Summary:

- Etsy’s stock has declined over 22% in the past year due to changing consumer behavior and increased competition from Amazon and Shopify.

- Despite challenges, Etsy’s focus on specialized platforms like Depop and Reverb shows potential for growth in sustainable and niche markets.

- Financials reveal mixed performance, but Q3 2024 results indicate stability with a slight revenue increase and strong cost control.

- A DCF analysis suggests a potential 25% upside, valuing Etsy shares at around $66.47, supporting a buy rating amidst cautious optimism.

Kenneth Cheung

Introduction

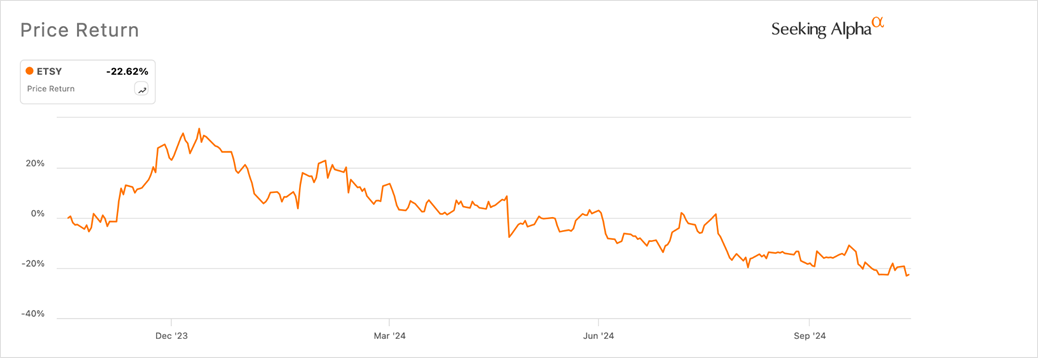

Etsy’s (NASDAQ:ETSY) shares have suffered a significant blow in the last year, falling by more than 22% – a notable decrease that is difficult to ignore. Some years ago, Etsy was thriving, taking full advantage of the e-commerce surge with certainty. However, in recent times, the scenario has changed. Consumer behavior is evolving as individuals prioritize essential items while reducing spending on non-essential luxury purchases. For a platform such as Etsy, which relies on handmade and niche products, this change is deeply impactful. With the increasing competition from major companies like Amazon (AMZN) and Shopify (SHOP), the future growth of Etsy seems more uncertain.

Seeking Alpha Seeking Alpha

However, solely concentrating on Etsy’s stock overlooks a broader perspective. Etsy doesn’t just operate its primary marketplace; it is also the driving force behind brands such as Depop and Reverb, which are capitalizing on growing and enduring markets. Depop is central to the growing resale market, a sector that is becoming popular among younger demographics who appreciate sustainability and unique, pre-owned discoveries. Young people from Gen Z and Millennials are focused on buying and selling items in a sustainable and stylish way through the platform Depop.

Although Etsy’s stock performance may not be strong, the company’s overall plan of focusing on specialized platforms and expanding into new markets indicates that there is still room for growth. It serves as a reminder that brief decreases in stock prices may not always tell the whole story, especially for a company that is committed to expanding and changing to keep up with changing consumer preferences. Etsy’s journey towards success might only be beginning.

The Business Model

Etsy’s a bit of a standout in the online shopping world, but it’s different from what most people might expect. It’s not like Amazon, with aisles upon aisles of the same stuff, and it’s far from the big-box retail machine. The charm here lies in simplicity. Etsy connects small creators, independent artisans, and vintage lovers with buyers looking for something unique, something with a bit of story to it. You won’t find a giant warehouse stacked with products or a complex logistics chain. Instead, Etsy’s role is more like a middleman—quietly bringing buyers and sellers together. In return, Etsy takes a little through fees, keeping the marketplace running without losing that handmade vibe that drew people in to begin with.

For sellers, the setup’s pretty straightforward: list a product, pay $0.20. Simple enough. But with every sale, Etsy takes a 6.5% cut on the total price (including shipping). And if sellers use Etsy’s payment system, they tack on another 3% fee plus $0.25 per order. It seems like a lot when you add it up, but many sellers see it as fair—especially those just starting out with tight budgets. Etsy’s fees cover the platform’s upkeep, and most sellers see this as a reasonable trade-off: a bit of pay to reach a global audience without upfront costs.

And Etsy doesn’t stop at listing fees. It has tools to help sellers succeed like in-platform ads to boost visibility and Etsy Plus for those wanting extra customization. Etsy even promotes items on platforms like Google and social media, where sellers pay an extra fee only if a buyer clicks through and makes a purchase. For some, it’s a relief—a way to get their products out there without wrestling with complicated ad campaigns.

For sellers without the time, money, or know-how to build their own e-commerce site, Etsy can be the ideal choice. It takes care of hosting, payments, and even global shipping logistics, so sellers can focus on creating. And buyers? They come to Etsy for a reason. They’re looking for the unique, the personal. Not just another item on a shelf but something made with care, a product with a bit of heart behind it.

Of course, like any growing platform, Etsy has its share of challenges. Growth always comes with trade-offs, and for Etsy, that’s meant balancing growth with keeping things real. What counts as “handmade”? What qualifies as “vintage”? These aren’t just marketing terms—they’re at the core of Etsy’s brand. So, Etsy has had to set up clearer standards for sellers to make sure buyers get what they came for authentic, hard-to-find items they won’t see on every other marketplace.

In recent years, Etsy has stepped up to improve things for sellers. Better shipping and refined search tools are changes that make things easier for sellers and buyers, too. And with competition coming from all sides, these tweaks are Etsy’s way of helping sellers stand out in a crowded space.

What about Etsy? It is not just a market; it is a type of ecosystem. Artists, collectors of vintage items, and regular shoppers gather in this location, creating an atmosphere that can feel almost intimate at its peak. It functions both as a platform and as a community, facing the same quirks and challenges as real communities. And for many individuals, that’s the reason they choose to stay.

Financials

Etsy’s journey since 2021 resembles a case study on the unpredictable nature of contemporary online retail. In its prime that year, Etsy appeared unbeatable. The stock surged to a staggering $308 in November 2021, as if it could continue increasing endlessly. However, now we find ourselves not too long later, with Etsy’s stock dropping below its levels before the pandemic. What caused Etsy’s momentum to suddenly change is a significant shift that raises some questions.

Stock Info with Tradingview

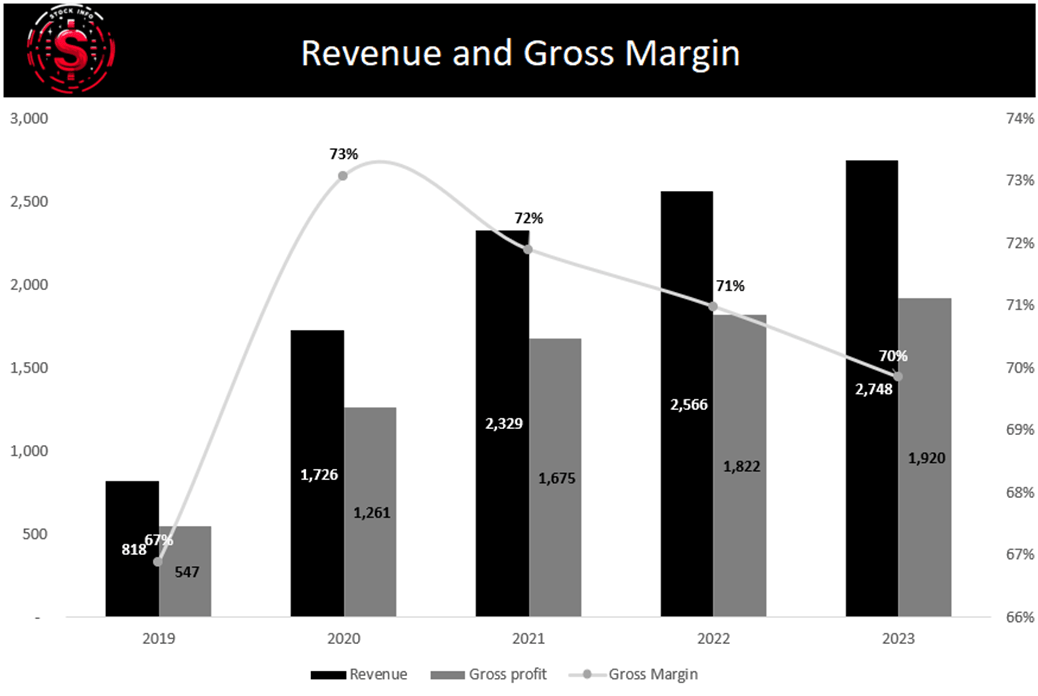

An examination of the financials doesn’t immediately indicate a catastrophe. There has been a slight decrease in gross margins since 2020, but it is not concerning enough to suggest a critical situation. In the midst of the pandemic’s peak period, Etsy experienced a surge in revenue growth, capitalizing on the rise in online shopping and the demand for one-of-a-kind, handmade products while individuals were confined to their homes. However, growth has leveled off since that time. That alone might contribute to the stock’s lackluster performance. However, looking at the bigger picture, Etsy’s margins remain strong, indicating that the company is not losing money rapidly.

Stock Info

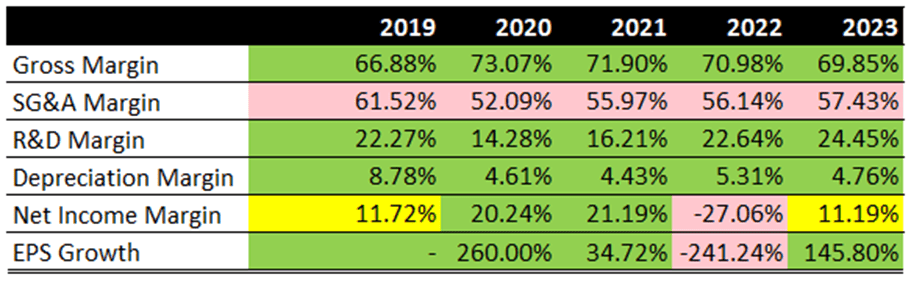

The true warning signal arises when you examine the net profit. 2022 was a difficult year, no doubt, as Etsy experienced a loss, a major setback for a company that was once seen as a strong force for expansion. Although there have been some improvements in 2023, there is not much reason to celebrate. Etsy experienced a significant drop in EPS, falling to -$5.48 in 2022, marking a sharp decline.

Stock Info with Company filings

When you zoom out to a five-year view, the picture doesn’t get much rosier. Yes, Etsy’s five-year CAGR sits at an impressive 27.42%, but that’s really the highlight in an otherwise mixed bag. Operating free cash flow and free cash flow have remained nearly flat over the same period, which is worrisome for a company that once pitched itself as a growth story. Stagnant cash flow doesn’t inspire much confidence, especially when growth was supposed to be Etsy’s defining narrative.

Stock Info

This sluggishness in cash flow reflects a broader sentiment in the market: a growing feeling that Etsy may have backed itself into too small a niche. Its market, once seen as Etsy’s strength, now looks like it might limit the platform’s future growth. And that sentiment is casting a long shadow. Many believe Etsy’s ability to expand is fading, but is that perception entirely accurate?

It’s worth digging deeper. The “no-growth” argument has some truth to it; Etsy’s niche focus could be seen as restrictive. But maybe, just maybe, that argument oversimplifies things. There’s more to consider here, and we’ll explore whether Etsy’s current challenges are signs of long-term stagnation or just growing pains in an evolving market.

A surprisingly good quarter

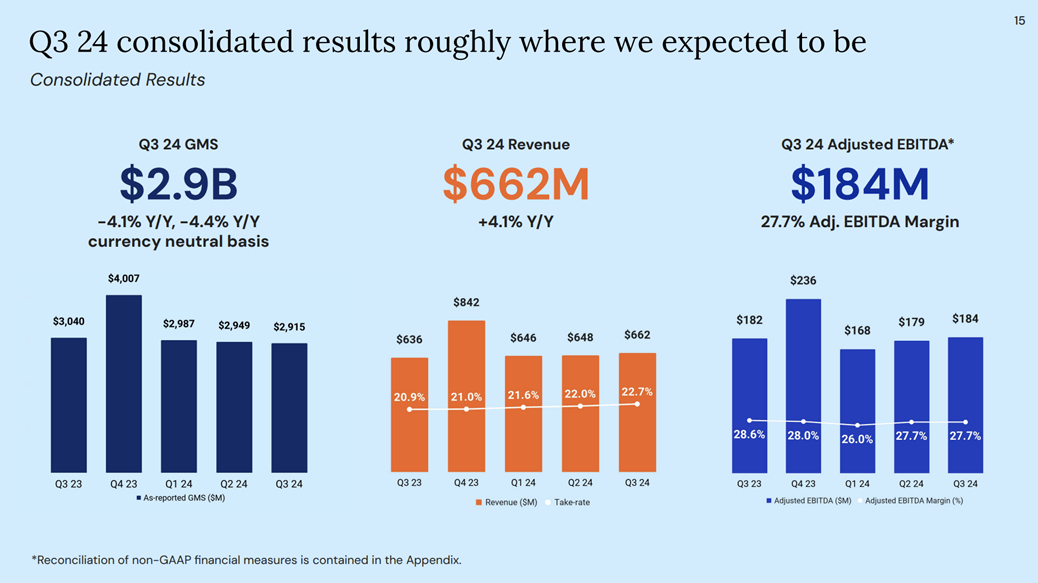

Etsy’s Q3 2024 results lined up pretty much as expected. GMS hit $2.9B, showing a slight drop of 4.1% Y/Y (or 4.4% on a currency-neutral basis). Yeah, it’s down a bit, but that decline really just mirrors some of the challenges Etsy’s dealing with—people cutting back on spending for non-essentials. Still, the numbers suggest Etsy’s marketplace is holding steady, staying active and competitive.

Revenue came in at $662M for the quarter, a 4.1% bump Y/Y. And with a take rate now at 22.7%, Etsy’s managing to capture more of each sale, which is a good sign. Adjusted EBITDA was $184M, slightly up from $179M last quarter, with the margin ticking up to 27.7% from 27%. It may not be a massive jump, but it reflects some solid cost control and smart operations. All in all, these numbers show Etsy’s staying stable, even finding a bit of growth. Looks like they’re handling the economic bumps with some cautious optimism.

Etsy Q3 2024 presentation

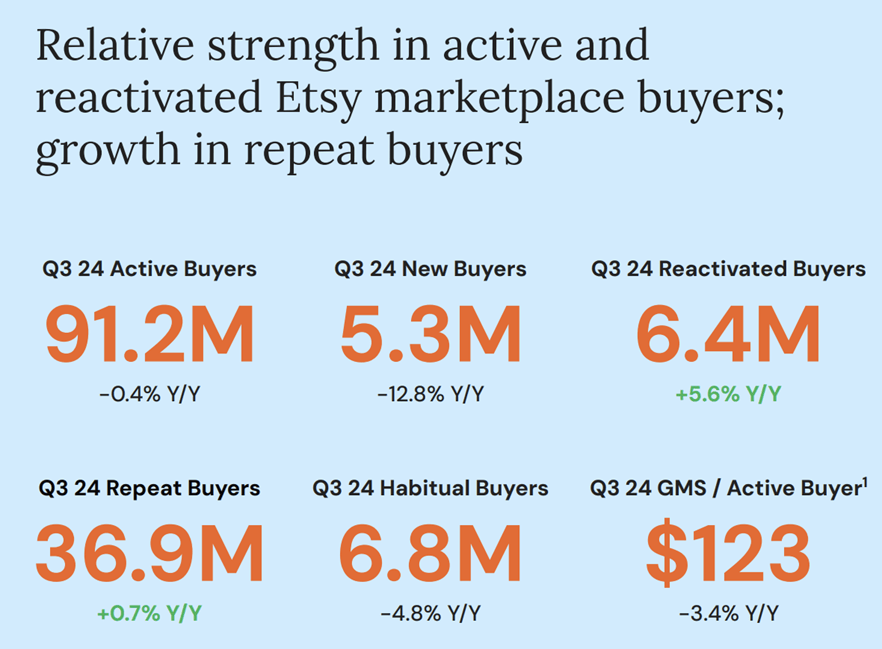

Etsy’s Q3 2024 buyer numbers paint a pretty stable picture, though with a few ups and downs. Active buyers sit at 91.2M, barely down by 0.4% Y/Y, which means most of Etsy’s shopper base is still sticking around. Reactivated buyers—folks who’ve come back after some time away—rose by 5.6% to 6.4M. That’s a good sign, showing Etsy’s got a knack for drawing old users back in.

Repeat buyers grew a bit, too, up 0.7% to hit 36.9M, which points to some solid loyalty. But new buyers are where things get a little trickier, dropping by 12.8% Y/Y to 5.3M. Pulling in fresh users seems to be a challenge. Habitual buyers, or those who shop on Etsy frequently, also dipped by 4.8%, down to 6.8M, which might hint at some caution from Etsy’s most dedicated shoppers, likely due to the broader economic climate. Plus, the GMS per active buyer has edged down by 3.4% Y/Y to $123, so people are spending a bit less on average.

Etsy’s still doing a decent job at keeping its core audience engaged and bringing some buyers back, even if it’s facing some bumps with new and frequent shoppers. There’s room to grow, but the platform’s holding steady where it counts.

Etsy Q3 2024 presentation

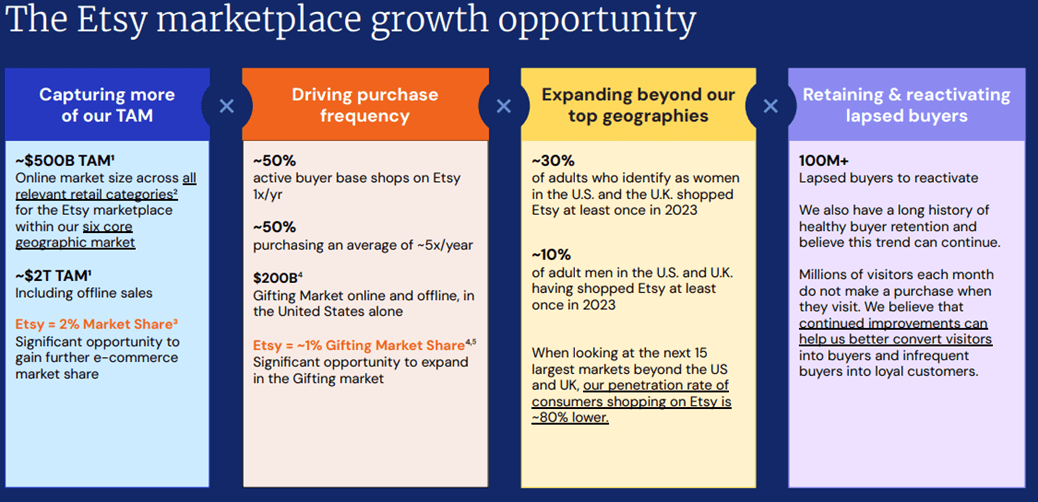

Etsy’s core marketplace may be steady, but the real excitement lies in its expansions with Depop and Reverb. These aren’t just side projects—they’re tapping into booming markets that resonate with younger, trend-driven shoppers. Depop, for instance, is capitalizing on Gen Z and Millennials’ love for resale, both for affordability and sustainability. It’s positioned right in the middle of the thrifted fashion movement, helping shoppers build unique wardrobes with less waste.

Etsy Q3 Earnings presentation

Then there’s Reverb, Etsy’s marketplace for musical instruments. It may be smaller, but it has a strong, loyal community. With a TAM of $24B in musical instruments, including $8B in used items, Reverb is attracting everyone from seasoned musicians to beginners looking for affordable gear.

Etsy Q3 Presentation

A surprising upside based on discounted cash flow

Whether you’re optimistic about Etsy’s growth or cautious, running a DCF analysis on its current cash flow is useful for uncovering hidden value that might not be obvious at first glance.

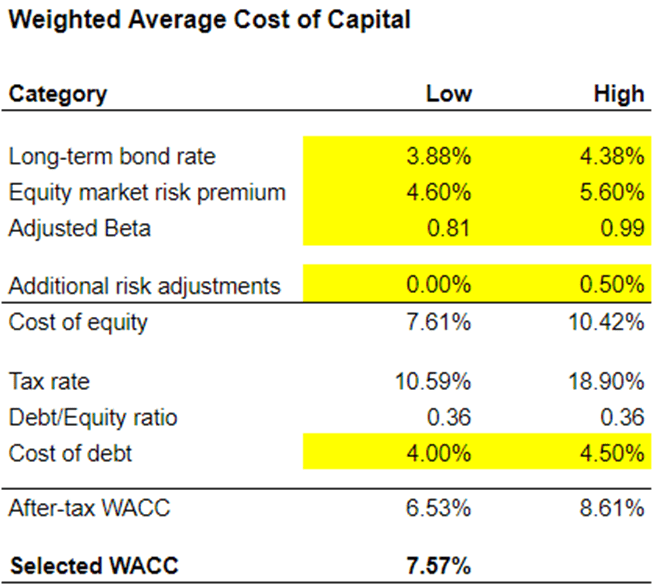

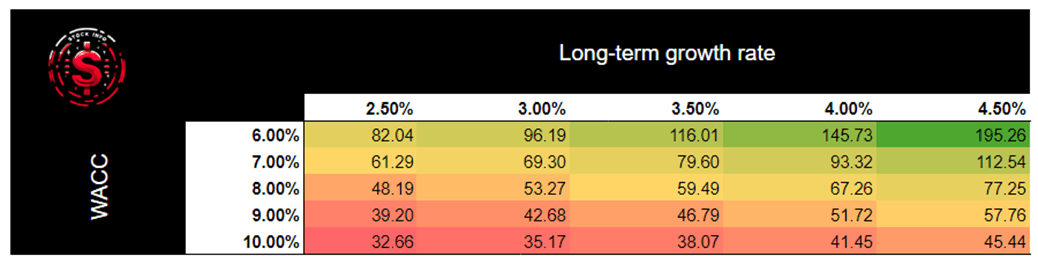

We began with the US 10-year bond rate as our long-term bond rate, integrating it into WACC calculations. This approach extended to the market risk premium and Etsy’s adjusted beta, along with other model inputs, resulting in a WACC of about 7.57%.

Stock Info Stock Info

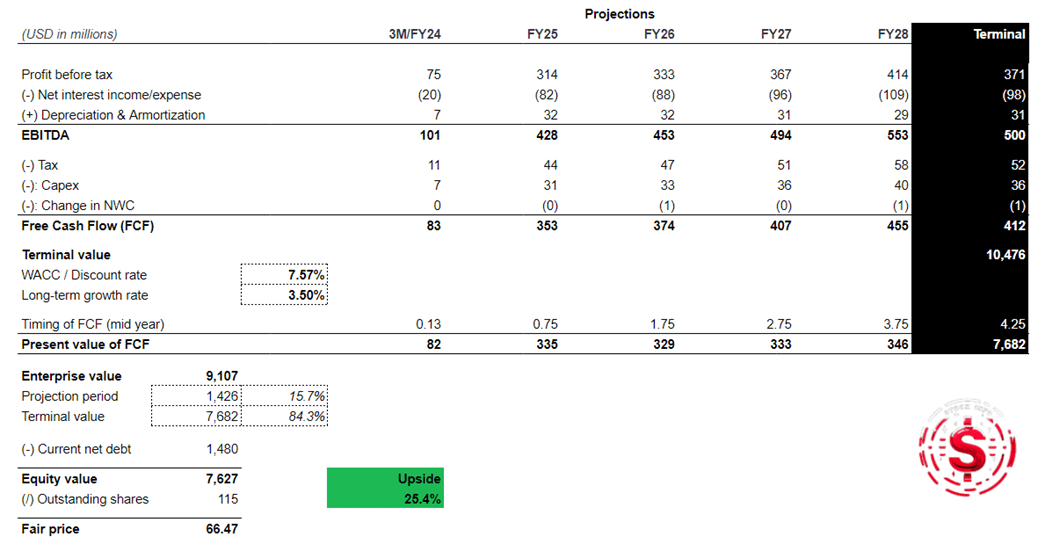

We then plugged this WACC into our DCF model, using Etsy’s latest earnings and assuming a conservative long-term growth rate of 3.5%. Some might say this rate is too cautious, but it felt appropriate. With these inputs, we arrived at an equity value of ~$7,545M. With ~115M outstanding shares, this yields a fair value estimate of $66.47 per share, as detailed in the tables above and below.

Stock Info

Given Etsy was trading around $53 at the time following its earnings release, this valuation indicates an almost 25% upside. That’s solid potential, especially with a big liquidity zone near $49-$50, as seen in the TradingView chart we referenced earlier.

This valuation, of course, depends on our specific model parameters and should be seen as one possible fair value estimate. The sensitivity matrix below illustrates how fair value shifts with changes to the growth rate and WACC, providing flexibility for experimenting with alternate WACC or growth assumptions – basically, you can use your own assumptions to generate a fair value of your own.

Stock Info Stock Info

While our DCF model points to potential upside, Etsy’s future still holds risks. The co. faces intense competition, and its reliance on discretionary spending adds uncertainty. Even with a solid valuation suggesting fair value, Etsy’s future hinges on navigating challenges like changing consumer priorities, heavy competition, and keeping sellers engaged while managing costs. Considering these risks alongside potential gains is essential for a full view of Etsy’s prospects.

Risks

Even with some relief from inflation and interest rates, Etsy faces plenty of challenges that could keep its stock on a downward slope. Consumer behavior is shifting, and while inflation has slowed, people remain cautious, prioritizing essentials over the unique, handmade goods that Etsy thrives on. This caution around non-essentials could easily slow Etsy’s growth.

The competition is fierce, too. Amazon’s “Handmade” section targets Etsy’s artisanal shoppers, while Shopify gives sellers customizable storefronts—an attractive option for those who want more control. To keep sellers and buyers engaged, Etsy might need to boost marketing or adjust fees, but moves like that could stress already tight margins.

Etsy’s reliance on small, independent sellers adds to the pressure. When Etsy raised fees in 2022, seller backlash was immediate. Another hike could drive sellers to alternatives like Shopify or social media platforms, reducing product diversity and dampening buyer interest.

On top of this, Etsy faces a maze of global regulations, from the EU’s VAT rules to evolving U.S. tax laws. Complying with these can be costly, both for Etsy and its sellers, who may find the added burden unmanageable. Each of these risks—shifting consumer habits, competition, seller dissatisfaction, and regulatory pressures—casts doubt on Etsy’s future. While the economy shows signs of improvement, Etsy’s path forward is far from clear.

Conclusion

Although Etsy’s stock has experienced a significant decline of over 22% in the past year, this doesn’t necessarily indicate a gloomy outlook for the future. Certainly, actual obstacles include stagnant sales, increased competition, and shifting buyer behaviors. Etsy is not just idling. The company is expanding its presence in various sectors, aiming to stimulate expansion and attract fresh clientele.

Consider its affiliated companies, Depop and Reverb. These are more than just small projects; they are Etsy’s way of entering new markets – vintage clothing and instruments. Both areas prioritize sustainability and personal touches, which resonate with younger consumers. Etsy’s management is demonstrating its willingness to expand beyond the main marketplace and explore opportunities that align with Etsy’s principles.

Our model suggests that Etsy has a decent amount of value in it, and their recent Q3 earnings show that Etsy still has potential for growth despite a difficult environment and stiff competition. We are giving Etsy a buy rating with a target price in the high $60s.

Some might see these ventures as distractions, but they’re central to Etsy’s strategy to diversify and grow. Etsy’s management is actively reaching into new niches and geographies, aiming to expand beyond the core platform. With a TAM of $500B across its main categories—and potentially $2T when adding offline sales—Etsy has big opportunities. Challenges like flat growth and competition are there, but with Depop and Reverb, Etsy is positioning itself for a future that could exceed expectations.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.