Summary:

- Eli Lilly received FDA approval to sell tirzepatide for obesity treatment, expanding its market beyond diabetes.

- Shares of Eli Lilly jumped 3.2% on the news, resulting in a $17.3 billion increase in shareholder wealth.

- Tirzepatide has shown promising results in clinical trials, with patients losing an average of 48 pounds over 72 weeks.

- This is slated to result in significant additional wealth creation for shareholders moving forward.

jetcityimage

Nov. 8 ended up being a day to celebrate if you are a shareholder of pharmaceutical giant Eli Lilly and Company (NYSE:LLY). News broke that the US FDA has finally granted the company approval to sell its drug, tirzepatide, for purposes of treating obesity and being overweight. This represents a significant widening of the opportunities for the drug that was previously only approved for treatment of diabetes. Management also made clear that they plan to get this version of the drug out to the public before the year is out, which could have a positive impact on its revenue and profits. But the real benefit is for the long haul because, as we have already seen this year, tirzepatide already is working wonders not only for patients, but also for the company’s top line.

A great day

Usually when we hear about companies experiencing significant moves higher or lower in response to news, the thought of double-digit gains or losses comes to mind. But when you’re dealing with a company that already has a market capitalization of almost $540 billion, it’s difficult to see a move of that magnitude. A big day for such a company would be one where you see a 3% gain or higher. And that is precisely what was experienced on Nov. 8, when shares closed up 3.2%. That resulted in shareholders getting wealthier by about $17.3 billion. But of course, investors are getting used to rather attractive returns. Back in June of this year, for instance, I wrote a bullish article about Eli Lilly that was focused on its weight loss initiatives. That article was the first that I had written about the company and it resulted in a “buy” rating for it. Since then, the S&P 500 has dropped by 1.5%. By comparison, shares of Eli Lilly have generated upside of 33.1%.

Naturally, a lot of this upside has been in anticipation of the news broke out on Nov. 8. Last year, management started selling tirzepatide, branded as Mounjaro, for the purpose of helping those with diabetes. However, the drug was not cleared at that time for use when it came to those who suffered from being overweight but who did not have diabetes. According to the press release issued by Eli Lilly on Nov. 8, the US FDA decided to approve tirzepatide for chronic weight management treatment for those who are overweight and obese. Those who are overweight are defined as those with a BMI of 27 or higher, while those who are obese have a BMI of 30 or higher.

The drug will not be sold under the same Mounjaro label. Rather, it will be called Zepbound. According to management, this drug is the first and currently only obesity treatment of its kind that activates both GIP and GLP-1 hormone receptors. This approval was based on significant research, including a study of 2,539 overweight or obese adults who had at least one weight related medical condition such as hypertension, dyslipidemia, obstructive sleep apnea, or cardiovascular disease. For the purpose of receiving this treatment, patients must have one weight-related condition such as these or they must have diabetes. But the study did not include anybody who is diabetic. This study, which lasted 72 weeks, resulted in an average of 48 pounds lost for those who took the highest dose, while those who took the lowest dose lost 34 pounds on average. By comparison, those who took a placebo lost only seven pounds. What’s really impressive is that around one in every three patients that took it at the highest dose lost over 58 pounds, or 25% of their body weight. That compares to the 1.5% lost by those on the placebo.

Management has not come out publicly with a timeline yet. But they did say that before the year is out this drug will be publicly available. The listed price of the drug will be set at $1,059.87, which is actually 20% lower than the 2.4mg injection of semaglutide that is owned by rival Novo Nordisk A/S (NVO). Those who are covered under insurance could pay as little as $25 for a one month or three month prescription, while some might have to pay as much as $550 for a one-month prescription if insured.

Eli Lilly

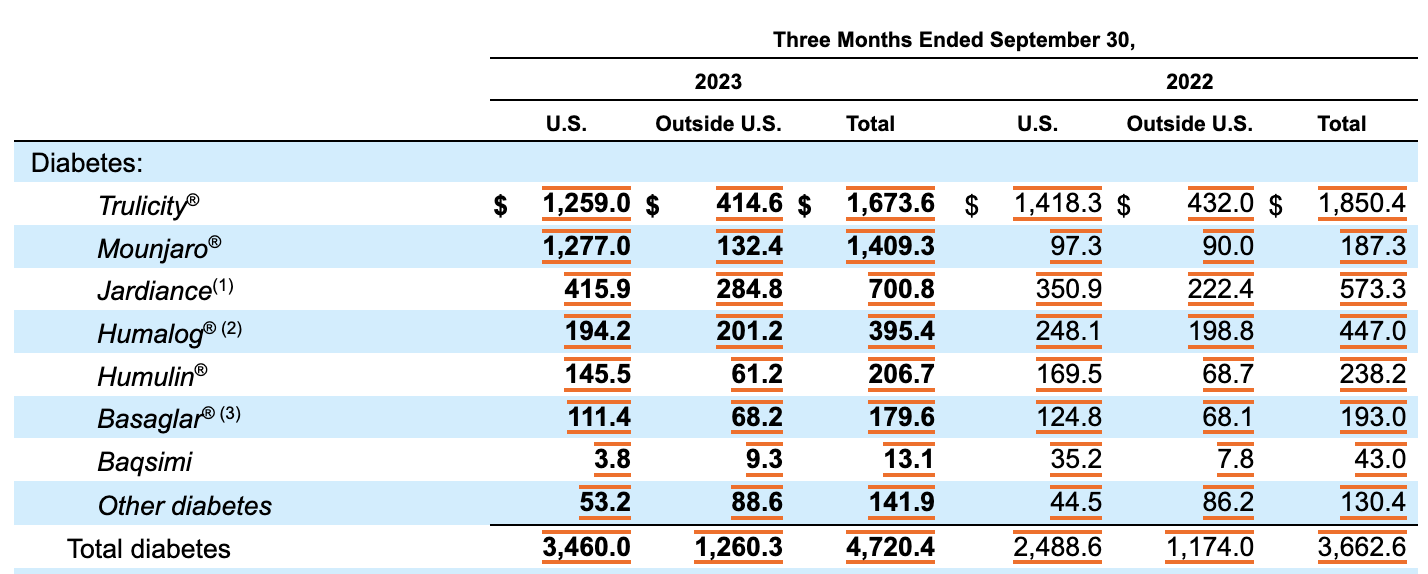

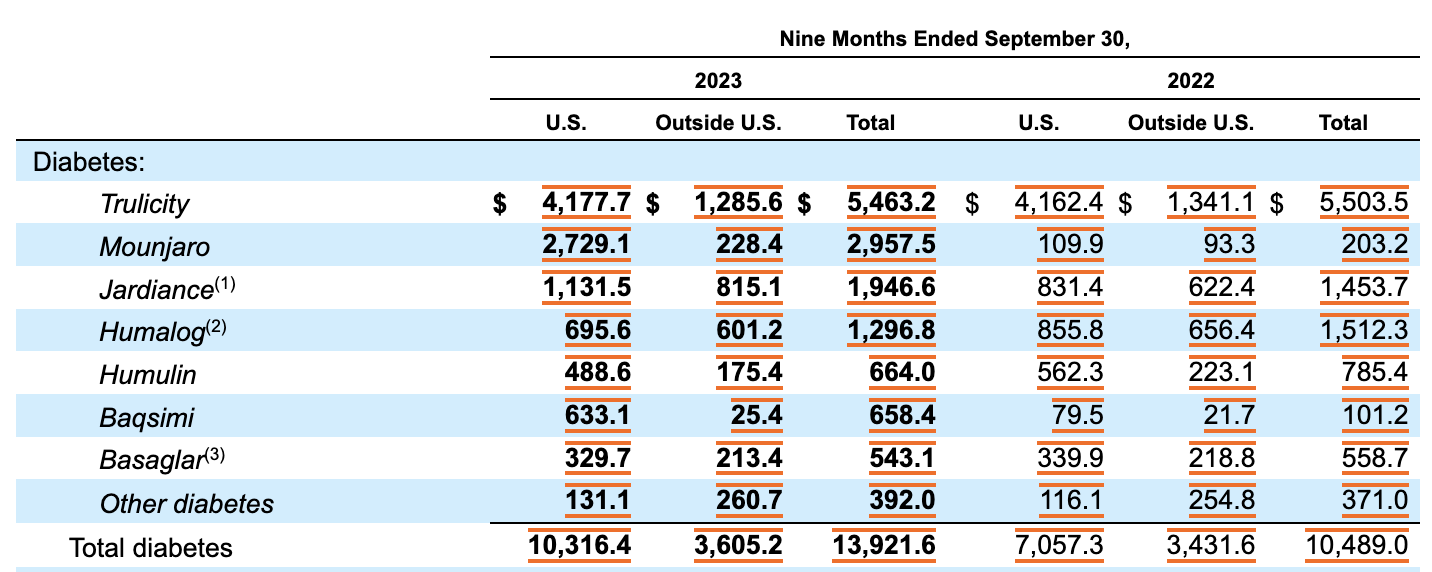

Nobody knows what the future holds. But if this is anything like Mounjaro, the end result for shareholders should be quite positive. In the third quarter of the 2023 fiscal year, for instance, Mounjaro generated revenue of $1.41 billion. That dwarfs the $187.3 million in revenue generated the same time one year earlier. And for the first nine months of 2023, sales totaled $2.96 billion compared to the $203.2 million reported for the same window of time of 2022. It’s possible that the company may have to deal with some degree of cannibalization. After all, during the third quarter, the company’s diabetes and weight management drug, Trulicity, saw revenue of $1.67 billion. That’s down from the $1.85 billion reported for the same time last year.

Eli Lilly

This is not to say that the company is going to see weakness in all of its weight and diabetes drugs. Jardiance, which is a tablet that’s used to help control blood sugar levels in those with type 2 diabetes and that’s used to reduce the risk of cardiovascular problems in adults who have heart failure or cardiovascular disease with type 2 diabetes, saw revenue jumped from $573.3 million in the third quarter of 2022 to $700.8 million the same time this year. All combined, revenue in the third quarter related to drugs aimed at treating diabetes and weight problems came in at $4.72 billion. That’s an increase of 28.9% over the $3.66 billion reported the same time last year.

Eli Lilly

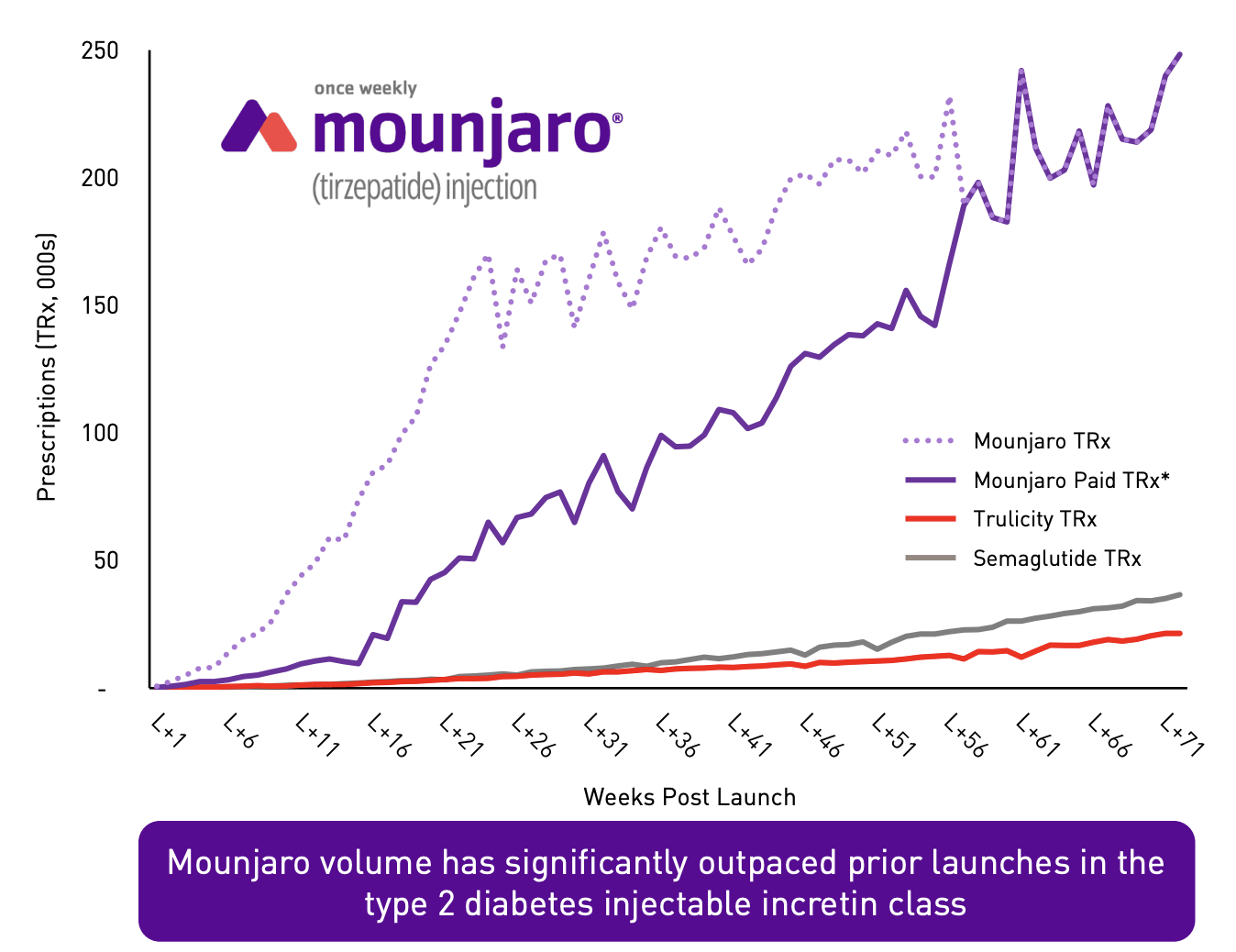

It’s unclear just how large a revenue opportunity these drugs will become. We do know that, as I detailed in my prior article on the matter, at least one credible estimate pegged the revenue opportunity for Mounjaro as being as high as $25 billion per year. And truly, the drug has been the most rapidly accepted drug in the company’s history. But the fact of the matter is that the overweight and obesity market opportunity is significantly larger than the diabetes market on its own is. In the US alone, it has been estimated that around 37.3 million people are diabetic, with 28.7 million of those being diagnosed and the rest currently undiagnosed. By comparison, an estimated 73.1% of all adults, happen to be overweight or obese. I figured that the total number of adults who are overweight or obese in this country is about 191 million.

National Institute of Health

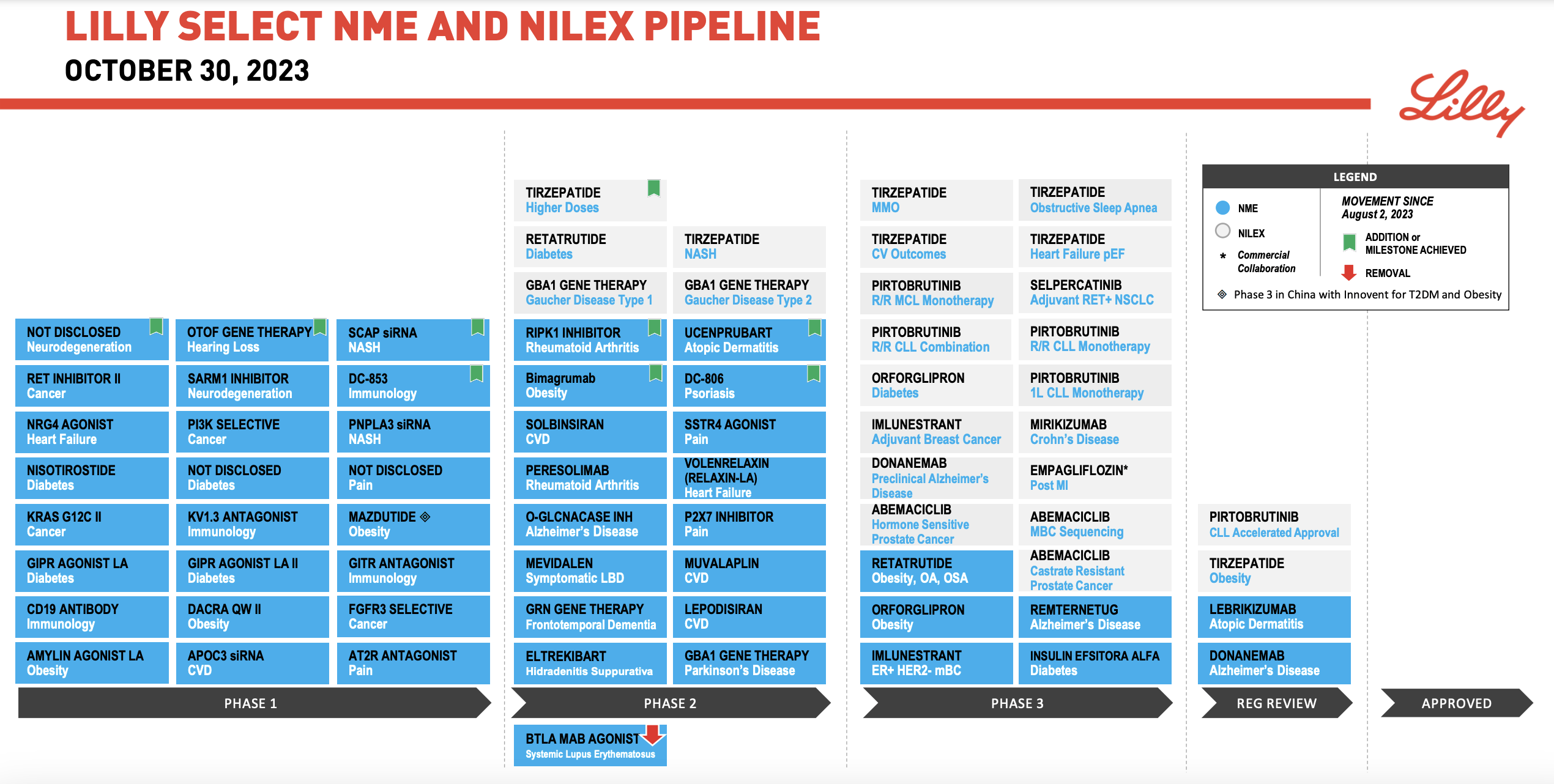

Globally, the picture is much different. Although the US has an extremely high obesity rate, obesity does pose significant problems across the globe. Obesity-related medical costs back in 2019 were estimated to be worth $173 billion. In fact, in 2021, the average annual health spend per person who is obese in this country and who had employer based insurance came in at $12,588. That’s significantly higher than the $4,699 estimated for those who were not obese. But globally, it’s estimated that by 2035, obesity will cost the global economy more than $4 trillion annually. With numbers like that, there’s significant growth potential for any drug that addresses these costs. It’s also worth noting that this is not the only drug that the company has at its disposal. Including other indications for tirzepatide, the company had seven different obesity and diabetes related drug trials as of the end of its latest quarter that were in Phase 1, 3 that were in Phase 2, and 4 that were in Phase 3.

Eli Lilly

Another note

On Oct. 5 of this year, I wrote another article about Eli Lilly and its acquisition of POINT Biopharma Global (PNT) in a deal valued at $1.4 billion. I viewed this as a solid opportunity for the company. It’s worth noting that, on Nov. 6, shares of the company rose about 2% after Biotechnology Value Fund, an owner of 16.5% of POINT Biopharma Global, pushed back against the transaction and indicated that it does not intend to tender its shares in support of the transaction because it could be leaving significant value on the table. In fact, this was followed up on Nov. 8 with a press release issued by Eli Lilly wherein the company said that it is extending the expiration of its tender offer from Nov. 9 of this year to Nov. 16. Management is expecting a tender of a majority of the outstanding shares of the prospect. But as of the time the tender offer extension was announced, only about 15 million shares, or 14.2% of all stock outstanding in its target, had been tendered. I’m bullish about the transaction, but unless management increases the buyout price rather considerably, we may not see the deal go through. I would see that as a net negative for the enterprise, but not a large enough negative to offset these other bullish developments.

Takeaway

Based on all the data provided, I must say that Eli Lilly is in a fine spot at this point in time. While we have no idea what the future holds, the data today is incredibly bullish and it’s likely that the company will see tremendous revenue growth as this drug catches on. Because of this, I have no problem keeping the business rated a “buy” even after shares have risen so significantly.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Crude Value Insights is an exclusive community of investors who have a taste for oil and natural gas firms. Our main interest is on cash flow and the value and growth prospects that generate the strongest potential for investors. You get access to a 50+ stock model account, in-depth cash flow analyses of E&P firms, and a Live Chat where members can share their knowledge and experiences with one another. Sign up now and your first two weeks are free!