Summary:

- Energy Transfer LP investors have outperformed their energy sector peers amid the energy market volatility over the past year.

- The recent dispute over pipeline practices highlights the moat-worthy nature of pipeline businesses and their ability to protect excess returns.

- Energy Transfer’s well diversified portfolio and solid execution track record support its continued outperformance.

- I highlight why its robust forward distribution yield of 8.7% underpins my bullish thesis on Energy Transfer.

- With Energy Transfer still relatively undervalued, investors should continue adding more units and going in more aggressively on steep pullbacks.

spooh

Unitholders in midstream infrastructure leader Energy Transfer LP (NYSE:ET) have continued to outperform their energy sector (XLE) peers. The thesis in Energy Transfer is straightforward. As an income-focused play, it has delivered admirable operating performance amid last year’s energy market volatility. I also urged investors to continue buying into ET at my previous November update, driven by its accretive Crestwood acquisition. Bolstered by ET’s primarily fee-based arrangements, Energy Transfer’s cash flows exhibit “limited commodity price sensitivity.” As a result, it provides the predictability and stability that income investors generally desire, coupled with its highly attractive forward distribution yield of 8.7%.

While its yield has normalized closer to ET’s 10Y average of 8.3%, I still gleaned highly constructive buying sentiments on ET, corroborating its outperformance potential. Seeking Alpha Quant’s solid “B+” momentum grade lends credence to my bullish thesis, benefiting energy investors.

ET posted its fourth-quarter earnings release in mid-February amid a recent dispute with The Williams Companies (WMB). Williams shot back at Energy Transfer’s alleged “anti-competitive” practices, denying “other projects from crossing ET’s pipelines.” As a result, it has led to an internal delay in its project timeline. However, Energy Transfer management refuted these claims, arguing that competitors “sought to bypass regulations” by building under the “guise of gathering pipelines.”

Consequently, I believe the recent dispute demonstrated that pipelines are moat-worthy businesses, given the enacted regulatory barriers. Not only do competitors need to invest in advance to capitalize on capturing higher volumes efficiently, but they can also act to deter competition. As a result, we have experienced how it has helped to protect Energy Transfer’s excess returns and cash flow stability.

Despite that, the delays in Energy Transfer’s Lake Charles LNG project indicate that regulatory hurdles cut both ways. The recent moratorium imposed by the Biden Administration on new approvals of LNG exports has also contributed to volatility in the natural gas (NG1:COM) market amid a natural gas supply glut. However, Energy Transfer’s well-diversified portfolio across the energy value chain has allowed the partnership to capture a record performance in 2023, as it “achieved seven operational records in Q4’23.”

As a result, unitholders should expect another solid year of growth CapEx for Energy Transfer, even as it aims to generate about $80M in cost synergies from its Crestwood acquisition (with $65M anticipated in 2024). Accordingly, Energy Transfer telegraphed a growth CapEx of between $2.4B and $2.6B, including $300M in deferred spending from 2023. It broadly aligns with the partnership’s long-term outlook of $2B to $3B. Therefore, I assessed that it demonstrates Energy Transfer’s confidence in delivering solid performances across its portfolio in 2024.

The partnership projects an adjusted EBITDA of $14.65B at the midpoint of its guidance range for 2024, representing a 7% YoY uptick. I don’t expect the growth cadence to continue as it integrates its Crestwood acquisition. As a result, we should expect Energy Transfer’s distributable cash flow or DCF to normalize post-2024, notwithstanding the improved cost synergies emphasized. Revised Wall Street estimates suggest that Energy Transfer’s adjusted EBITDA growth could decelerate to 3.1% in FY25. However, given its best-in-class “A” profitability grade, I expect ET to continue outperforming, bolstered by an attractive valuation and distribution yield.

ET is valued at a forward adjusted EBITDA multiple of 7.9x. Seeking Alpha Quant assigned ET a relatively attractive “B-” valuation grade, underscoring its appeal. However, the market knows it too, as seen in ET’s relative outperformance against its energy sector peers. As a result, are there still opportunities for ET investors to continue adding to their positions, leveraging its robust forward yield?

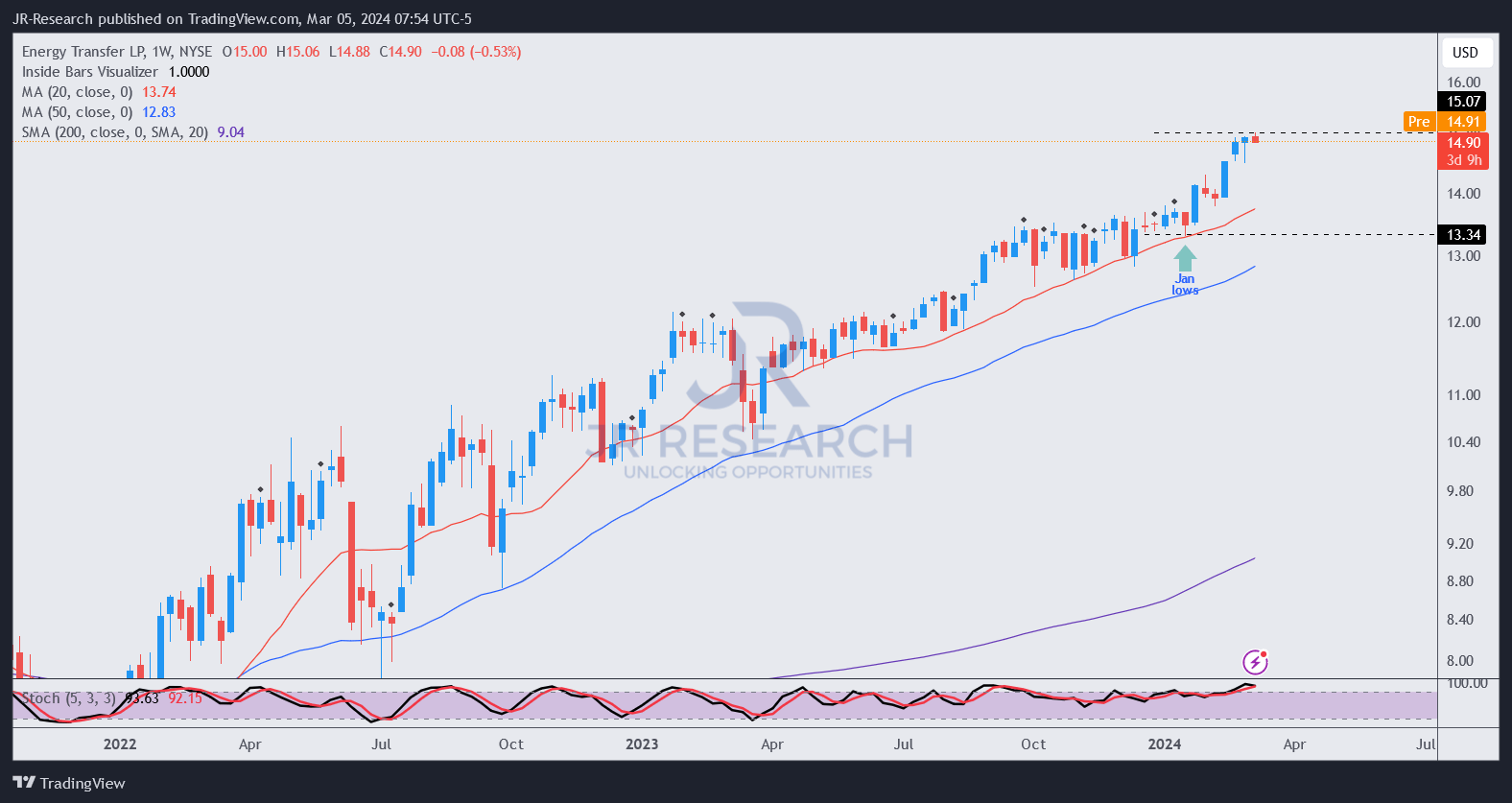

ET price chart (weekly, medium-term, adjusted for distributions) (TradingView)

ET’s medium-term uptrend has continued unabated, with pullbacks offering buying opportunities to level up.

While the $15 level has stalled ET’s recent upward momentum, I didn’t assess red flags on its price action, which could lead to its momentum toppling over decisively.

Energy Transfer’s solid execution track record (“A-” earnings revisions grade) and robust profitability fundamentals support its continued outperformance. Benefiting from a still attractive valuation, ET’s positive price action corroborates the fundamentalist’s perspective.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA’s bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!