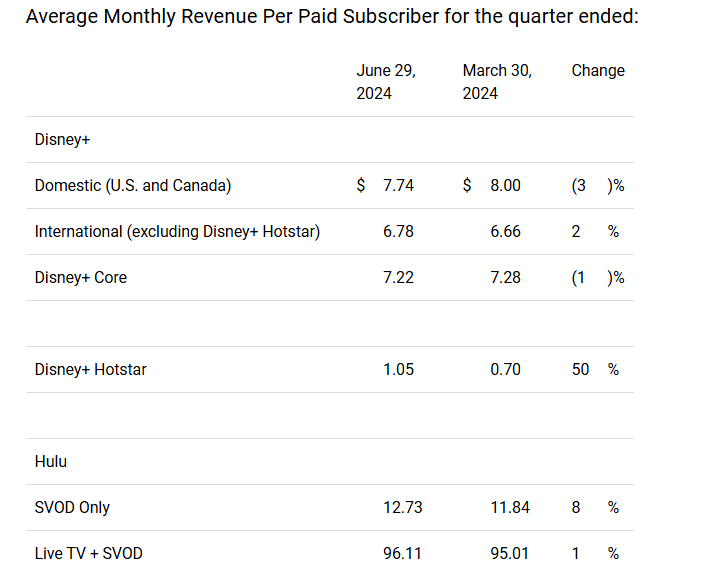

We will circle back to that, but for now, let’s look at how Disney beat earnings estimates if the experience segment was so weak. The answer, of course, was that Bob Iger delivered the streaming profitability in a hurry. This was done through very modest growth in subscribers.

Disney Q3 Results

Revenue per subscription also did not move materially.

Disney Q3 Results

But through strict expense control, Disney achieved profitability in streaming. This has got to be one of the fastest turnarounds we have seen in a segment this size. Disney+ is a fairly large ship and Bob Iger planned it moving to profits about a year back. And here we are. This has also proved many bears wrong that felt Disney+ will be an endless money pit. It has come in the face of rival streaming companies foundering through that same process. Disney raised its guidance for the year and analysts, of course, followed suit.

Outlook

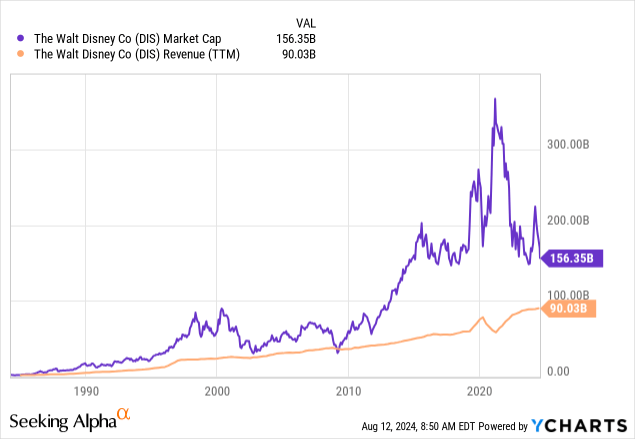

It has taken a lot of work since Disney hit $200 a few years back, but the valuation has finally become attractive. This is what we wrote about the bizarre valuation back then.

When investors get disenchanted with growth rates, Disney is likely to trade close to 1.5X revenues.

Seeking Alpha

Even using an optimistic $110 billion revenue outlook, the losses can be substantial.

Earnings estimates look fairly solid and even the good old value buyers are going to start to appear over here.

Seeking Alpha

So what’s wrong? Why are we sticking with a hold? Well, there are two reasons here. The first being that while the front end kept upgrades, the back end is being taken to the cleaners. You can see that by the change in earnings estimates for Fiscal 2024 and the change in earnings for Fiscal 2025 and beyond.

Seeking Alpha

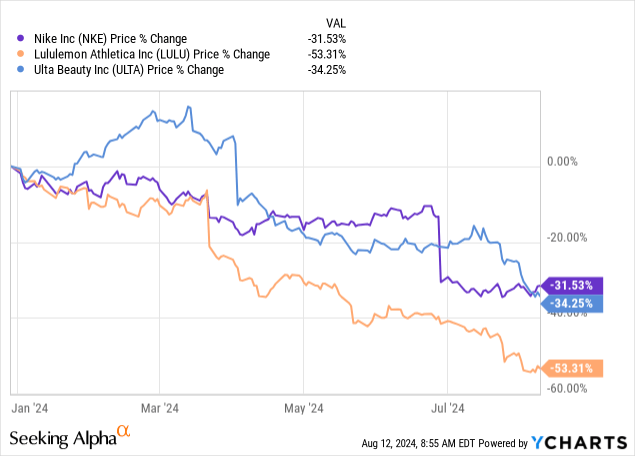

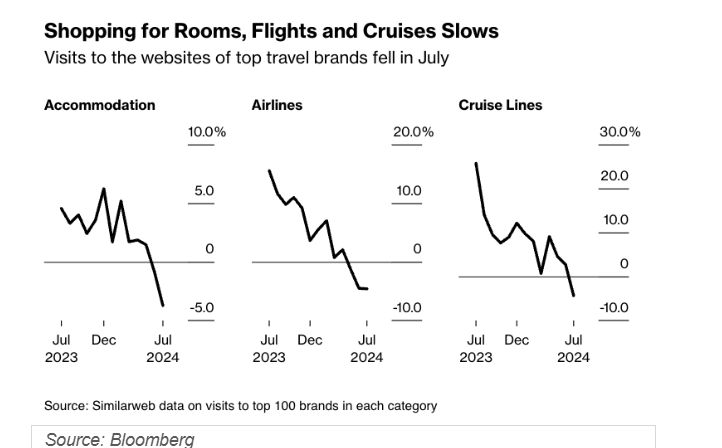

Bog Iger’s stellar performance on Disney+ profitability was just a tad ahead of schedule. But the slowdown in experiences is raising alarm bells on the longer-term outlook. We have also seen some rather steep drops in consumer discretionary stocks over the last 6 months.

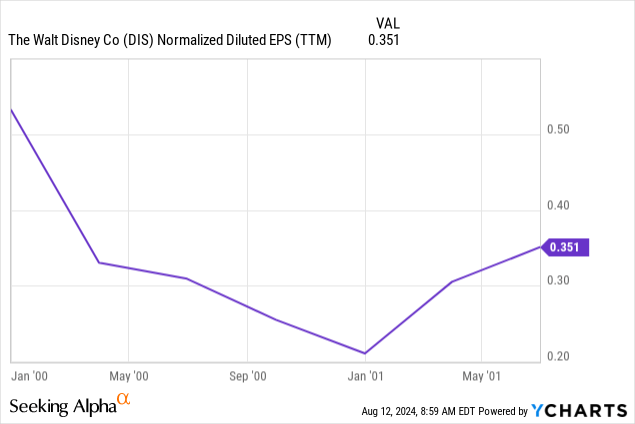

This coupled with some other troubling trends, likely points towards a recession being at hand. The issue is always that analysts underestimate the margin impact during a recession. You can add a “magical” tag all you like, but the fact remains that Disney is extremely sensitive to the economy. Below we show how earnings played out in 2000-2001. We purposefully chose this as this was a mild recession and nowhere in the ballpark of the Global Financial Crisis or the COVID-19 ugliness.

Even there, earnings absolutely cratered. If some online trends are correct, we might be just warming here for what’s next.

Bloomberg

Verdict

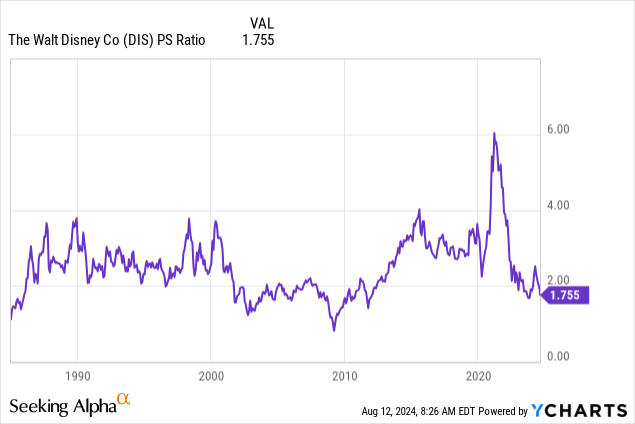

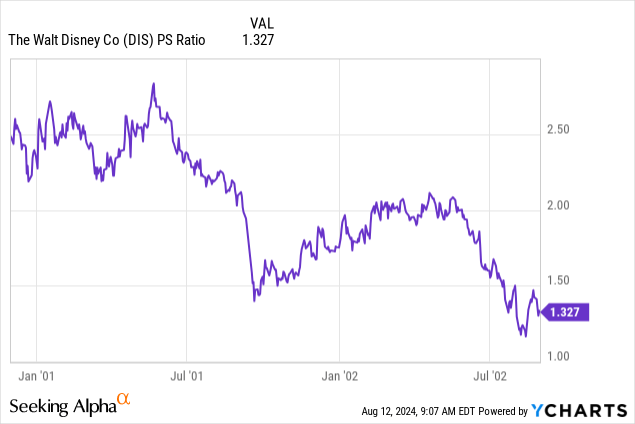

Of course, as value investors, you need to make a stand at some point. We had previously estimated that $80 would be that point and that certainly offers some chances of making money even today. But in all honesty, we think the stock will likely go even lower, and we would not rule out breaking $70 eventually. Investors looking for an entry should keep their eyes on the price-to-sales ratio. This strips out the earnings volatility which can be fairly extreme around recessions. Disney troughed nearly 1.25X in 2002 on the back of that mild recession.

We won’t go into the numbers for 2008 as this site is not authorized for R-rated content. But expect some fireworks to the downside if a recession is confirmed.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are you looking for Real Yields which reduce portfolio volatility?

Take advantage of the currently offered discounton annual memberships and give CIP a try. The offer comes with a 11 month money guarantee, for first time members.