Summary:

- Iger’s return comes during a challenging period due to the pandemic, which severely affected Disney’s key revenue streams, especially its theme parks.

- Despite facing competition in the theme park industry and challenges with its streaming service, Disney remains in a bullish position with potential for significant growth in the near future.

- The current DIS stock price suggests a potential buy opportunity for long-term investors, with a support zone between $80-$88.

Wirestock

The Walt Disney Company’s (NYSE:DIS) recent history has been characterized by both successes and setbacks, with leadership changes, strategic shifts, and external challenges reshaping the entertainment giant’s trajectory. With the return of Bob Iger as CEO, a veteran executive known for his successful reign from 2005 to 2020, Disney is poised to reposition itself amidst the pandemic’s aftermath, which has hit its primary revenue sources, such as theme parks, significantly. This piece offers a technical analysis of Disney, aiming to forecast its next steps and identify critical investment points for long-term investors. It reveals that Disney’s stock price is currently operating around a crucial support threshold, suggesting a solid bottom formation in progress. The article delves further into a historical review, identification of pivotal levels, recommended actions for investors, and potential risk factors associated with Disney.

A Balance of Growth, Profitability, and Succession Planning

The extension of Bob Iger’s CEO contract at Disney through 2026 reflects a vote of confidence in the veteran executive who originally led the company from 2005 to 2020. Iger’s return to the helm came amidst the turbulence of the pandemic which dealt a severe blow to Disney’s primary revenue sources, particularly its theme parks. With a renewed commitment to cost-cutting and strategic reorganization, Iger has made it his mission to revitalize Disney’s fortunes and regain the magic that propelled the company to its once lofty heights. One of the biggest tasks Iger faces is improving the financial performance of Disney’s direct-to-consumer streaming business, namely Disney+. Under the former CEO, Bob Chapek, the platform saw significant subscriber growth, adding approximately 235 million subscribers in the last fiscal year. However, this rapid expansion led to hefty operating losses in fiscal 2022.

Cutting costs and reducing content spend may have its own risks. There must be an equilibrium between drawing in new subscribers with appealing content and overseeing operational costs. Growth for Disney+ has decelerated in domestic markets while observing a downtrend in India. Hence, Iger’s mission of revitalizing the streaming platform requires intricate balancing. The company’s future rests significantly on its ability to correctly handle this situation.

Furthermore, Iger is facing the challenge of rejuvenating Disney’s famed animation studio. Although recent releases like Elemental and Lightyear have performed well at the box office, they haven’t achieved the level of success that previous Disney animations have enjoyed. There’s hope for a major hit with the upcoming release of Wish, and Iger’s extended tenure could provide much-needed stability and vision to this crucial division. Perhaps one of the most critical tasks for Iger is his role in succession planning. After the less-than-smooth transition from Iger to Chapek in 2020, the Disney board is keen to ensure a more seamless leadership handover. With his proven track record and deep knowledge of the company, Iger’s guidance will be invaluable in grooming a new CEO who can take the reins and navigate the company through its next phase.

Meanwhile, competition in the theme park industry, primarily from Universal Studios’ Epic Universe set to open in 2025, poses a considerable challenge for Disney. Iger’s experience and strategic thinking will be crucial in formulating a response to this new rival. It remains to be seen whether this will involve new theme park developments, expansions, or innovative attractions at Disney’s existing parks.

Despite facing numerous hurdles, Disney has managed to maintain a robust revenue stream, as evidenced in the following chart. The drop in net income was a fleeting phenomenon, and it’s now on an upward trajectory, registering a substantial $4.121 billion in net income for 2022. Given these strong financial metrics and the company’s ability to overcome challenges, it’s clear that Disney remains in a bullish position, with potential for significant growth in the near future.

Diving into Disney’s Historical Performance

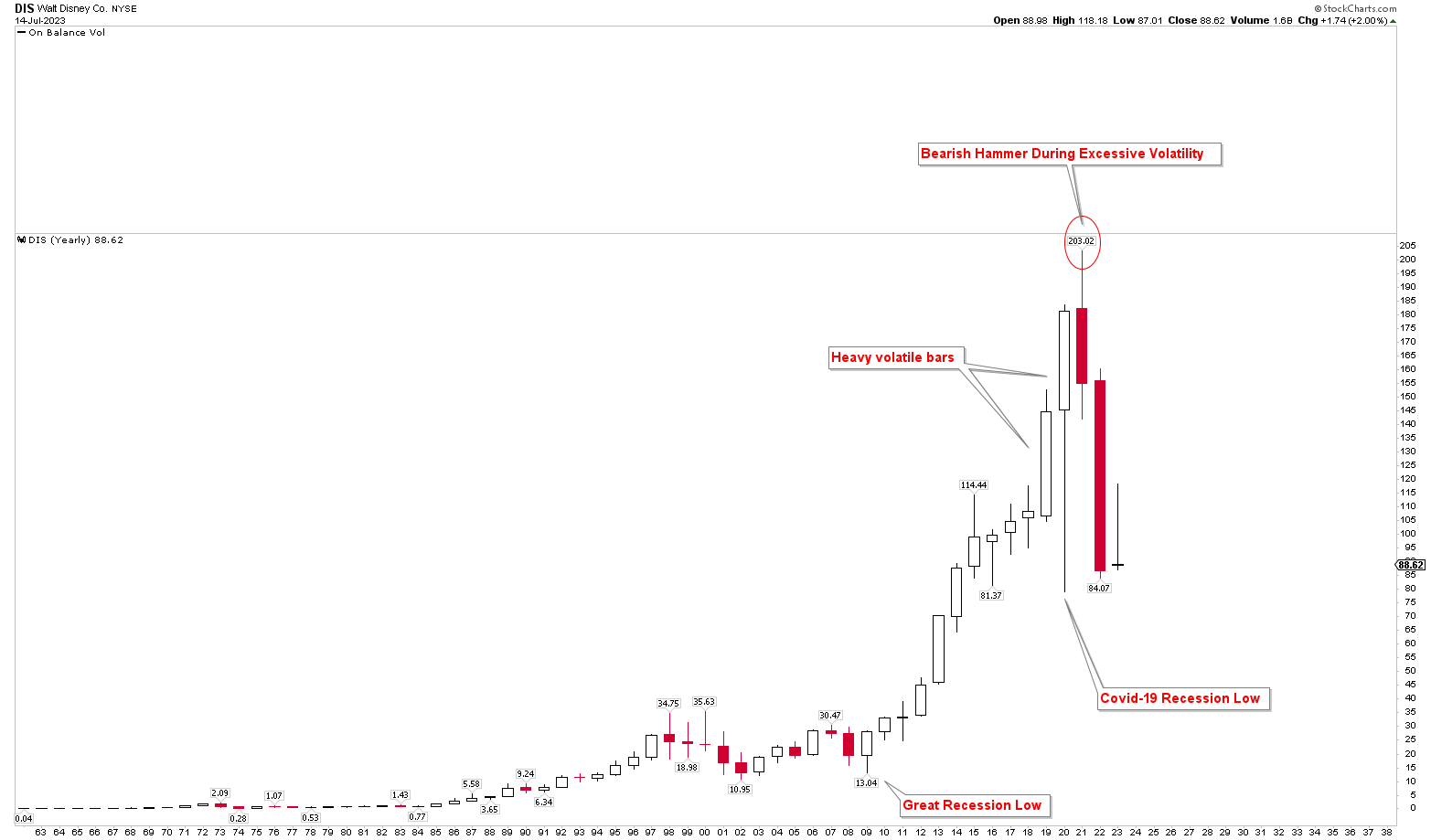

When looking back at the performance of Disney’s stocks in the long run, an overwhelmingly bullish outlook is evident as seen in the yearly chart below. The company witnessed a robust growth trajectory, bouncing back from the Great Recession lows of $13.04 and hitting an all-time high of $203.04. This sustained upward climb spanned over a decade, largely driven by the general economic recovery following the Great Recession. As discretionary income and consumer spending bounced back, Disney, a company heavily reliant on discretionary spending, reaped substantial benefits.

Disney Yearly Chart (stockcharts.com)

Disney’s portfolio was further bolstered by strategic acquisitions during this period. These include Marvel Entertainment in 2009, Lucasfilm (known for the Star Wars franchise) in 2012, and 21st Century Fox in 2019. These acquisitions brought a suite of profitable franchises under Disney’s control, unlocking numerous opportunities for cross-promotion and expansion. The success of the Marvel Cinematic Universe, the Star Wars franchise, and Disney’s own animated offerings played significant roles in Disney’s growth.

A new chapter in Disney’s growth story began with the launch of its streaming service, Disney+, in 2019. It rapidly amassed millions of subscribers, providing a new source of revenue and serving as a testament to the appeal of Disney’s extensive library of content, which included offerings from Pixar, Marvel, Star Wars, and National Geographic. However, the growth trajectory was interrupted in 2021 when the stock price hit $203.02 and subsequently retreated. This retreat led to a significant drop in the stock price in 2022, which fell to levels comparable to those seen during the Covid-19 pandemic lows.

It’s important to note that the annual charts show a considerable amount of volatility during 2019 and 2020. The launch of Disney+ sparked a surge in Disney’s stock price as investor optimism soared. However, the outbreak of the Covid-19 pandemic in 2020 brought about unprecedented challenges. With theme parks and resorts forced to close, cruise line operations suspended, film productions halted, and live sports events canceled, Disney’s revenues took a significant hit, leading to a steep fall in its stock price. Despite these challenges, Disney+ emerged as a bright spot. The platform’s impressive subscriber growth, coupled with optimism around vaccine development and the potential return to normal operations, helped the stock price recover from its 2020 lows.

Uncovering Key Thresholds in Disney’s Landscape

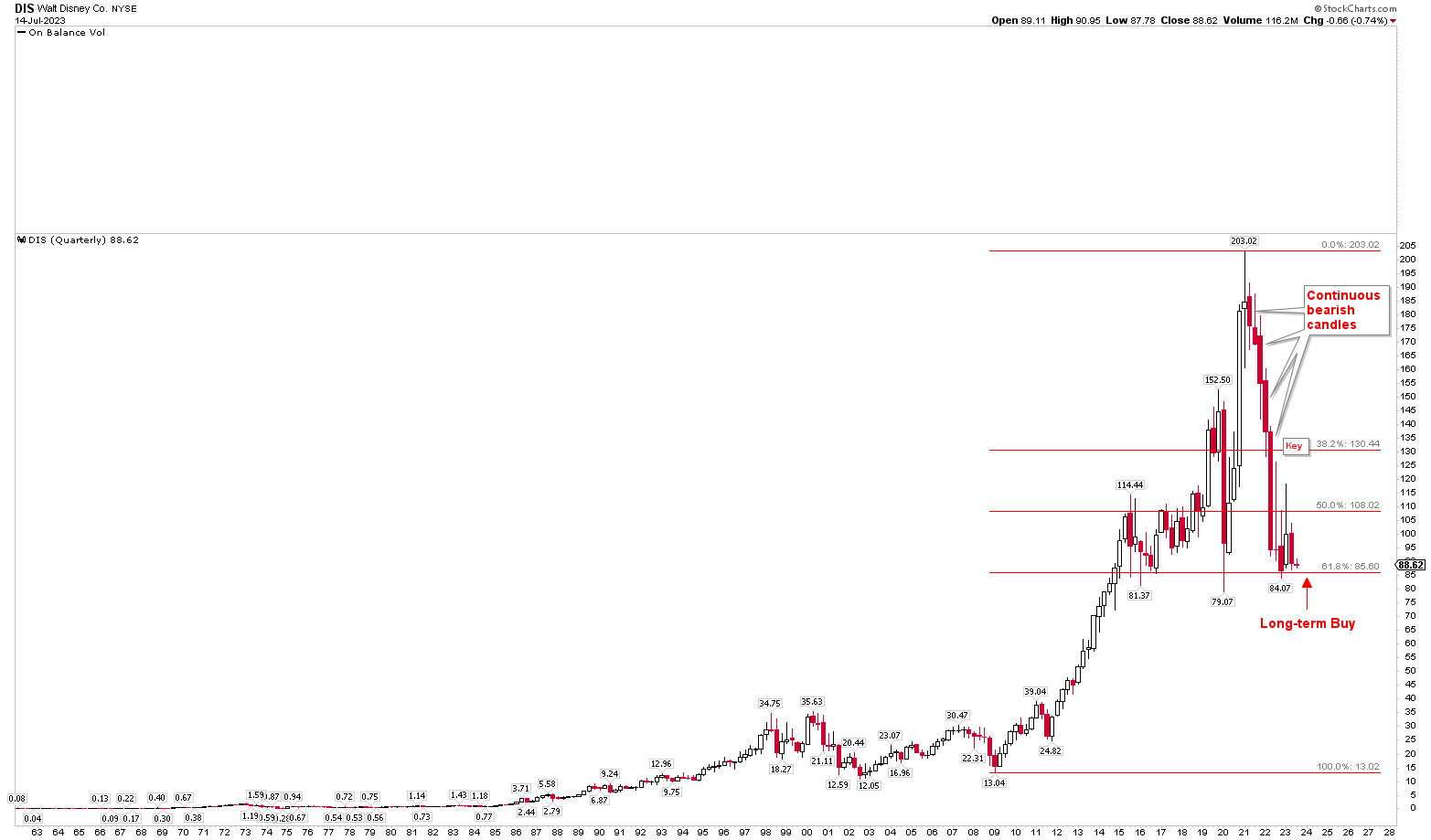

Disney’s bullish trend is undeniable, yet the stock is currently experiencing a drop toward its key levels. The Fibonacci retracement of the price from 2009 low of $13.04 to the all-time high of $203.04, as depicted in the quarterly chart below, reveals that the stock price has been on a steady decline from its peak, ultimately hitting the 61.8% retracement level of $85.60. Interestingly, the stock appears to be consolidating at this level, indicating the potential bottom formation. While there is no conclusive confirmation of this bottom formation as of yet, this level certainly provides a compelling buy opportunity for long-term investors.

Disney Quarterly Chart (stockcharts.com)

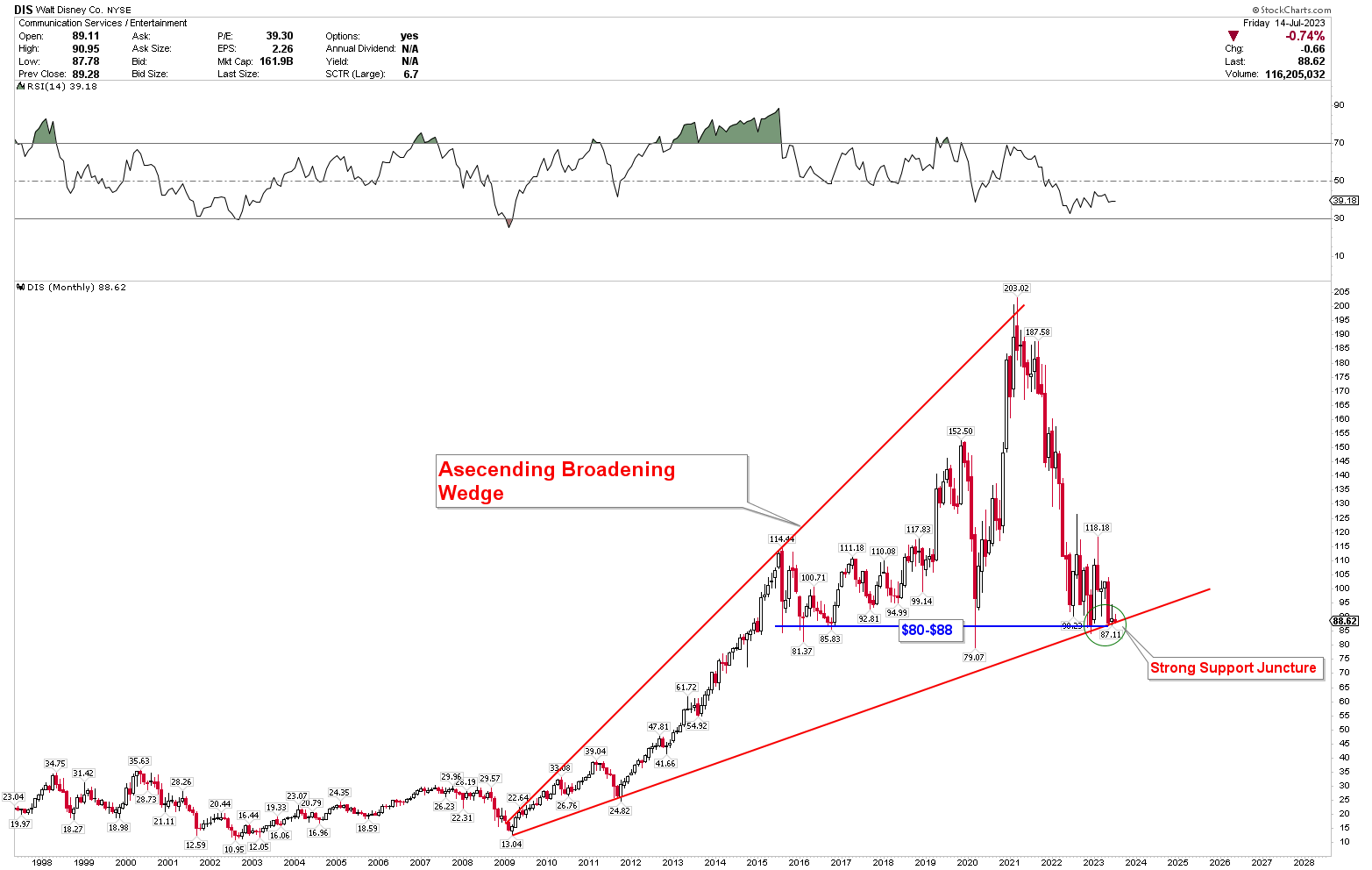

Zooming in further to the monthly chart, an ascending broadening wedge is visible, starting from the 2009 low. This formation typically suggests price volatility and substantial fluctuations. Interestingly, the 61.8% retracement level aligns with the support line of the ascending broadening wedge. Adding further strength to this support level is a horizontal line that corresponds with the current price level. Thus, the support region spanning from $80 to $88 becomes a crucial level for Disney.

Disney Monthly Chart (stockcharts.com)

Key Action for Investors

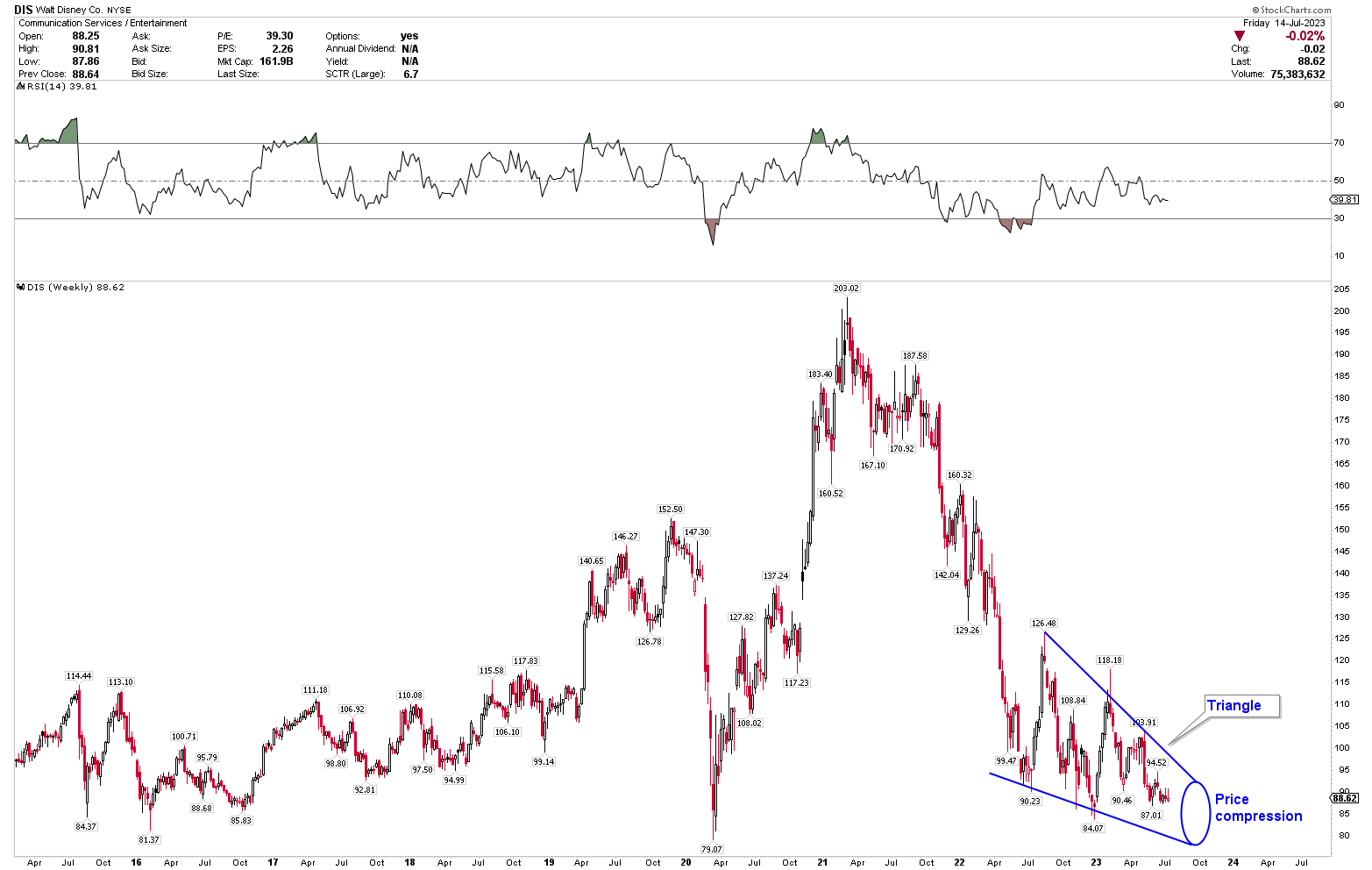

Based on the aforementioned analysis, it’s evident that Disney offers a compelling investment opportunity for those looking at long-term holdings. The region between $80 and $88 is a crucial long-term support area, confirmed by the ascending broadening wedge, 61.8% Fibonacci retracement, and the horizontal support line. For short-term considerations, the triangle presented in the weekly chart below indicates that the next dip to hit the lower support line of the triangle could provide an excellent entry point for investors.

Disney Weekly Chart (stockcharts.com)

While the current market scenario remains uncertain, long-term investors already in the market may consider accumulating more stocks at this point, provided they exercise prudent money and risk management. It is worth noting that a monthly close below $79 could alter the medium-term bullish outlook and signal further declines.

Market Risk

While Bob Iger’s return as CEO signals a renewed focus on cost-cutting and strategic reorganization, the task of improving Disney+’s financial performance remains a significant challenge. Disney’s theme park industry faces significant competition, particularly from Universal Studios’ Epic Universe set to open in 2025. Failure to formulate a robust strategic response to this competition could negatively impact Disney’s revenues from this sector.

Another risk lies in the company’s streaming service. Although it has managed to garner a substantial number of subscribers, it also led to a considerable increase in the operating loss at the direct-to-consumer business. This situation necessitates delicate handling to prevent further financial strain. Furthermore, Iger’s cost-cutting measures, including job cuts and reduced content spending, could potentially affect the company’s operational efficiency and creative output. Also, the current economic climate and higher interest rates could apply pressure on consumers’ discretionary spending, possibly leading to reduced visits to Disney parks or lesser purchases of Disney merchandise. While these challenges might be temporary, they could still negatively impact the company’s earnings in the near term.

From a technical standpoint, Disney’s stock price is presently situated at a critical long-term support level, though indications of a reversal are yet to surface. If the monthly closing price falls beneath $79, it would represent a breach of this sturdy support area, potentially leading to a further decline in the stock price.

Bottom Line

In conclusion, the return of Bob Iger to Disney’s helm represents a strategic move to regain the company’s momentum following the significant impact of the pandemic. His challenges are multi-faceted, ranging from improving the financial viability of Disney+, revitalizing the animation studio, handling succession planning, and tackling competition in the theme park industry. Despite the complexities, Iger’s leadership is trusted, even though the path forward is arduous. An analysis of Disney’s performance reveals a strong history of growth interrupted by significant challenges, with the stock currently experiencing a downturn toward key levels. The current scenario suggests a potential buy opportunity for long-term investors, although the medium-term outlook could turn bearish if the stock price closes below $79. The presence of substantial support indicated by the ascending broadening wedge, 61.8% Fibonacci retracement, and horizontal support line heightens the likelihood of this support zone being the long-term low. It could be beneficial for investors to consider long positions within the price range of $80-$88 anticipating higher prices in the future.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.