Summary:

- Recent stock price pullback has made XOM an attractive option for commodity exposure under Ray Dalio’s 4-asset model.

- XOM’s profit displays strong correlations with natural gas and oil prices.

- In addition, XOM shares offer a discounted valuation due to recent price corrections.

- Finally, in contrast to commodity’s notorious price volatilities, XOM enjoys a much more stable earnings growth.

sefa ozel

XOM stock: Previous thesis and new developments

I recently wrote an article on Exxon Mobil stock (NYSE:XOM) under the title “Exxon Mobil Q2: Pioneer Assets Create More Upside Potential.” It was published on Aug. 2, 2024. The article was a review of its Q2 earnings as the title suggests. Specifically, I argued that:

Exxon Mobil Corporation stock delivered strong Q2 earnings, beating consensus estimates on both lines. In particular, the progress and benefits from the Pioneer assets integration far exceeded my earlier expectations. The Pioneer acquisition boosts Q2 production to record levels, and I also expect it to lower breakeven costs. Combined with other catalysts, I see good odds for its share price to reach $174 in the next 1-2 years.

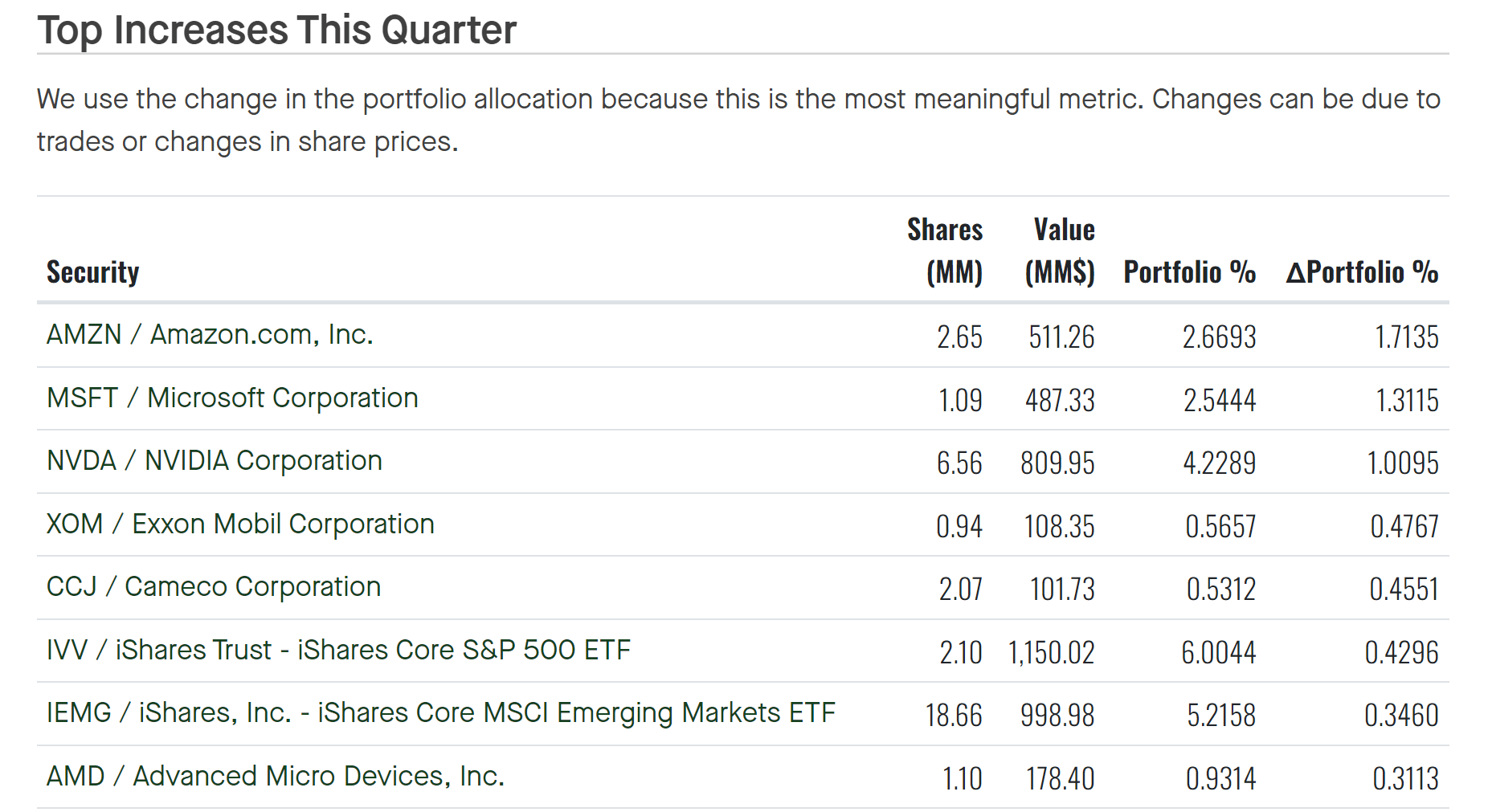

Since that writing, there have been a few new developments surrounding the stock that motivated this update. First, the stock price pulled back a bit (by about 5% since my writing) and thus offers a more attractive valuation (more on this later). More importantly, Bridgewater Associates recently filed its latest 13F and the filing disclosed a sizable addition to its energy exposure. More specifically, as you can see from the chart below, XOM ranked the fourth-largest position increase for Bridgewater in the past quarter. The position increased from 151k shares a quarter ago to the current 941k shares. Besides XOM, Bridgewater also opened a new position in Chevron (CVX), a stock that I added myself in the past few weeks.

These developments promoted me to analyze XOM from the perspective of Ray Dalio’s (Bridgewater’s founder) view on diversification, especially his four-asset model. In the remainder of this article, I will explain why energy shares like XOM and CVX are excellent proxies (or even better proxies than buying a commodity fund directly) for commodity exposure under current conditions.

Fintel

XOM stock and Dalio’s 4-asset model

For readers new to our investing approach and/or Dalio’s 4-asset model, let me start with some basics. These basics have been covered in our early articles and are briefly recapped here:

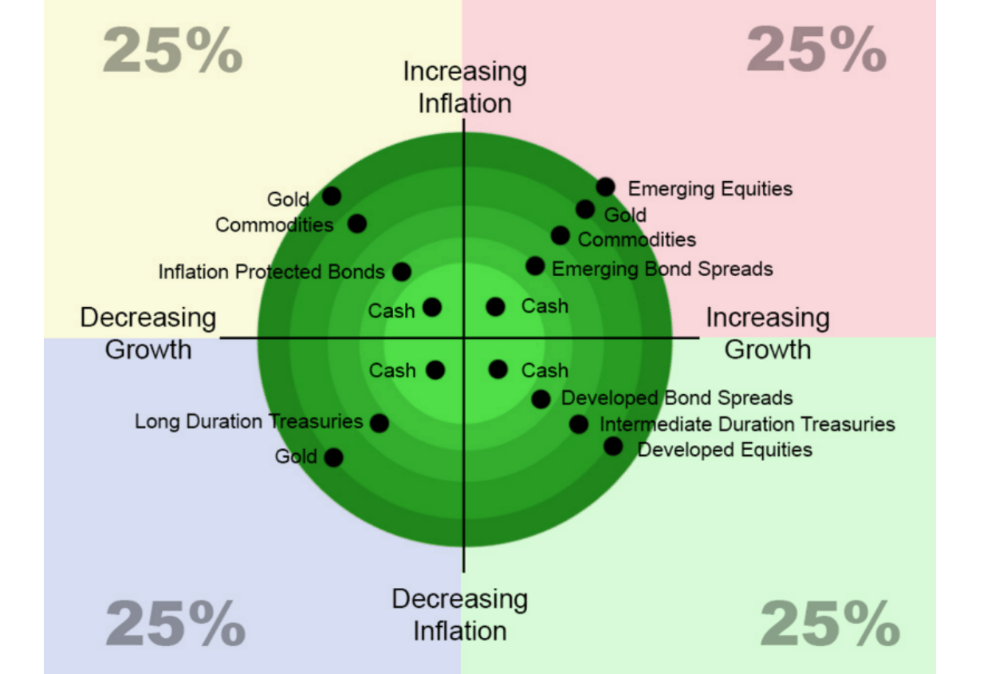

Diversification across different stocks is the LAST step of investing. The grand investing hierarchy should begin with risk isolation, asset class allocation, geographical diversification, and consideration of macroscopic cycles. That is why our first step is always risk isolation using a barbell model. Then the second step is asset allocation across classes that respond differently to fundamental economic forces. Ray Dalio identified four of them as shown in the chart below. Only after these steps do other more detailed steps follow (such as the choice of specific stocks).

macro-ops.com

Next, I will explain why XOM is a good way to gain commodity exposure under this grand scheme under current conditions. My considerations fall into the following three buckets and I will elaborate on them one by one in the rest of the article.

- Its earnings correlated with two key commodity prices (i.e., natural gas and oil prices) closely.

- Its valuation is at a substantial discount under current conditions.

- Unlike community prices that suffer random volatilities, XOM’s earnings enjoy much better stability and growth persistence.

XOM stock’s correlation with commodity prices

The chart below shows the correlation between XOM stock’s quarterly operating cash flow and natural gas price (top panel) and oil price (bottom panel). You can see XOM’s operating cash flow has been quite closely (i.e., positively) correlated with both commodity prices.

To wit, the top panel shows the relationship between XOM’s cash flow and Henry Hub’s natural gas spot prices. Over the long term, the correlation coefficient between these two variables fluctuated but generally remained positive and was close to 1 for extended durations (which would represent a perfect correlation). The long-term average is a positive 0.526. The bottom panel displays the correlation between XOM’s cash flow and gas and the West Texas Intermediate crude oil spot prices. As seen, similar to the relationship with natural gas, the correlation coefficient between XOM’s cash flow and WTI prices has also been generally positive and large over the long term. The average correlation coefficient is 0.658, suggesting an even stronger correlation compared to natural gas.

Such close correlation provides commodity exposure to our portfolio without directly owning a commodity fund, which often charges relatively expensive fees and features more trading friction than XOM or CVX shares. Besides these advantages, next, I will explain two more advantages which are far more potent in my view under current conditions.

Seeking Alpha![xom]](https://static.seekingalpha.com/uploads/2024/9/11/48844541-17260640915498996_origin.png)

XOM stock: Discounted valuation

First, XOM is for sale at a sizable discount, thus offering a wide margin of safety. More specifically, the chart below compares the P/E ratios and dividend yield for XOM stock against its five-year averages. As seen, both the TTM and FWD P/E ratios for XOM are below their five-year average, indicating a discounted valuation. To wit, the TTM P/E ratio of 12.38 is about 8% lower than its five-year average of 13.43. The FWD P/E ratio of 13.01 is almost 13% lower.

Seeking Alpha![xom]](https://static.seekingalpha.com/uploads/2024/9/11/48844541-17260640912828062_origin.png)

XOM stock: EPS growth outlook

The second advantage that XOM offers is more persistent earnings growth in contrast to the large and random price volatilities that commodity prices are notorious for. More specifically, the chart below shows the consensus EPS estimates for XOM stock in the next five years. As seen from these consensus estimates, XOM’s EPS is expected to experience a rather stable growth curve during this period. The company’s earnings are projected to grow from about $8.51 per share in FY 2024 to about $10.04 in five fiscal years, translating into a compound annual growth rate (“CAGR”) of 4.1%. Under this growth projection, the forward P/E ratios are projected to decrease steadily in tandem, from the current 13.02x to only 11.04 in FY 2028.

I indeed see plenty of growth catalysts to support such a projection for Exxon Mobil. As detailed in my last article, the recently closed purchase of Pioneer Natural Resources is the top one on my list. This acquisition has already begun to bear fruit on both the top and bottom lines. Meanwhile, integration and merger-related cost synergies are quickly being realized. With its strong cash flow, I expect the company to accelerate its share repurchases to offset the acquisition-related share dilution and boost EPS growth.

Seeking Alpha![xom]](https://static.seekingalpha.com/uploads/2024/9/11/48844541-17260640916360674_origin.png)

Other risks and final thoughts

As a popular stock on the Seeking Alpha platform, several recent articles by other authors (especially those with a bearish view) have thoroughly discussed the downside risks associated with XOM. I won’t repeat their analysis here anymore. Here, I will just point out a few issues that are more specific to the thesis in this article.

Using XOM (or other energy shares) as a proxy for commodity exposure has certain advantages under current conditions as argued above (valuation discounts, generous dividends, lower earning/price volatility, etc.). However, there are also deviations and limitations. The company’s traditional oil and gas operations correlate closely with commodity prices. However, an increasingly diversified operating structure could decrease such coloration in the long term. For example, XOM is expanding its alternative energy portfolio. Specifically, the company is investing heavily in carbon capture and storage, lithium battery development, and the more mainstream clean energy arenas, solar, wind, and hydrogen. These developments could be good news from a business perspective. However, I expect them to weaken my argument for using XOM as a proxy for commodity exposure over time. They could also introduce additional uncertainties such as environmental and legal risks that commodity funds don’t normally face.

To conclude, with the many macroeconomic and geopolitical risks afoot, I think now is a good time for investors to consider diversification from a more strategic level. In addition to diversification among different stocks/sectors, investors should also consider diversification across different asset classes, including commodities. It’s the goal of this article to explain why the recent price correction in the energy sector has offered XOM not only as a viable but also as an attractive proxy for commodity exposure.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CVX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.