Summary:

- Exxon Mobil Corporation reported its first-quarter earnings results on Friday morning.

- The performance was great. Profits and cash flows are strong, and Exxon Mobil is building a fortress balance sheet.

- Since Exxon Mobil Corporation is far more expensive compared to some of its peers, it may not be the best investment in the energy space.

Lorado/E+ via Getty Images

Article Thesis

Exxon Mobil Corporation (NYSE:XOM) reported its first-quarter earnings results on Friday morning. The company outperformed expectations and delivered strong results across the board. Investors can be very happy with XOM’s operational performance, but its valuation is not the lowest in the energy space – although it isn’t high in absolute terms, either.

What Happened?

Exxon Mobil Corporation reported its first-quarter earnings results on Friday before the market opened. The company’s top-line and bottom-line results can be seen here:

Seeking Alpha

While revenues were down on a year-over-year basis, and missing estimates, Exxon Mobil was way more profitable than what the analyst community had expected. For a mature value company such as Exxon Mobil, profits are more important than sales, I believe, thus I see these numbers positively.

Exxon Mobil: The King In The Energy Space

Not too long ago, the market wasn’t appreciating Exxon Mobil. The company lost its place in the Dow Jones Index, and for some time, its peer Chevron Corporation (CVX) was trading at a higher market capitalization versus Exxon Mobil. At the time, the market didn’t like Exxon Mobil’s growth spending and its focus on bringing new major oil projects forward, such as its vast asset base in Guyana.

But with oil prices rising significantly following the pandemic, Exxon Mobil is now back where it belongs – at the top of the energy space. This holds true when we look at its market capitalization, but also when we look at the underlying results that Exxon Mobil generates. Those were not only strong during 2022, but XOM continued to perform very well in early 2023, despite the fact that oil and gas prices have pulled back significantly from the highs seen in the summer months of 2022.

Exxon Mobil generated net earnings of $11.4 billion during the first quarter, which was around 15% below the levels seen during the previous quarter, Q4 2022, but which was up massively on a year-over-year basis. Even better, Exxon Mobil’s Q1 2023 results were the best Q1 results in the company’s history – not even in 2008, when oil prices peaked at around $150 XOM was this profitable. This can be explained by several contributing factors.

First, Exxon Mobil’s ongoing investments in its asset base are increasingly paying off. While some other energy companies have changed their business model by reducing oil and gas investments while putting more money into green energy investments, XOM has remained focused on developing hydrocarbon assets, primarily in the Permian Basin and in Guyana. At the same time, Exxon Mobil has also been investing in refining assets – its 250,000 barrels per day Beaumont refinery expansion started production and reached capacity in Q1, for example. Exxon Mobil is also active in the “green” industry via its emerging carbon-capture business, which is potentially very promising, but we don’t know yet how profitable this franchise will become. But unlike peers such as BP p.l.c. (BP) or Shell plc (SHEL), XOM continues to pursue growth in the hydrocarbon space, which is paying off in the current oil price environment. Excluding the impact of divestments and the Sakhalin-1 expropriation, production was up by a hefty 300,000 barrels per day during the first quarter, relative to the previous year’s first quarter.

Second, Exxon Mobil has been laser-focused on bringing down expenses in order to boost margins. Most energy companies moved in this direction following the 2014 oil price crash, and even more so following the 2020 oil price crisis during the initial phase of the pandemic. Overall, the industry has become leaner and more efficient, but Exxon Mobil stands out among its peers. Its cost-cutting efforts have been highly effective, and the company continues to pursue additional cost savings, despite the fact that it is very profitable already. By the end of 2023, XOM plans to have achieved $9 billion in structural cost savings, while the cost savings totaled $7.2 billion at the end of 2023. Throughout the coming three quarters, XOM thus plans to shave another $2 billion in expenses. Investors can be very happy about this shareholder value-driving approach of improving XOM’s efficiency – a leaner and meaner XOM is a more profitable, lower-risk XOM.

Exxon Mobil’s strong profitability naturally also translates into a compelling cash flow picture. The company generated operating cash flows of $16.3 billion during the first quarter, which translates into free cash flows of $11.4 billion once we account for investments and divestments. With $6.3 billion in capital expenditures during the quarter, XOM is pretty much on track to achieve its ~$24 billion investment target for the current year. With annualized free cash flows in the $46 billion range, Exxon Mobil trades at a little more than 10x free cash flows right now, which is far from a high valuation in absolute terms.

There are several ways for a company to utilize its free cash flows. They can be returned to shareholders via dividends and/or buybacks, they can be used for deleveraging, or they can be used for M&A. While there are rumors about potential acquisitions by Exxon Mobil (Pioneer Natural Resources (PXD) is a rumored target), XOM has not made any major M&A moves in the recent past. The company is thus focused on shareholder returns and debt reduction, which is not a bad thing.

During the first quarter, Exxon Mobil paid out $8.1 billion to its owners, with a little more than half of that via buybacks, and the remainder via dividends. The buyback pace of around 4% is very solid, although by far not the highest in the energy space. The dividend yield of 3.1%, likewise, is solid but not great relative to the peer group average. When it comes to strengthening the balance sheet, Exxon Mobil has made massive progress in recent years. As of the end of the first quarter, Exxon Mobil’s net debt (total debt minus cash and equivalents) stood at just $8 billion – that’s down from a peak of more than $60 billion at the end of 2020. It would not be surprising to see Exxon Mobil end 2023 with a positive net cash position, as paying down another $8 billion in net debt shouldn’t be too hard for the company over the next three quarters, at least if there is no major acquisition. Exxon Mobil has guided for $17.5 billion in buybacks during 2023, which is relatively in line with the buyback pace in Q1, thus it does not look like shareholder returns will be ramped up again in the near term.

Unless oil prices drop substantially, XOM should thus have ample excess free cash flow in Q2-Q4 that can be used for debt reduction while continuing to offer shareholder payments at a similar level as in Q1. Exxon Mobil’s fortress balance sheet that is getting stronger every quarter insulates the company from rising interest rates and reduces risks – even if oil prices were to fall off a cliff (which seems unlikely to me), XOM would be well-positioned to stomach that.

XOM’s Valuation

From an operational basis, there are many things that look great. Production is growing, the company owns strong low-risk, low-cost assets in the Permian Basin and Guyana, and management has done a great job when it comes to bringing down expenses and improving margins.

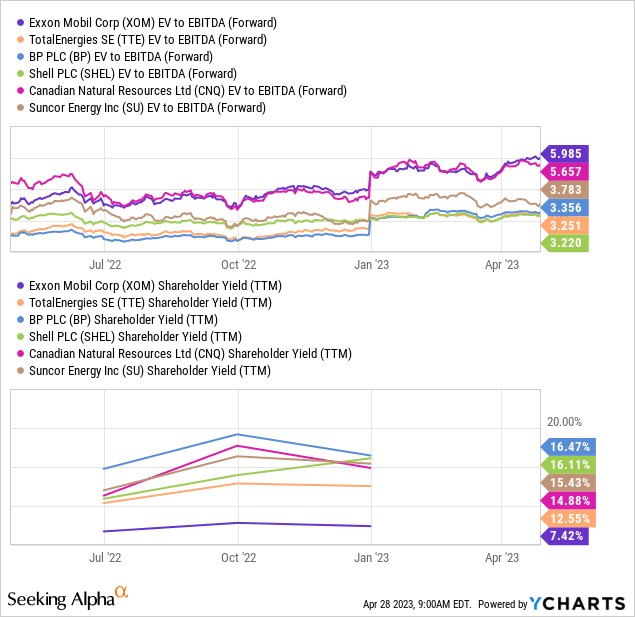

Unfortunately, while not being expensive in absolute terms, XOM is by far not as cheap as some of its peers:

XOM trades with an enterprise value to EBITDA multiple of 6.0, which is substantially higher compared to the valuation its European peers trade at, such as TotalEnergies SE (TTE), Shell, and BP. The Canadian integrated energy companies such as Canadian Natural Resources (CNQ) and Suncor (SU) are also cheaper. That’s not XOM’s fault, but it means that shareholders have to pay a substantial premium if they want to own XOM over other major energy players. At the same valuation, I surely would prefer XOM over Shell or BP – but when the latter two trade at half the valuation XOM trades at, I think differently.

XOM’s premium valuation also results in a comparatively weak shareholder yield – not in absolute terms, but in relative terms. While a 7% shareholder yield is very solid, the 13%-16% shareholder yields of XOM’s peers are even more attractive, of course.

Takeaway

Exxon Mobil Corporation is the largest (Western) oil company and one of the strongest for sure. Its performance has been great, and its strategy of focusing on assets such as Guyana is paying off. The Q1 results were highly compelling as well, and I believe that XOM can rightfully be called the king in the energy space.

But with some of its peers trading at exceptionally low valuations, while Exxon Mobil Corporation is considerably more expensive, I still prefer to hold its cheaper, higher-yielding peers, although I would surely switch to Exxon Mobil Corporation in case they were to trade at similar valuations and yields.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BP, SHEL, SU, CNQ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Is This an Income Stream Which Induces Fear?

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% – 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio’s price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!