Summary:

- Several key catalysts have been evolving around Alphabet Inc./Google since its Q3 earnings report.

- Positive catalysts include advancements in AI, quantum computing chips, and aggressive share repurchase programs.

- Negatives include the potential to divest Chrome and unbundle Android from other Google services.

- My assessment is the positives outweigh the negatives.

- I see good odds for the GOOGL market cap to surpass $3 trillion in 2 years or so.

RichVintage

GOOG stock: Previous thesis and new catalysts

I last analyzed Alphabet Inc. aka Google (NASDAQ:GOOG), (NASDAQ:GOOGL) on October 25, 2024. My last article, titled “Google Q3 Preview: Buy And Forget At $165,” provided a preview of its Q3 earnings. As the title has already given away, the article argued for a buy thesis ahead of the earnings report (ER) when the stock was trading around $165. My buy rating was based on the following considerations:

Despite competition, rising demand for large language models positions Google well for growth, with Q3 earnings likely to surprise positively. Google’s valuation is attractive, trading at a P/E ratio of 23.58x, significantly below its historical average and the broader market. Given its sizable net cash position, its P/E is even lower than on the surface. The combination of its compressed valuation and the potential for a Q3 surprise could trigger a large price surge.

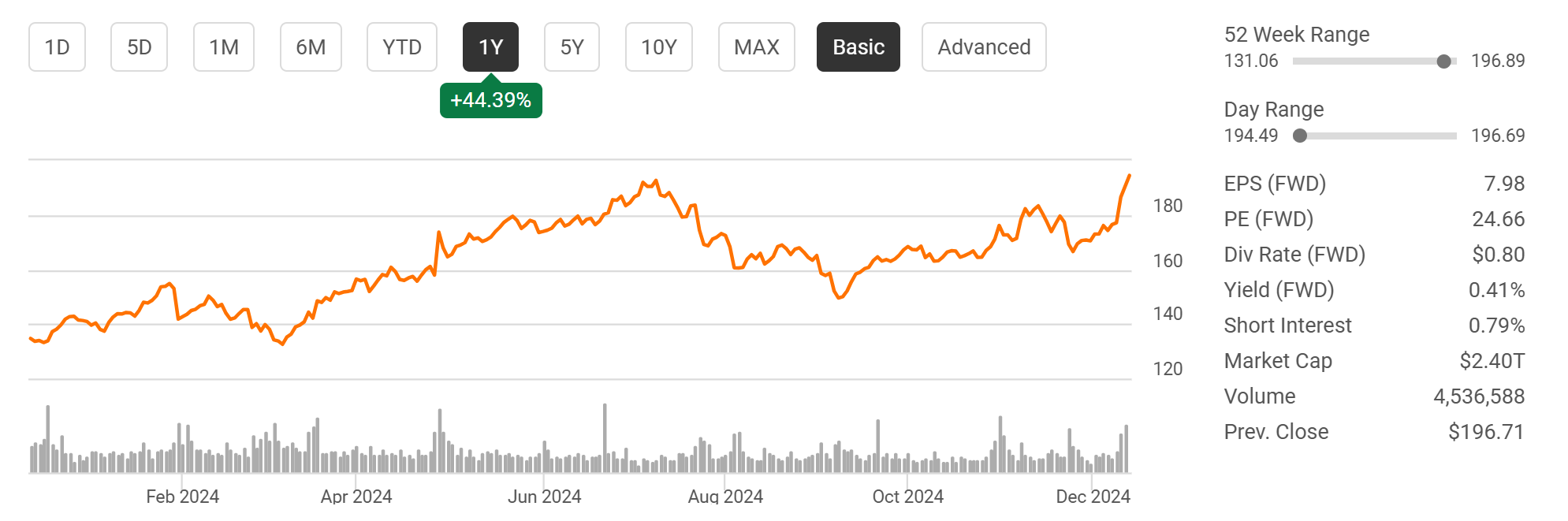

Since then, there have been a few new catalysts surrounding GOOG, and it is the goal of this article to reexamine the impacts of these catalysts on the stock. To keep the article focused and within a reasonable length, I will limit myself to the top 3 catalysts in my assessment: the updates provided in its Q3 report, the latest advancements with its quantum computing chips, and also its shareholder return programs. My conclusion from this assessment is that GOOG is still undervalued at its current P/E (of around 25x) and market capitalization of $2.4 trillion, as illustrated by the chart below. I expect the company to reach $3 trillion market capitalization in a year or two, and thus reiterate my buy rating despite the large price rally since my last writing.

Seeking Alpha

GOOG stock: Q3 earnings recap

Let me start with a recap of its Q3 earnings. As I argued in my preview article, GOOG Q3, reported on October 29th, 2024, indeed delivered a strong performance. To wit, the company reported Normalized EPS of $2.12, exceeding analysts’ estimates by $0.27. GAAP EPS also came in at $2.12, also beating expectations by the same amount. Revenue for the quarter reached $88.27 billion, surpassing estimates by $2.05 billion. Notably, its cloud revenue surged 35% YOY in Q3. In the next section, I will explain why I expect such momentum to sustain or even further accelerate going forward.

Looking ahead to the upcoming quarter, analysts expect GOOG to maintain its strong performance. The consensus estimate for Normalized EPS is $2.12, while the GAAP EPS estimate stands at $2.11. Revenue is projected to reach $96.62 billion, translating into a QoQ growth rate of almost 10%. Finally, note that the prevailing market sentiment is quite bullish, as reflected in the recent earnings revisions. Over the past 90 days, there have been 32 upward revisions to GOOG’s EPS estimates and only 5 downward revisions. I strongly agree with such a positive outlook for several fundamental reasons, as elaborated immediately below.

Seeking Alpha

GOOG’s on an accelerated path to $3T market capitalization

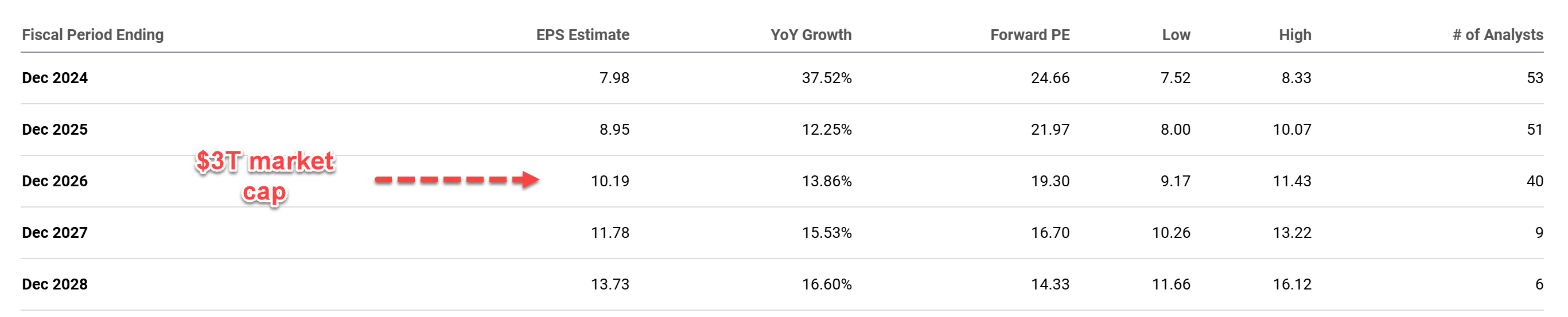

Let me start with a more global view before diving into the specific catalysts. The next table displays the consensus EPS estimates for GOOG in the upcoming years. As seen, the expectation is for its EPS to grow at double-digit rates over the coming years. In particular, these estimates point to an EPS of $10.19 by FY 2026. Assuming its current P/E multiple and share counts, GOOG’s market cap will reach/surpass the $3 trillion mark by then. With this broader view, I will next detail the catalysts that can accelerate its path to a $3T market cap.

Seeking Alpha

The immediate catalyst is the rapid growth of its cloud, as mentioned above. A key driver for the rapid growth in recent quarters involves GOOG’s AI solutions. I am impressed by the progress GOOG has made on the AI front and by the performance of its AI products after trying them out myself. Notably, since the release of its Q3 ER, GOOG has recently released its Gemini 2.0 Flash AI model in an experimental stage. According to GOOG, Gemini 2.0 can “tackle more complex topics and multistep questions, including advanced math equations, multimodal queries and coding.”

In the mid-term, the real game changer – a term I don’t use liberally and reserve only for a few technologies – in my view is its quantum computing chip (code-named Willow). The results (quoted below) that GOOG published in Nature are highly encouraging. My view is that these results pave the way for practical deployment, which would fundamentally change the landscape of high-performance computing, including AI applications.

The chip is capable of handling complex calculations in a span of five minutes, while the world’s most powerful supercomputers would need 10 septillion years. “Our results present device performance that, if scaled, could realize the operational requirements of large-scale fault-tolerant quantum algorithms,” Google researchers wrote in the study’s abstract.

Other risks and final thoughts

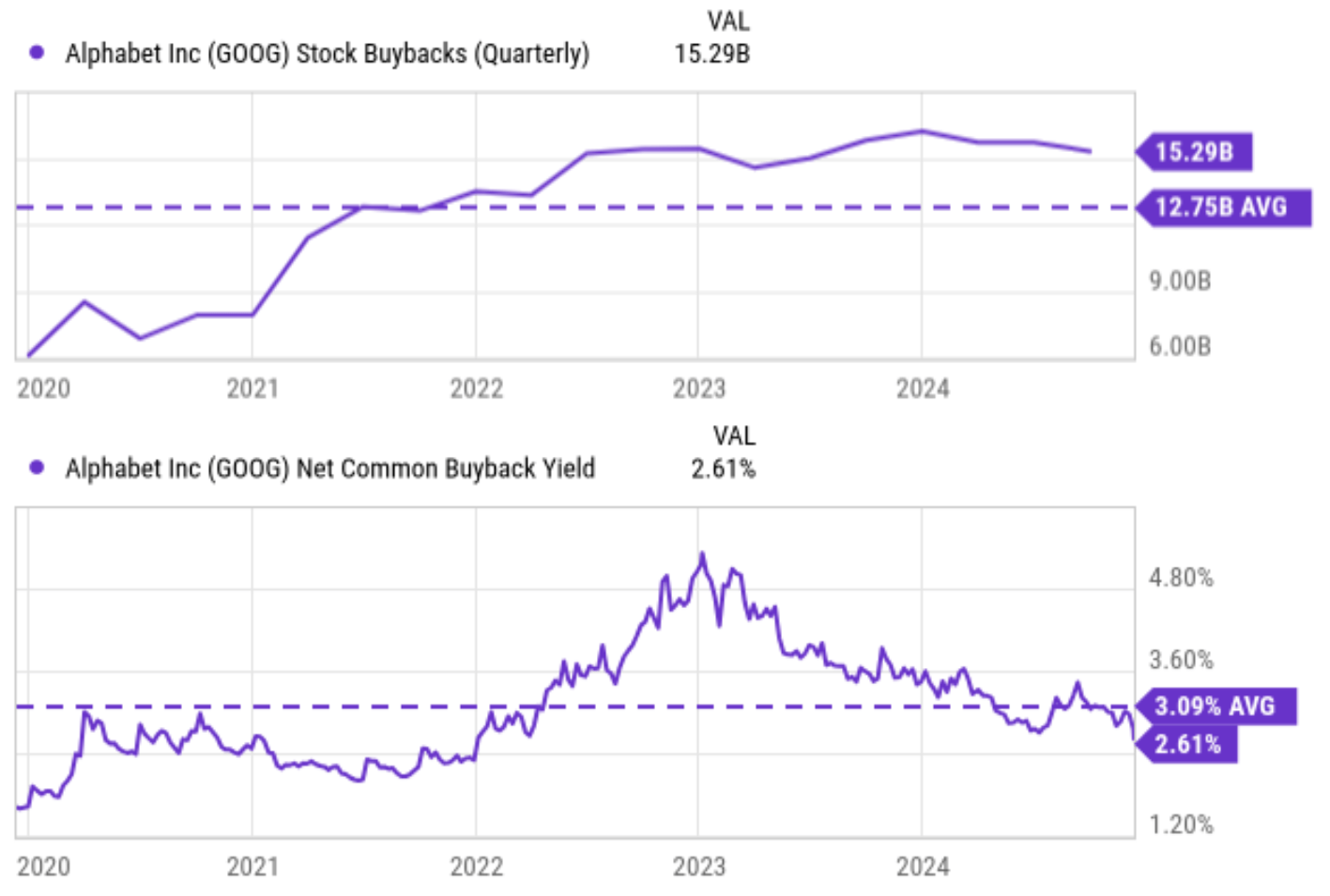

Another factor that can accelerate GOOG’s path to $3T market cap is its aggressive share repurchase program. As seen in the chart below, GOOG has been spending on average over $12.75 billion per quarter on share repurchases in the past 5 years, and the pace has accelerated recently. In the past quarter, it spent $15.29 billion on share repurchases. If you agree with my above assessment that the company’s current P/E represents a discount given the growth catalysts afoot, then the buybacks under current valuations would accelerate its EPS growth and help it reach a $3T market cap sooner.

Finally, the share buyback program is also a key mechanism the company uses to return capital to shareholders, as illustrated by the second chart below (which is a screenshot of its Q3 cash flow statement). GOOG has demonstrated a strong commitment to returning capital to shareholders through all the usual channels: debt reduction, share repurchases, and also dividends (which were initiated in the June quarter). The share repurchases are by far the largest component of the shareholder return. On average, the net common buyback yield is about 3.1% in the past 5 years, far higher than the dividend yields of many dividend-paying stocks.

Seeking Alpha Seeking Alpha

In terms of downside risks, regulatory risks, especially antitrust concerns, are the top risk in my view. In August, Google lost its antitrust case with the U.S. government. As part of the decision, a U.S. District Court judge referred to Google as a monopolist and ruled that Google maintained a monopoly in two product markets, general search services and general text advertising. Google plans to appeal the decision, but the appeals process could take years. Then in October, the U.S. Justice Department (DOJ) released potential remedies for the case. The U.S. DOJ submitted its final proposed remedy in late Nov and the key components are quoted below (with emphasis added by me):

The divestiture of Google’s Chrome browser directly disrupts Google’s ability to use its browser dominance to push users towards its own services. Unbundling Android from Google products, or divesting it completely either voluntarily or in the event of noncompliance, creates opportunities for other app stores or services to compete more fairly.

Google is expected to respond by December 20 and the outcome of this case is still uncertain can could have a substantial impact on GOOG’s future.

Despite these uncertainties, I am seeing a skewed reward/risk curve here. In a nutshell, I am seeing too many positive catalysts to outweigh the negatives. The top catalysts analyzed in this article include the latest advancements in its AI products, quantum computing chips, and also its share repurchase programs. Finally, a full disclosure, I don’t directly own GOOG shares. I have established a sizable position in XLC (The Communication Services Select Sector SPDR ETF Fund) recently to gain targeted exposure to GOOG and a few other companies in the sector that I am bullish on. XLC provides concentrated (which is our preferred style) exposure to GOOG (about 20%), META (about 20%), and a few other key players in the communication services sector. XLC’s top 10 holdings represent more than 73% of its assets. We have a good understanding of all of them (and have written in-depth analyses on most of them) and feel bullish about them. It is just easier for us to own XLC than a couple of individual stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of XLC either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.