Summary:

- Guyana has approved the Exxon Mobil Corporation partnership’s proposed 35 well 2 ship drilling campaign over 5 years.

- But this campaign implies more expenditures “down the road” for FPSO’s and associated expenses.

- Management can already plan on about $100 billion in expenditures just with the discoveries already made.

- There will likely be a speedup over time of Guyana progress.

- Point Thompson provides speculative upside at this point.

Jeremy Poland

There has long been an argument that Exxon Mobil Corporation (NYSE:XOM) is large enough that “a billion here and a billion there” is not significant. So many just did not realize the significance of the latest approval by Guyana of a 35-well campaign over roughly 5 years. After all, what is a billion-dollar two ship drilling campaign spread over years for a company the size of Exxon Mobil. But it turns out every commercial discovery made will add roughly $9 billion or more to that “small” commitment. When one considers that the exploration discovery rate currently exceeds 50%, that initial commitment is looking very significant.

Now admittedly, one cannot tell whether each discovery that is commercial will need an FPSO or whether they will need to combine a few discoveries to justify an FPSO.

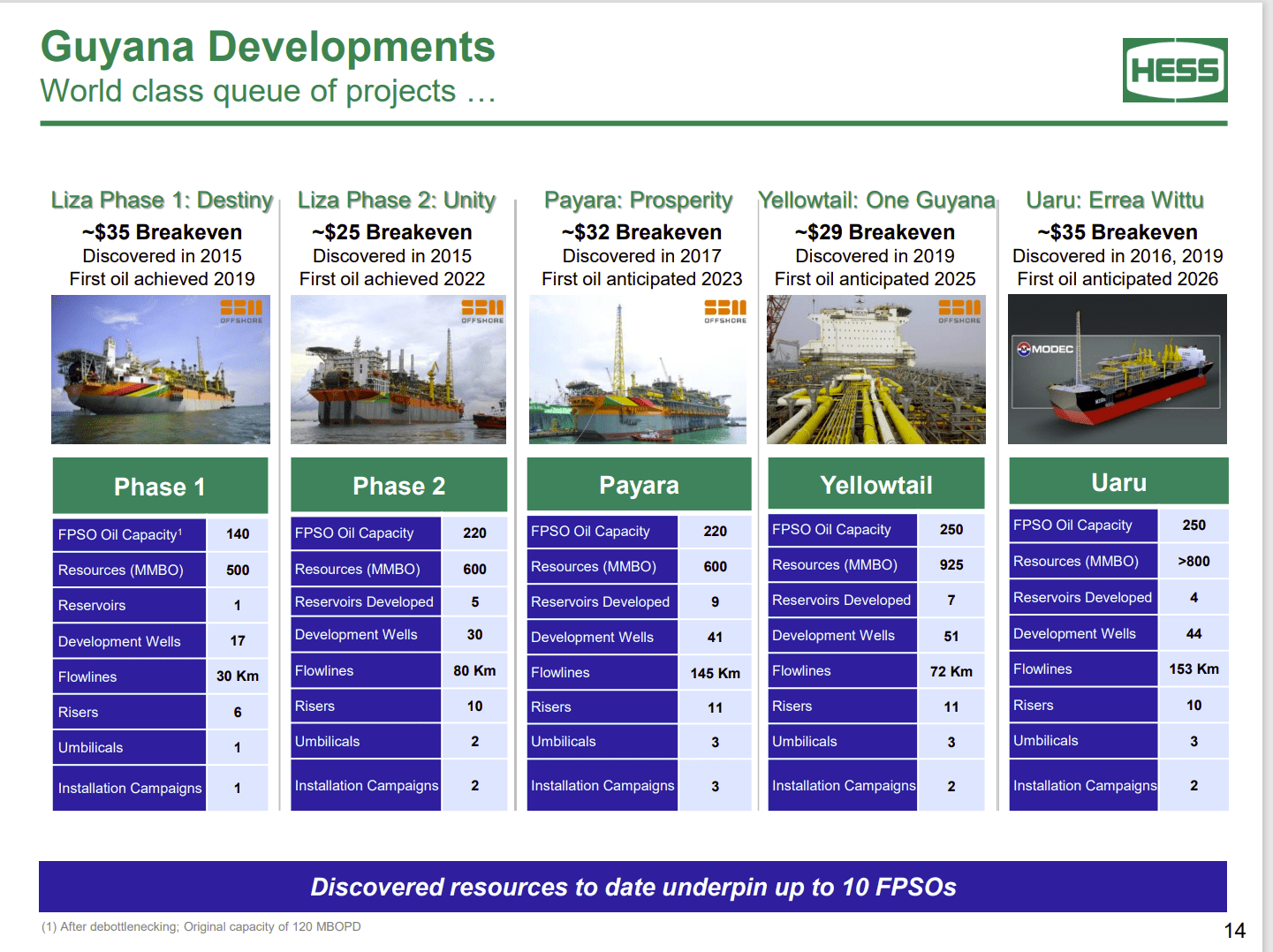

Hess Presentation Of Current FPSO Status Of Guyana Partnership (Hess Presentation At J.P. Morgan Energy, Power & Renewables Conference June 2023)

Management already has probably a “line of sight” to spend at least $100 billion of partnership money as shown above. The fact that they are going for still more expenditures demonstrates the optimism of the future production of what is quickly turning into the largest basin find in modern times.

While it can be argued that current progress is too slow to be meaningful to a company like Exxon Mobil, I would argue that anyone putting the kind of money down now and lining up the commitment shown above, is going to sooner, rather than later, have a material addition to current production.

Management already has four FPSOs approved as shown above and the partnership has a reasonable way to get to 6 more FPSOs. Clearly, if the company has plans for the partnership to continue to explore, then the likelihood of still more FPSOs in the “certain” future is going to be climbing.

Investors need to remember that the partnership retains something like 5 million acres after the “giveback” to Guyana. Even though it has been delayed one year, it will still happen. This is still a whole lot more acreage than many basins make available for bids at any given time. What you are likely seeing is the operator trying to convert as many acres as possible to producing and therefore not subject to future givebacks. But that is a pretty standard race against time that I have reported on many times over the years.

The other thing to consider here is that Exxon Mobil is getting a lot of attention for just one of the blocks held in Guyana and really no attention at all for any holdings in Suriname. Yet all of this provides still more upside potential if a commercial discovery is determined to justify producing.

One of the things that Hess Corporation (EHS) management has mentioned several times is how Exxon Mobil manages an FPSO through the approval process while another FPSO is in the development or building phase, and still another one in the hookup and initial production phase. With all the holdings in the area, that scenario could eventually multiply several times over depending upon which partnership and lease holdings have commercial discoveries.

Point Thompson

Point Thompson is one of the company’s investments that is producing liquids up in Alaska. This project is also one of the largest natural gas fields in North America. There has been talk about finding ways to export this gas to markets to take advantage of what is anticipated to be a strong natural gas market. However, so far anything solid has not yet really emerged. Still, with liquids production already in place, it would be probably economically attractive to at some point produce the gas for use elsewhere. This would likely be a long-term speculative upside potential project at this time.

Production Growth

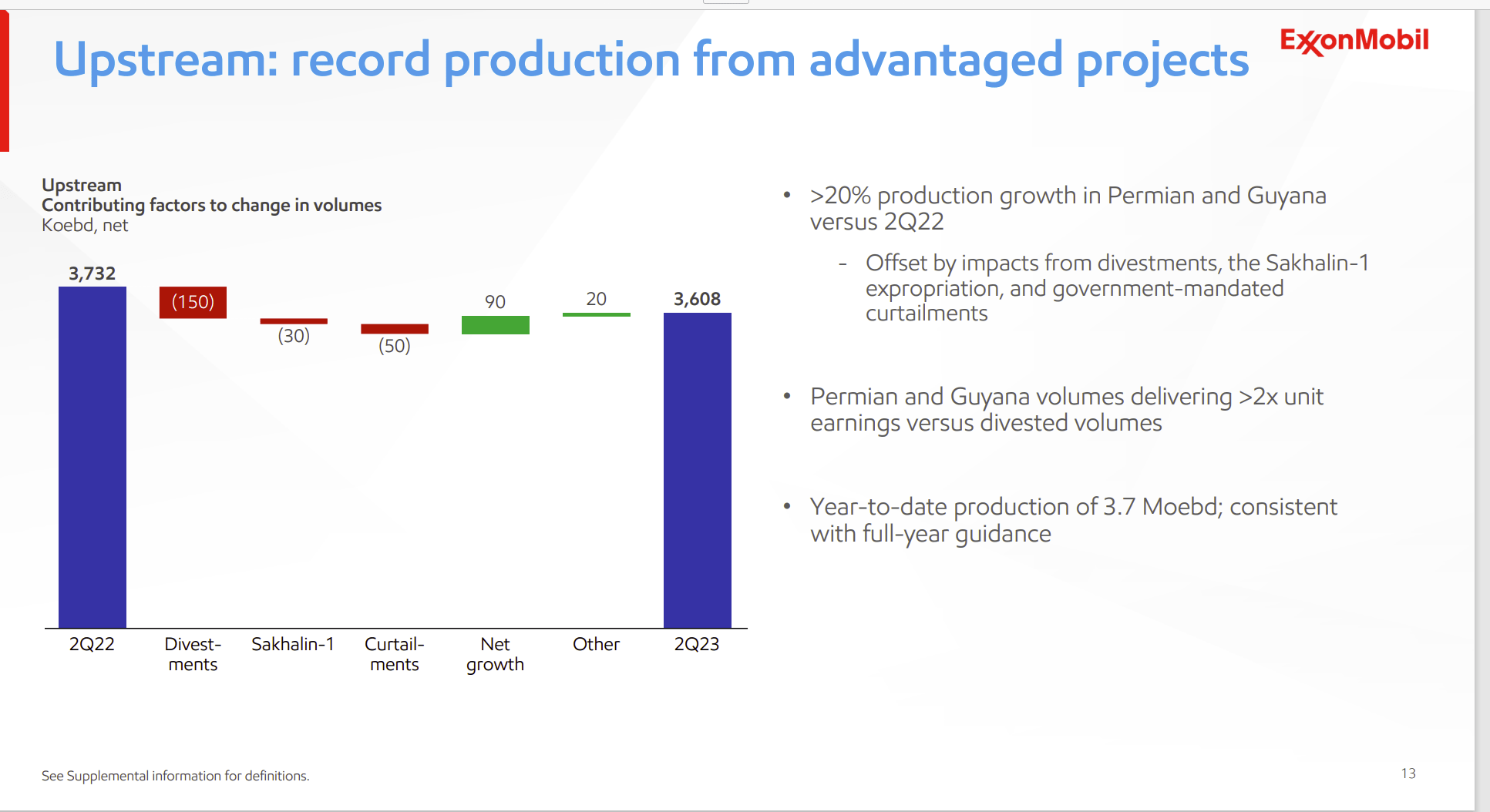

Production growth has been rather robust for a company of this size. There were some one-time items that hid the progress. But sooner or later the growth will show through.

Exxon Mobil Quarterly Production Growth Comparison (Exxon Mobil Second Quarter 2023, Earnings Slide Presentation)

Organic growth is already heading towards 10%. Now taking into account the one-time items volume was actually below the previous quarter (sequentially speaking). Even though volume was down sequentially, the volume reported was still very strong compared to the year before. Management has still more projects that will accelerate the growth rate besides Guyana.

There is a robust production growth guidance for the Permian operations and additional refining capacity was built to handle that volume. The company earnings will not only benefit from the additional production but also should benefit from the refining upgrade to more valuable products.

This pattern points to a likely future scenario for Guyana. Right now, the Guyana partnership produces oil. But there certainly would be a market for refined products should the company follow its usual pattern of adding the capability to produce value added products from the production.

Major 2023 Projects

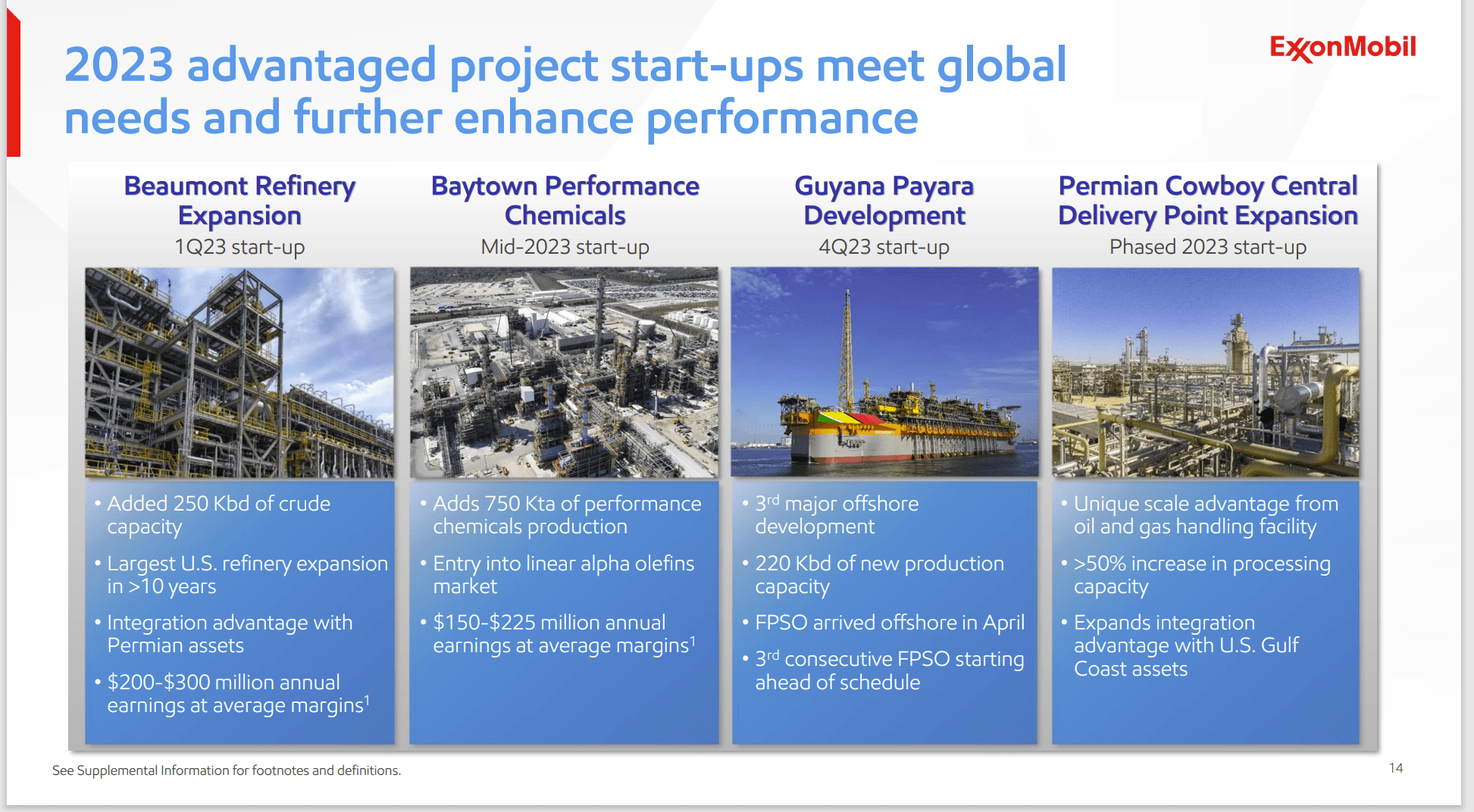

This is just a summary of the major 2023 projects that will begin to add to cash flow in the near future.

Exxon Mobil Summary Of Major Capital Projects (Exxon Mobil First Quarter 2023, Earnings Conference Call Slides)

The major projects are the result of billions in expenditures over a multi-year budget. But they are all scheduled to start up and contribute to cash flow either this fiscal year or not long after this fiscal year.

Since this slide was made, Exxon Mobil announced the acquisition of Denbury Inc. (DEN). This acquisition will add yet another major project to the group shown above.

Management has more of these projects underway and still more in the planning stage. Some like Point Thompson are more likely in the talking or wishing stage.

But the key is that this company is now on a growth trajectory. For a long-time, this company “tread water” and the stock price largely reflected that. Now, clearly that is changing to a growth trajectory.

That means that future dividend increases are likely to be larger than what has happened in the past. It takes time to transition to a new growth strategy (and money). So, dividend increases are currently lagging behind the profitability progress. But in the long run, dividend increases will catch up the pace of corporate growth.

The result of all of this is that Exxon Mobil is slowly turning into a growth and income play. For the last decade or so, it was primarily an income play with growth as an afterthought. As the growth part increases in importance, the company is likely to receive a higher valuation in the market long-term to recognize that growth.

Even without that consideration, the oil and gas industry is historically cheap and relatively out-of-favor. Just returning to some normal valuations should result in some decent appreciation pretty much across the board. Any premium growth projects would add to that. As a result, Exxon Mobil remains a strong buy consideration for those looking for a growth and income vehicle.

The oil and gas industry has cycles. But this company is safe enough to hold through those cycles. That appeals to a lot of risk averse investors.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of XOM, HES either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: I am not an investment advisor, and this article is not meant to be a recommendation of the purchase or sale of stock. Investors are advised to review all company documents and press releases to see if the company fits their own investment qualifications.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

I analyze oil and gas companies like Exxon Mobil and related companies in my service, Oil & Gas Value Research, where I look for undervalued names in the oil and gas space. I break down everything you need to know about these companies — the balance sheet, competitive position and development prospects. This article is an example of what I do. But for Oil & Gas Value Research members, they get it first and they get analysis on some companies that is not published on the free site. Interested? Sign up here for a free two-week trial.