Summary:

- Disney’s shares dropped 4.5% after exceeding revenue and earnings expectations in Q3, driven by concerns over theme park operations and the pending Hulu acquisition.

- Disney’s streaming business showed mixed results with Disney+ Hotstar subscribers declining, while Disney+ Core subscribers and other streaming services saw growth.

- Despite some weak spots, Disney’s overall financial performance was strong, with growth in revenue, earnings, and cash flow, leading to a ‘strong buy’ rating.

JHVEPhoto

Contrary to the hopes and dreams of its shareholders, The Walt Disney Company (NYSE:DIS) saw its shares decline by 4.5% on August 7th. This came after the company announced financial results for the third quarter of its 2024 fiscal year. Prior to earnings, I had written my own preview of what investors should expect. Revenue and earnings per share came in higher than analysts anticipated. Cash flows are growing nicely and management is buying back a great deal of stock. However, fears regarding the health of the theme park industry, combined with concerns over how much the company will ultimately have to pay Comcast (CMCSA) for the 33% of Hulu that it owns, created a wave of pessimism that impacted shares for the day.

While I understand where the market is coming from, I believe that the former concern is not all that the market is making it out to be. The latter could be more problematic. But with a wide range of possible outcomes, and a good deal of time before a conclusion is ultimately reached, I would argue that the share price movement seen in response to this development was an overreaction. When you look at most other parts of the company, you see a healthy, growing, and vibrant enterprise. And in all likelihood, this trend will continue for the foreseeable future.

A look at headline news

Before we get into the deeper details provided by management, it would be helpful to touch briefly on the overall financial results achieved by Disney during the third quarter of the company’s 2024 fiscal year. During the quarter, Disney generated $23.16 billion worth of revenue. This was 3.7% higher than the $22.33 billion generated one year earlier. According to the most recent estimates that analysts had set forth, the sales reported by management came in at $65.8 million above what was anticipated. However, if we use the estimates that analysts had set as of the time of the publication of my prior article, the outperformance would be even higher at $135 million.

Author – SEC EDGAR Data

On the bottom line, the company also exceeded forecasts. Earnings per share came in at $1.44. This was $0.39 per share greater than what analysts were expecting. And from the time that I wrote my prior article on the company, the earnings beat came out to $0.41 per share. This resulted in net income for the company of $2.62 billion. This is a massive improvement over the $460 million, or $0.25 per share, loss reported for the third quarter of 2023. Other profitability metrics came in strong for the most part. While operating cash flow for the quarter fell from $2.80 billion to $2.60 billion, on an adjusted basis that strips out working capital, we get a rise from $1.81 billion to $3.43 billion. Meanwhile, EBITDA for the company expanded from $3.99 billion to $4.56 billion.

Author – SEC EDGAR Data

In the chart above, you can see results for the first nine months of the 2024 fiscal year compared to the first nine months of the year prior. This shows that the revenue, earnings, and cash flow performance experienced in the third quarter of this year compared to the same time last year was not a one-time thing. The company is consistently outperforming compared to what it achieved in 2023. This can be due not only to growing demand for the company’s products and services, but also because of cost-cutting initiatives. Management had previously upgraded its cost-cutting plan to $7.5 billion. And judging by these cash flow figures, the business is well on its way to that goal.

A look at streaming

Author – SEC EDGAR Data

Given that the big growth story at Disney in recent years has been its streaming business, I always like to start my deep dive into the company touching on those results. This really comprises three different businesses. The first of these is Disney+. During the quarter, the company saw yet another decline in the number of Disney+ Hotstar subscribers to 35.5 million. This compares to the 36 million seen in the second quarter of 2024. And it’s also well below the 40.4 million reported for the third quarter of 2023. For those not familiar with the company and the nitty-gritty details of its operations, this is the segment of the streaming operations that caters to low-value markets like India. And after having an initial surge of popularity there, there has been some decline. Part of this drop can certainly be attributed to the fact that management is focusing on raising prices in that market. During the most recent quarter, the company generated $1.05 per month from these subscribers. That’s up from $0.70 per month in the second quarter of this year, and it’s up from the $0.59 per month reported for one year ago.

Author – SEC EDGAR Data

Outside of all of this, you have what management refers to as its Disney+ Core subscribers, which make up its higher value markets. This part of the streaming platform has experienced some rather impressive growth. In the most recent quarter, the company boasted 118.3 million subscribers. That happens to be 0.7 million above what was seen just one quarter earlier. It also is 12.6 million more subscribers than what the company saw the same time last year. Over the same window of time, the company also saw a growth in average payment upper subscriber per month from $6.58 to $7.22. While this may not sound like much, this kind of change year over year, using the number of core subscribers that the company currently has, translates to an extra $908.5 million in annual revenue. If we add onto this the Disney+ Hotstar subscribers, total monthly compensation per subscriber would be $5.80, which is up from the $5.76 seen in the second quarter and which compares nicely against the $4.92 per month seen last year.

Author – SEC EDGAR Data

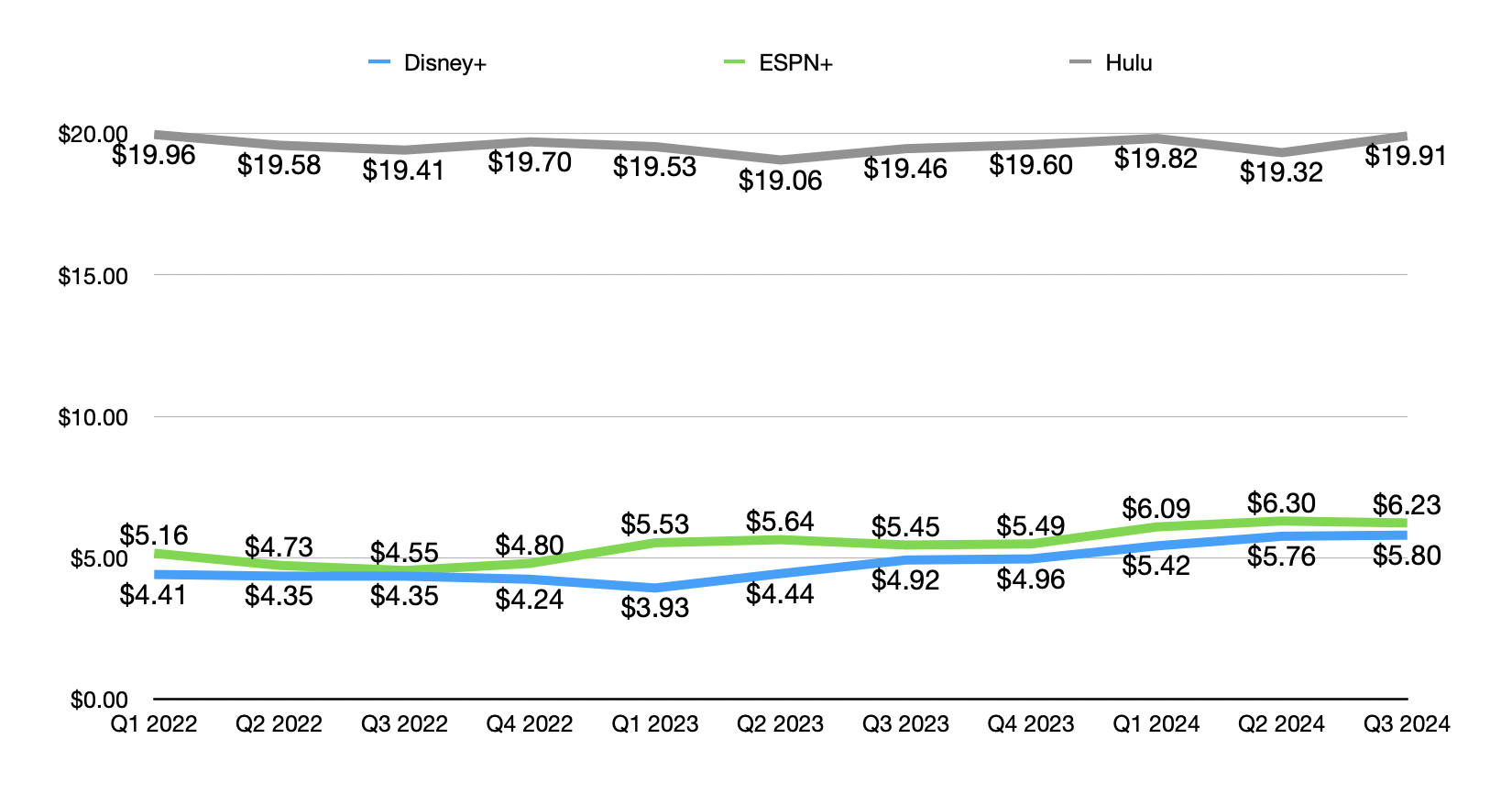

Other streaming operations deserve some attention as well. ESPN+ saw a slight uptick in the number of subscribers from 24.8 million in the second quarter of this year to 24.9 million today. That’s still down from the 25.2 million reported for the third quarter of 2023. And just like with Disney+, ESPN+ has been successful in capturing higher prices from its customers. In the most recent quarter, this came out to $6.23 per month. That compares favorably to the $5.45 per month reported one year ago. And lastly, there is Hulu. During the quarter, Hulu hit an all-time high subscriber count of 51.1 million. That’s an increase over the 50.2 million reported in the second quarter, and it’s up from 48.3 million last year. As was the case with the other two streaming services, Hulu also experienced a growth in pricing from $19.46 per month to $19.91 per month.

Other major operations

Author – SEC EDGAR Data

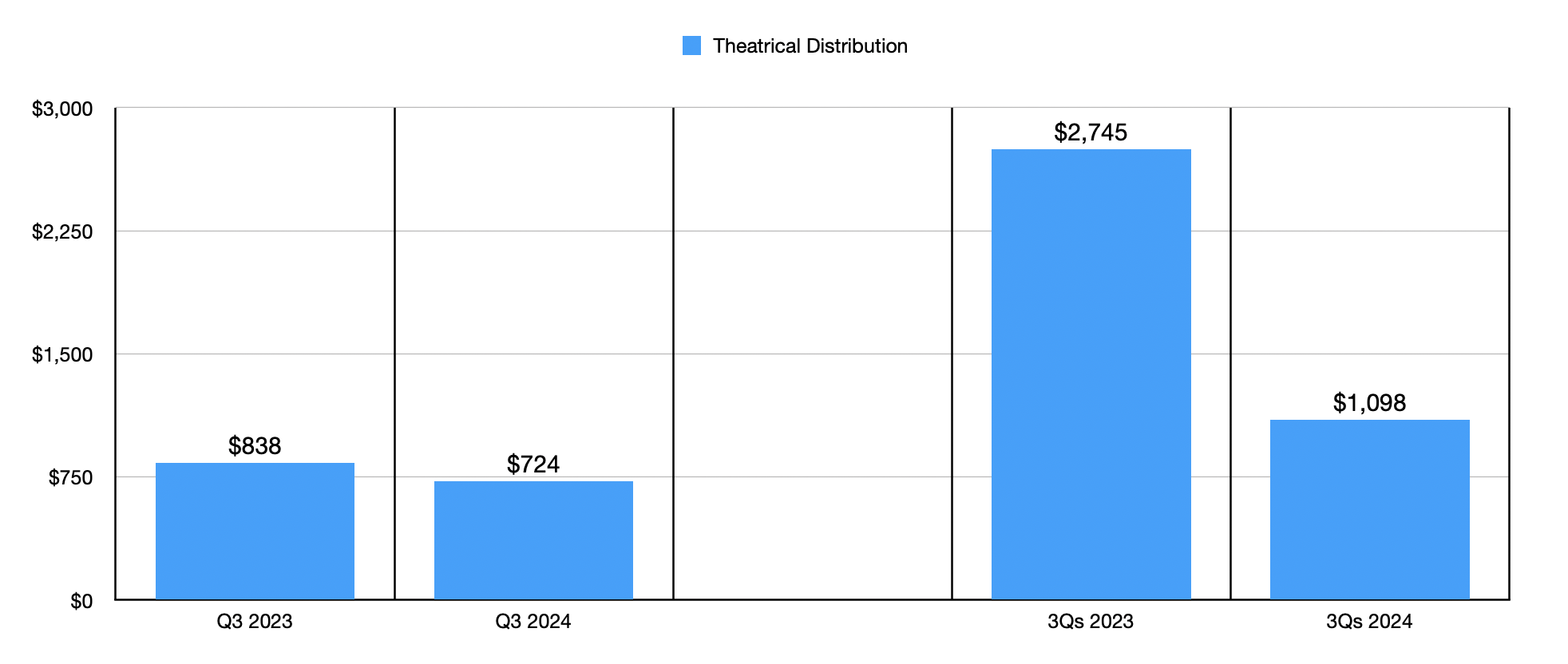

Outside of streaming, there are plenty of other important parts to the entertainment giant that deserve attention. For starters, there is the Theatrical Distribution part of the firm. In my earnings preview about the company, I made clear that we would likely see little to no benefit in the third quarter from recent box office successes. Sure enough, that ended up being the case. During the quarter, the company reported revenue of $724 million. That’s down from $838 million reported in the third quarter of 2023. But in all honesty, I think that this is only setting us up for a stellar fourth quarter. Combined, Inside Out 2 and Deadpool & Wolverine have been instrumental in pushing Disney to become the first production studio to see box office revenue this year exceed $3 billion. Globally, Inside Out 2 stands as the highest grossing animated box office film in history with global revenue of $1.56 billion, with $629.5 million coming from the domestic market. Meanwhile, Deadpool & Wolverine is well on its way to top the $1 billion mark, with global box office sales of $879.2 million, with $421.2 million of that coming from the domestic market.

Most other parts of the company have done quite fine. Theme park admissions revenue, for instance, ended the quarter at $2.78 billion. That is 1.8% above the $2.73 billion reported one year earlier. This was one of the parts of the company that caught a lot of heat from the investment community, as the growth was considered unimpressive. It is true that YoY global attendance rose by only 1%, driven by a 4% rise internationally and flat attendance domestically. Per capita guest spending remained flat, with a 1% decline in the international arena and a 1% increase domestically. But the way I see it, growth is growth all the same. This doesn’t mean, of course, that weak consumer spending won’t eventually result in some sort of decline. But as we have seen over the years, the theme park operations of the company are incredibly resilient and always popular.

Author – SEC EDGAR Data

More impressive was the resorts and vacations side of the business. Revenue of $2.12 billion happened to be 6.3% greater than the $1.99 billion reported one year earlier. Merchandise, food, and beverage sales associated with the Parks & Experiences operations of the company successfully increased by 1.6% from $1.96 billion to $1.99 billion. And lastly, parks licensing and other revenue jumped 7.7% from $504 million to $543 million. If you add all of these parts of the company combined, you would see revenue for the latest quarter of $7.43 billion. That is 3.4% above the $7.19 billion reported for the third quarter of 2023. For such a large and mature company, I consider this acceptable.

Author – SEC EDGAR Data

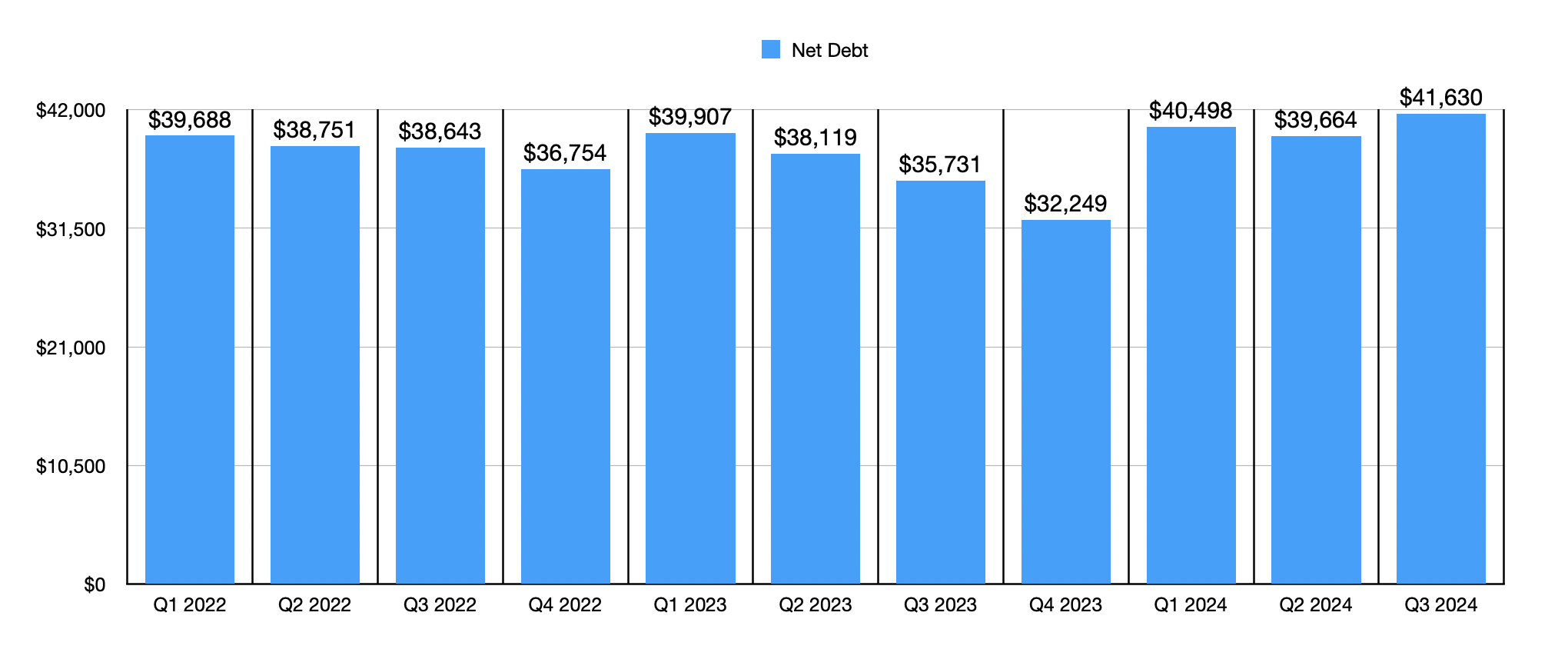

This is not to say that there weren’t any other weak spots beyond what I already mentioned. The biggest surprise that I had was that the company saw an increase in net debt for the quarter. Net debt came in at $41.63 billion. That happens to be $1.97 billion greater than what the company ended the second quarter of this fiscal year at. Fortunately, we know that some of this change can be attributed to management’s decision to repurchase 14 million shares for approximately $1.5 billion. Clearly, management believes that buying stock at current prices makes more sense than paying down debt. Even though I am not a fan of stock buybacks, I think it would be hard to argue with that logic.

Though not exactly connected with the earnings release, one other thing that might have weighed on the company was a development regarding the joint venture entered into between Disney, Warner Bros. Discovery (WBD), and Fox Corporation (FOX) (FOXA). The venture, known as Venu Sports, would control more than 80% of nationally broadcast sporting content and over half of national sports content. In an article that I wrote earlier this year regarding fuboTV (FUBO), I detailed how this maneuver could serve as an existential crisis for the company. I ultimately rated it a ‘sell’. And since then, shares are down 36.7%. But on August 7th, news broke that certain members of Congress sent a letter to the US Justice Department expressing their worries about this venture, with some even urging the department to see if this involves any antitrust violations.

A look at Hulu

Last thing I would like to touch on is Hulu. I know that, earlier in this article, I talked about the growth of the company and the rise in pricing reported by management. But one thing I did not do was talk in detail about what is going on between Disney and NBC Universal (a subsidiary of Comcast). Back in November of last year, NBC Universal exercised its right to force Disney to acquire the 33% stake in Hulu that Disney did not previously own. This involved Disney paying to NBC Universal a guaranteed minimum payment of $8.61 billion. However, an arbitration process would be implemented in order to see to what extent Disney might need to pay above that in order to adequately reflect the fair value of the streaming company.

In its quarterly filing, Disney stated that they don’t expect a decision in this arbitration until sometime in the 2025 fiscal year. However, they indicated that NBC Universal is pushing for an extra $5 billion. Management did make it clear that the additional payment required could be as little as nothing. But in all likelihood, they said, somewhere between nothing and $5 billion is what will likely be seen.

Author – SEC EDGAR Data

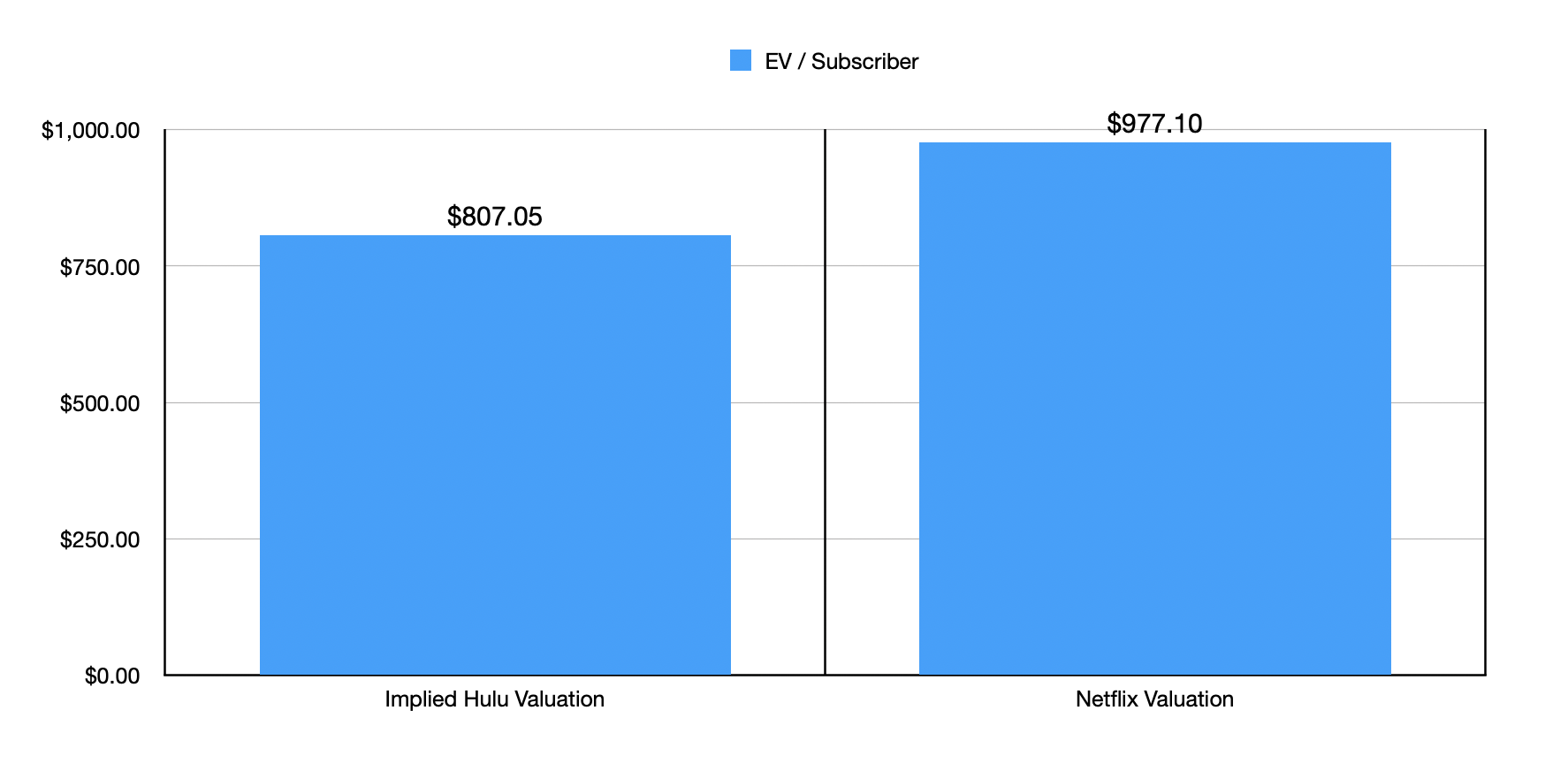

I do think that this is something that investors should be paying close attention to. I say this because, to me, an extra $5 billion would be quite steep. To see what I mean, I decided to look at the implied valuation of Hulu in this case. The easiest way to do this is to look at the valuation of $41.24 billion that is implied from this payment and compare that to the number of paid subscribers the company currently has. This works out to $807.05 per paid subscriber. This is lower than the $977.10 per subscriber that rival Netflix (NFLX) is currently being valued at on an enterprise value basis.

Even though this is a discount, it’s worth noting that Netflix is larger, is growing more rapidly, and is more profitable from a margin perspective than Hulu is. This conclusion of mine does require some assumptions. You see, in the most recent quarter, programming and production costs for both Disney+ and Hulu were disclosed. But there’s also another category called ‘other operating expense’ that is split in some unknown way between the two streaming platforms. If we assume that the split would be proportional to the programming and production costs, then this would translate to approximately $523.5 million being attributable to Hulu.

If we strip this out from the equation and annualize the profits achieved by Hulu based on a projection of revenue from the number of subscribers at present and the current rate being charged to those customers, we get operating profits of $1.55 billion based on revenue of $12.21 billion. This implies an operating margin of 12.7%. Following the same approach with Netflix gives us an operating margin of 27.7% off of revenue of $38.82 billion. Now, it is true that if we end up looking at the picture from the perspective of the total price paid for the business relative to the operating profits of the business, the 26.6 times that Hulu would be valued at would be only slightly above the 25.3 times that Netflix is going for. But on an enterprise value to revenue basis, Hulu Is being valued at a multiple of 3.38 compared to the 6.99 that Netflix is going forward.

Author – SEC EDGAR Data

While the enterprise value to sales approach indicates that Hulu is being undervalued relative to Netflix, I actually think that the enterprise value to operating profit scenario is the most relevant. And this does show the companies being valued closely to one another under the assumption that the total settled value of Hulu is determined to be $41.24 billion. But because of the growth differences and the margin differences, I think that is a difficult story to sell. In all likelihood, the total fair value will come in some number lower than this. But it’s not unthinkable that Disney could be forced to shell out between $1 billion and $3 billion to complete this transaction.

Takeaway

Based on the data provided, I must say that I was pleasantly surprised with most of the results achieved by Disney. While there were some weak spots, I think that the market is overreacting. The core parts of the company are still doing just fine. While there does appear to be a slowdown at the park level, we will see ebbs and flows as the economy waxes and wanes. But at the end of the day, none of this changes the fact that Disney is an incredibly valuable company with some of the greatest assets on the planet. It is with that in mind that I’m happy to keep the company rated a ‘strong buy’ for now.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DIS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!