XOM’s stock price has diverged from the broader market since my last writing.

The price diverge, combined with the new development in its business fundamentals, has made XOM an even stronger buy.

Besides my outlook for higher oil prices, I also see several key catalysts afoot that are more specific to XOM.

The top two are XOM’s margin recovery and the acquisition of the Pioneer assets.

The acquisition boasts some of the lowest breakeven costs and could double XOM’s throughput in that region.

z1b

XOM stock: pullback offers an entry point

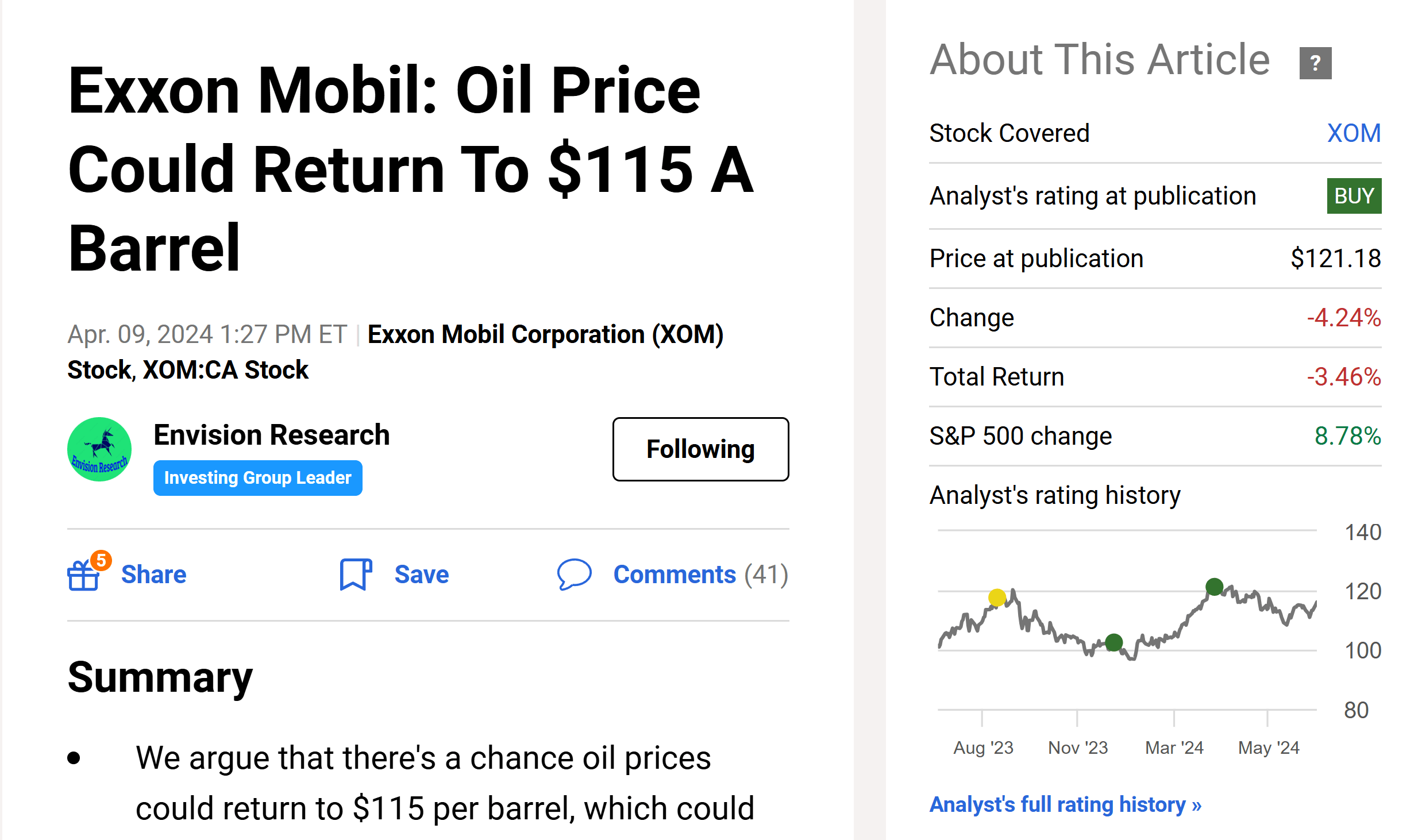

I last covered Exxon Mobil (NYSE:XOM) with a bull thesis a little more than three months ago as you can see from the chart below. To wit, the article was entitled “XOM: Oil Price Could Return To $115 A Barrel” and was published on Seeking Alpha on April 9, 2024. The article focused on the potential catalysts that could drive oil prices up and the subsequent impact on XOM’s EPS. More specifically, the article argued that:

… there is a chance that oil prices could return to $115 per barrel, which could push Exxon Mobil’s stock price to around $200. Exxon Mobil’s breakeven oil price is well below the current oil price, and every dollar of oil price adds about $0.21 to its bottom line. Key catalysts for higher oil prices include inflation, geopolitical tensions, production cuts by OPEC, and recovering global economies.

Seeking Alpha

The article was thus more oriented toward the macro perspective. Since then, there have been a few new developments that motivated this updated assessment. First, the stock price has diverged from the broader market since my last writing. As seen in the chart, XOM’s price suffered a 4% pullback while the market advanced by almost 9%. Second, XOM has released its quarterly earnings and provided more updated information about its financials and business operations.

Against this background, this article will switch the perspective to focus on issues and catalysts more specific to XOM. And as you will see, my conclusion from this updated assessment is that the recent price pullback has made XOM an even stronger buy.

XOM stock: EPS outlook and margin expansion

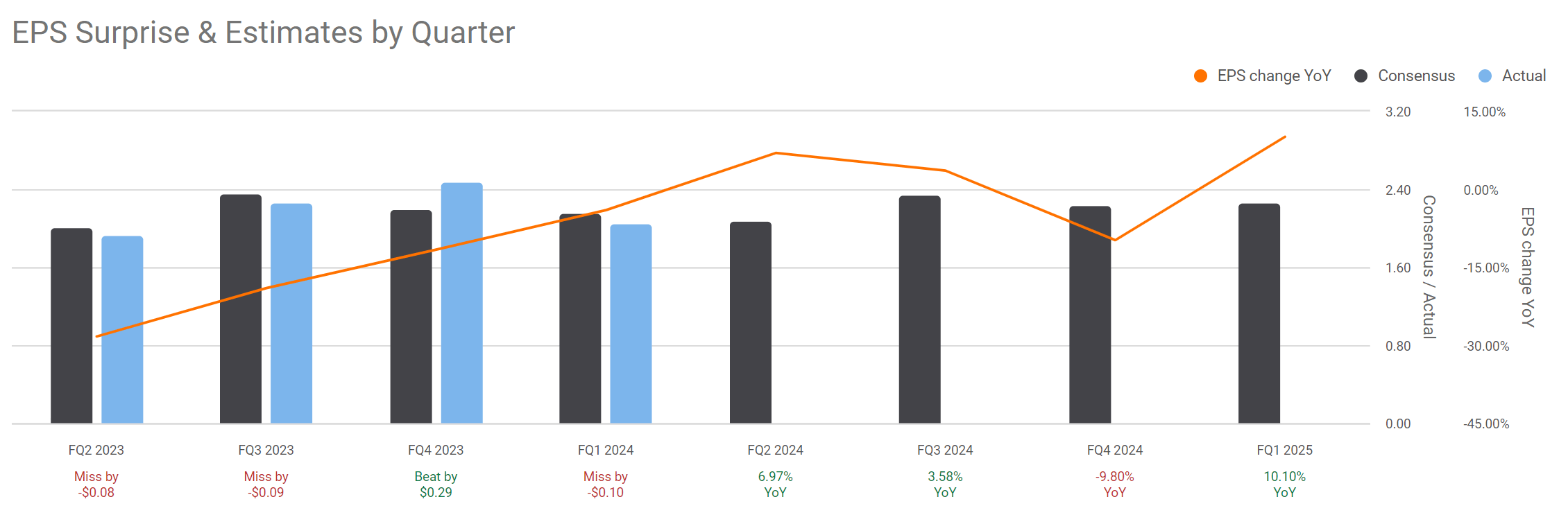

For earnings reported in Q1 2024, XOM earned $2.06 per share. It’s better than what I expected but missed consensus estimates by $0.1 (see the chart below). The key headwind in my view is the refining margin, which contracted year over year owing to relatively lower commodity prices. However, there are notable positives too, such as strong upstream production, particularly in Guyana, and the expansion at the Beaumont refinery.

Seeking Alpha

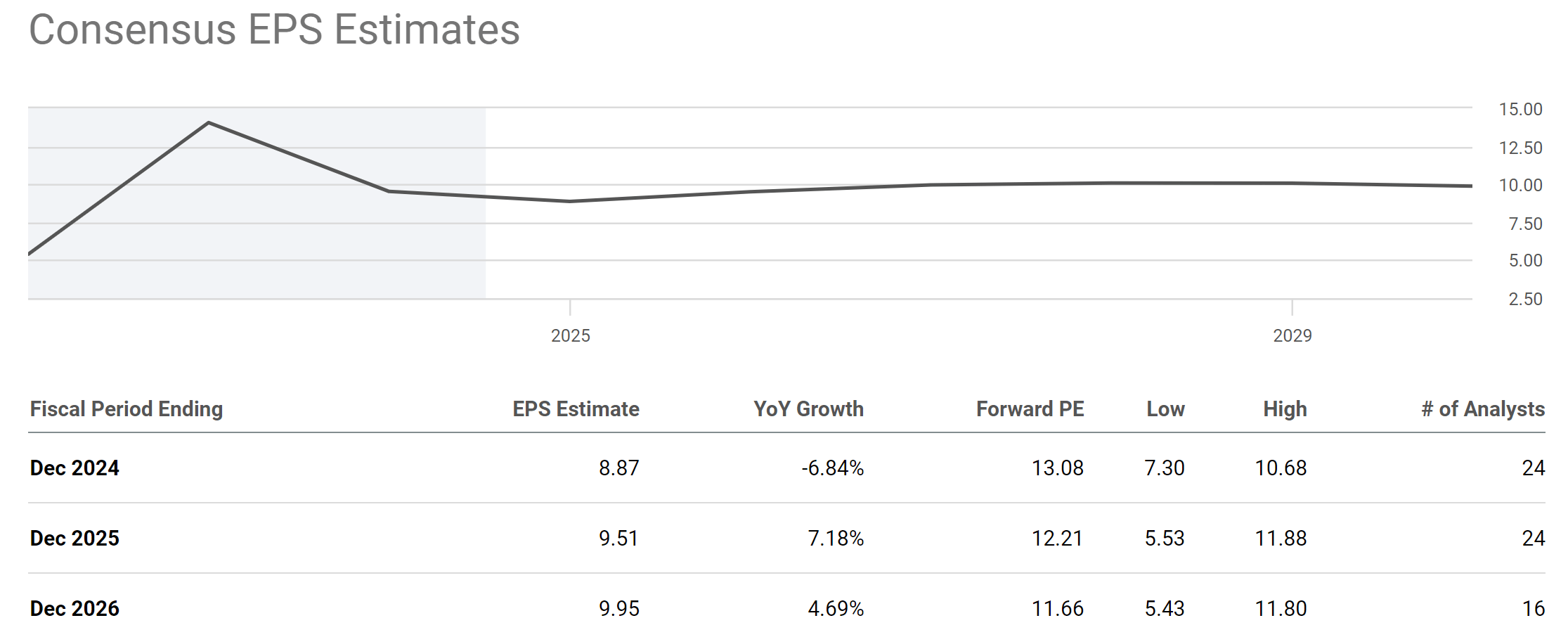

Looking ahead, the market expects a robust EPS recovery starting in 2025. More specifically, the chart below shows consensus EPS estimates for XOM stock in the next few years. As seen, the consensus EPS estimates for XOM stock point to a 6.84% decrease in FY 2024 YOY, followed by a 7.18% increase in FY 2025 and another 4.69% increase in FY 2026. The price pullback, combined with the EPS recovery potential, has translated into very attractive valuation multiples. As seen, the FWD P/E ratio for 2024 is 13.08 currently and will decline to 12.21 in 2025 and 11.66 in 2026 based on the consensus EPS. I will revisit the implications of such multiples a bit later.

Seeking Alpha

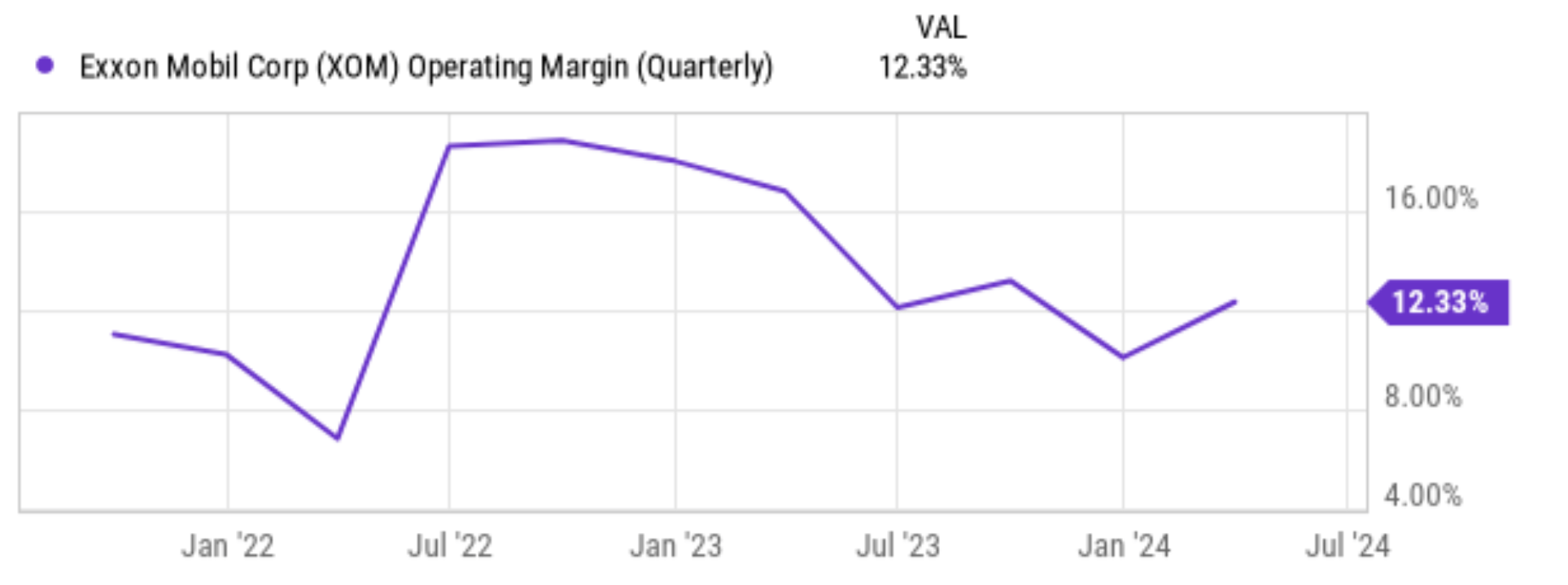

I see the same profitability recovery potential for several key reasons. First and foremost, as argued in my earlier article, I’m still seeing large odds for higher oil prices. Second, XOM has been effective in its cost controls and operating improvements, which has been helping to prop up the bottom line despite commodity price fluctuations. More specifically, the chart below shows the operating margin for XOM stock in recent quarters. As seen, the operating margin for XOM stock has been under pressure after peaking in July 2022, falling from around 17% to as low as ~9.07% at the end of 2023. However, since 2024, the margin has reversed trend and expanded to the current level of 12.33%.

Finally, XOM has recently completed the acquisition of Pioneer Natural Resources. As elaborated on next, I expect this to be a key growth driver in the years to come.

Seeking Alpha

XOM stock: Acquisition of Pioneer Natural Resources

XOM recently finalized its acquisition of Pioneer Natural Resources. Pioneer shareholders received 2.3234 shares of Exxon Mobil for each share held. The deal effectively doubles the company’s operating presence in the Permian Basin. XOM investors should read the release in full detail. Here I will just quote my takeaway (with the emphasis added by me):

The merger of Exxon Mobil and Pioneer creates an Unconventional business with the largest, high-return development potential in the Permian Basin. The combined company’s more than 1.4 million net acres in the Delaware and Midland basins have an estimated 16 billion barrels of oil equivalent resource. Exxon Mobil’s Permian production volume will more than double to 1.3 million barrels of oil equivalent per day (MOEBD), based on 2023 volumes, and is expected to increase to approximately 2 MOEBD in 2027, based on initial estimates… Combining Pioneer’s differentiated Permian inventory and basin knowledge with ExxonMobil’s proprietary technologies, financial resources, and industry-leading project execution excellence is expected to generate double-digit returns by recovering more resources….

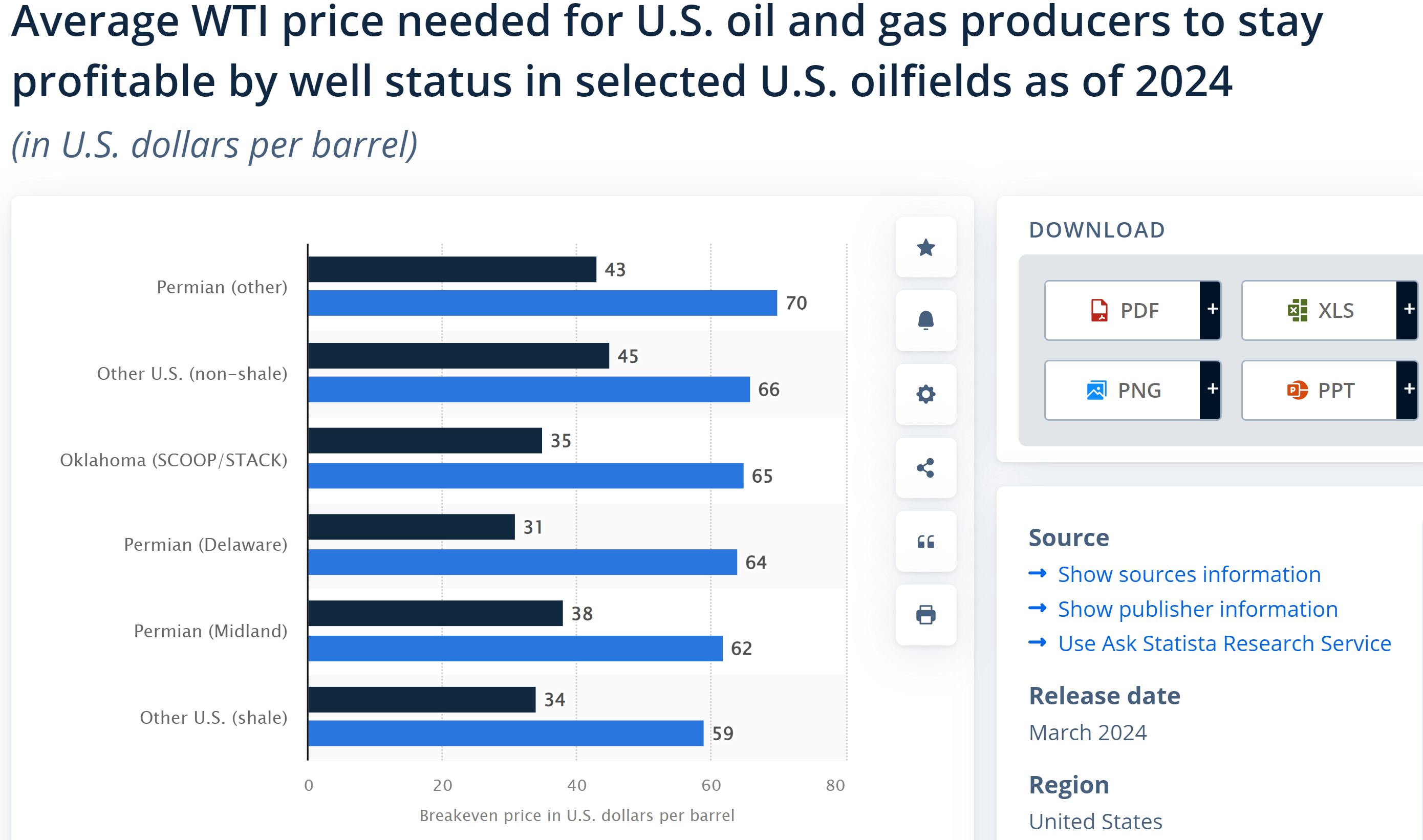

Indeed, I’m very optimistic about the capacity ramp-up and double-digit return potential the company anticipates. The acquired assets boast some of the lowest break-even production prices (at least among U.S. oil producers). The next chart below shows the breakeven oil prices for the major oil and gas producers in the U.S. As seen, the average WTI price needed for U.S. oil and gas producers to stay profitable (2024 figure) ranges from $31 to $45 per barrel for various well statuses in different U.S. oilfields. And the lowest breakeven price is $31 per barrel for the Permian (Delaware) region.

Statistica

Other risks and final thoughts

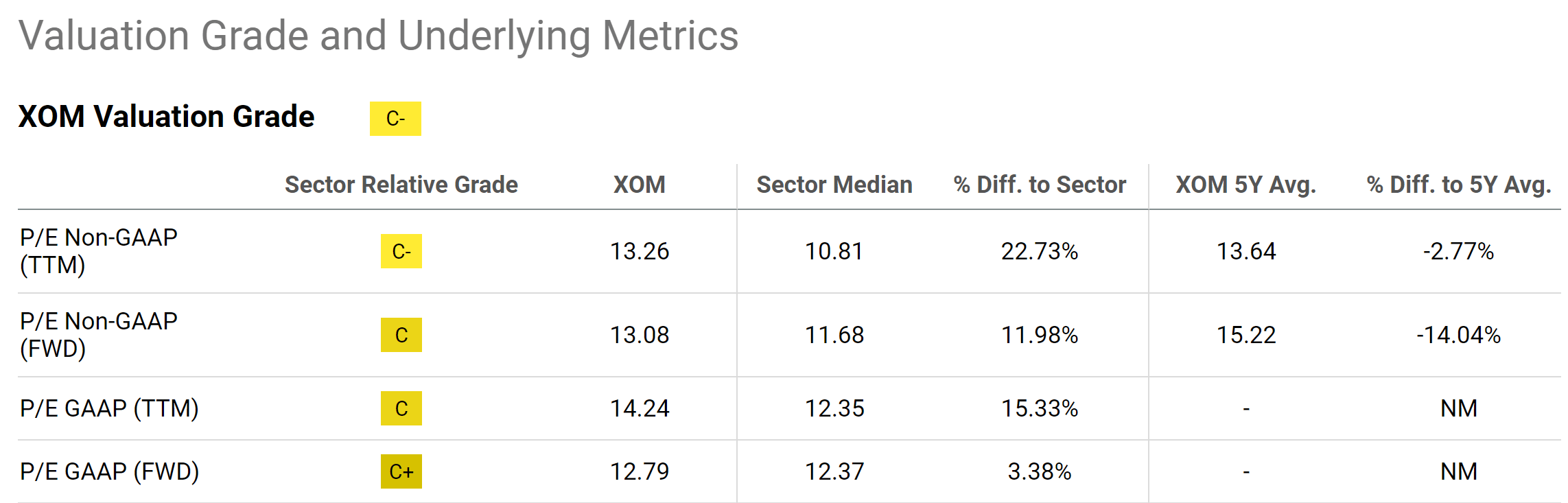

Another upside risk is the attractive valuation. As aforementioned, the recent price corrections, combined with the earnings growth potential, have resulted in a very attractive entry point. The FWD P/E ratio is only 13.08 (on a non-GAAP basis). It’s more than 14% below its historical average as seen in the next chart, which summarizes XOM stock’s valuation grade. With the EPS growth, the implied P/E ratio would shrink to about 11x in about two years, too attractive to ignore for such a sector leader.

Seeking Alpha

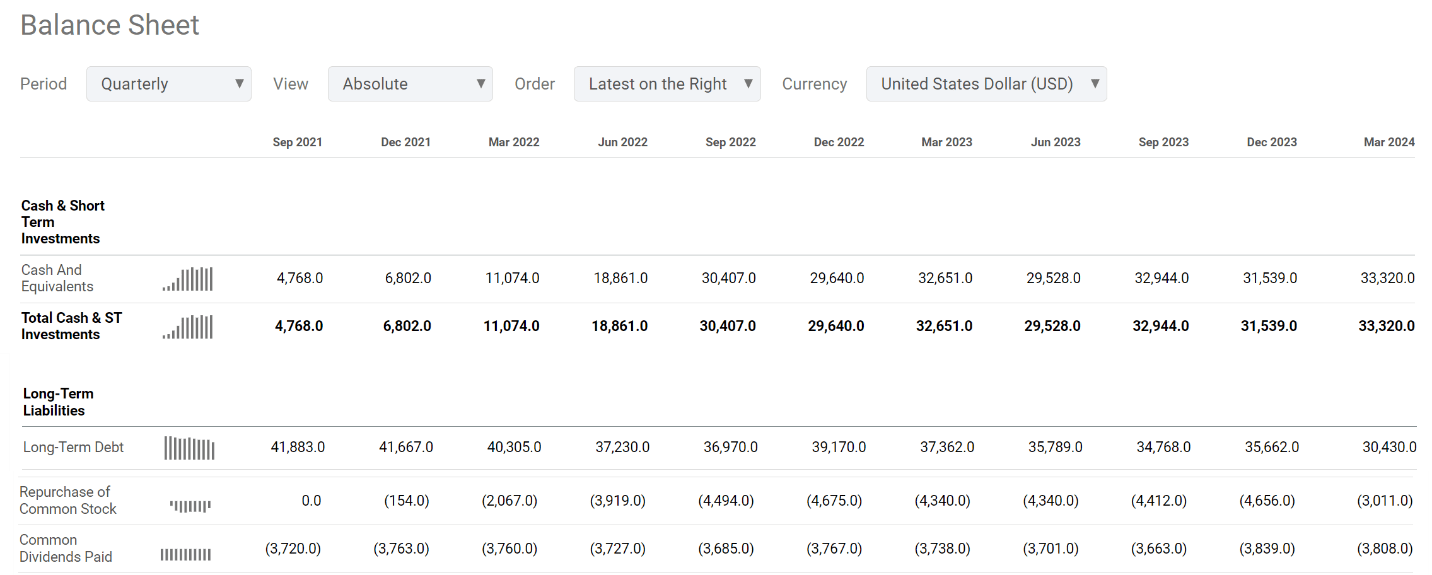

A final return driver is XOM’s holistic capital return program to shareholders. A point that XOM bulls often make is its dividend king status and the sizable payouts. I fully agree, but I also need to point out that cash dividends only provide an incomplete picture and underestimate the return potential. What really matters for investors is not (or not only) the cash dividends, but the total shareholder yield – the sum of cash dividends, share repurchases, and also debt paydowns. XOM has been generating plenty of cash to do all three in recent quarters as you can see from its balance sheet and cash flow statement below. Actually, in recent quarters, XOM has been rewarding shareholders a lot more vis share repurchases than cash dividends. To top it off, after all of these efforts (acquisitions, dividends, buybacks, and debt paydown), the company still manages to grow its cash position. As of March 2024, its cash and short-term investments have increased to $33.3 billion, compared to $32.6 billion a year ago and only $11 two years ago.

Seeking Alpha

In terms of downside risks, XOM and its peers share common risks such as fluctuations in oil prices, increased regulatory scrutiny related to environmental impact, etc. Besides these common risks, XOM faces specific risks that may not be as pronounced for its peers. With its extensive global operations, XOM faces heightened operational risks, particularly in politically unstable regions. The integration of the Pioneer Natural Resources acquisition could take some time and involve some speed bumps. Notably, the Federal Trade Commission’s closing conditions for the acquisition restrict Pioneer’s CEO from serving on Exxon’s board of directors. Such restriction adds difficulty to the integration process, in my view.

To conclude, my assessment is that the upside potential far outweighs the downside risks under current conditions. The combination of the price pullback since my last writing and the updated business fundamentals has made XOM an even stronger buy. Besides my outlook for higher oil prices (the topic of my previous article), I also see company-specific catalysts with the top ones being XOM’s margin recovery and the acquisition of the Pioneer assets.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.