Exxon Mobil Corporation is in advanced negotiations to acquire Pioneer Natural Resources Company in a potential game-changing takeover valued at $60 billion.

The deal would grant Exxon a dominant position in the oil-rich Permian Basin and reshape the U.S. oil industry.

The potential acquisition has led me to consider alternative oil stocks such as Devon Energy, Canadian Natural Resources, and Diamondback Energy.

Stadtratte

Introduction

I did not expect to write this article so soon after I wrote an article titled I Might Double My Pioneer Natural Resources Investment – Again. That article was written on August 29.

In that article, I reiterated why Pioneer Natural Resources Company (NYSE:PXD) is one of my all-time favorite oil and gas investments. Apparently, I wasn’t the only one, as Exxon Mobil Corporation (NYSE:XOM) is making a move to buy the entire Pioneer company, as reported by the Wall Street Journal.

While I don’t mind Exxon Mobil paying a premium for stocks that I own, I hate this potential deal, as I wanted to hold PXD for many decades, benefitting from its ability to reward investors with special dividends.

In this article, I’ll walk you through the potential deal and explain how I’m dealing with this situation. After all, the stock is my second-largest energy holding and my 10th-largest overall position. Losing PXD will leave a big hole, especially when it comes to my average (expected) portfolio yield.

So, let’s get to it!

Exxon To Buy Pioneer?

When talking about Exxon, I always use it as an opportunity to brag a bit about my investment in the company. In 2020, I bought Exxon in the low $30 range, which was a few cents away from its multi-decade low.

The company was the first upstream energy holding of what would become an energy-overweight portfolio.

As some readers may remember, I sold Exxon because I wanted a stock with special dividends. As much as I still like Exxon, I prefer companies that are focused on oil production, have deep reserves, efficient production, a healthy balance sheet, and (this is why I sold Exxon) plans to distribute almost every cent of free cash flow to shareholders.

Now, Exxon is buying that company from me – so it seems.

In an exclusive article that ruined my sleep, the Wall Street Journal wrote that Exxon is preparing to make a massive bid for Pioneer.

Wall Street Journal

According to the article, Exxon Mobil is in advanced negotiations to acquire Pioneer Natural Resources, which is a potential game-changing takeover valued at approximately $60 billion that could significantly reshape the U.S. oil industry. Please note that this implies roughly a premium of roughly 20%.

The deal, expected to be finalized within the coming days, would grant Exxon a dominant position in the oil-rich Permian Basin of West Texas and New Mexico, aligning with the company’s growth plans.

If completed, the acquisition of Pioneer Natural Resources, with a market capitalization of about $50 billion, would stand as Exxon’s largest deal since its merger with Mobil in 1999.

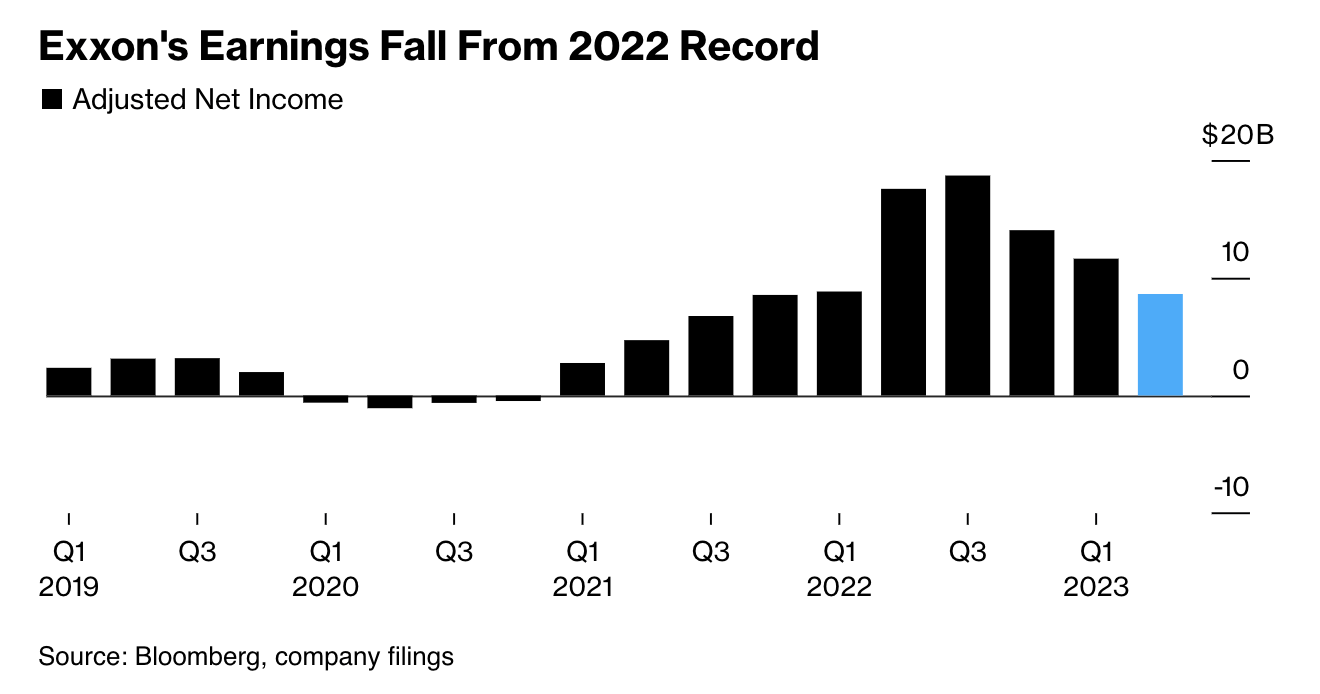

This strategic move comes after Exxon’s record-breaking profit in 2022, leaving the company financially robust and eager to delve deeper into West Texas shale.

Looking at Bloomberg data below, Exxon has been doing so well lately, thanks to elevated oil and gas prices. It also benefited from favorable refinery spreads. After all, it’s one of the world’s largest refiners as well.

Bloomberg

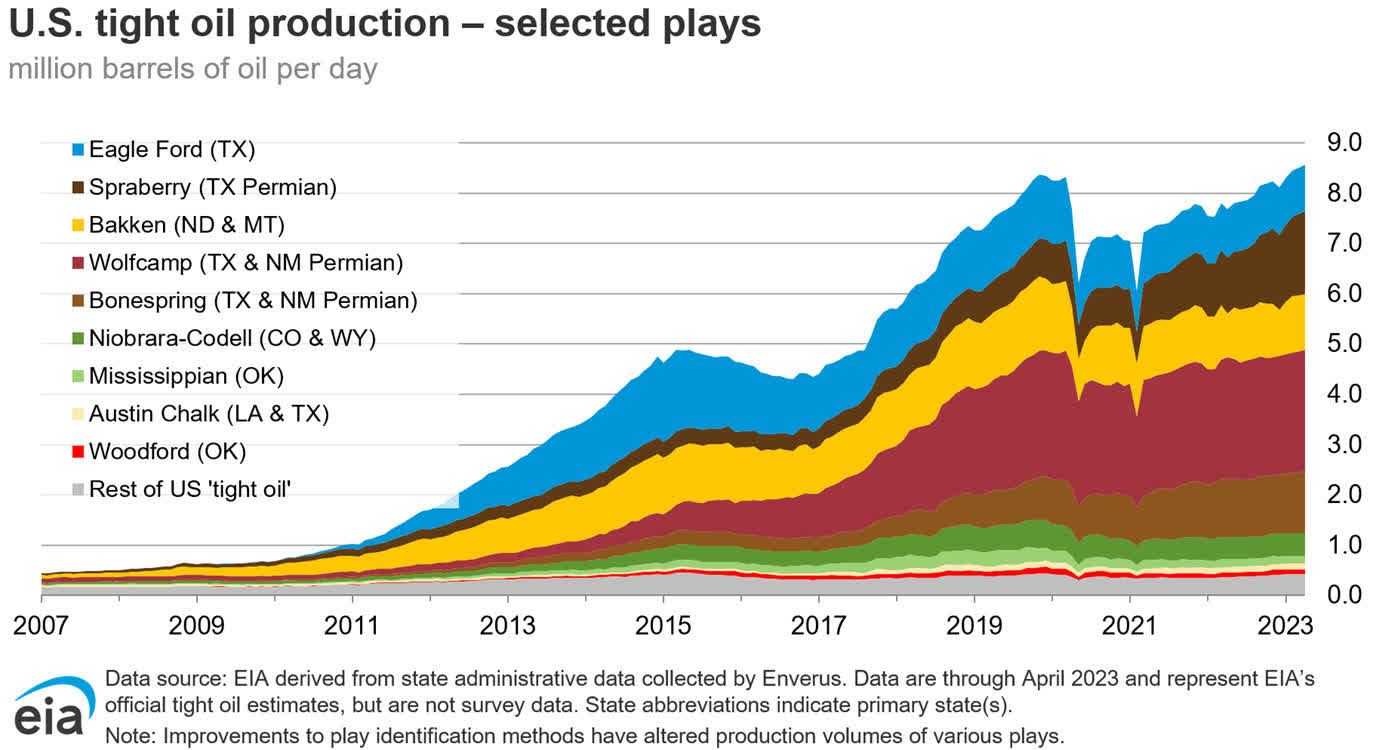

As I’ve written in many (almost countless) articles, the U.S. shale industry is going through a transition. We’re beyond peak supply growth (not peak supply), companies are slowly running out of Tier 1 reserves (the best drilling spots), and even the mighty Permian Basin is expected to see peak production (not peak production growth) in 4Q24.

Energy Information Administration

When adding that most companies make billions in excess cash in this environment, it makes sense that M&A talks are heating up.

According to the Wall Street Journal, the prospective Exxon-Pioneer deal may signal a broader trend of consolidation within the shale industry as companies face the imperative to extend their drilling capabilities and secure their future amid diminishing drilling opportunities.

Pioneer, in this case, might be one of the best takeover targets.

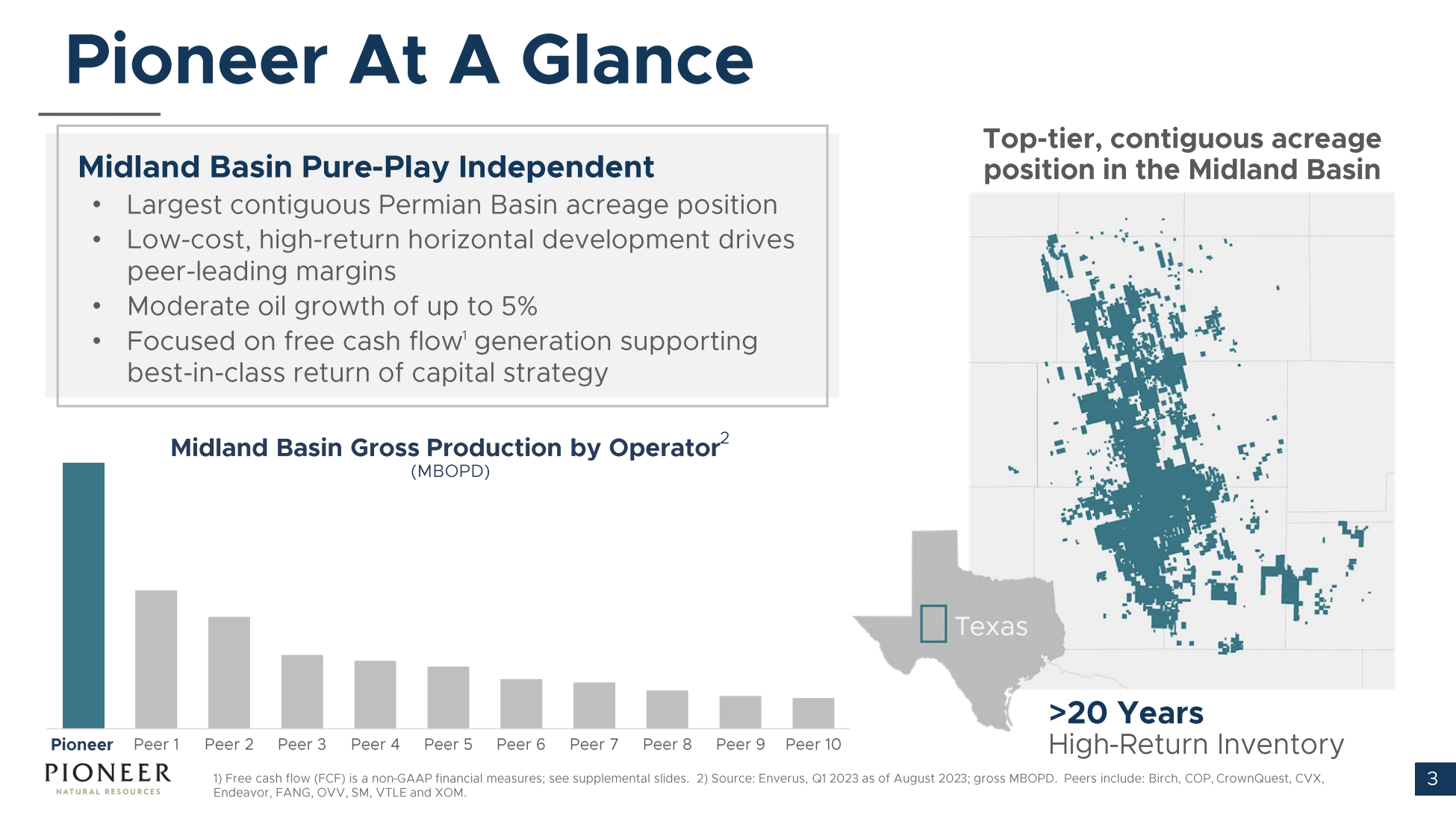

With its expansive acreage in West Texas, particularly in the highly productive Midland Basin, Pioneer stands as a key player in the U.S. shale boom. The company’s substantial untapped drilling locations and well-positioned assets make it an attractive target for Exxon in a potential acquisition that could pave the way for further industry consolidation in the Permian Basin.

Interestingly enough, just yesterday, I was interviewed by a major publication in the U.S. about exactly these benefits.

As the overview below shows, Pioneer has more than 20 years’ worth of high-return inventory in the Midland Basin. No peer even comes close to that in this high-margin basin.

Pioneer Natural Resources

Not only that, the company is also in a good position to sell its gas. In the second half of this year, 70% of its natural gas is expected to be sold out of the basin. Next year, that number could be 80%. Hence, the company gets 19% better pricing than its average peers in a pipeline-constrained region.

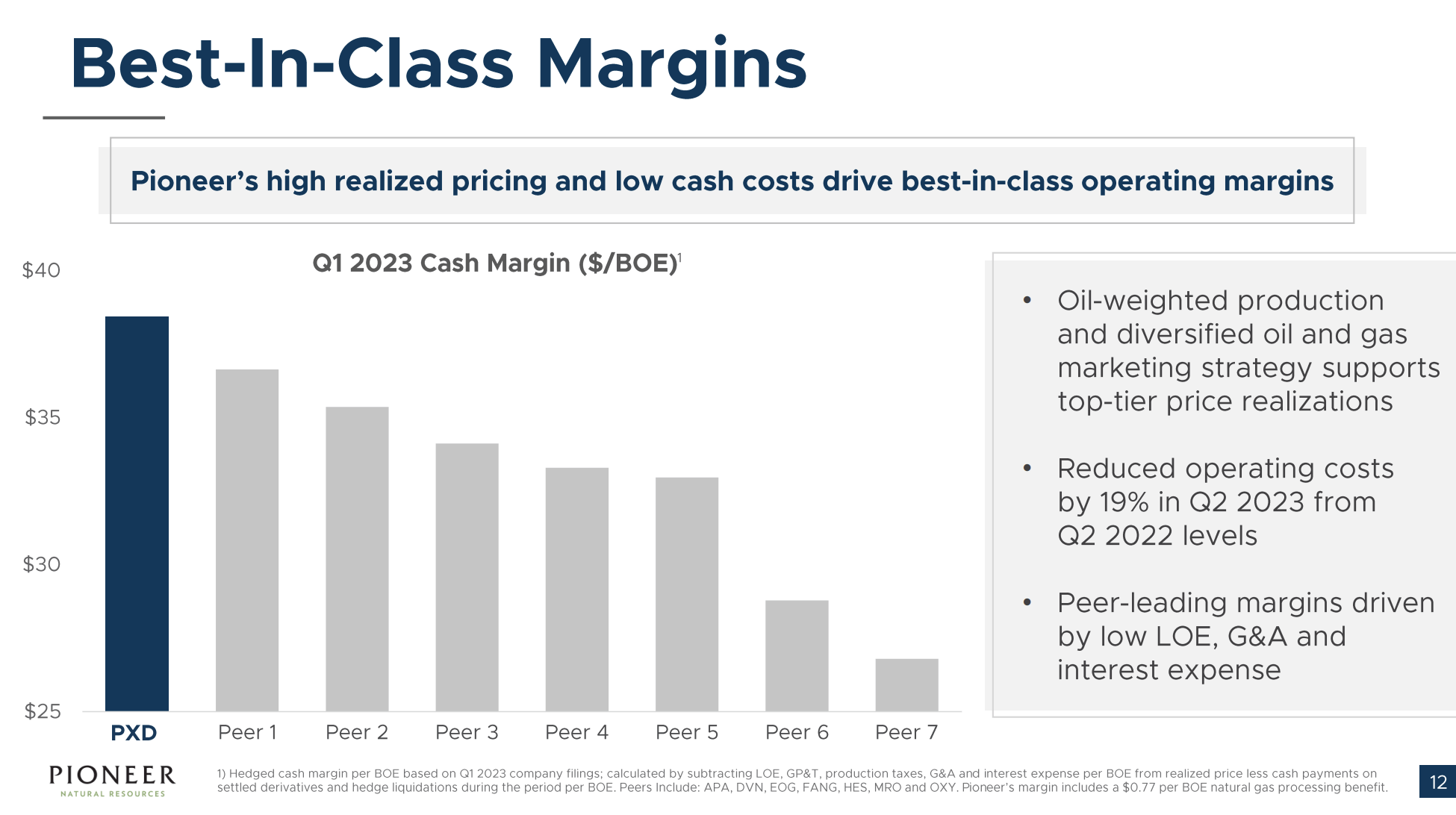

The company is also one of the most efficient drillers on the planet. In its own peer group, the company’s Q1 2023 cash margins were close to $40.

Pioneer Natural Resources

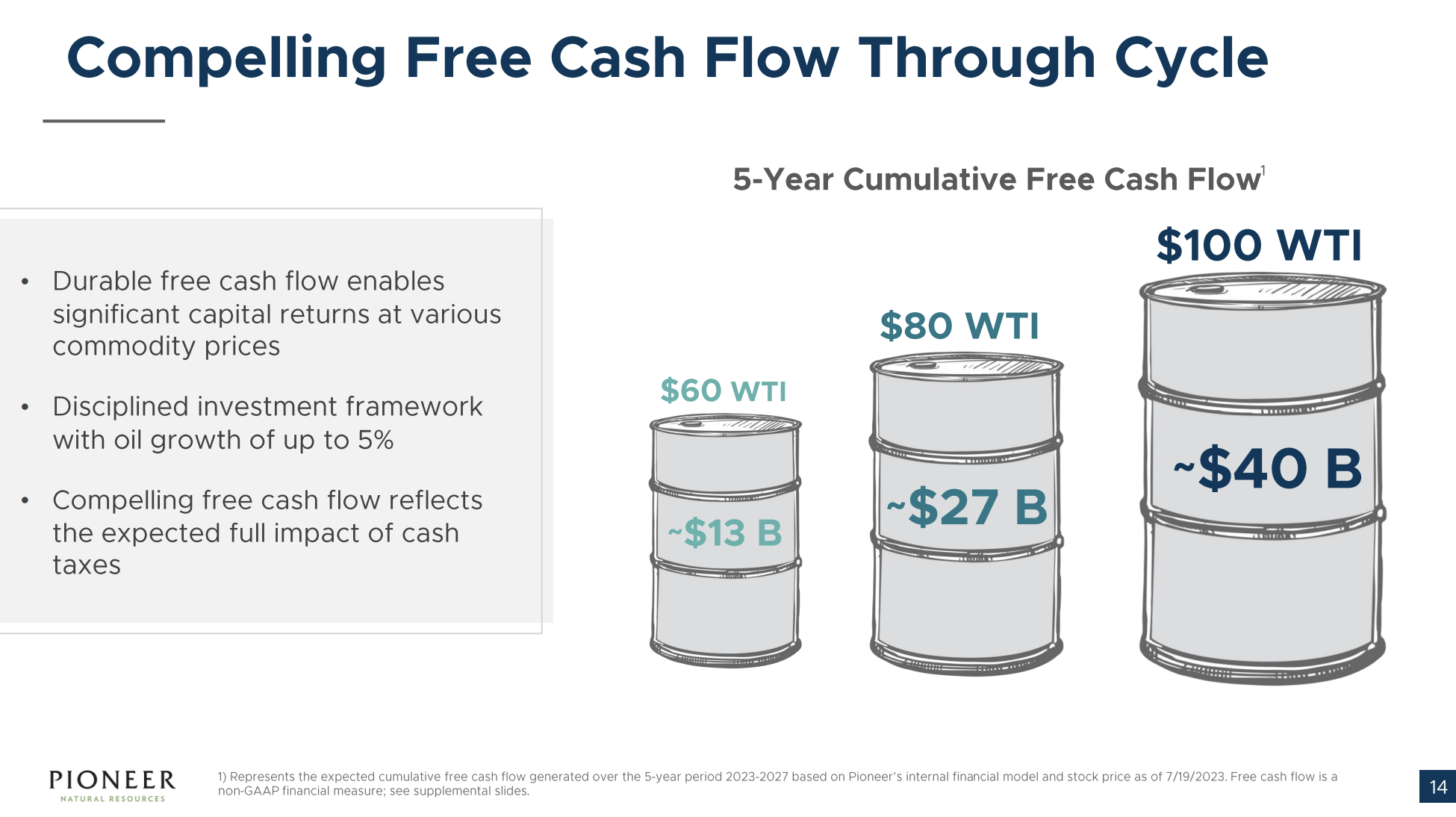

As a result, the company is a cash cow. For example, at $80 WTI, the company is able to generate $27 billion in cumulative free cash flow over five years. That’s 54% of its market cap!

On top of that, the company aims to distribute 75% of its free cash flow through its base dividend, special dividends, and buybacks (mainly dividends).

This would translate to an annual distribution yield of 11% at $80 WTI. At $100 WTI, that number would be 16%.

Pioneer Natural Resources

Given my bullish view on oil, I believe that buying Pioneer at a 20% premium is a total steal.

It also needs to be said that these talks started to surface earlier this year. I expect that we will see a confirmation of these talks in the next few days.

If Pioneer accepts, I hope it is an all-cash deal, as I’m not looking to get equity in the post-acquisition company.

Here’s what I would do.

Now What?

I just joked that the Wall Street Journal article ruined my sleep. That was partially due to the fact that many people who have my phone number had the same question: now what?

As I already said, I do not like this takeover. While a potential 20% premium is nice, I’m a long-term investor who spent months before making the decision to buy Pioneer.

Having said that, it’s a good thing that I discuss so many other opportunities on this website.

I decided that I would keep my strategy unchanged. I will keep my oil exposure unchanged. The question is what I’m buying.

Here are a few alternatives. Please note that I include links to recent articles that I wrote for in-depth research. Just click on the name of each company.

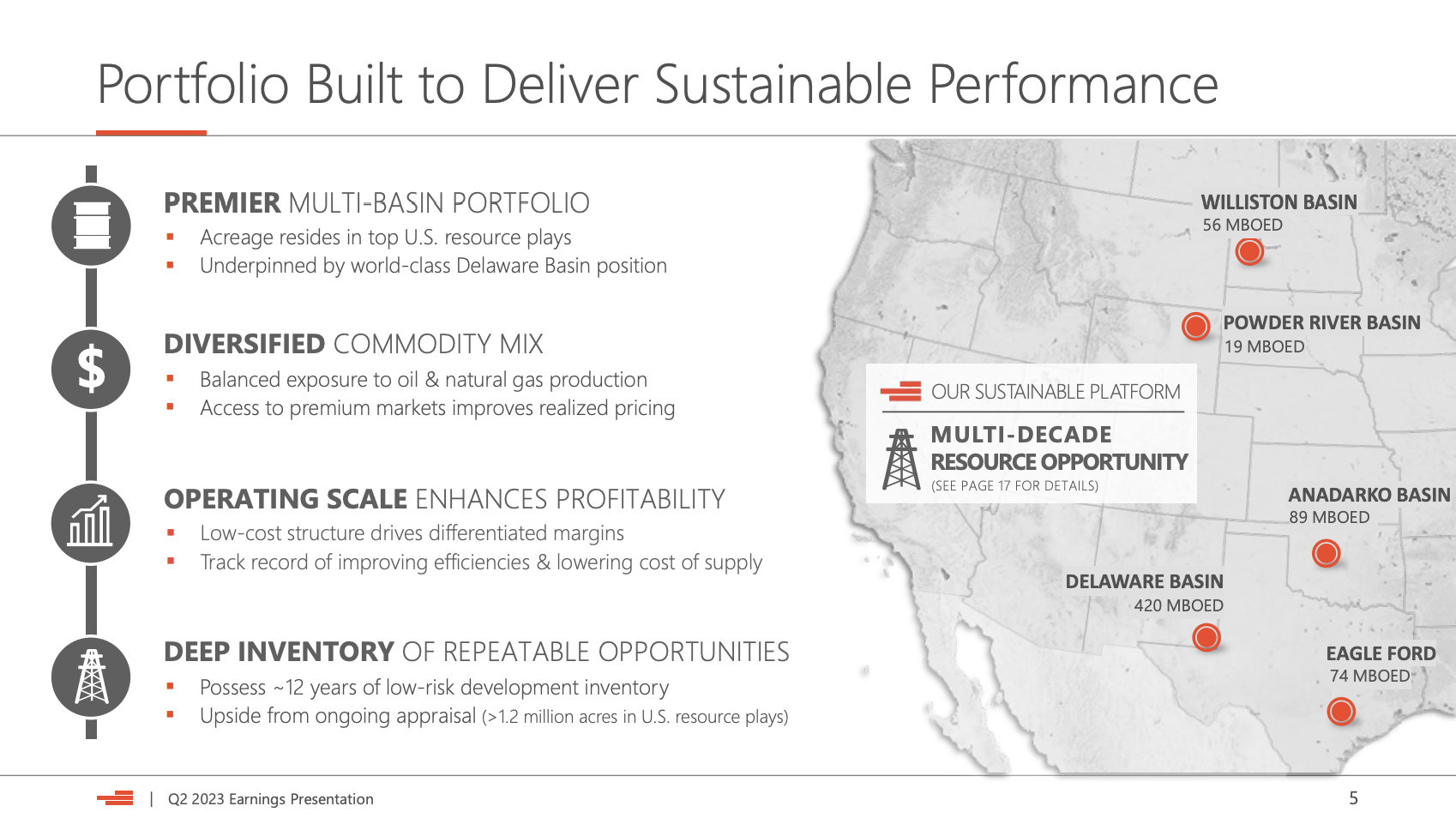

Devon also has premier assets in the Permian Basin (Delaware Basin), where it produces more than 420 thousand barrels of oil equivalent per day.

The company’s 5% expected production growth this year is breakeven at $40 WTI, which shows how efficient this company is.

Devon Energy

On top of that, the company has more than 20 years of unrisked inventory, a BBB+ balance sheet, and a clear plan to distribute up to 40% of post-base-dividend free cash flow to shareholders through a variable dividend.

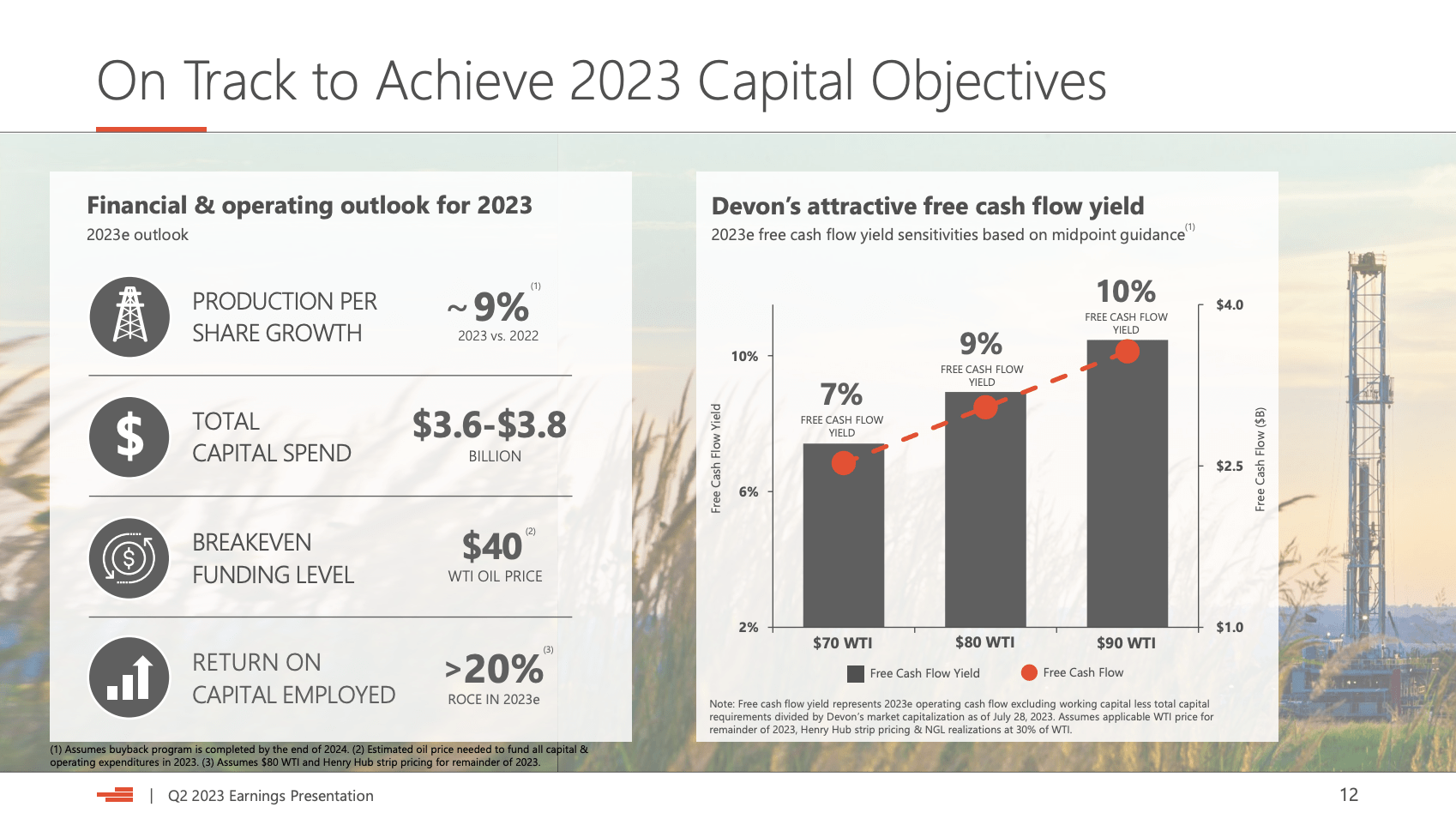

At $80 WTI, the company has a free cash flow yield of close to 11%. Please note that I adjusted the data in the chart below for its lower stock price.

Devon Energy

At elevated oil prices, double-digit dividends are almost a guarantee.

Devon Energy

I also believe that Devon is a potential takeover target. I would not be surprised if an oil major were to make a move over the next 12 months.

However, I hope they don’t, as I believe that DVN would make a great major holding in my dividend portfolio.

With PXD (almost) out of the picture, CNQ is now my single favorite oil stock. As much as I like DVN and the other stock I’ll show you in this article, CNQ lets my heart beat faster.

The only problem is that it’s already my largest position in energy.

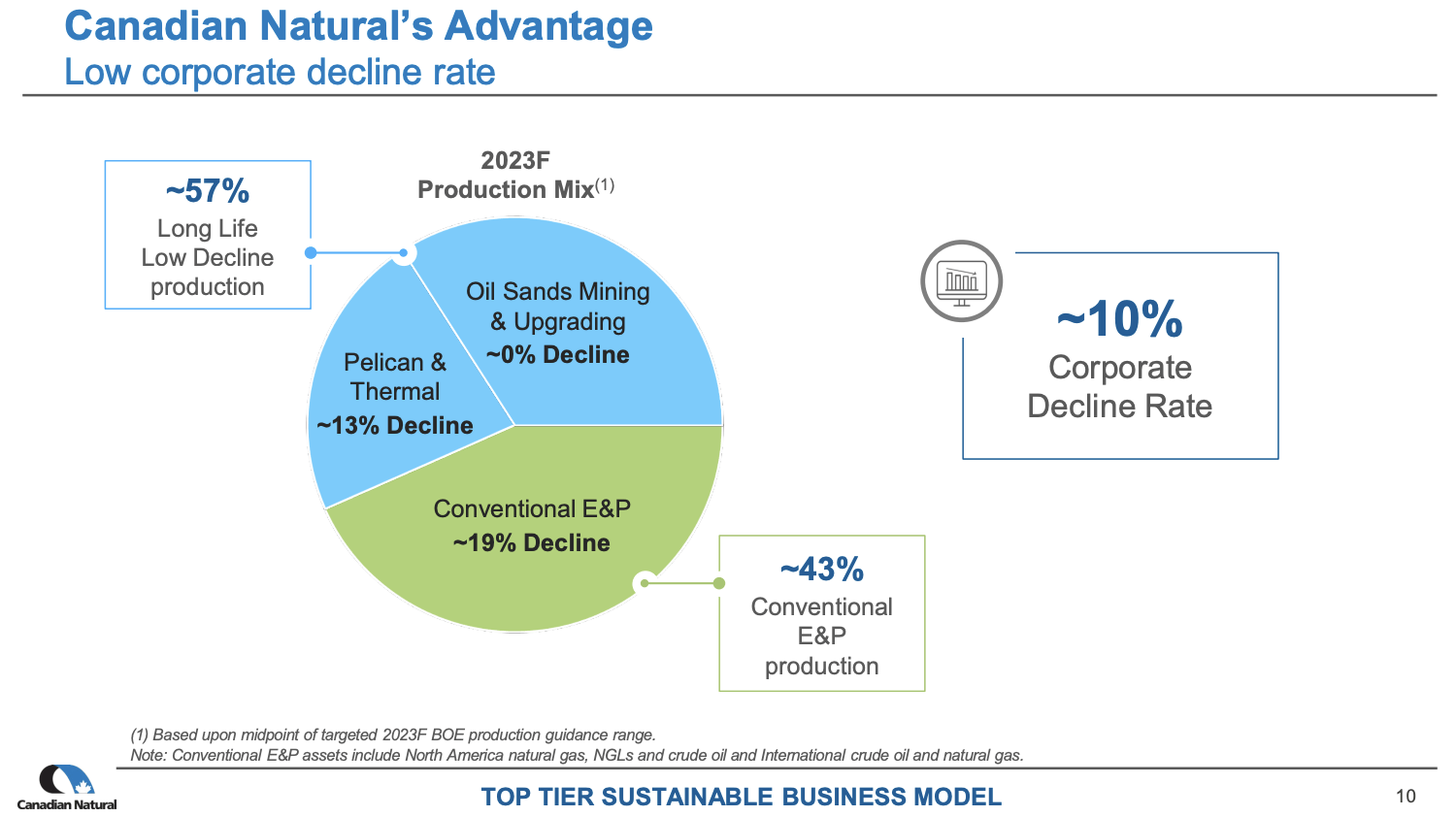

Canadian Natural is a company engaged in the production of oil sands, natural gas, and conventional oil production. It has more than 30 years’ worth of total reserves. Its oil sands operations have a reserve life of at least 40 years.

Furthermore, oil sands aren’t just efficient, but they also come with no decline rates and other risks that shale producers have. 57% of the company’s production are long-life, low-decline assets.

Canadian Natural Resources

Even better, its oil sands operations are breakeven between $20 and $30 WTI!

The entire company is breakeven close to $40.

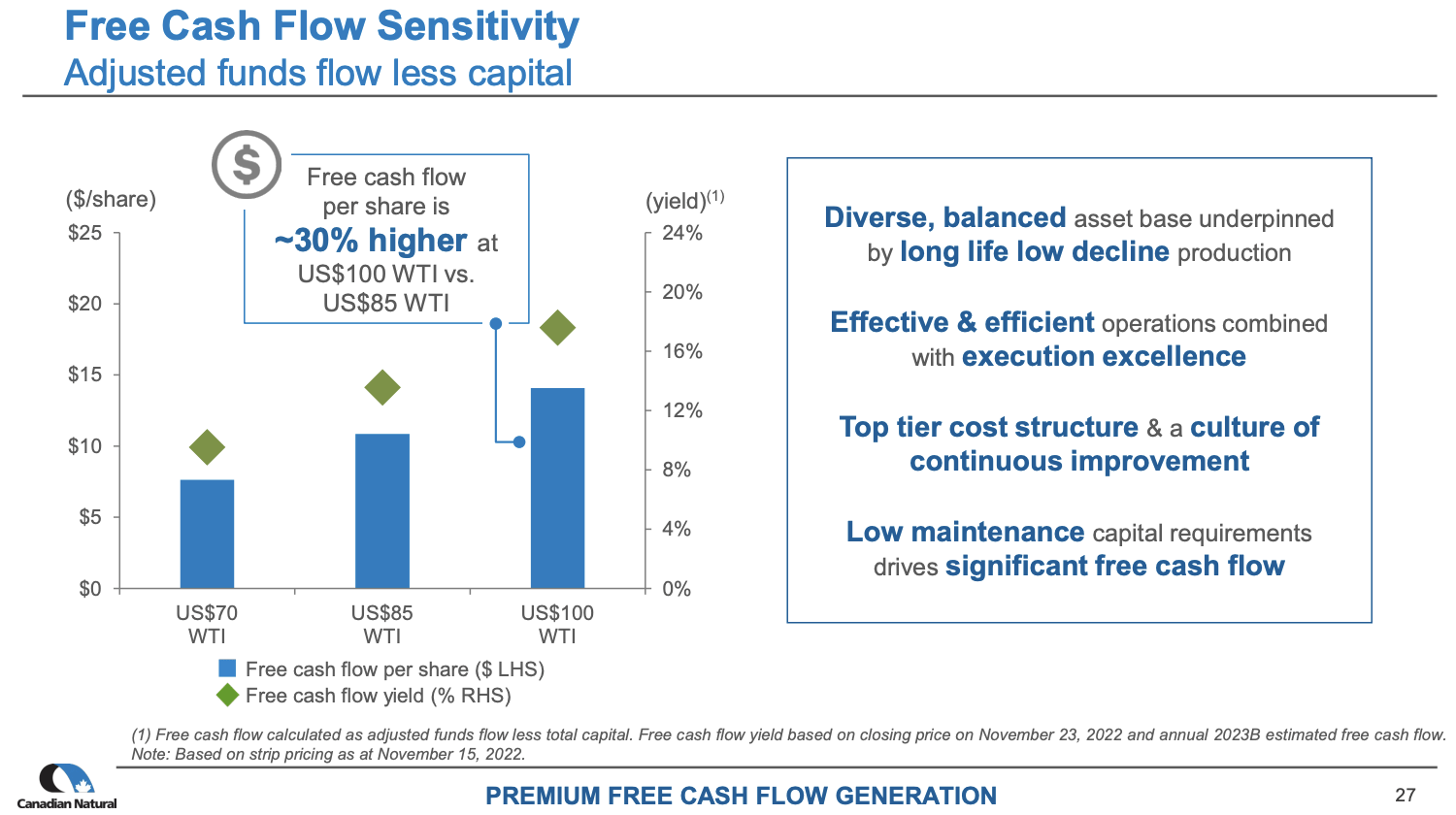

Next year, the company is expected to lower net debt below CAD 10 billion. That paves the way for a 100% free cash flow payout.

This is what I wrote in the article I referred to above:

Looking at the data below, we see that the company is capable of generating a free cash flow yield of roughly 18% at $100 WTI. Even at $70 WTI, the company is capable of generating a free cash flow yield of more than 10%.

Canadian Natural Resources

The only drawdown (for some) is that this company is based in Canada.

Having said that, I believe that CNQ is a must-own. I’m likely to deploy some proceeds of PXD into this company, making it an even more dominant holding of my portfolio.

FANG is an independent oil and natural gas company focused on unconventional, onshore reserves in the Permian Basin, with substantial acreage and proven reserves.

The company has at least 12 years’ worth of production reserves and a history of consistently adding to its inventory. Since 2013, its reserves have grown by 47%, including M&A. It also owns Viper Energy Partners (VNOM), which owns drilling acres in the Permian.

Diamondback Energy

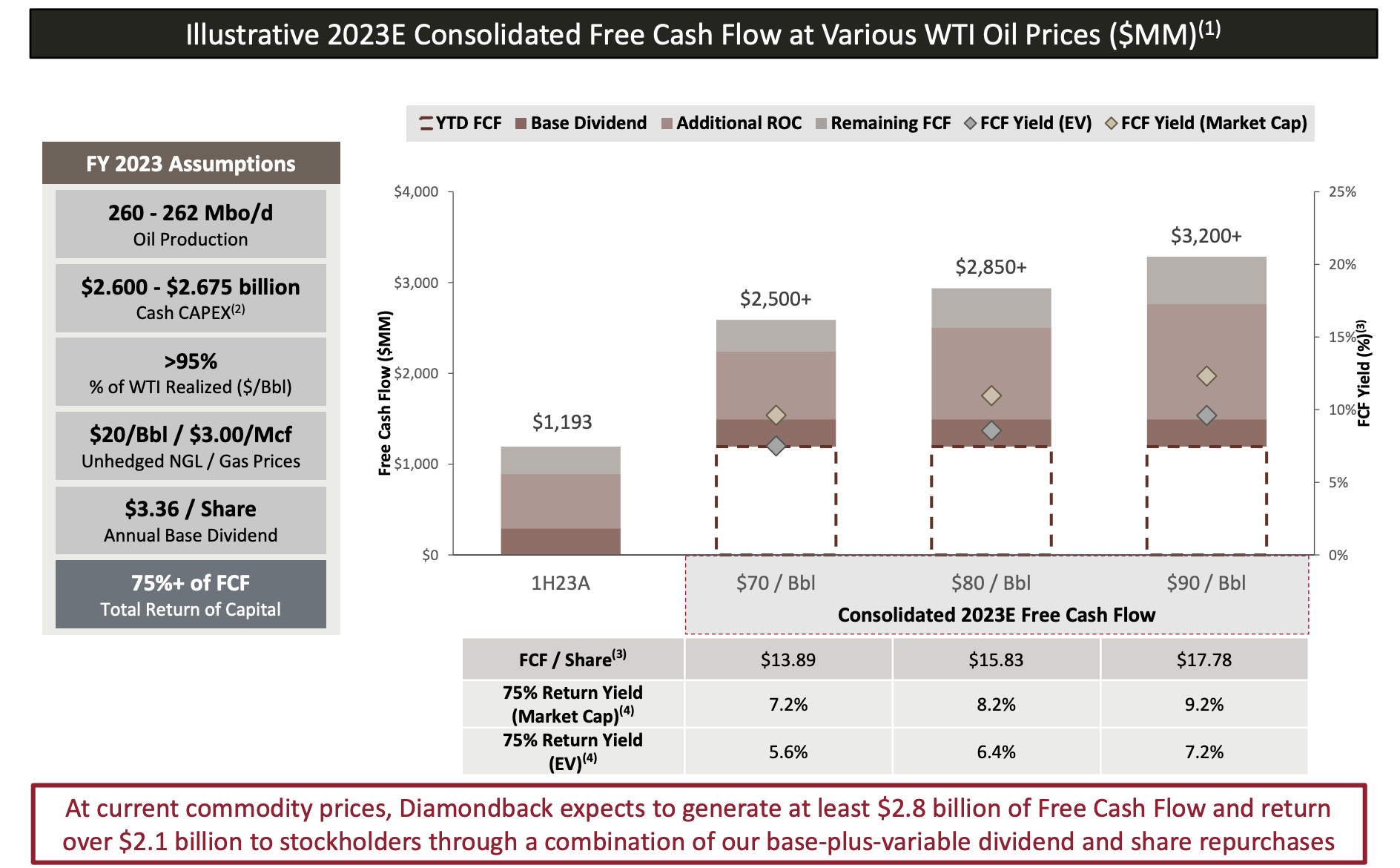

The company has efficient operations, enabling it to protect dividends even at low oil prices and strong pricing power. In 2Q23, oil price realization was at 97% of WTI.

Its production is so efficient that it can cover its base dividend at $40 WTI!

It is free cash flow positive in the high-$30 range, making it one of the most efficient producers in the U.S. – next to DVN and PXD.

With a strong balance sheet, low debt levels, and efficient capital allocation, FANG prioritizes shareholder distributions through dividends, buybacks, and special dividends, aiming to distribute at least 75% of its free cash flow.

Diamondback Energy

This is what I wrote in my October 1 article:

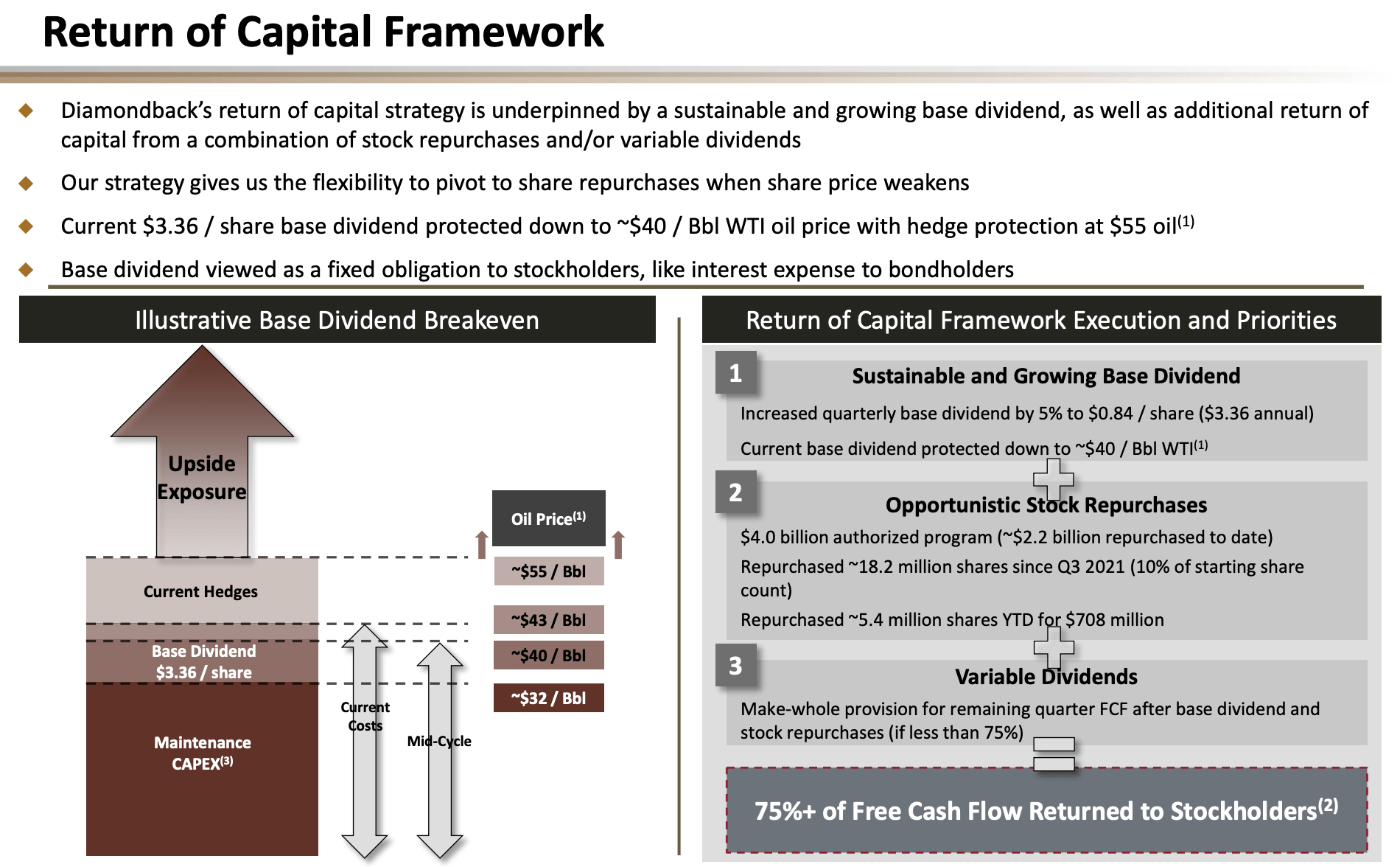

Thanks to low debt levels, debt reduction is NOT a capital priority of the company.

It has other priorities (as seen in the overview below, which also shows its hedges and breakeven point):

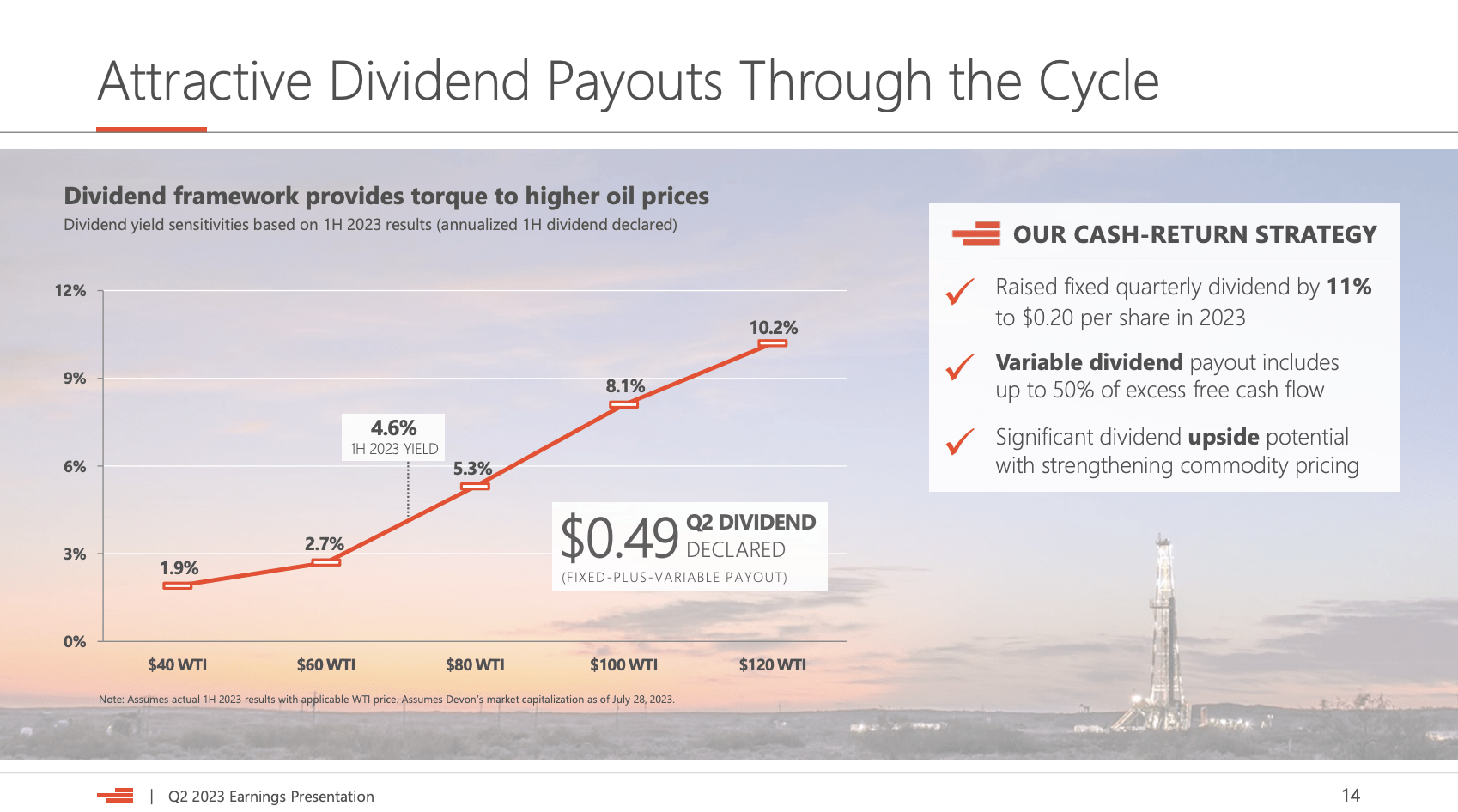

1. Protecting and growing its base dividend. After hiking its dividend by 5% on August 1, it now pays a base dividend of $0.84 per share per quarter, which translates to a yield of 2.2%.

2. Opportunistic share buybacks. Since the second half of 2021, the company has bought back $2.2 billion in stock, which translates to 8% of the current $28 billion market cap.

3. Variable/special dividends. The company aims to distribute 75% of its free cash flow. This means that at elevated oil prices, it will use special dividends to reward investors.

At $90 WTI, investors can expect a total distribution yield of roughly 9%. Even at $70 WTI, that number is still 6.7%.

Diamondback Energy

FANG reminds me a lot of DVN. I believe that FANG could also be a takeover target, although I’m not betting on potential M&A. I’m a long-term investor looking for great companies that (hopefully) add value to my portfolio for decades to come.

Having said all of this, the companies mentioned in this article are NOT the only high-quality companies on the market. There are many others that make sense to buy.

However, the stocks in this article are the first ones on my list.

I believe that all of these companies have the capabilities to come with long-term capital gains and very high shareholder distributions (mainly consisting of dividends).

Over the next few days, I will figure out which of these companies I’m buying.

Regarding the PXD takeover, I believe that the rumors are for real. I expect a formal offer over the next two weeks.

Also, please always be aware that oil stocks are volatile. Do your own due diligence and assess how much energy is right for your strategy.

Takeaway

In this article, I delved into the unexpected news of a potential acquisition of Pioneer Natural Resources by Exxon Mobil, a move that (somewhat) took me by surprise after declaring PXD as a long-term favorite.

The deal, valuing Pioneer at approximately $60 billion, could reshape the U.S. oil industry and trigger a new wave of takeovers.

Despite the premium, I’m not happy about losing a key holding I intended to keep for decades, benefiting from its special dividends.

Exploring my options, I have alternatives like Devon Energy, Canadian Natural Resources, and Diamondback Energy, each with unique merits and potential for high dividends.

Ultimately, my strategy remains intact, aiming for long-term capital gains and robust shareholder distributions.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of PXD, CNQ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Join iREIT on Alpha today to get the most in-depth research that includes REITs, mREITs, Preferreds, BDCs, MLPs, ETFs, and other income alternatives. 438 testimonials and most are 5 stars. Nothing to lose with our FREE 2-week trial.