Summary:

- Eli Lilly announced impressive Q1 2024 financial results, with revenue surging by 26% YoY and exceeding expectations for earnings per share.

- The company raised its full-year 2024 revenue guidance and adjusted earnings per share guidance.

- While facing challenges with the price of its stock and supply chain issues, Eli Lilly anticipates significant increases in shipment volumes in the second half of 2024.

- Initiating coverage with a cautious Buy based on Eli Lilly expansion plans, strong management team, and high demand. However, near-term volatility is possible due to all time highs.

- My analysis specializes in identifying companies that are experiencing growth at a reasonable price. Rating systems don’t consider time horizons or investment strategies. My articles aim to inform, not to make decisions.

Morsa Images/DigitalVision via Getty Images

Investment Thesis

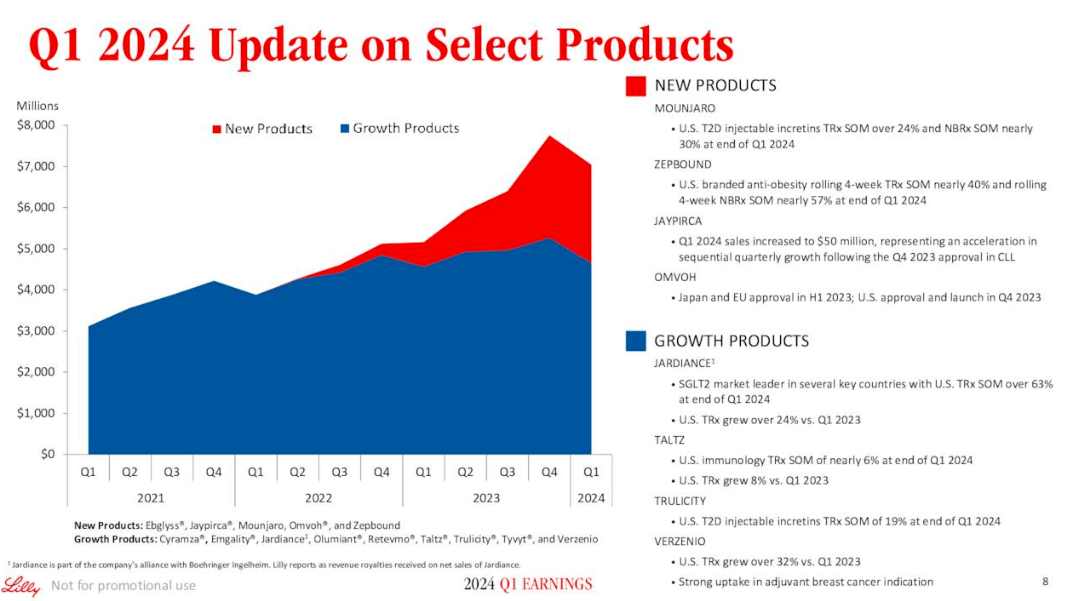

Eli Lilly (NYSE:LLY), announced impressive financial results for the first quarter of 2024. Revenue surged by 26% YoY, fueled by strong sales of not only obesity drugs Mounjaro and Zepbound but also other drugs in their portfolio including Verzenio and Jardiance growing at 40% and 19% respectively. In their latest earnings report, profit rose to $2.24 billion from $1.34 billion a year earlier, with earnings per share exceeding expectations reaching $2.58.

LLY earnings presentation

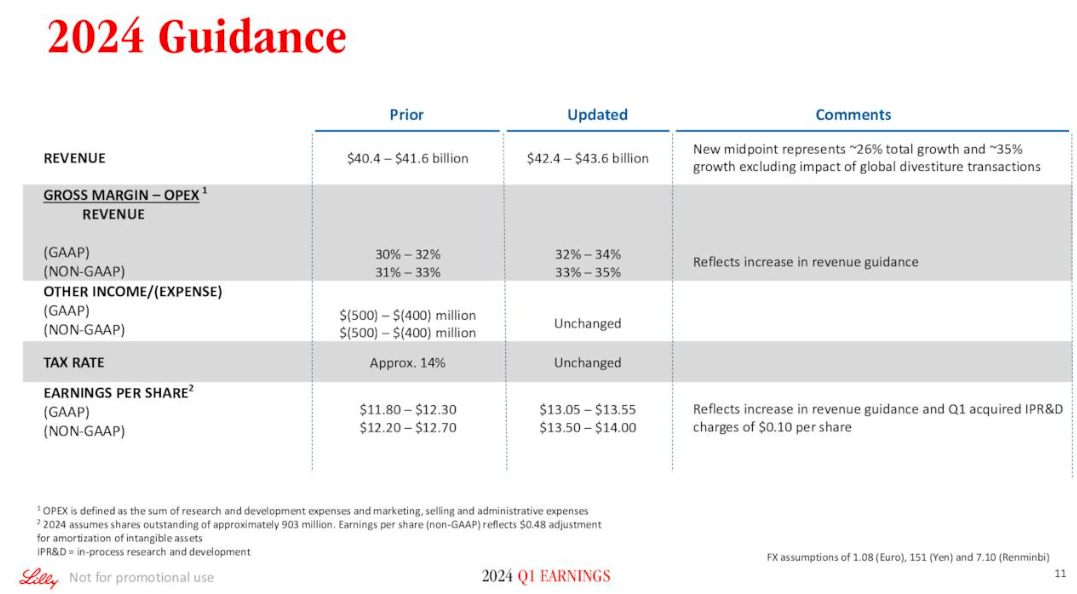

I’m very optimistic about their future and LLY raised its full-year 2024 revenue guidance to a range of $42.4 billion to $43.6 billion, up from the prior estimate of $40.4 billion to $41.6 billion. Similarly, adjusted earnings per share guidance climbed to $13.50 to $14.00 per share, exceeding the previous range of $12.20 to $12.70 per share.

LLY earnings presentation

However, I find that Eli Lilly is not without any challenges. The price of the stock seems to be reaching new all-time highs every month and a deeper look into the company’s financials, corporate strategy and management is needed to get a better picture of its potential.

Also, the company is currently facing supply constraints for some of its most in-demand drugs, particularly Mounjaro and Zepbound, both of which are used for the growing demand for anti-obesity drugs. Despite this hurdle, during the earnings call, LLY’s CFO mentioned that they anticipate significant increases in shipment volumes by the second half of 2024, thanks to ongoing investments in expanding manufacturing capacity.

Given the strength we’re seeing in our business and projections for continued acceleration expected in the second half of the year, we are increasing our full year revenue outlook by $2 billion on the top and bottom ends of the range to be between $42.4 billion to $43.6 billion. This increase is primarily due to the strong performance of Mounjaro and Zepbound and greater visibility and confidence into our production extension for the remainder of 2024.

I aim to find companies that are growing at a reasonable price. I believe LLY is a good candidate as I believe their growth will expands over the mid-term and while exact market share for obesity drugs isn’t available, the high demand and expected growth suggest LLY could continue to be a major player in a market projected to reach $100 billion by 2030. For all these reasons, I am inclined to start coverage on LLY with a cautious Buy.

Management Evaluation

Dave Ricks, Eli Lilly’s CEO for over 7 years, boasts a lengthy and well-rounder career with the company having joined the company in 1996. He posses experience across marketing, sales, drug development, and international operations. Under his leadership, Lilly has achieved record-breaking R&D and business results. Additionally, both Ricks and Eli Lilly have received positive reviews on Glassdoor, indicating employee satisfaction with the company culture and leadership.

I also find that he has a “high alignment ratio” with the company success with a significant portion of around 75% of his compensation tied to the company future success in the form of stock awards.

Salary.com

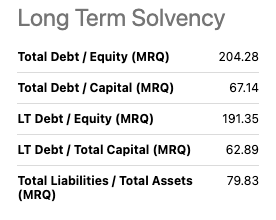

Anat Ashkenazi has extensive experience in finance at Eli Lilly, working across various financial and strategic roles since 2001. Currently, as CFO, she oversees finances for research, development, manufacturing, and commercial aspects of the company. Notably under her leadership, the company has started to fund significant capacity expansion that began in 2023, which increased debt and drove debt to equity ratio above 200%, especially when the company does not have any free cash flow and every dollar spent on interest is not available for future growth. While concerning, I believe the company has entered in a phase where they are capitalizing on previous investments and thus is experiencing revenue growth, suggesting future returns on investments.

However, with declining cash reserves and high debt servicing costs, there’s limited room for additional spending. I believe this presents a key opportunity for future success: growing their cash balance.

Seekingalpha

Finally, Dr. Dan Skovronsky, the company’s Chief Scientific Officer, who boasts a scientific and leadership background. As EVP of Science and Technology, he heads Lilly Research Laboratories and Lilly Immunology, serving as an advisor to the company. Prior to joining Lilly in 2010, he founded and led Avid Radiopharmaceuticals Inc. Throughout his tenure at Lilly, Dr. Skovronsky has held various key positions including Chief Medical Officer and overseen areas like diabetes research and product development.

Overall, I believe the Eli Lilly team demonstrates a strong commitment to the company’s long-term success. Rick’s leadership and high alignment ratio has been noticeable on their Glassdoor review scores. I believe the management is well positioned to navigate the current capacity challenges. Their strategic move into the obesity drug market has demonstrably benefited the company. Given all these factors, I’m rating the Eli Lilly team with an “Exceeds Expectations”.

This is the first time I’ve given a company management this rating. However, it’s crucial to acknowledge inherent risks. The company’s debt level, and free cash flow issues require close monitoring to ensure long-term growth sustainability.

Glassdoor

Corporate Strategy

Eli Lilly boasts a competitive edge over with a diversified drug portfolio. While rivals like Pfizer (PFE) exited the obesity drug race for now, LLY first mover advantage with Mounjaro and Zepbound for weight management positions them strongly. Their diversified portfolio including an Alzheimer’s drug in late-stage trials holds promise in a growing market and positions them better than Novo Nordisk high reliance in their diabetes treatment. Though the exact number of successful drugs is difficult to define, LLY consistent focus on innovation across various therapeutic areas positions them well for future growth, compared to companies potentially over-reliant on one area.

I have created the table below comparing LLY current strategy to some of it current competitors:

|

Eli Lilly |

Novo Nordisk (NVO) |

Amgen (AMGN) |

Roche (OTCQX:RHHBY) |

|

|

Corporate Strategy |

Focuses on innovation in key areas like diabetes, oncology, and immunology. Launching new drugs in key areas including a late stage drug for Alzheimer. Expanding geographically. Strategic collaborations |

Focus on diabetes and other chronic diseases. Maintaining first mover advantage and expanding GP1 portfolio. Investing in R&D for new treatments |

Specializes in the development and marketing of biotechnology drugs. Expanding into new areas. Acquisitions and partnerships focus. |

Focus on pharma and diagnostics, with a strong presence in oncology. Maintaining market share in oncology. Investing in personalized medicine. Expanding into gene therapy. |

|

Obesity Drug Status |

Approved |

Approved |

Mid-stage |

Early Stage |

|

Advantages |

Strong pipeline in diversified portfolio, positive company morale, first mover advantage. |

First mover advantage in diabetes market, established brand recognition in Europe and increasing in the US. |

Strong focus on biologics, history of successful drugs. |

Strong market position in oncology, history of innovation. |

|

Disadvantages |

High debt levels. Free Cash flow issues. |

Reliant on diabetes market future success. Potential generic competition. |

Limited portfolio in small molecule drugs, high R&D costs. |

High drug pricing, potential for generic competition. |

Source: From companies’ website, presentations, SeekingAlpha

Valuation

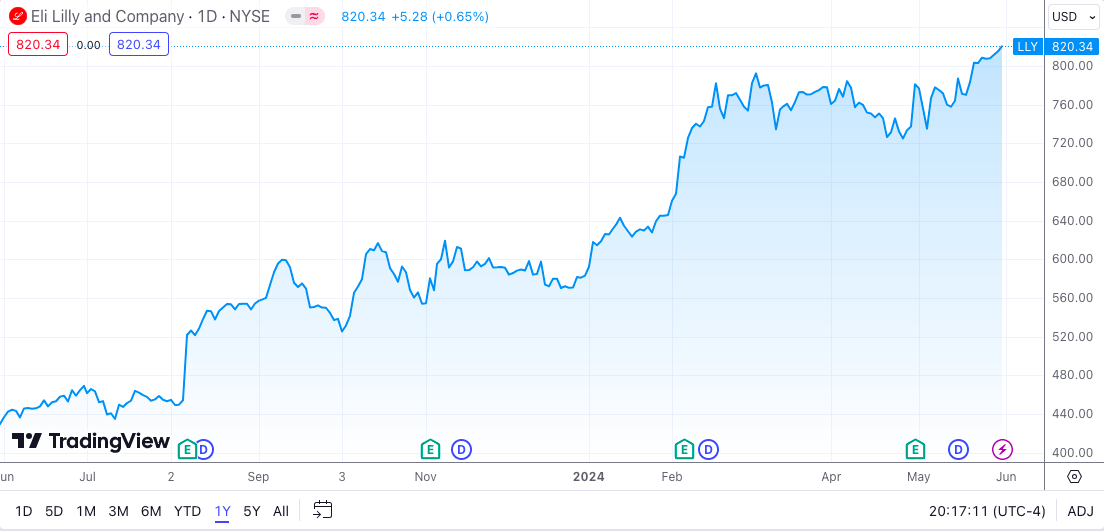

Eli Lilly currently trades at around $820.34, increasing around 5% after it reported earnings in late April.

To assess its value, I employed a conservative 11% discount rate, this rate reflects the minimum return an investor expects to receive for their investments. Here, I am using a 5% risk free rate, combined with the additional risk premium for holding stocks versus risk free investments, I’m using 6% for this risk premium. While this could be further refined, lower or higher, I’m using it as a starting point only to get a gauge for unbiased market expectations.

Then, using a simple 10 year two staged DCF model, I reversed the formula to solve for the high-growth rate. To achieve this, I assumed a conservative terminal growth rate of 4%. In my experience, this rate reflects a slower but more sustainable growth trajectory for mature companies in the long term. Again, this rate can be higher or lower, but from my experience I feel comfortable using a 4% rate. The formula used is:

$820.34 = (sum^10 FCF (1 + “X”) / 1+r)) + TV (sum^10 FCF (1+g) / (1+r))

Solving for g = 34.5%

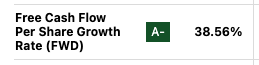

This suggest that the market currently prices LLY FCF to grow at a rate of 34.5%. However, according to Seeking Alpha analyst consensus FCF is expected to grow at a 38.56%.

Seekingalpha

Therefore, I believe Eli Lilly is slightly undervalued at this point with the market only pricing a 34.5% growth in FCF. I also have confidence in the management ability to carry out its expansion strategy and maintain its first mover advantage despite current supply chain challenges.

Technical Analysis

LLY has been on a tear, with their stock price hitting all-time highs recently and closing the week at around $820. However, the 1-year chart reveals occasional dips between earnings reports, like the ones seen in September and October 2023 so it’s hard to predict its short-term path.

Despite its short-term fluctuations, I’m cautiously optimistic about LLY’s long term growth potential. This cautiousness arises from the pharmaceutical industry’s reality: successful drugs often have a short-lived life. New companies can enter the market with a new formula and online pharmacies, like Hims & Hers (HIMS) may bypass FDA during shortages, taking away market share.

While LLY has a diversified drug portfolio, including a promising late-stage Alzheimer drug, offer some protection, their significant focus on the GLP-1 drug might be hindering investments in other areas.

Overall, right now, I believe in the mid-term potential, and I’m inclined to rate the stock a Buy on any weakness; however, close monitoring is crucial. Next earnings report is estimated to be August 8th.

Tradingview

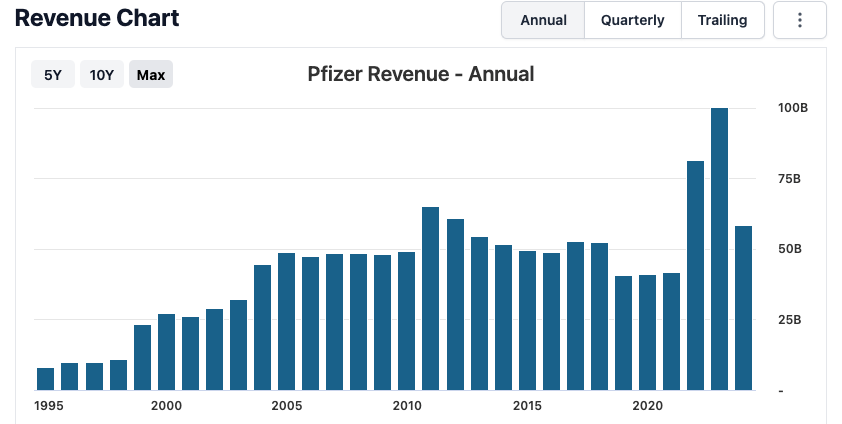

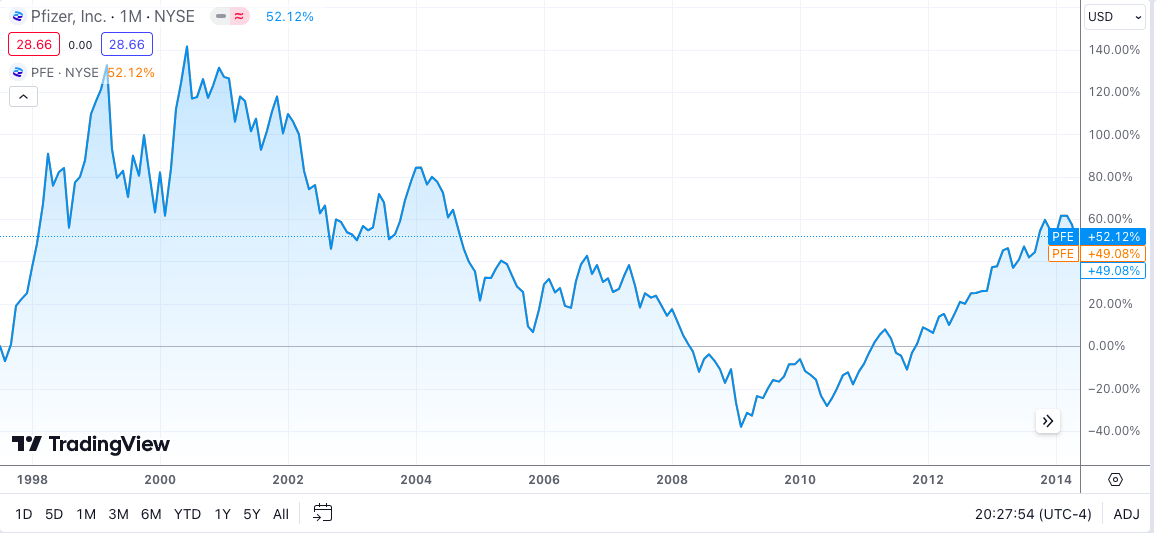

Finally, although a different scenario and time, the dot com bubble, Pfizer’s experience serves as cautionary tale for LLY. After the phenomenal success of Viagra in 1998, Pfizer revenue growth eventually slowed down, impacting their stock price. New entrants, including a drug from LLY, started to compete for market share as soon as 2003.

This underlines the importance of considering all factors that can affect a pharmaceutical company. As new information and market development emerge, I will continuously assess my investment thesis for LLY.

Stockanalysis.com

TradingView

Takeaway

Eli Lilly is on a tear, but closer look is needed. Strong Q1 results and a diversified portfolio are impressive, but high stock price and debt require caution. Management is strong, and the obesity drug lead is a plus. However, free cash flow could potentially become a concern in the future. Valuation suggest LLY is slightly undervalued but competition and focus on GLP-1 drugs are risks. Overall, I find LLY mid-term potential good, but close monitoring is crucial. Given all the factors I am starting my coverage of LLY with a cautious buy.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in LLY over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

My analysis specializes in identifying companies that are experiencing growth at a reasonable price. Rating systems don't consider time horizons or investment strategies. My articles aim to inform, not to make decisions.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.