Summary:

- GoDaddy Inc. provides website hosting and related software services globally.

- The worldwide market for website hosting services is expected to reach $180 billion by 2027, driven by increasing demand for web presence and cloud-based business functionality.

- GoDaddy’s recent financial trends show slowing revenue growth.

- I’m Neutral [Hold] on GoDaddy Inc. stock in the near term.

metamorworks

A Quick Take On GoDaddy

GoDaddy Inc. (NYSE:GDDY) provides a variety of website hosting and related software services globally.

I previously wrote about GDDY with a Hold outlook.

While its U.S. payments business is a bright spot with substantial growth potential, total revenue growth is expected to slow.

The stock looks fully valued at its current valuation, so I remain Neutral [Hold] on GDDY for the near term.

GoDaddy Overview And Market

Arizona-based GoDaddy was founded to provide various website hosting services to organizations globally.

The company is led by Chief Executive Officer Aman Bhutani, who was previously President, Brand Expedia Group and Technology Senior Director at JP Morgan Chase.

The company’s main offerings include:

-

Website Hosting

-

SSL Certificates

-

Website Creation Software

-

Digital Marketing

-

Business Applications

-

Payments

-

Search Engine Optimization.

GDDY serves individuals, businesses of all sizes, developers and domain investors.

According to a 2020 market research report by Grand View Research, the worldwide market for website hosting services was an estimated $56.7 billion in 2019 and is expected to reach $180 billion by 2027.

This represents a forecast CAGR of 15.5% from 2020 to 2027.

The primary drivers for this expected growth are an increasing number of individuals and companies seeking a web presence and a growing desire to perform more business functionality in the cloud.

The onset of the COVID-19 pandemic generated strong growth in Internet-based activity, providing a boost to the industry which continues even after the waning of the pandemic.

Major competitive or other industry participants include:

-

Automattic

-

Wix

-

Weebly

-

Shopify

-

BigCommerce

-

Squarespace

-

MailChimp

-

MindBody

-

Others.

GoDaddy’s Recent Financial Trends

Total revenue by quarter has grown slowly after stronger growth during the global pandemic; Operating income by quarter has turned up recently, likely due to seasonal factors:

Seeking Alpha

Gross profit margin by quarter has remained within a narrow range; Selling and G&A expenses as a percentage of total revenue by quarter have trended slightly lower recently:

Seeking Alpha

Earnings per share (Diluted) have varied seasonally within a range, as the chart shows below:

Seeking Alpha

(All data in the above charts is GAAP.)

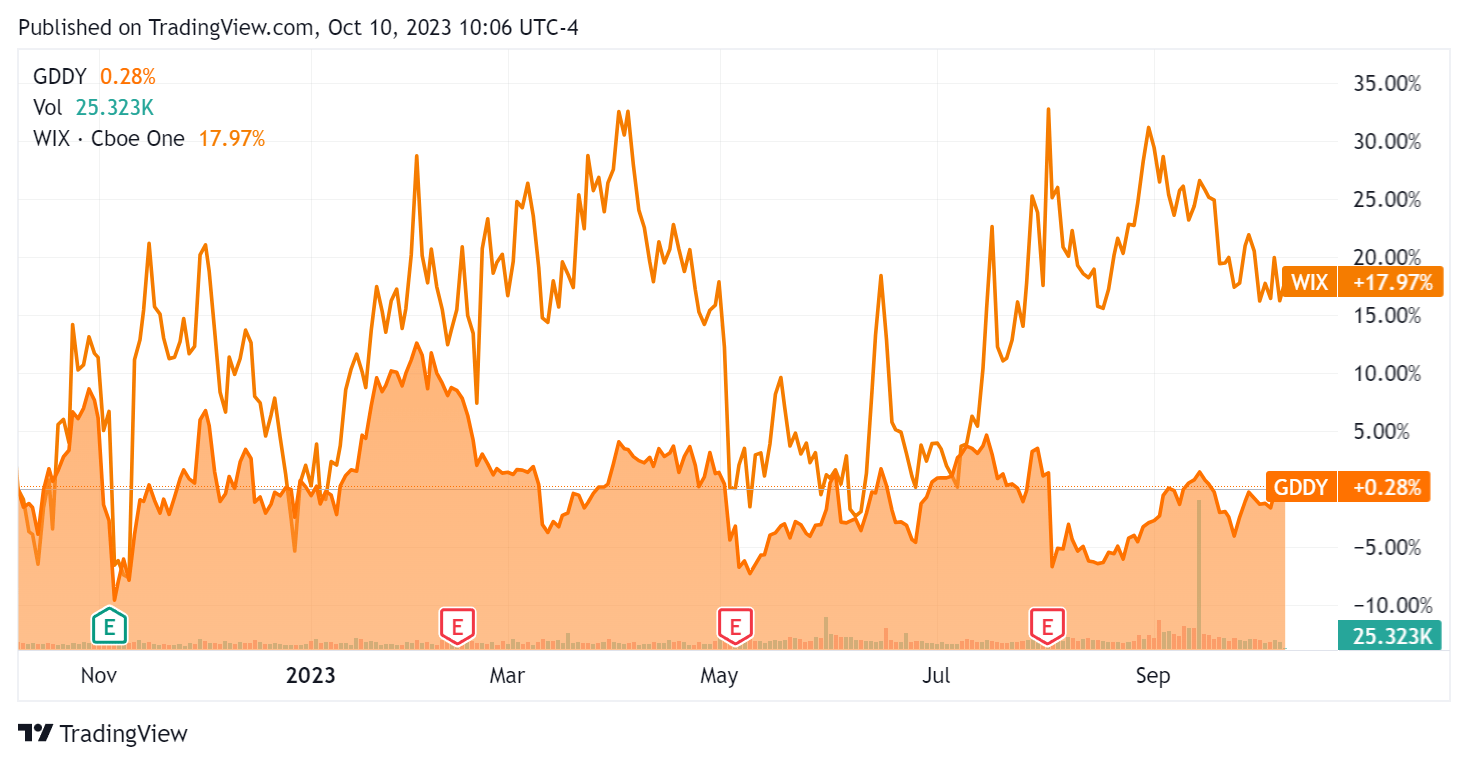

In the past 12 months, GDDY’s stock price has risen only 0.28% vs. that of Wix.com Ltd.’s (WIX) growth of 17.97%:

Seeking Alpha

For balance sheet results, the firm ended the quarter with $756.4 million in cash, equivalents and trading asset securities and $3.8 billion in total debt, of which $18.2 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $888.1 million, during which capital expenditures were $58.1 million. The company paid $287.9 million in stock-based compensation in the last four quarters, the highest trailing twelve-month figure in the past eleven quarters.

Valuation And Other Metrics For GoDaddy

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

3.4 |

|

Enterprise Value / EBITDA |

19.8 |

|

Price / Sales |

2.8 |

|

Revenue Growth Rate |

3.9% |

|

Net Income Margin |

7.8% |

|

EBITDA % |

17.1% |

|

Market Capitalization |

$10,940,000,000 |

|

Enterprise Value |

$14,130,000,000 |

|

Operating Cash Flow |

$946,200,000 |

|

Earnings Per Share (Fully Diluted) |

$2.07 |

|

Free Cash Flow Per Share |

$5.52 |

(Source – Seeking Alpha.)

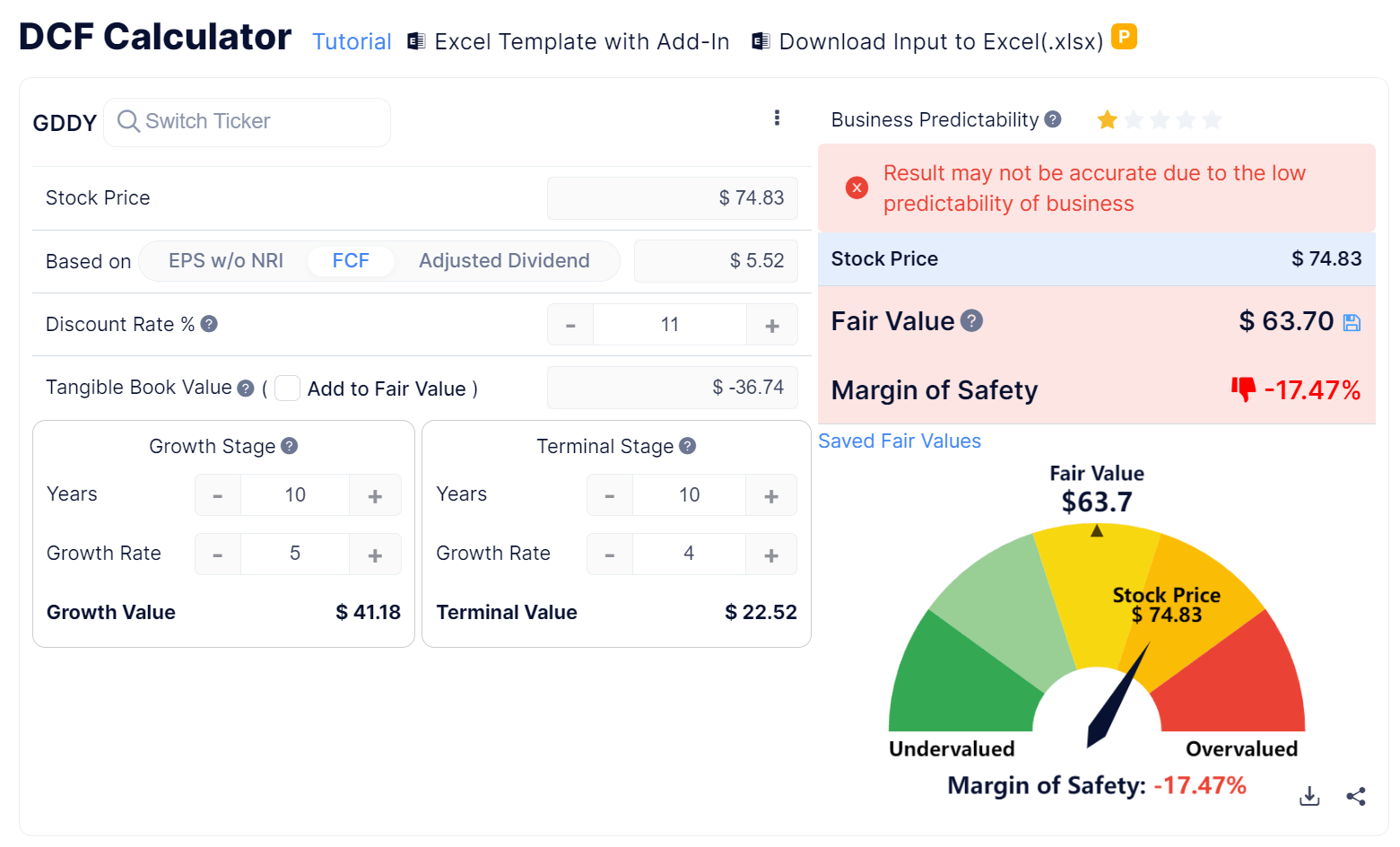

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and free cash flow:

GuruFocus

Based on the DCF, the firm’s shares would be valued at approximately $63.70 versus the current price of $74.83, indicating they are potentially currently overvalued.

Also, as a reference, a relevant partial public comparable would be Wix:

|

Metric [TTM] |

Wix |

GoDaddy |

Variance |

|

Enterprise Value / Sales |

3.4 |

3.4 |

-1.2% |

|

Enterprise Value / EBITDA |

NM |

19.8 |

–% |

|

Revenue Growth Rate |

9.3% |

3.9% |

-58.2% |

|

Net Income Margin |

-4.3% |

7.8% |

–% |

|

Operating Cash Flow |

$147,220,000 |

$946,200,000 |

542.7% |

(Source – Seeking Alpha.)

GDDY’s most recent unadjusted Rule of 40 calculation was 21.0% as of Q2 2023’s results, so the firm is in need of further improvement, per the table below:

|

Rule of 40 Performance (Unadjusted) |

Q1 2023 |

Q2 2023 |

|

Revenue Growth % |

5.3% |

3.9% |

|

EBITDA % |

17.4% |

17.1% |

|

Total |

22.7% |

21.0% |

(Source – Seeking Alpha.)

Sentiment Analysis

The chart below shows the frequency of certain keywords in management’s most recent conference call with analysts:

Seeking Alpha

The chart indicates a number of macroeconomic questions and headwinds the company has faced in business conditions and migration churn.

Analysts asked leadership about the drivers of core business growth, increasing expectations for its Applications & Commerce segment and EBITDA margin expansion ahead.

Management said that business growth will be driven by reductions in ForEx headwinds, migration churn and aftermarket comparisons to prior results.

For its Applications & Commerce segment, the company is seeing momentum with new customer payment bundled solutions and accelerating growth in GPV (Gross Payment Volume) from converting existing customers to its payment solutions.

EBITDA margin expansion is expected to come from improved marketing efficiencies, cloud migration efficiencies and benefits from its restructuring initiatives.

Commentary On GoDaddy

In its last earnings call (Source – Seeking Alpha), covering Q2 2023’s results, management’s prepared remarks highlighted the outperformance of its Applications & Commerce segment, with 7% YoY growth in gross revenue.

Private registrations grew by 3% but that was offset by a drop in domain aftermarket activity.

The firm is launching generative AI technologies to enable customers to quickly build websites and related functions without coding.

Also, management continues to focus on growing its payments segment, seeking to convert more of its 21 million customer base to this sticky offering set.

Total revenue for Q2 2023 rose 3.2% year-over-year, but gross profit margin fell by 1.6%.

The firm’s customer retention rate for GoDaddy-branded products was “above 85%,” which is only moderate. Many other software companies report higher customer retention figures.

Selling and G&A expenses as a percentage of revenue dropped by 1.4% YoY, and operating income slid by 2.1%.

The company’s financial position is relatively strong, with ample liquidity, substantial long-term debt and strong positive free cash flow.

GDDY’s Rule of 40 performance has been stable and in need of further improvement.

Looking ahead, consensus full-year 2023 revenue is expected to grow at 4.1% over 2022.

If achieved, this would represent a drop in revenue growth rate versus 2022’s growth rate of 7.2% over 2021.

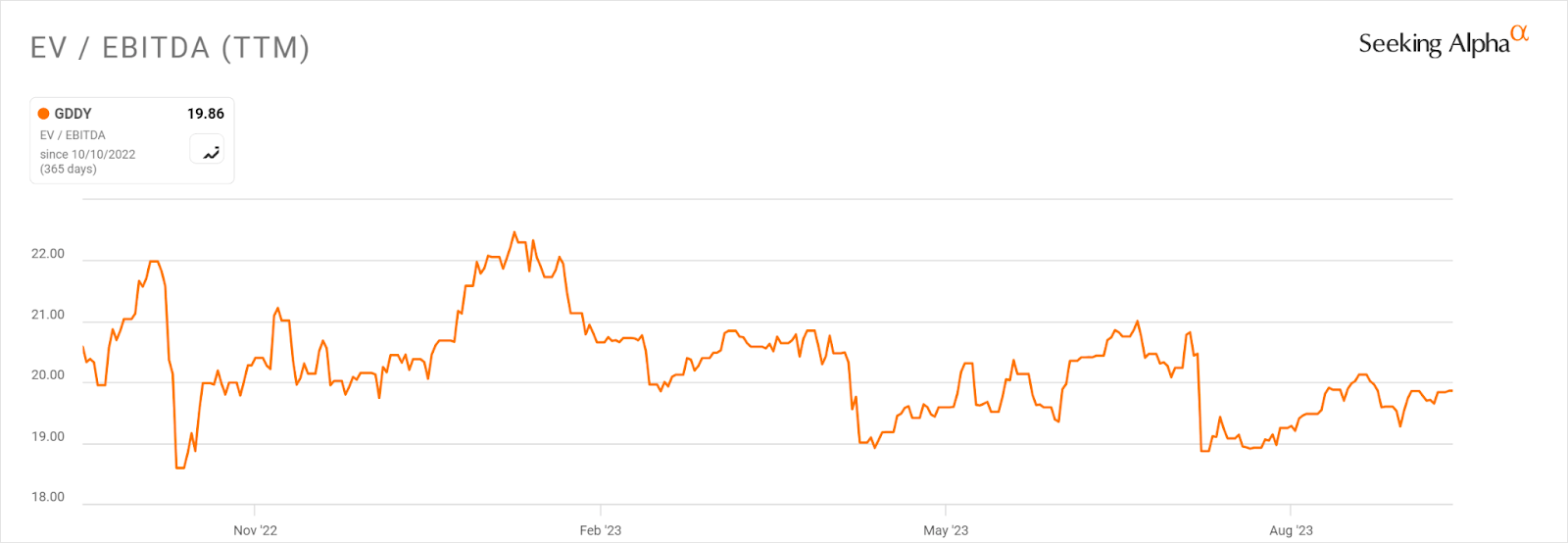

In the past twelve months, the firm’s EV/EBITDA valuation multiple has fallen 3.5%, as the chart from Seeking Alpha shows below:

Seeking Alpha

A potential upside catalyst to the stock could include improved payments uptake by customers and benefits from the firm’s restructuring efforts.

While management may “feel good about expanding” margins and increasing its growth rate, some of that growth rate increase is from getting over previous comparables and expected FX headwinds dying down.

These trends are likely not robust growth drivers indicating strong future performance.

Moreover, based on expected free cash flow, my discounted cash flow calculation suggests that GDDY is trading at full value when compared to its discounted cash flow value.

Accordingly, I remain Neutral [Hold] on GDDY for the near term.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Consider becoming a member of IPO Edge.

Gain Insight and actionable information on U.S. IPOs with IPO Edge research.

Members of IPO Edge get the latest IPO research, news, and industry analysis. Get started with a free trial!