Summary:

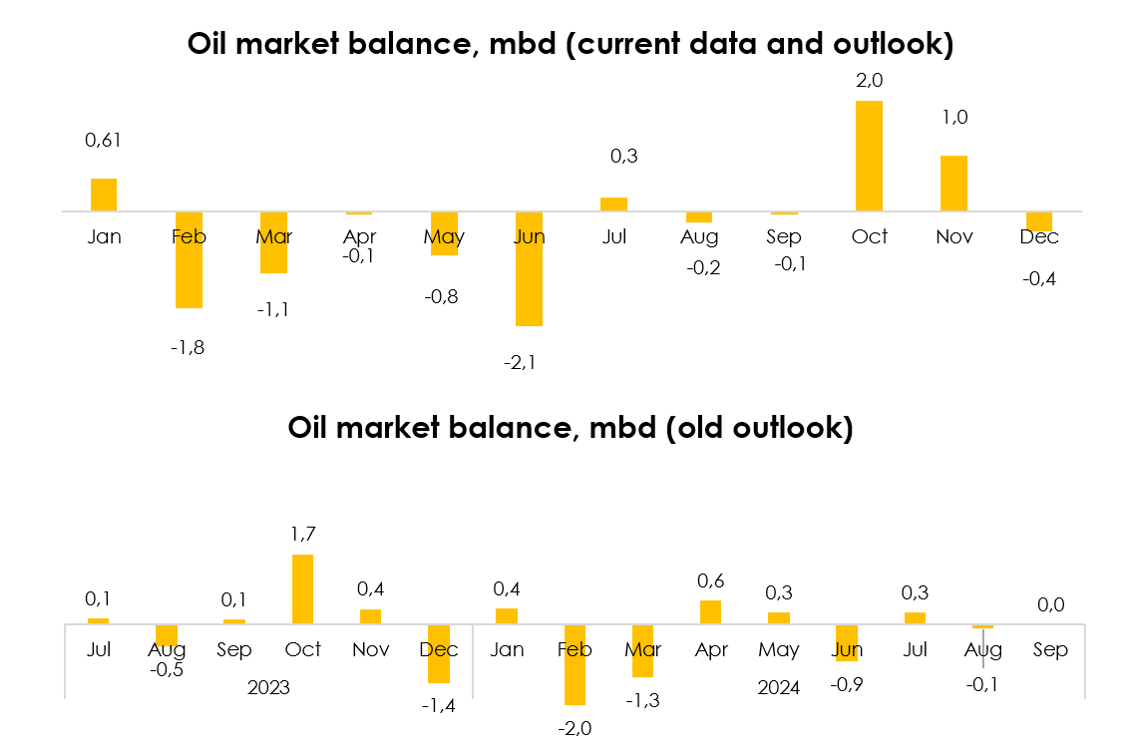

- We have changed the forecast for the oil market balance in Q2 2024 to a deficit due to a decrease in the forecast for production in Russia and OPEC+.

- We have raised our forecasts for XOM’s oil and gas volumes available for sale due to the expectations of rising demand in the key regions for the company.

- We are cutting the forecast for Exxon Mobil’s gross costs from 55.7% of revenue to 54.1% for 2024, and from 56.1% of revenue to 55.2% for 2025.

- The deal with Pioneer is expected to be closed in Q2 2024, and it will increase XOM’s oil and gas production capacity and reduce the production costs.

JHVEPhoto/iStock Editorial via Getty Images

Investment thesis

We have covered the stock before, and there have been a number of changes since last quarter, which are the subject of this report:

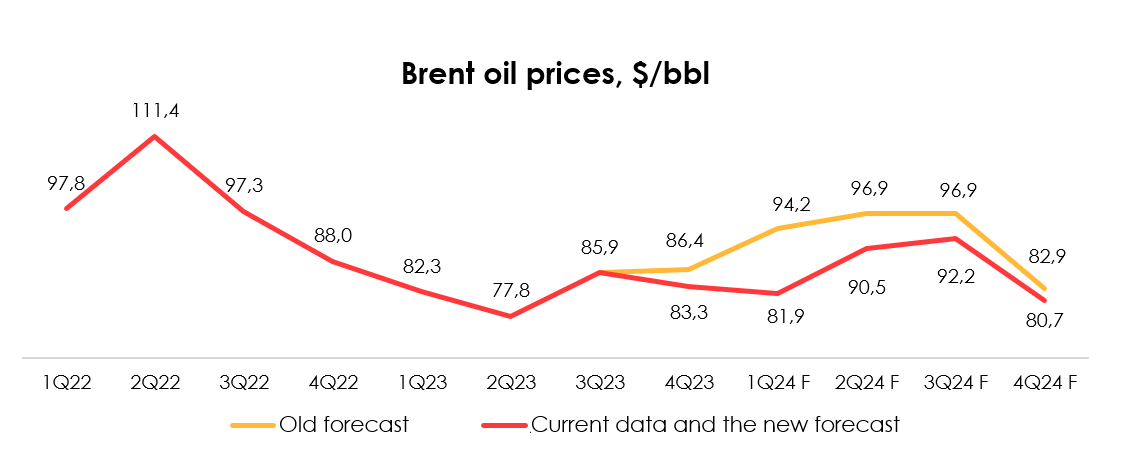

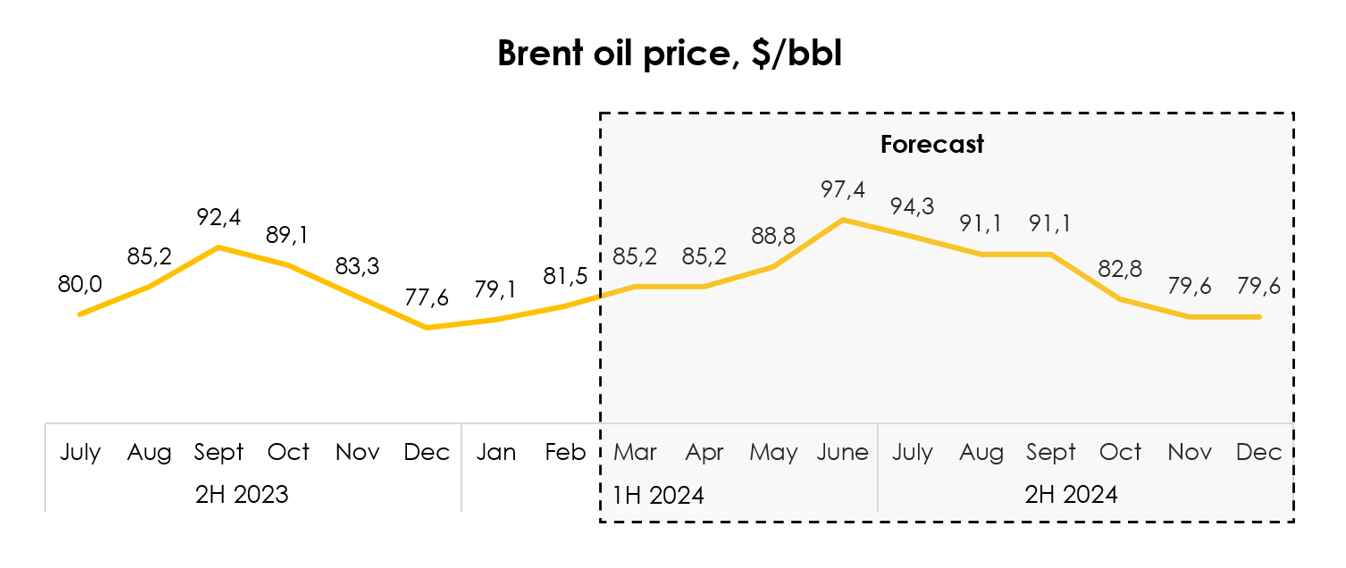

- We have lowered our oil price forecast for 2024 from an average of $92.7/bbl to $86.3/bbl. At the same time, we expect oil prices to rise to $97/bbl in June 2024 on the back of a tight market, and to $80/bbl in November-December 2024.

- Both the TTF and Henry Hub forecasts have also been lowered.

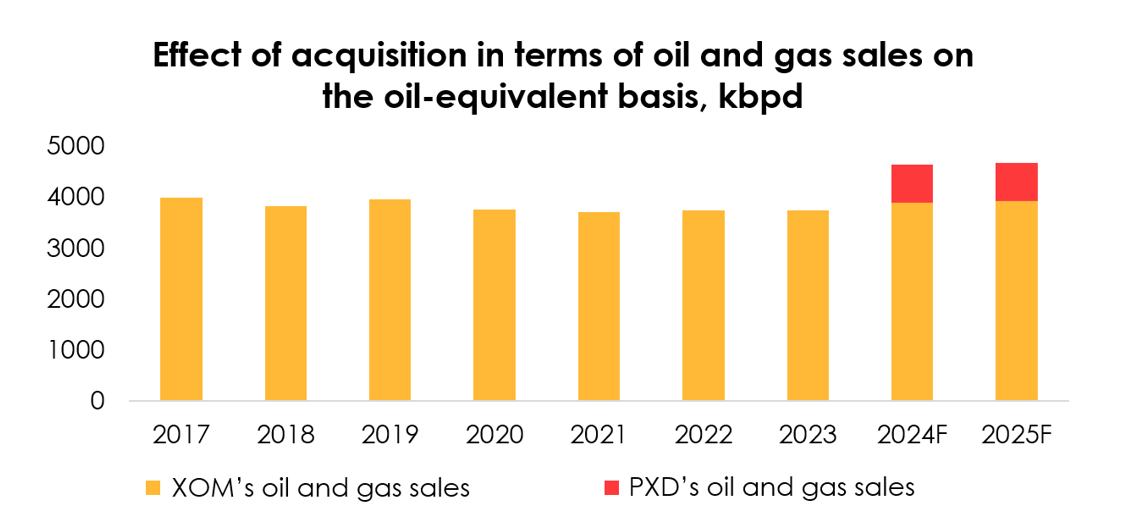

- We have raised the total average volume of Exxon Mobil’s (NYSE:XOM) oil and gas available for sale from 3842 kbpd to 3891 kbpd for 2024, and from 3871 kbpd to 3929 kbpd for 2025 due to expectations of rising gas demand in the regions that are key for the company and the increased forecast for oil production around the world over the next two years, with Exxon Mobil’s share of the global oil production market expanding.

The deal with Pioneer Natural Resources will tentatively close in 2Q 2024. We expect that, once the deal is completed, it will boost Exxon Mobil’s capacity to produce oil and gas from 3891 kbpd on the oil-equivalent basis to 4635 kbpd in 2024, and from 3929 kbpd to 4674 kbpd in 2025, which is equivalent to a growth of 24% y/y and 1% y/y, respectively.

Based on the new assumptions, we assign the HOLD rating for the shares.

Oil market balance

Below are the main factors that have influenced the revision of the oil market balance forecast since our previous report.

On the supply side:

1. Russia will continue to reduce oil production

In April 2023, at the OPEC+ meeting, Russia announced a voluntary reduction of oil production from 11.2 mb/d in February 2023 to 10.7 mb/d by the end of 2024 (excluding condensate – from 9.95 to 9.45 mb/d). Russia also voluntarily reduced exports of oil and petroleum products by 0.5 mb/d in August 2023 and by 0.3 mb/d in September-December 2023 (from about 7.6 mb/d in May to 7.3 mb/d in September-December 2023) compared to May-June 2023.

For Q2 2024, it was decided to further reduce oil production (in addition to reducing production to 10.7 mb) by an average of 471 thousand barrels per day. In April, the production cut will amount to 350 thousand b/d, and exports will be reduced by 121 thousand b/d. In May, the reduction in oil production will amount to 400 thousand b/d and the export cut will be amount to only 71 thousand b/d. In June, production will be cut by 471 thousand b/d and there will be no cut in exports.

We have lowered our forecast for Russia’s oil production in Q2 2024 from 10.7 mb/d to 10.3 mb/d due to the announcement of an additional 0.471 mb/d reduction in Russia’s oil production in Q2 2024.

Total exports of oil and petroleum products decreased from 7.7 mb/d in 2022 to 7.4 mb/d in 2023. In 2024, we expect that exports of oil and petroleum products will amount to 7.0-7.4 mb/d, taking into account the voluntary cuts.

2. OPEC+ extended oil production restrictions for Q2 2024

In May 2023, Saudi Arabia voluntarily reduced oil production by 0.5 mb/d compared to April 2023 (from 10.5 to 10.0 mb/d). In addition to Saudi Arabia, other OPEC+ countries continued to reduce oil production. Later, OPEC+ extended these voluntary production cuts from May 2023 to all of 2024.

In July 2023, Saudi Arabia decided to further reduce production by 1 mb/d (Saudi Arabia’s quota was not reduced) – from 10 mb/d in June to 9 mb/d. Later, this voluntary production cut was extended to Q1 2024. In Q1 2024, several OPEC+ countries also voluntarily reduce oil production from 2024 quotas: Iraq – by 223 kb/d, the United Arab Emirates – by 163 kb/d, Kuwait – by 135 kb/d, Kazakhstan – by 82 kb/d, Algeria – by 51 kb/d and Oman – by 42 kb/d.

In March 2024, OPEC+ decided to extend the production cut of Saudi Arabia by 1 mb/d and other countries (in fact, production of other countries is not significantly different from quotas) for Q2 2024.

We have lowered our forecast for OPEC+ oil production in Q2 2024. We now expect OPEC oil production in Q2 2024 to be roughly the same as in Q1 2024 – 31.8 mb/d. At the same time, we expect oil production (excluding condensate) from the OPEC+ countries participating in the oil production deal (including Russia) to decline from 34.9 mb/d in January 2024 to 34.5 mb/d in Q2 2024.

3. The United States will resume sanctions against Venezuela in April

In this context, we do not expect Venezuela’s oil production to grow significantly in 2024, remaining at the level of 0.8 mb/d.

On the demand side:

1. Concerns over low economic activity in China and slowing demand put pressure on oil prices

Concerns about the global economic slowdown and weak demand are not being negatively impacted by oil prices. Since November, China’s PMI has mostly been falling below 50: from 49.5 in October to 49.1 in February 2024.

At the same time, business activity indices in the US and the EU have been growing since the beginning of 2024. (The U.S. and Chinese manufacturing PMIs fell below 50, missing forecasts. The US PMI rose from 47.9 in December 2023 to 52.2 in February 2024. The EU PMI rises from 43.1 in October to 44.4 in December 2023 and 46.5 in February 2024.

We expect oil demand in the EU to remain at 2023 levels in 2024 due to the economic slowdown, and in the US to grow slightly – by 0.2 mb/d YoY. At the same time, we expect demand in China to grow by 0.5 mb/d YoY in 2024 and in other countries (excluding the US, EU and China) by 1.15 mb/d YoY.

2. Net speculative positions in oil increased in March 2024

Since the beginning of 2024, the CFTC net speculative positions in oil have grown significantly: from 164 mln barrels in January 2024, up to 192 mln barrels at the end of February and up to 239 mln barrels in the 2nd week of March 2024, the minimum indicator of net speculative positions in 2023 was observed in July – 138 million barrels. The increase in net speculative positions was mainly due to an increase in the volume of long positions.

Oil prices were supported by the opening of speculative longs. Given the relatively weak increase in oil prices, it is possible that demand in February was lower than expected.

Speculative net positions in oil rose in March amid an increase in speculative longs. The net position in oil returned to the average levels of 2021-2022 after reaching extremely low levels at the end of 2023.

Invest Heroes

Outlook for Brent oil prices

As a result of the weaker oil price environment than we had previously expected, we are setting a more conservative premise for the pace of price growth in March 2024. As a result, we have lowered our forecast for the Brent crude oil price in Q1 2024 to $81.9/bbl.

We have lowered our oil price forecast for 2024 from an average of $92.7/bbl to $86.3/bbl. At the same time, we expect oil prices to rise to $97/bbl in June on the back of a tight market, and to $80/bbl in November-December.

Invest Heroes Invest Heroes

Macro outlook for the gas market

According to the International Energy Agency, gas demand will rise by 2.5% y/y (+2 pp y/y) in 2024, driven by renewed demand growth in key natural gas markets.

Most of the growth will come from the Asia-Pacific region (which includes Exxon Mobil’s two major gas markets: Asia and Australia and Oceania, together accounting for more than 60% of gas demand) where it is expected to come to 4% y/y in 2024, following a 2.5% increase in 2023. One of the largest gas importers in APAC is China, where industrial activity is recovering and gas consumption in the power sector is more intensive. In addition to China, it is worth noting such fast-growing markets as Thailand, India, as well as Bangladesh and Pakistan, where higher gas demand is expected due to reduced domestic production of gas and putting into operation new gas-fired power plants.

In the US (the second most important market for Exxon Mobil, accounting for 30% of gas demand), natural gas consumption expanded by less than 1% in 2023, which was attributable, among other things, to low economic activity and mild weather conditions. Natural gas was used to generate 42% of all US electricity in 2023 (+3 pp) amid the ongoing the shift from coal to gas. The IEA forecasts that gas demand will rise by about 1% y/y in 2024 due to:

- increasing gas consumption in the residential and commercial sectors (provided the return of normal weather conditions), which will be partially offset by lower gas demand in the industrial sector amid a weak macroeconomic environment, as well as a moderate increase in the use of renewable energy (given the extension of the IRA).

In the EU, according to previously adopted measures, countries will continue to reduce gas demand by 15% y/y until the end of the 2023/24 heating season. However, once the year 2024 is over, demand is estimated to rise by 3% y/y due to the anticipated recovery of economic activity in Europe.

IEA

Gas price outlook

We use the Henry Hub and TTF benchmarks to forecast gas prices for domestic sales in the US and for international sales, respectively.

A significant increase in US gas production, along with extremely warm winter resulted in a gas surplus in the country, which brought down Henry Hub prices. Price volatility held above average throughout the year due to the increased share of gas-powered electricity generation (42% of all electricity).

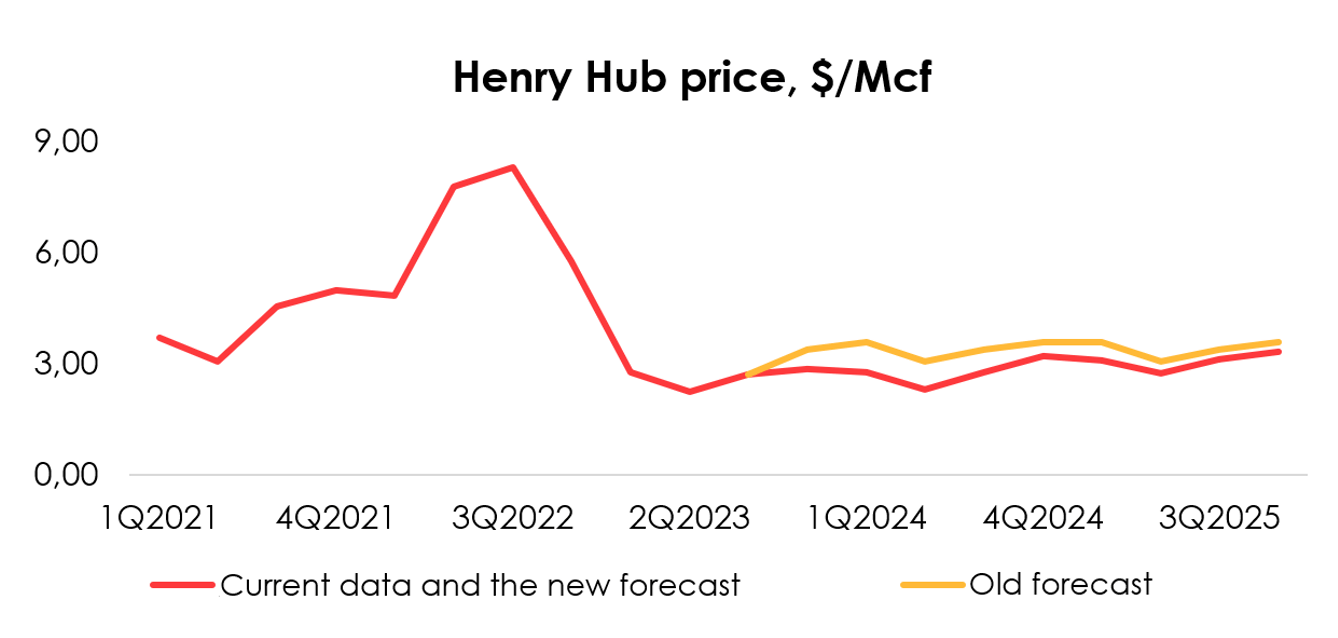

The forecast for this price benchmark is provided by the US Energy Information Administration (EIA). The agency reduced it price estimate. For the short-term, that’s because mild weather conditions are seen persisting until the start of 2Q 2024. For the medium-term, we believe, it is because production is set to hold high. The Henry Hub price forecast was cut from $3.38/Mcf to $2.76/Mcf and $3.06/Mcf for 2024 and 2025, respectively.

EIA

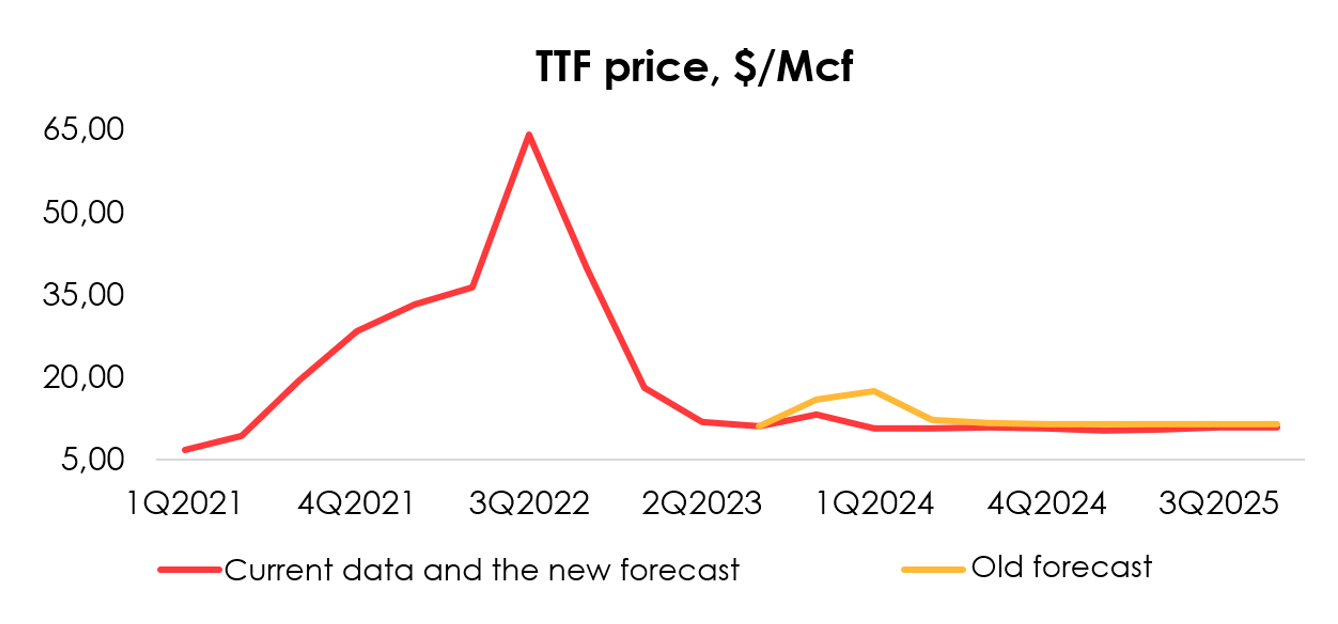

Based on the macroeconomic environment that we described above, we are lowering the forecast for the TTF price from $13.25/Mcf to $10.84/Mcf for 2024, and from $11.54/Mcf to $10.69/Mcf for 2025.

Invest Heroes

Exxon Mobil’s revenue structure

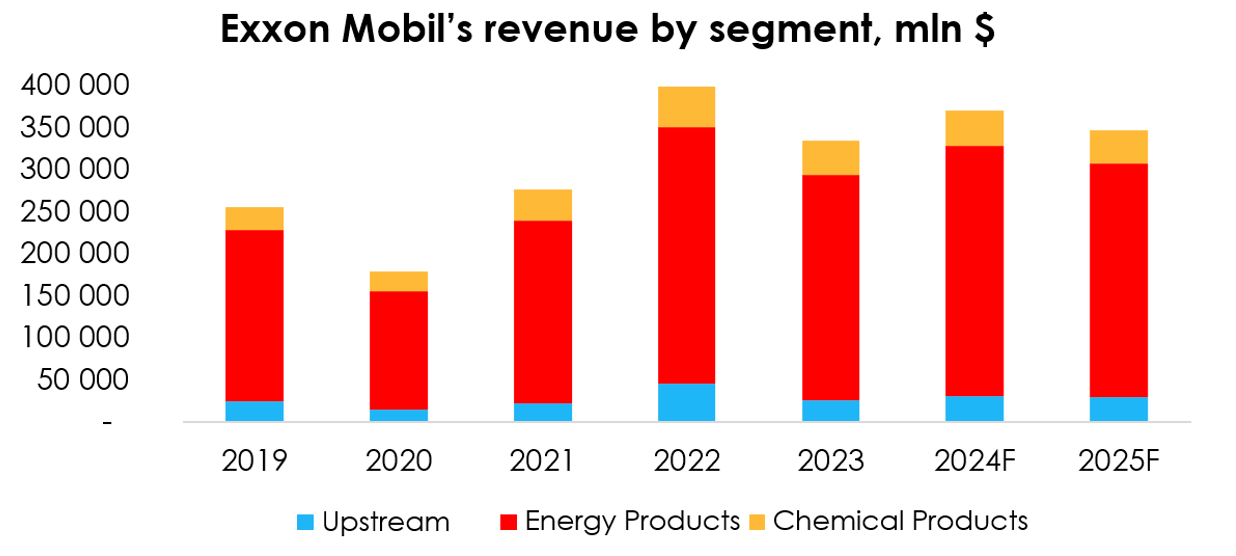

The biggest proportion of the revenue structure comes from the Energy Products segment, which consistently brings XOM ~80% of its revenue and comprises oil and gas processing. The Chemical Products segment, which produces petrochemicals, brings in ~11%. The Upstream segment (oil exploration and production) makes up ~9% of the company’s total revenue.

We expect the revenue structure by segment to be maintained over the forecast period.

Invest Heroes

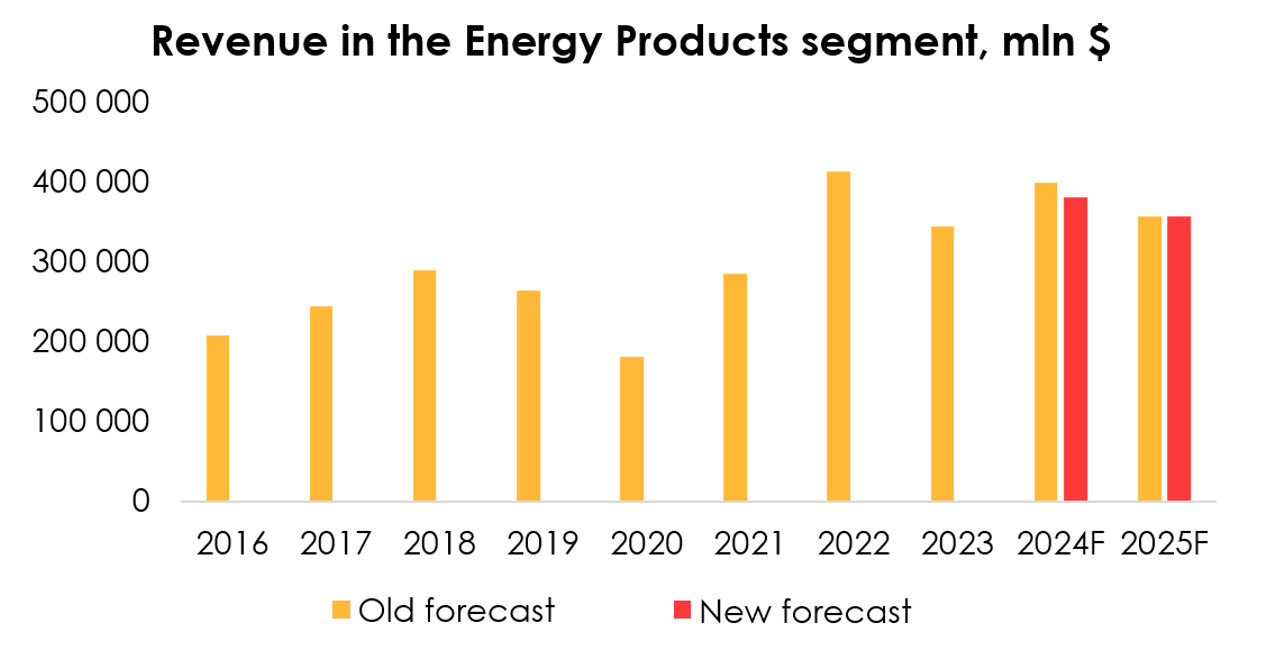

We have lowered the forecast for the Energy Products segment from $321.9 bln (+20% y/y) to $298.3 bln (+11% y/y) for 2024, and from $287.6 bln (-11% y/y) to $279 bln (-6% y/y) for 2025 due to:

- the reduction of the forecast for Brent oil prices from $92.7/bbl to $86.3/bbl for 2024, and from $82.9/bbl to $80.7/bbl for 2025;

- the expected decline of selling prices of oil products in 2024-2025 that will follow oil prices;

- the reduced forecast for natural gas prices on the US domestic market and in international sales.

Despite the lower forecast in 2024, we expect revenue in the segment to rise YoY, which will largely drive up all of Exxon Mobil’s revenue in 2024.

Invest Heroes

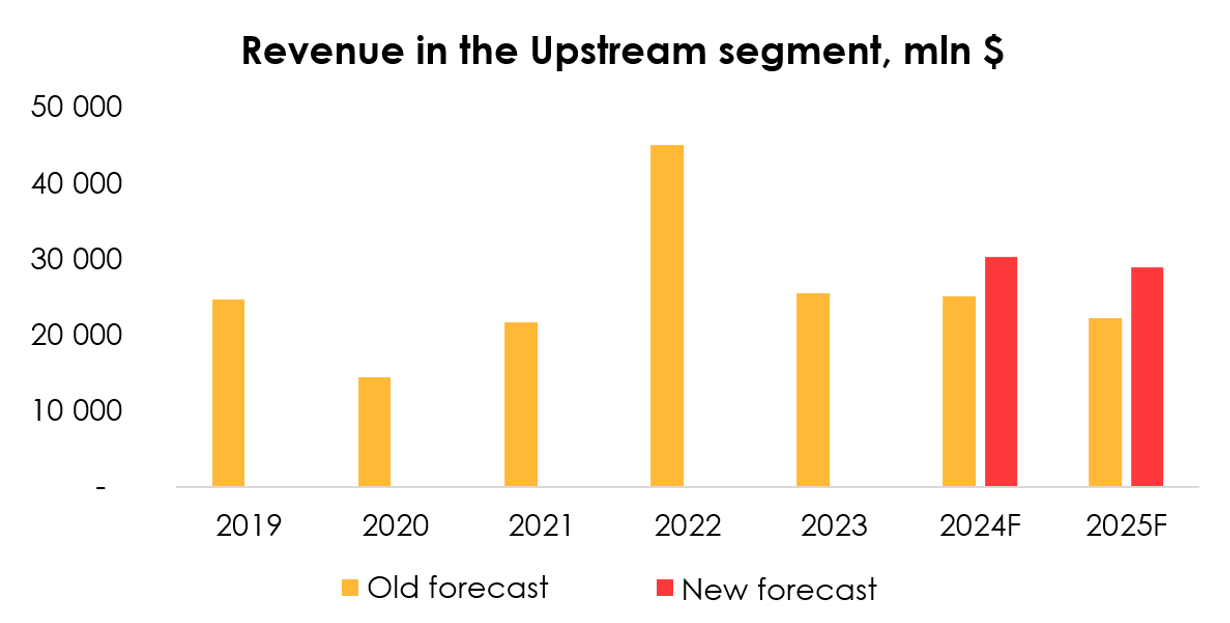

We have raised the forecasts for oil and gas volumes available for sale due to:

- expectations of rising demand in the regions that are key for the company: Asia, the US and Australia;

- the increased forecast for oil production around the world over the next two years, with Exxon Mobil’s share of the global oil production market expanding.

As a result, we have raised the total average volume of oil and gas available for sale from 3842 kbpd to 3891 kbpd for 2024, and from 3871 kbpd to 3929 kbpd for 2025.

As such, we are raising the forecast for revenue in the Upstream segment from $25.1 bln (-2% y/y) to $30.4 bln (+19% y/y) for 2024, and from $22.3 bln (-11% y/y) to $29 bln (-4% y/y) for 2025 on the back of rising volumes of oil and gas sales from 2024-2025 and the increased forecast for 2025 oil prices, which was partially offset by the lower forecast for gas prices in 2024 and 2025.

Invest Heroes

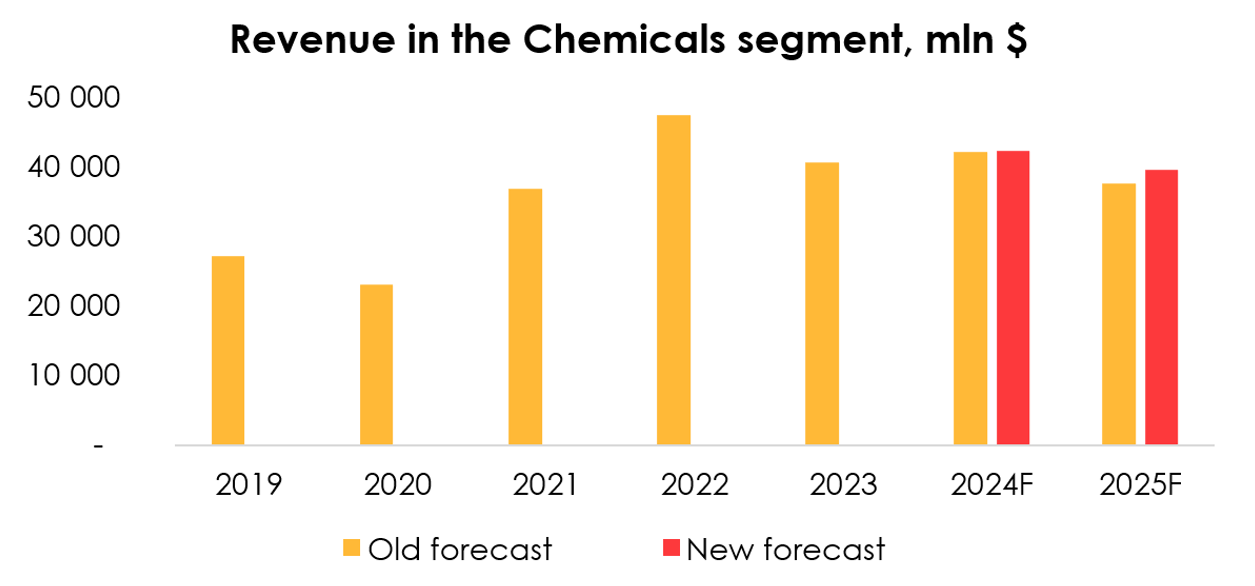

The forecast for revenue in the Chemical Products segment has been raised from $42.2 bln (+4% y/y) to $42.4 bln (+4% y/y) for 2024, and from $37.6 bln (-11% y/y) to $39.6 bln (-7% y/y) for 2025, which was driven by the projection that selling prices of oil products will be higher in 2024 following oil prices.

Invest Heroes

Exxon Mobil’s financial results

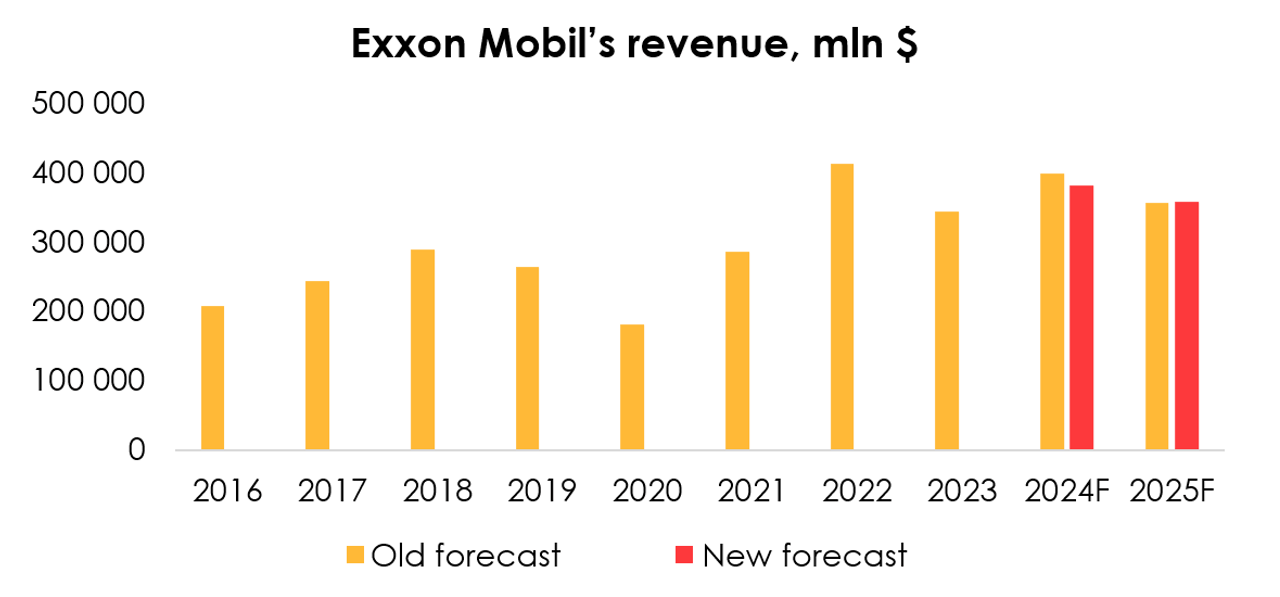

We are lowering the forecast for Exxon Mobil’s revenue from $400.1 bln (+16% y/y) to $381.6 bln (+11% y/y) for 2024, but are raising it from $357.7 bln (-11% y/y) to $358 bln (-6% y/y) for 2025 due to:

- the lower forecasts for revenue in the Energy Products for 2024 and 2025, which was partially mitigated by the higher revenue forecast for the Chemical Products and Upstream segment;

- the increased forecast for the sales volumes.

Invest Heroes

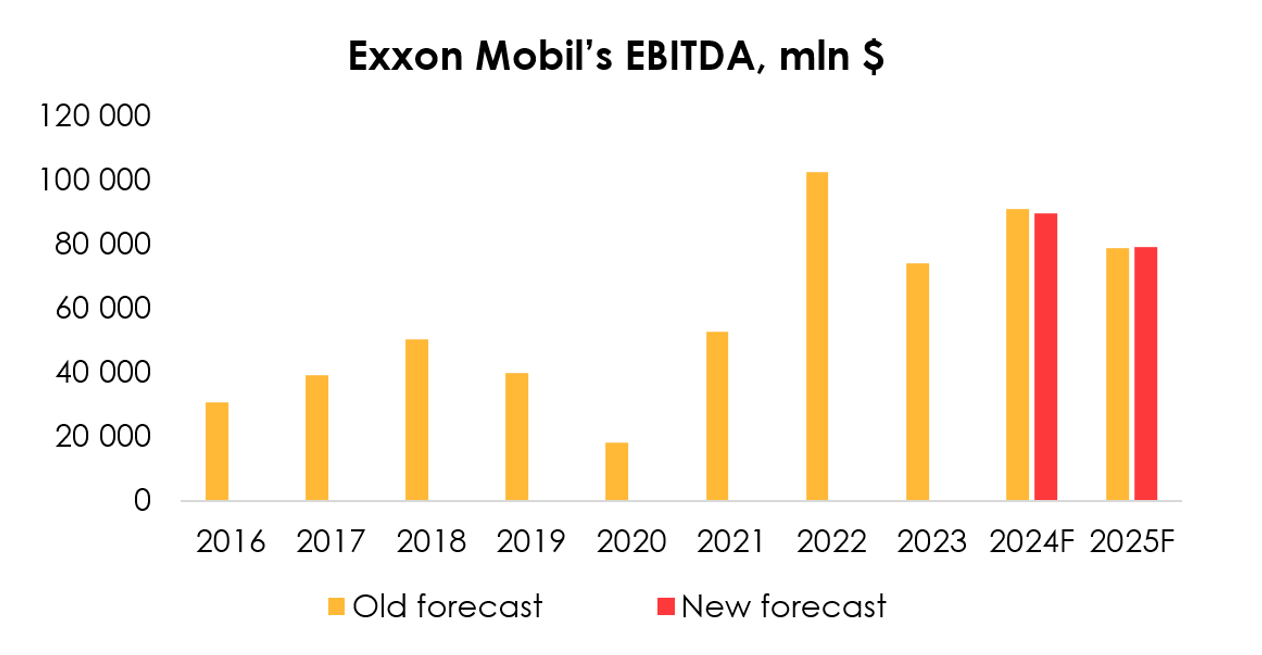

In 4Q 2023 the spread between the purchasing price of oil and oil products and the Brent oil price came down from the record high level of the prior quarter. We are maintaining the assumption that the spread will normalize by the end of 2024 and will hold within the current range until then, and we are cutting the forecast for Exxon Mobil’s gross costs from 55.7% of revenue to 54.1% for 2024, and from 56.1% of revenue to 55.2% for 2025.

Therefore, we are lowering the forecast for Exxon Mobil’s EBITDA from $91.2 bln (+23% y/y) to $89.6 bln (+21% y/y) for 2024, but are raising it from $78.8 bln (-14% y/y) to $79.2 bln (-13% y/y) for 2025 due to:

- the reduction of the forecast for Exxon Mobil’s revenue for 2024, and its increase for 2025;

- the reduction of the forecast for gross costs in 2024 and 2025.

Invest Heroes

Deal to buy Pioneer Natural Resources

The deal will tentatively close in 2Q 2024, meaning the two companies will consolidate their financial statements starting from 3Q 2024.

In our report for 3Q 2023 we have described in detail what benefits we expect to arise from the deal for both companies. Here are the highlights:

- Exxon Mobil is set to reduce oil and gas production costs, compared with the industry-average level, through technology and knowledge sharing with Pioneer Natural Resources.

- In what sets it aside from competition, XOM widely uses the cube development technique, and the acquisition of Pioneer, which has also fully moved to using this practice, is in line with Exxon Mobil’s well development strategy.

We expect that, once the deal is completed, it will boost Exxon Mobil’s capacity to produce oil and gas from 3891 kbpd on the oil-equivalent basis to 4635 kbpd in 2024, and from 3929 kbpd to 4674 kbpd in 2025, which is equivalent to a growth of 24% y/y and 1% y/y, respectively.

Invest Heroes

Therefore, by combining capabilities with Pioneer Natural Resources, Exxon Mobil will be able to produce more resources, while improving efficiency through technology sharing. A separate event will be held after the closing of the transaction to provide full details about the synergies.

Pro-forma financial results

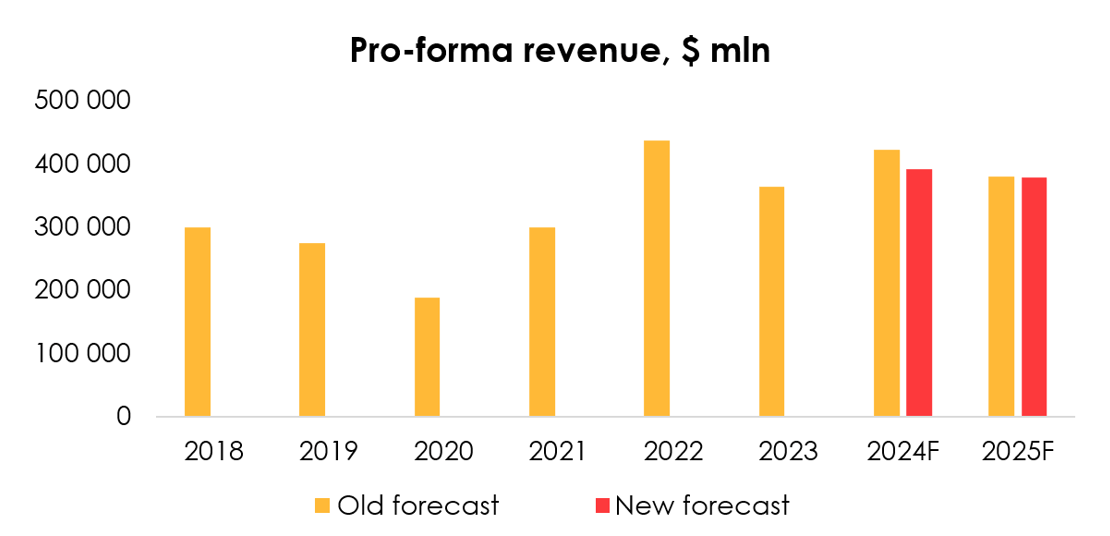

We anticipate that following the acquisition of Pioneer Natural Resources Exxon Mobil’s combined revenue will reach $391.9 bln (+8% y/y) in 2024, down from our earlier expectations of $422.9 bln (+16% y/y), and it will reach $378.2 bln (-3% y/y) in 2025, up from our earlier expectations of $379.9 bln (-10% y/y).

The lower forecast was largely driven by the delay with the completion of the deal with Pioneer, and cuts to the revenue forecasts for Exxon Mobil and Pioneer.

Invest Heroes

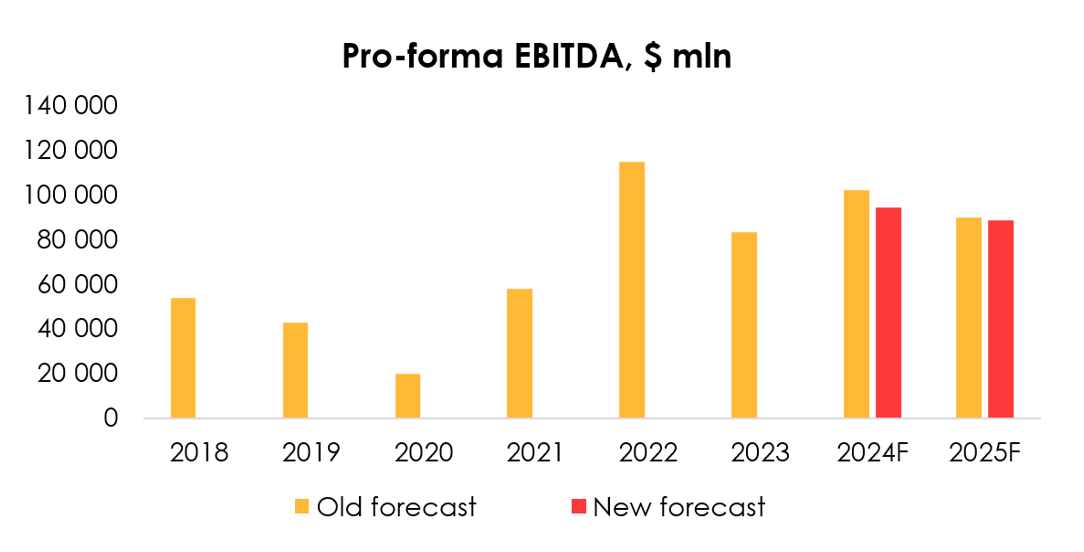

Consequently, the forecast for Exxon Mobil’s combined EBITDA was cut from $102.5 bln (+23% y/y) to $94.4 bln (+13% y/y) for 2024, and from $90 bln (-12% y/y) to $88.8 bln (-6% y/y) for 2025.

The lower pro-forma forecast is also attributable to reduced expectations for Exxon Mobil’s EBITDA, and to a smaller extent, for Pioneer’s.

Invest Heroes

Valuation

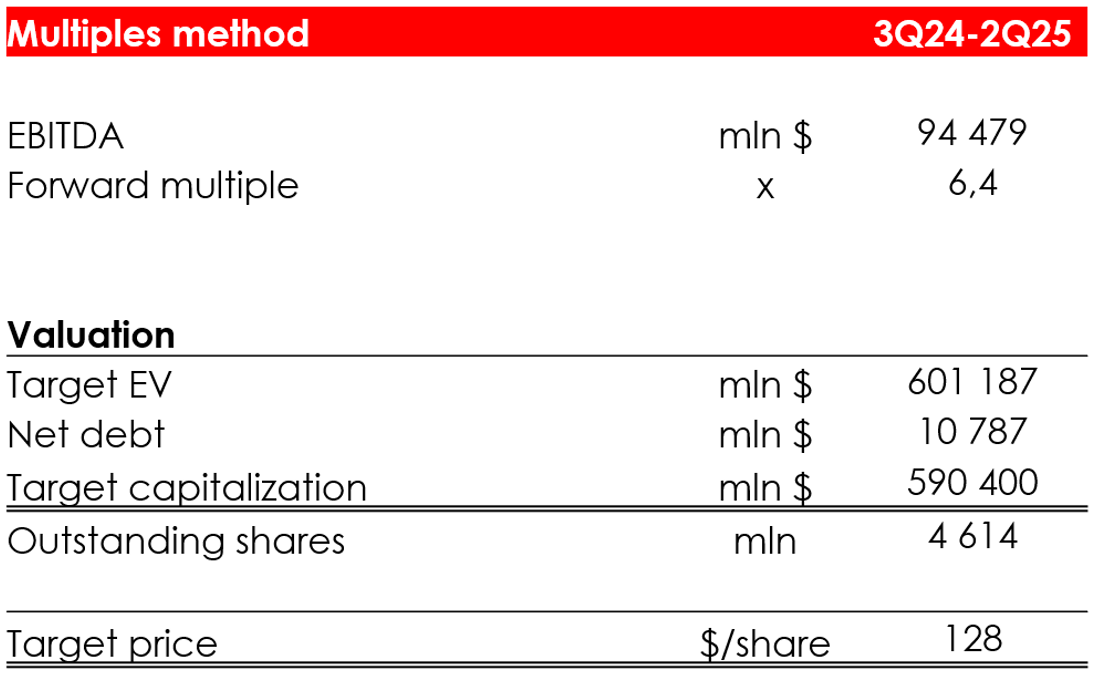

We are lowering the target price from $139 to $124 due to:

- the lower pro-forma EBITDA forecast for 2024;

- the shift of the forecast period to 3Q 2024 – 2Q 2025, the time when the deal with Pioneer Natural Resources will have been completed.

Based on the new assumptions, we are maintaining the rating for the shares at HOLD.

The price of $124/share was achieved by computing the target price based on the multiples method, and discounting it at the rate of 13% per annum.

Invest Heroes Invest Heroes

Conclusion

In line with the company’s portfolio diversification strategy, Exxon Mobil is actively pursuing M&A deals. The deal with Pioneer Natural Resources is expected to be closed in Q2 2024 and it will not only increase Exxon Mobil’s capacity to produce oil and gas, but also will reduce oil and gas production costs, compared with the industry-average level, through technology and knowledge sharing with Pioneer Natural Resources.

Based on the new assumptions for the oil balance market and the gas market, we assign a HOLD rating to the stock. To manage your positions, we recommend following the earnings releases of Exxon Mobil and Pioneer Natural Resources as well as the news related to the oil and gas market.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.