Summary:

- In spite of recent performance, Exxon Mobil has been one of the best-performing stocks in the energy sector over the past few years.

- There are certain short-term risks that would likely continue to weigh on performance in the coming months.

- In the long run, Exxon is still among the best-positioned companies in the sector, but delivering similar returns to the 2021-22 period is unlikely.

chitsanupong kathip

The past 3-year period has been one of the best on record for the Energy sector and high quality names, such as Exxon Mobil (NYSE:XOM) in particular.

Buying XOM when the stock was trading in the 30s was a tough decision to make for both retail and institutional investors alike and yet the signs that the stock was significantly undervalued were easy to see.

Since then, XOM stock delivered more than a 250% total return, thus outperforming the Energy Select Sector SPDR® ETF (XLE) and more importantly the S&P 500 by a very wide margin.

As future performance was beginning to get priced-in in late 2022, I turned more cautious just as investors’ optimism was reaching new highs. And as it almost always happens, once sentiment shifts at such a rapid pace the stock disappoints.

Seeking Alpha

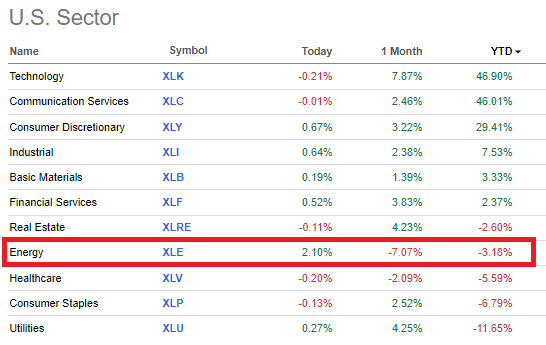

But it wasn’t just XOM that underperformed the market in during this time period. The whole energy sector has been under pressure for most of 2023, after delivering outstanding returns in two years prior.

Seeking Alpha

Regardless of all that, however, this dynamic could be very confusing for investors with many remaining extremely bullish and hyped about future prospects of XOM, while others are seeing the stock as a sell.

In my view, neither of these views are sensible and although I don’t see XOM as an attractive buy opportunity yet, the stock cannot be a sell at this point in time.

Fairly Priced

Investing in cyclical industries could be relatively easy for those with long-term investment horizons, who are also willing to go against the mainstream narrative and pick the highest quality businesses within the given sector.

That is why, buying Exxon Mobil at the cyclical lows for the Oil & Gas industry was not as risky as it might have seemed back then.

(…) the cyclical downturn in oil & gas prices presents an opportunity for long-term-oriented investors as XOM’s valuation fell to levels last seen in 2003. At the same time, XOM is one of the most financially-sound entities in the sector, has continued to invest heavily through the bottom of the cycle and has the scale necessary to bring new technologies to life.

Source: Seeking Alpha

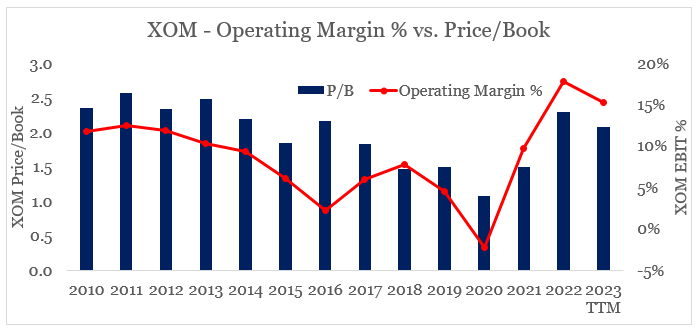

Margins were in negative territory back then and the stock was trading near book value which made it a bargain even if it wasn’t for the strong recovery in oil prices that we saw in recent years.

As we see on the graph below, however, Exxon’s margins are near record high levels right now and the Price/Book multiple has followed suit.

prepared by the author, using data from Seeking Alpha

Having said that, Exxon’s current P/B multiple of 2.1 is in-line with its historical average (2010 to 2022) of 2.0. Given the record high margins at the moment, this is telling us that the market is already pricing in a decline in profitability going forward.

To an extent, this creates a margin of safety for investors but it’s not all about how high margins are. When investing in cyclical industries, margin variance over the years is also a crucial area for long-term investors.

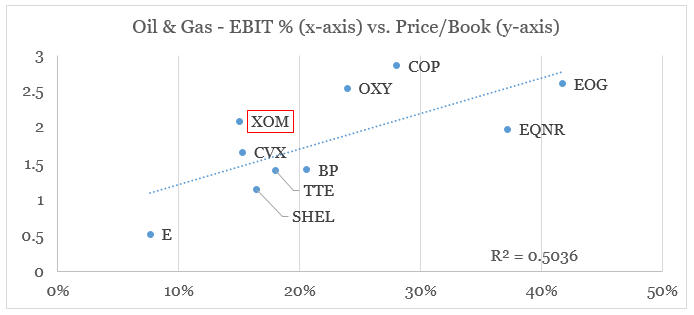

That is one of the reasons why XOM trades at higher multiples when compared to other integrated Oil & Gas majors, such as Shell (SHEL) and TotalEnergies (TTE).

prepared by the author, using data from Seeking Alpha

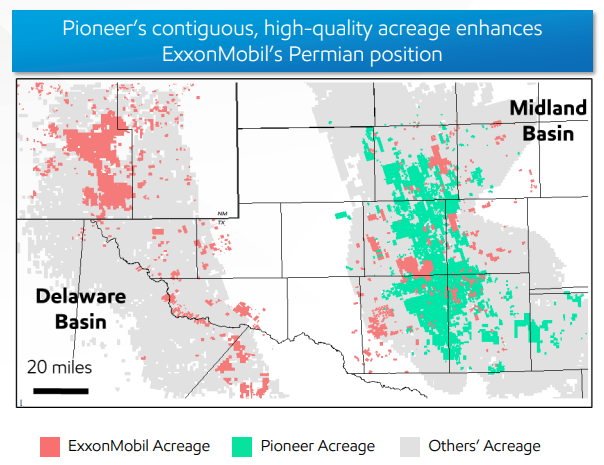

It is Exxon’s strong competitive advantages in the upstream segment, where it is now consolidating its properties in the highly attractive Permian Basin (see below) while continuing to invest in high return projects in Guyana.

Exxon Mobil Investor Presentation

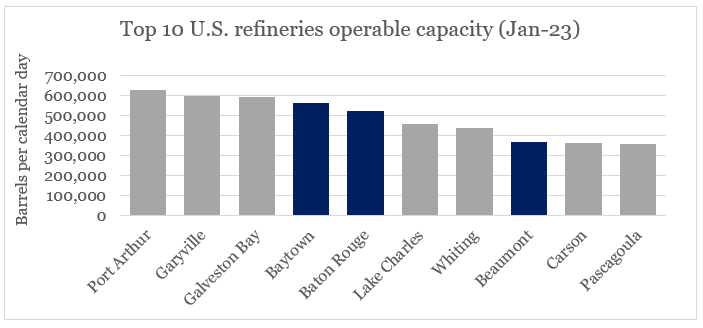

In Downstream, Exxon also has a significant competitive advantage stemming from its scale, with the company operating 3 out of the 10 largest U.S. refineries.

prepared by the author, using data from eia.gov

This justifies the company trading at a premium to its peers within the Oil & Gas sector, once we control for current profitability.

Short-Term Risks

Even though, Exxon is fairly priced at the moment and the Energy sector remains highly attractive in the long run, there are certain short-term risks that are likely to continue to weigh on XOM returns.

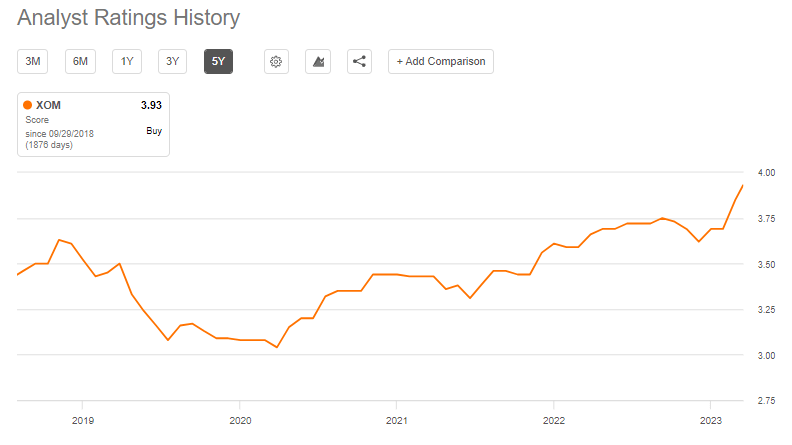

One headwind is the extreme optimism within the sell-side analyst community. Consensus ratings have reached their highest levels over for the past 5-year period and with that sell ratings are non-existent at the moment.

Seeking Alpha

This creates a heavily one-sided market for Exxon’s shares and could exacerbate a potential downturn within the sector and equities more broadly.

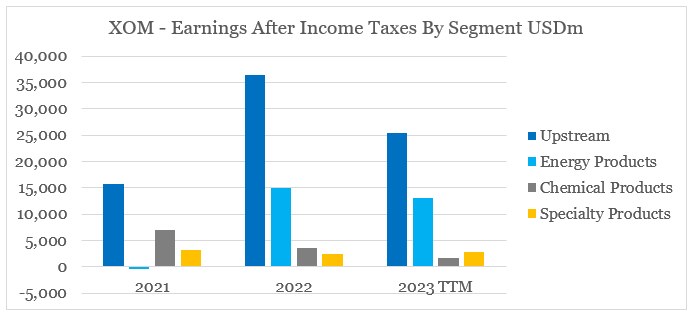

The company is also now entering a heavy investment cycle which will be marked with higher capital expenditures, acquisition costs and other expenses. Record high upstream profits are also coming-off from their cyclical peaks (see the graph below) and the company would need to continue to ramp-up investments in low carbon solutions.

prepared by the author, using data from SEC Filings

All that would continue to weigh on free cash flow in the coming year and as a result will cool-off short-term investor sentiment.

Why Exxon Is Not A Sell

While I would not rush in to buy Exxon at current levels, I cannot justify a sell rating either. As we saw above, XOM remains as one of the best choices within the large cap energy space on the back of its strong competitive positioning.

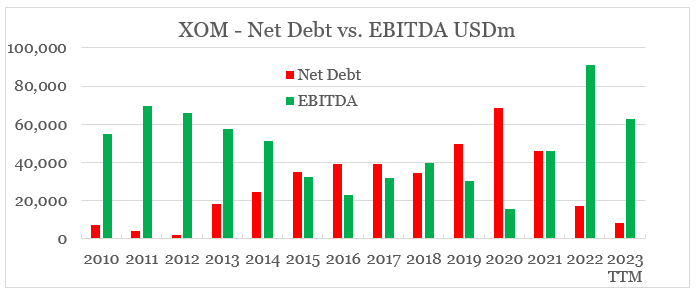

On top of that, Exxon’s management has significantly reduced certain idiosyncratic risks related to the company’s debt load and its dividend pay-outs.

By paying out debt more aggressively in recent years and preserving cash, Exxon’s management has managed to reduce the level of net debt to one of its lowest levels in more than 10 years. At the same time, profits would be more than enough to cover interest payments at a time of rising interest rates.

prepared by the author, using data from Seeking Alpha

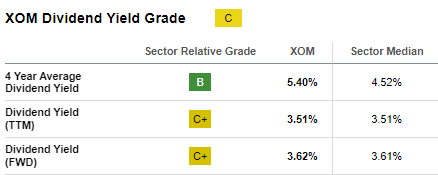

The dividend yield, on the other hand, is not as attractive as it used to be when I first recommended XOM. With a forward dividend yield of 3.6%, there are far more attractive opportunities out there for yield-seeking investors.

Seeking Alpha

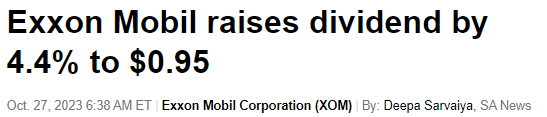

Nonetheless, XOM is now in a good position to consistently grow its dividend beyond the short-term which once again bodes well for long-term investors, who are willing ignore short-term risks.

Seeking Alpha

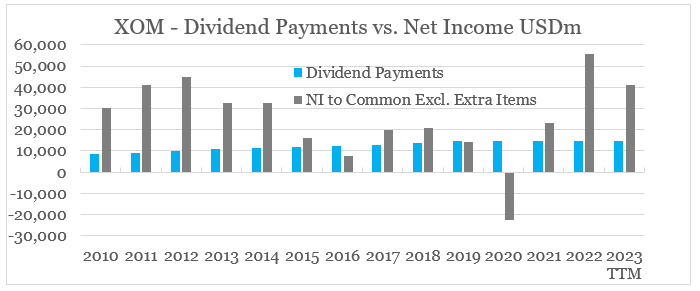

The reason being that contrary to the 2015-2020 period, Exxon’s dividend payout ratio is now at healthy levels.

prepared by the author, using data from Seeking Alpha

Having said that, I expect management to remain prudent when it comes to dividend increases within the current environment. Not only are we now faced with a significant risk of a recession, but at the same time Exxon’s management will have a hard task of integrating Pioneer Natural Resources (PXD) while spending more on capital expenditures in a highly uncertain macroeconomic and geopolitical climate.

Conclusion

Whether or not Exxon Mobil is buy, hold or a sell, largely depends on one’s investment horizon. For anyone looking to hold the stock for a short-period of time, the task at hand is very difficult and largely depends on factors outside of management’s control.

For those having a longer investment horizons, however, Exxon could still be an attractive addition to an equity portfolio. At the moment, however, the stock is fairly priced, offers a less attractive dividend yield and is faced with certain risks that should not be ignored.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CVX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Please do your own due diligence and consult with your financial advisor, if you have one, before making any investment decisions. The author is not acting in an investment adviser capacity. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC filings. Any opinions or estimates constitute the author's best judgment as of the date of publication, and are subject to change without notice.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

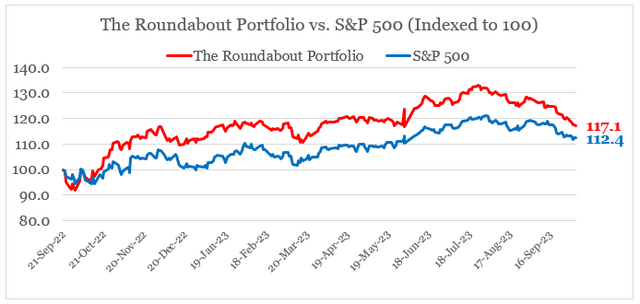

Looking for better positioned high quality businesses in the energy space?

You can gain access to my highest conviction ideas in the sector by subscribing to The Roundabout Investor, where I uncover conservatively priced businesses with superior competitive positioning and high dividend yields.

Performance of all high conviction ideas is measured by The Roundabout Portfolio, which has consistently outperformed the market since its initiation.

As part of the service I also offer in-depth market analysis, through the lens of factor investing and a watchlist of higher risk-reward investment opportunities. To learn more and gain access to the service, follow the link provided.