Summary:

- A. O. Smith recently released their Q3 financial report, and they improved their year-over-year earnings per share by 27%.

- Also, the company increased their quarterly dividend by 6.7%, repurchased a meaningful amount of shares and deleveraged their balance sheet.

- Much of the earnings growth was caused by margin improvement, but in the future, the largest contributor to earnings growth should be increased sales.

demaerre

Dividend aristocrat A. O. Smith (NYSE:AOS) has already been part of my portfolio for half a decade, but I didn’t pay too much attention to the company or its shares, because the company seems to have been in quiet waters. Even though they were also affected by covid, inflation and interest rates, their earnings and dividend growth have been steady and solid.

The company reported some nice results for the first 9 months of 2023, but one of the most important questions for investors is if the company will be able to continue its decent performance. So let us zoom in on A. O. Smith and their Q3 earnings and outlook for the full year 2023.

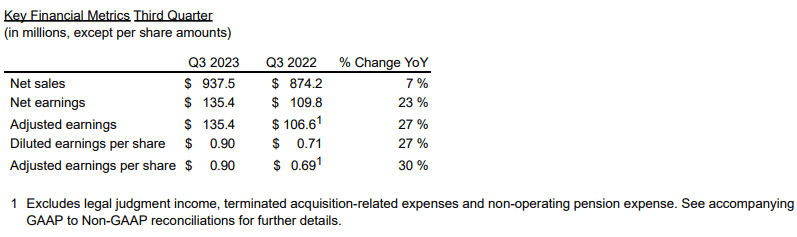

Q3 2023 earnings

A. O. Smith released their quarterly earnings on October 26th this year, and although their quarterly earnings per share did not break their record high of the second quarter this year, they still look very decent and amounted to a year-over-year increase of 27%.

A. O. Smith Q3 2023 earnings (A. O. Smith Q3 financial report)

Sales in North America, their largest market by far, grew by 9%. While the demand for boilers dropped, sales of residential water heaters more than compensated for this. In the rest of the world, sales grew by 1% (6% adjusted for currency fluctuations), but locally there were large differences. In India for example, sales grew by 13%, and much of their revenue growth in other parts of the world was driven by recently introduced kitchen appliance products in China.

Margins in North America were 23.9%, while those in the rest of the world were 9.9%. Both margin numbers increased in Q3. These increased margins are stated by the company to be mainly the result of lower material costs.

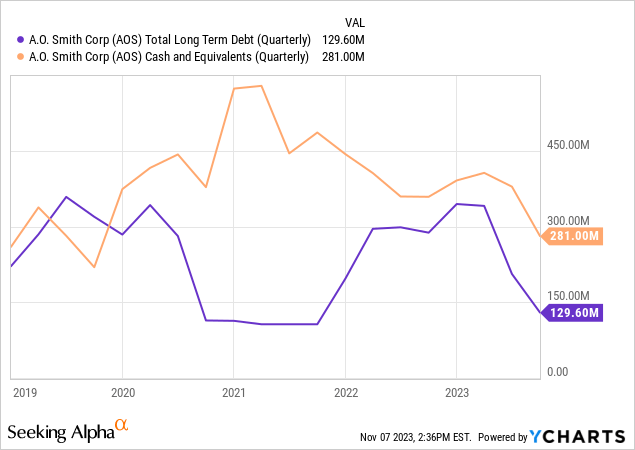

Also, A. O. Smith deleveraged their balance sheet in a meaningful way, to deal with the recently increased costs of debt, as you can see in the graph below:

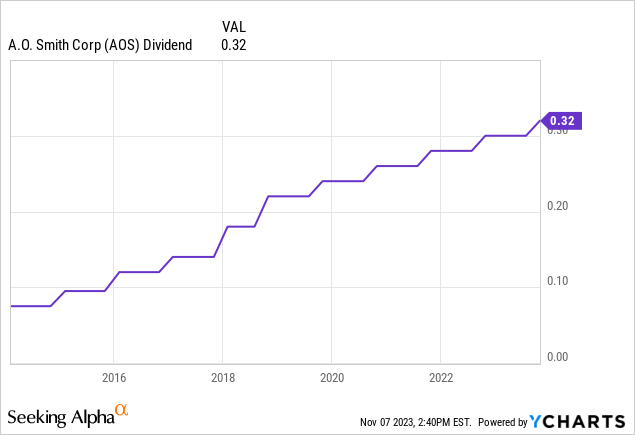

Already some weeks before their Q3 financial report, the company proposed a dividend increase from a quarterly $0.30 to $0.32. This amounts to an increase of 6,7%. Though current dividend yield of 1.8% by far not high enough to entice income-oriented investors, A. O. Smith remains a dividend aristocrat and has a five-year annual dividend growth of 10%.

Also, A. O. Smith repurchased about 2.4 million shares in 2023, amounting to a total cost of $161.4 million and reducing their total outstanding shares by 1.6%. Of the total costs, $91.8M was spent in the third quarter. The company expects to spend $300M on buying back shares during the full year of 2023, which means that we can still expect more than $100M of share repurchasing during the last quarter of 2024.

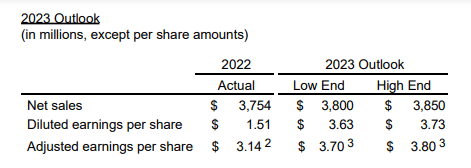

A. O. Smith 2023 outlook (A. O. Smith Q3 2023 financial report)

A. O. Smith updated their outlook for 2023, which improved in comparison with last quarter. They now expect a 2% sales increase in 2023 compared to 2022, but their expected earnings per share are meaningfully higher as a result of improved margins. At the mid-point of their estimates, EPS is expected to grow by 19% in 2023 year-over-year.

Bottom line and expectations

A. O. Smith experienced a very decent growth in earnings in the first three quarters of 2023, but their revenue increase was quite modest. Most of the earnings growth was caused by improving margins. Since the margin improvements were mainly caused by lower material costs, it is uncertain if they can continue to the same extent. Material costs seem to have stabilized lately, and I believe they are less likely to be a future source of margin improvement for the company. For the future, earnings growth and revenue growth is likely to go hand-in-hand.

A. O. Smith seems like a very well-run company, also judged by the fact that they chose to decrease their borrowing costs by paying off debt in 2023. Their net debt is negative, and the company has a very healthy-looking balance sheet.

Looking at the modest growth of the sales of the company, their healthy but relatively modest increase in dividend, and the low dividend payout ratio, A. O. Smith looks like a holding most suitable for long-term dividend growth investors. A. O. Smith’s sales are not very cyclical, although increased interest rates might have the result of some consumers postponing their purchase or renewal of their water heater. On the other hand, in the case of defects, purchases will rarely be postponed since water heating is a necessity for most homes.

Growth could come from sales in the rest of the world, most notably India where their sales have increased by 13% year-over-year in Q3 2023. Also, the water heater market is likely to evolve as a result of a larger focus on renewable energy. This could lead to an increase in sales of electric and solar heater systems. But I believe this will be a relatively gradual change, not leading to sudden explosive growth but more likely a modest upward move in sales and revenue.

A. O. Smith is currently trading for a forward price-to-earnings ratio of 18.9. This looks like a fair valuation for their stock, and more or less in line with their historic average which seems to hover around 20. But the nature and stability of their business is not likely to lead to heavy share price fluctuations. In my opinion, A. O. Smith is an example of a company suitable for a hold forever strategy, and should be treated as such. A decent holding for dividend growth investors.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AOS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.