Summary:

- Alphabet collapsed around 42% from its all-time-high marked on February 2, 2022 during the ongoing bear market.

- While it could be tempting to buy considering the share price decline, my two fair value calculations indicate at most a fair valuation without a margin of safety.

- Additionally, both from a technical and a macroeconomic point of view, further downward pressure seems highly likely.

Justin Sullivan

1. Introduction

We are in the midst of a bear market and Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) collapsed around 42% from its all-time high of $151.55 on February 2, 2022.

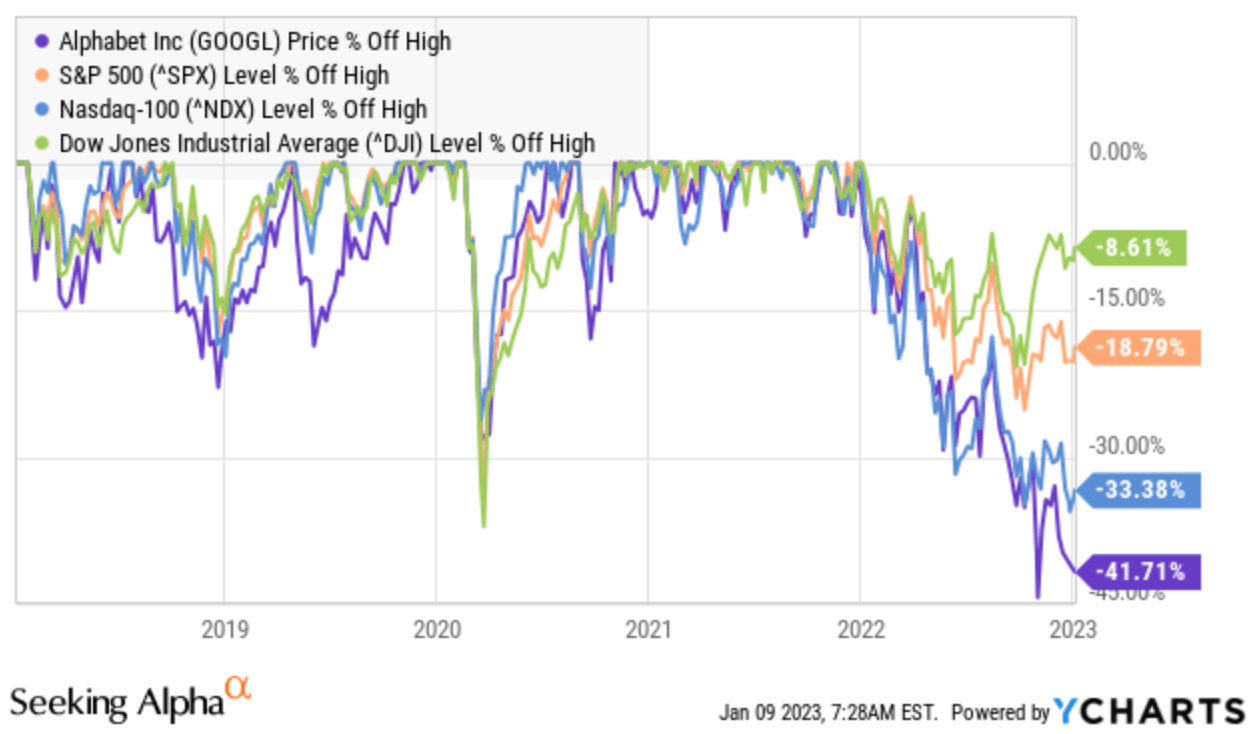

Consequently, Alphabet has underperformed all the major indices, such as the S&P 500, Dow Jones as well as the Nasdaq (see chart).

Price % off high – Alphabet vs indices (YCharts)

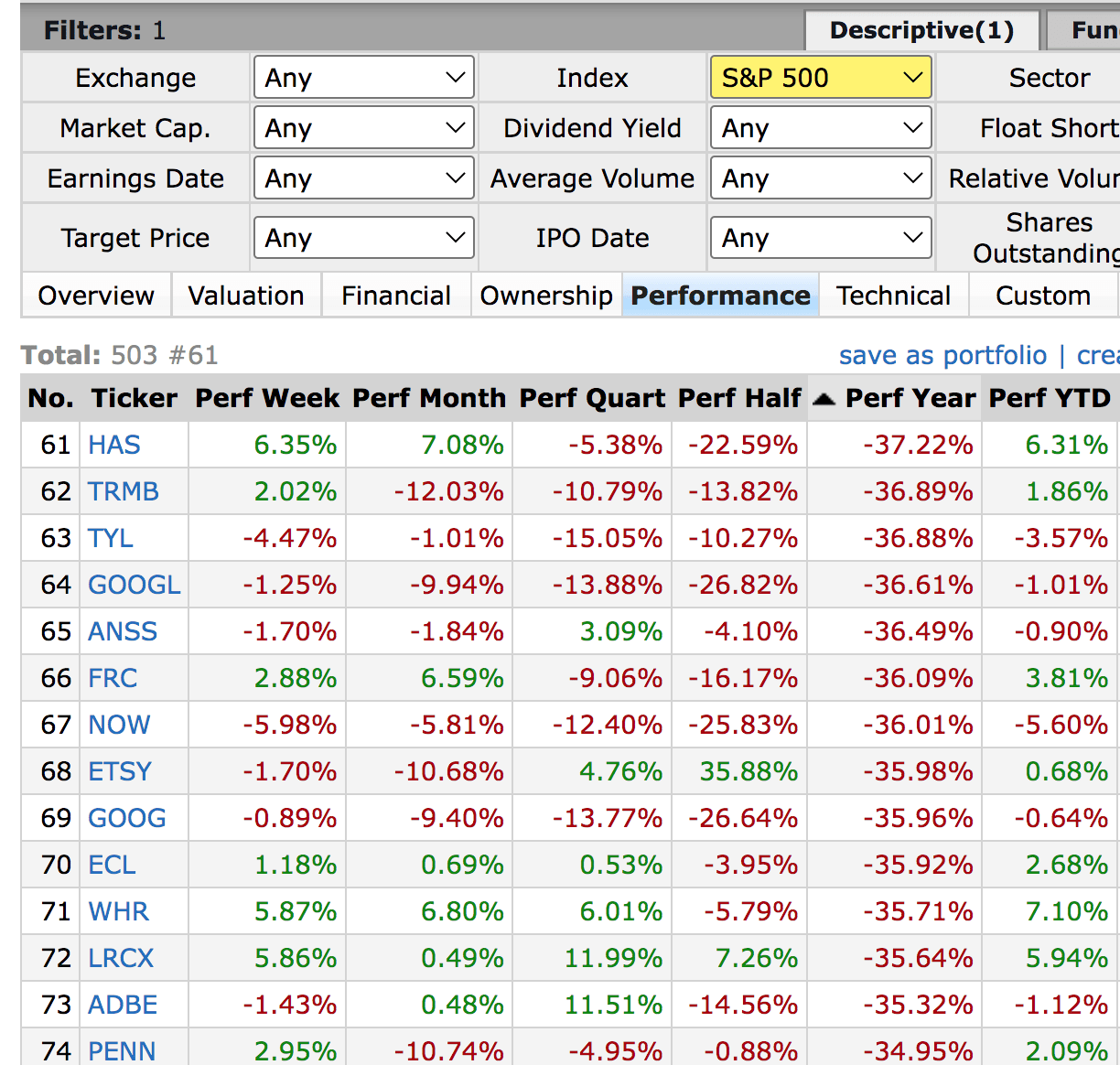

Compared with the S&P 500 stocks, Alphabet is one of the worst performers over a 12-month period with a decline of 37% (see chart).

Performance of Dow Jones stocks (Finviz)

So, is now a good opportunity to buy Alphabet?

2. Fair Value Calculation

I prepared two valuation models in order to make a more accurate assessment of the valuation. I have chosen a conservative approach due to the monetary tightening phase of central banks on a global scale and the related rapidly rising interest rate environment. Other factors favoring a conservative approach include the uncertain macroeconomic and political environment and rising recession risks, which have probably not yet been fully priced in.

Furthermore, the advertising business, where Alphabet generates the bulk of its revenues, is cyclical and therefore vulnerable to economic cycles

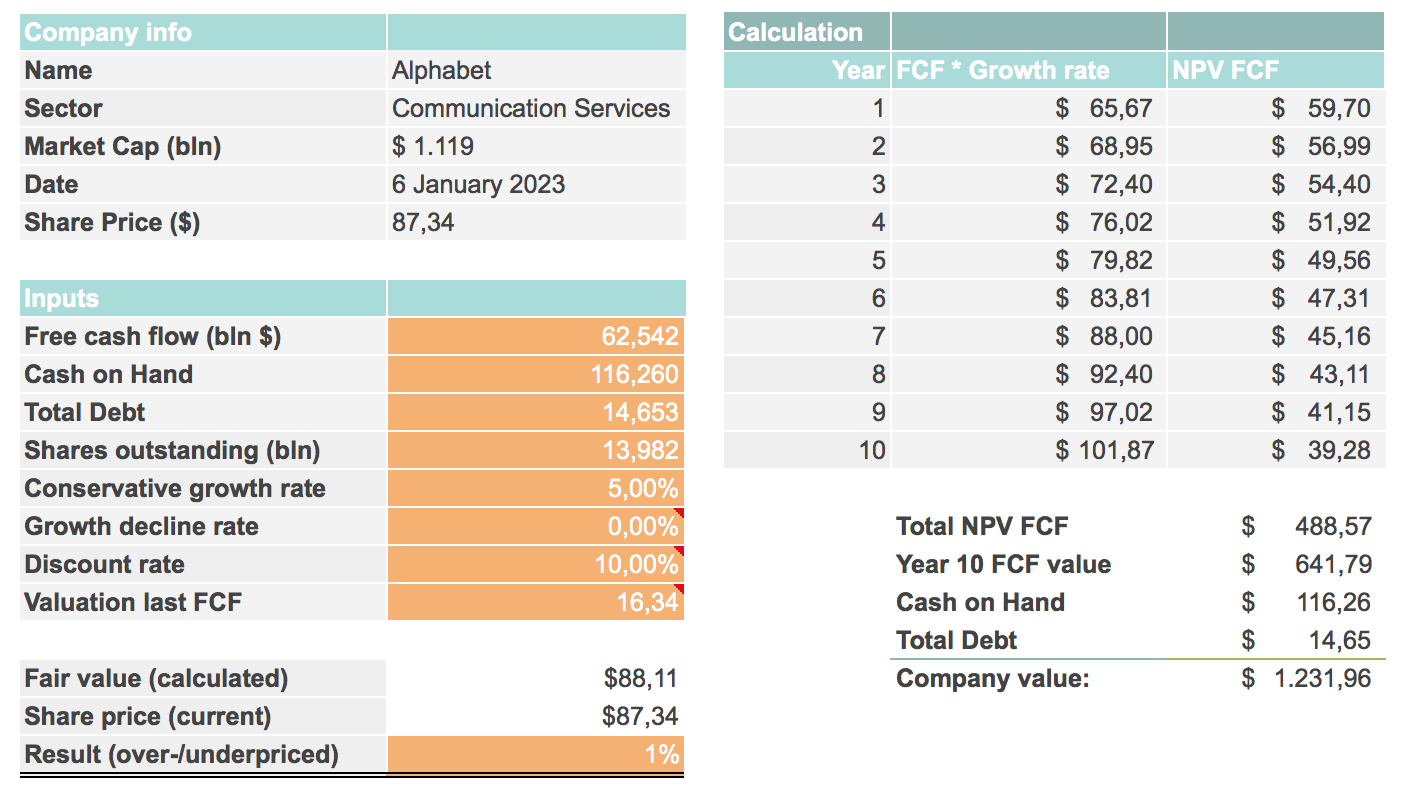

The first valuation method is based on a DCF calculation. In order to choose a conservative approach, I have chosen a growth rate of 5% per year in terms of the free cash flow. Additionally, analysts’ consensus predict FCF decline of 5% in FY 2022 before there is a significant increase in the FCF again in the following years, according to MarketScreener. In terms of Price/Cash flow multiple, I have chosen a multiple of 16.34 for the last FCF, which represents the 4-year average of the years 2014-2017 and is slightly below that of the current 5-year valuation of 18.72 (2018-2022), according to Morningstar.

In the first valuation method based on a DCF calculation, the fair value is $88.11, which corresponds to a current fair valuation of the stock (see figure below).

Alphabet fair value calculation based on DCF (Author’s calculation)

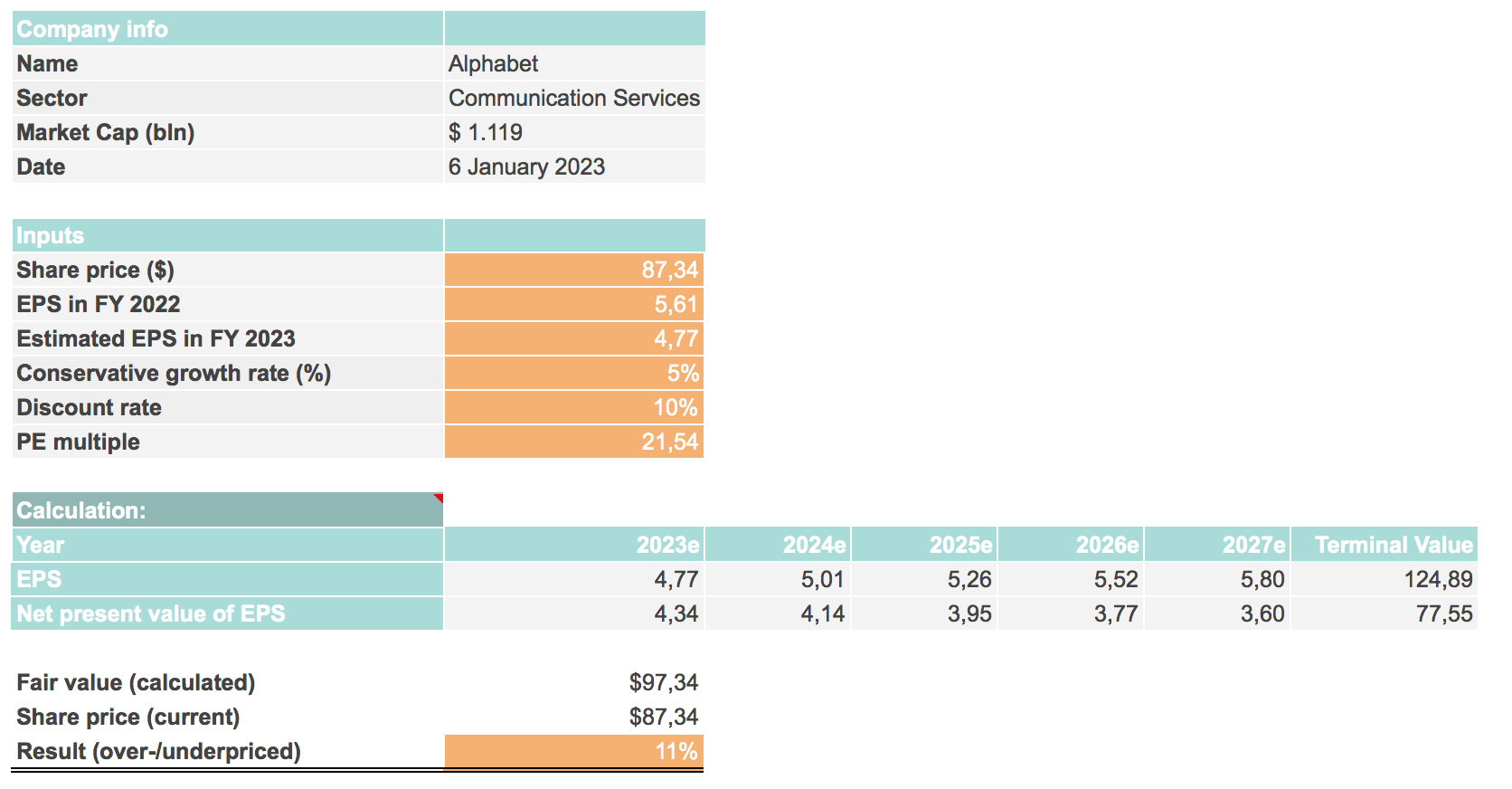

The second valuation method is based on an earnings-per-share calculation. In order to choose a conservative approach, I have chosen a growth rate of 5% per year in terms of EPS growth. The 5-year average EPS growth rate was 32.14, according to Morningstar. Nevertheless, analysts’ consensus predict EPS drop of 15% in FY 2022 before there is a significant increase in the EPS again in the following years, according to MarketScreener.

In terms of P/E multiple, I have chosen a multiple of 21.54 for calculating the terminal value, which represents the 4-year average of the years 2013-2017 and is well below the current 5-year valuation of 31.73.2 (2018-2022) but close to the average S&P 500 valuation (19.23), according to Morningstar.

In the second valuation method the fair value is $97.34, which corresponds to a slight undervaluation of the stock of 11% and thus close to a fair valuation (see figure below).

Alphabet fair value calculation based on EPS (Author’s calculation)

3. Technical Analysis

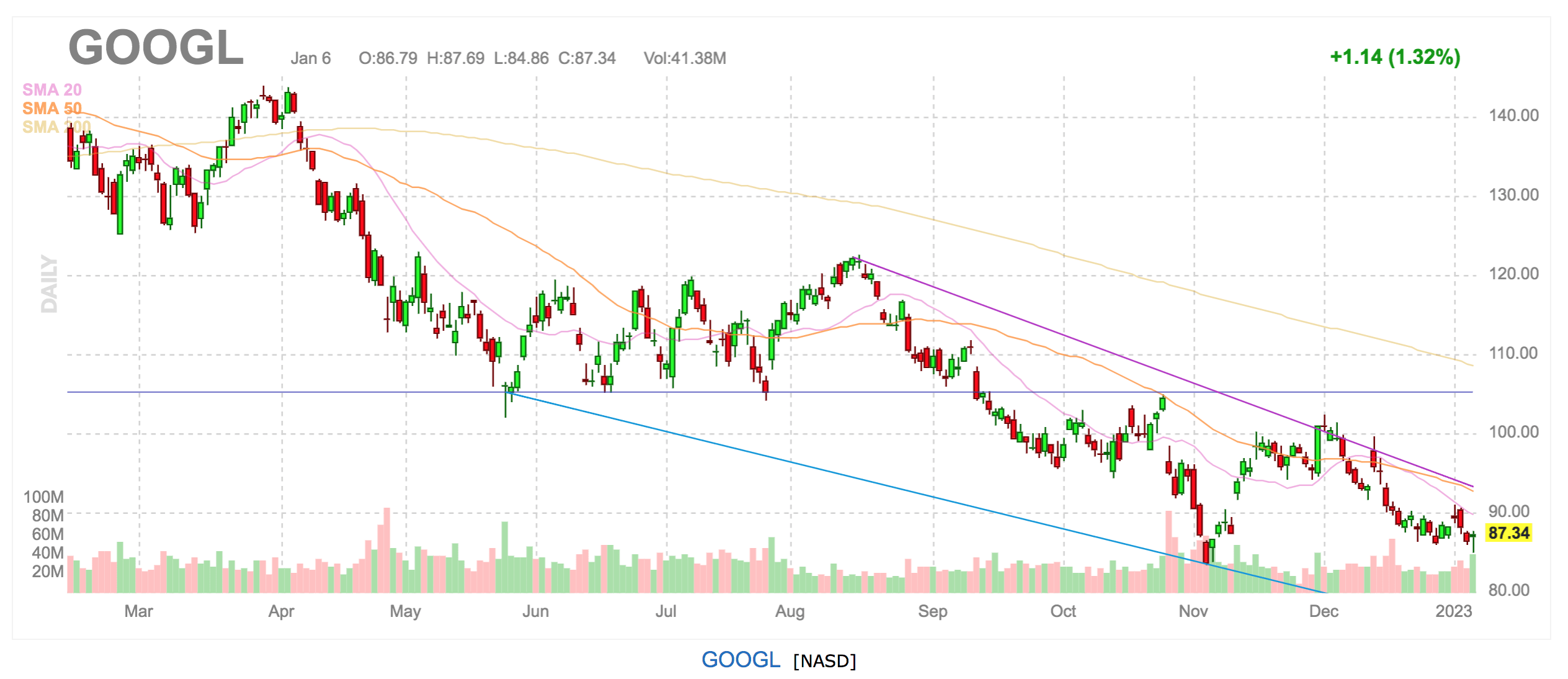

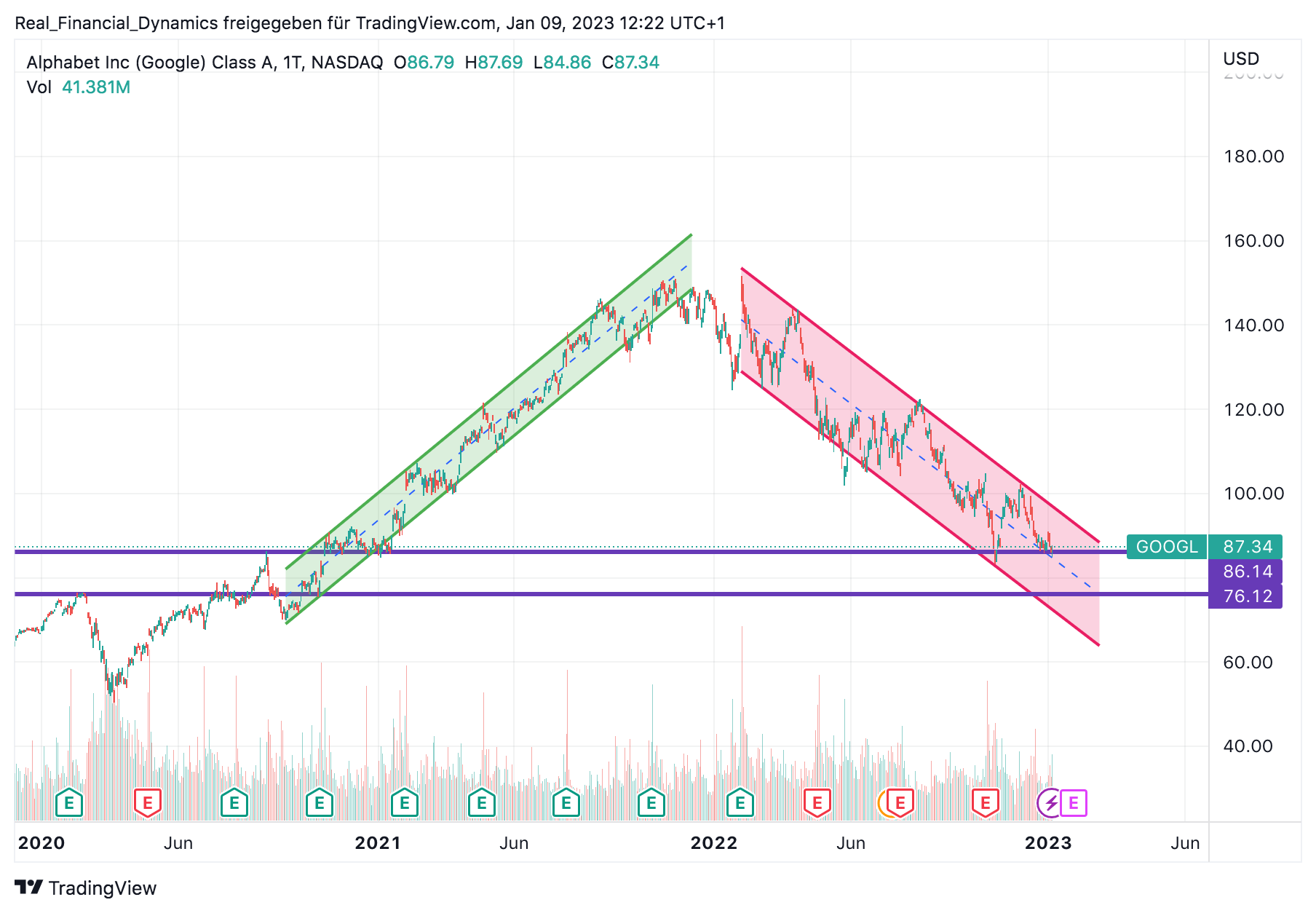

Looking at the chart, it is striking that Alphabet is caught in a downtrend and marks one 52-week-low after another, which favors a further decline in the share price (see following chart).

Alphabet chart – stuck in a downtrend (Finviz)

Consequently, Alphabet could either bounce at around $86, which could act as a short term support or – the currently more likely scenario considering the strong down trend – fall to around $76, which could act as a support line, before a meaningful upward reaction could occur (see following chart).

Alphabet chart – caught in a downtrend (TradingView)

4. Conclusion

It appears highly likely that Alphabet will continue to fall, both from a fundamental and a technical point of view.

While Alphabet is a fundamentally and financially very solid company with a cash hoard of over $100 billion, my fair value calculation based on a DCF method shows a current fair valuation of the stock and my fair value calculation based on an EPS method indicates a slight undervaluation of just 11%, leaving no margin of safety.

From a fundamental point of view, there are additional weighing factors, such as a potential threat to Alphabet’s search engine Google by Microsoft’s investment in ChatGPT and Alphabet’s highly cyclical ad revenues.

From a technical point of view, Alphabet is exposed to further downward pressure, unless the macroeconomic environment and the central banks’ rapid monetary tightening loosen up. This in fact would lead to an update of the fair value and the assumptions behind it.

The technical analysis favors a fall to around $76, which would mean that the Post-COVID gains, resulting from the unprecedented monetary supply by central banks and governments, would vanish with it.

In summary, investors seem better advised to be patient and wait for the environment and the stock to stabilize for better entry-level conditions.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.