Summary:

- Exxon Mobil Corporation announced a massive acquisition of Pioneer Natural Resources, expected to provide $2 billion in pre-tax synergies.

- Exxon Mobil generates strong earnings, with production of 3.7 million barrels/day and a double-digit QoQ increase in earnings.

- The company’s outlook shows volatility will remain, but it should continue to execute on its goals and focus on long-term growth with major acquisitions.

CHUNYIP WONG

Exxon Mobil Corporation (NYSE:XOM, “ExxonMobil”) recently announced the massive acquisition of Pioneer Natural Resources, one of the largest in its history, which we discussed in detail here. The company is the largest publicly traded oil company outside of Saudi Aramco, and recently announced its earnings. As we’ll see throughout this article, it’s a strong company at a valuation to match.

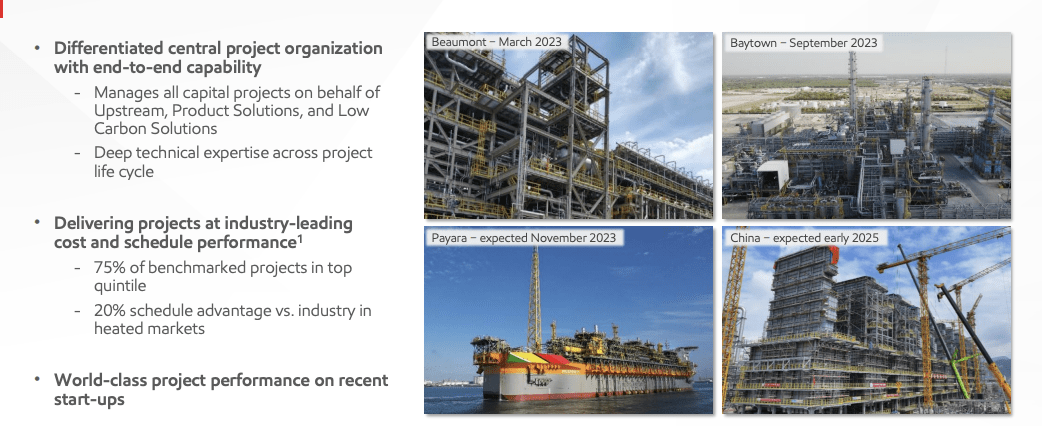

ExxonMobil Global Scale

ExxonMobil is set apart by its global scale and ability to construct massive projects.

ExxonMobil Investor Presentation

The company has had numerous accomplishments, such as the ramp-up in production from Guyana. It’s built its expert refining capacity, and is working on numerous projects with $10s of billions in capital requirements. The company continues to execute in the top percentiles, supported by its strong project history.

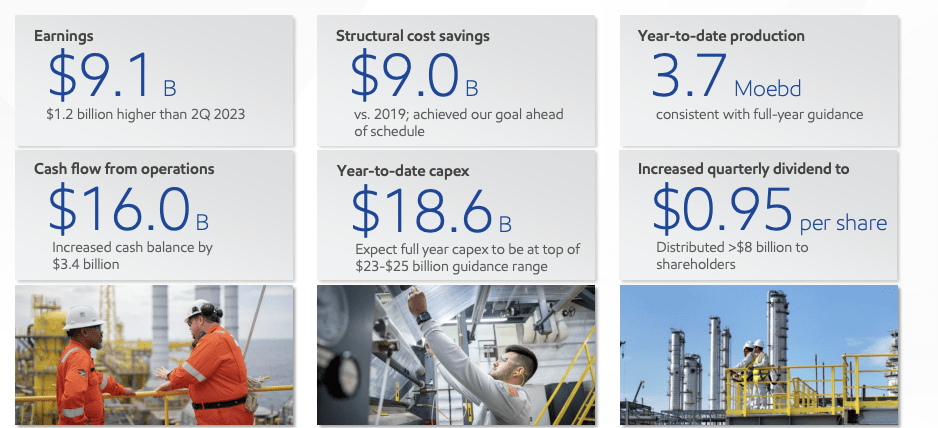

ExxonMobil Q3 Earnings

The company generated strong earnings for the third quarter, supported by its production.

ExxonMobil Investor Presentation

The company’s production was 3.7 million barrels / day. The company’s annualized dividend is $3.8 / share, a roughly 3.5% dividend yield, which costs it $15 billion annualized. That’s less than 2Q worth of earnings, with the company’s earnings for the quarter coming in at $9.1 billion. That was a double-digit QoQ increase.

The company is continuing to focus on structural cost savings, with quarterly capex at $4.7 billion. CFFO is $16 billion, with free cash flow (“FCF”) comfortably in the double-digits. That means an almost double-digit FCF yield for the company helping to highlight its financial strength. The company has minimal debt and can utilize that FCF for strong shareholder returns.

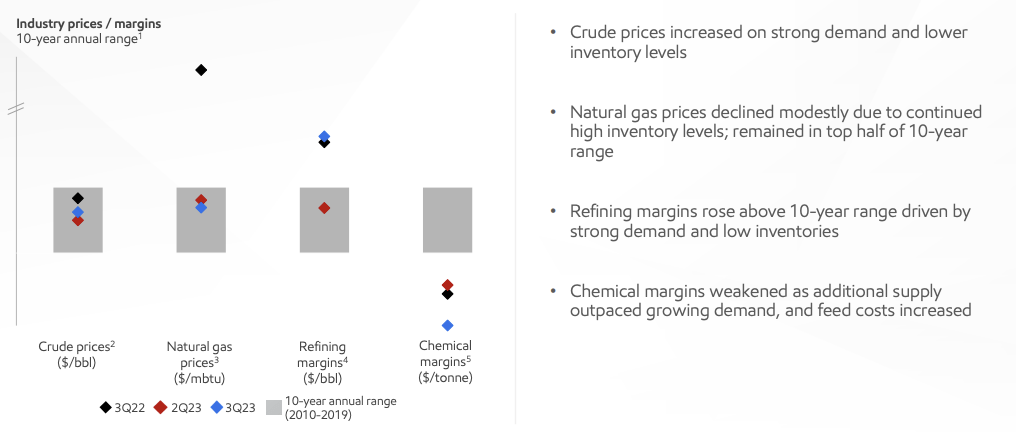

ExxonMobil Pricing

The company’s pricing shows the continuous volatility in the industry.

ExxonMobil Investor Presentation

Chemical margins are well below their 10-year historic range. Refining margins have improved QoQ and are well above averages. Crude prices and natural gas prices are within the average, but especially natural gas prices are down substantially YoY. The volatility in the company’s pricing shows the benefit of an integrated portfolio.

The company makes more in some sectors and less than others. Overall, minus a massive downturn in the industry, cash flow remains strong.

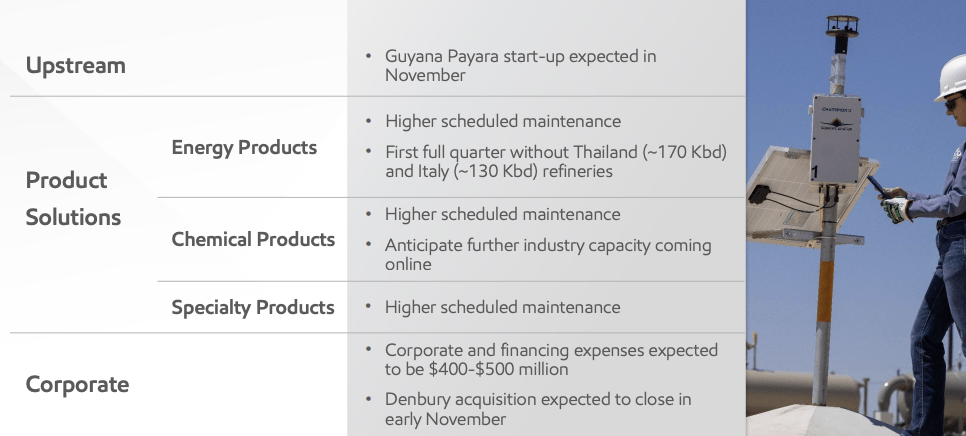

ExxonMobil Outlook

The company’s outlook shows that volatility will remain, but the company will continue to execute on its goals.

ExxonMobil Investor Presentation

Payara will start-up in November, adding roughly 50 thousand barrels / day in high margin production for the company. However, the company has also sold its Thailand and Italy refineries which will impact margins there. Maintenance will be temporarily higher, and in chemicals with more capacity, margins will continue to be compressed.

The company is working to close a number of major acquisitions, including Denbury and Pioneer Natural Resources, which both have a strong focus on long-term growth.

ExxonMobil Pioneer Natural Resources

The company’s Pioneer Natural Resources is the largest acquisition that the company has made in decades.

ExxonMobil Investor Presentation

The $60 billion acquisition is expected to provide $2 billion in pre-tax synergies. The company is receiving Midland acreage that it believes is better than its own, with strong integrations to the company’s existing acreage. $2 billion synergies per year will help the overall cash flow of the business. The high-margin production guidance is impressive.

The company expects combined Permian production to hit 2 million barrels / day in 2027. The company once aimed for $15 / barrel in Permian production targets, and we expect it to be able to improve on that. At current prices, that means substantial margins and profits.

Thesis Risk

The largest risk to our thesis is that ExxonMobil is priced for a higher oil price environment. Russia’s invasion of Ukraine combined with global uncertainty, and a reopening from COVID-19, after years of underinvestment, have all buoyed demand. There’s no guarantee that prices will remain higher, and if they decline, that can hurt long-term returns.

Conclusion

ExxonMobil is a giant. Acquiring Pioneer Natural Resources is a great move, although we would have liked to see a cash-heavy acquisition, even in the current interest rate environment. The company could always redirect its massive cash flow to paying down debt, with the combined company outputting almost $50 billion a year in FCF ($35 billion post dividend).

The dilution, for a company known to repurchase shares, indicates to us that ExxonMobil knows its share price is currently potentially on the higher end. We don’t find that surprising, the company is reliant on longer term oil prices to justify its valuation and longer term shareholder returns. Still the benefit of synergies along with its asset strength can help in the long-term.

ExxonMobil’s ability to drive long-term shareholder returns make it a valuable investment opportunity. Let us know your thoughts in the comments below.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of XOM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

You Only Get 1 Chance To Retire, Join The #1 Retirement Service

The Retirement Forum provides actionable ideals, a high-yield safe retirement portfolio, and macroeconomic outlooks, all to help you maximize your capital and your income. We search the entire market to help you maximize returns.

Recommendations from a top 0.2% TipRanks author!

Retirement is complicated and you only get once chance to do it right. Don’t miss out because you didn’t know what was out there.

We provide:

- Model portfolios to generate high retirement cash flow.

- Deep-dive actionable research.

- Recommendation spreadsheets and option strategies.