Summary:

- Home Depot is set to release its Q1 earnings next Tuesday.

- While the delayed start of the spring selling season is a concern, I expect the company to maintain its guidance.

- The long-term market share gain story is attractive and the company’s investor conference in June can be a positive catalyst.

jetcityimage

Home Depot (NYSE:HD) is scheduled to release its Q1 earnings before the market opens on Tuesday, May 16, 2023. Although the company does not provide quarterly guidance, it has guided that it expects flat comp sales for the full year and a mid-single-digit decline in EPS.

When examining Home Depot, there are two contrasting narratives. On one hand, demand is returning to normal levels after a couple of exceptionally strong years, and macroeconomic conditions are challenging due to high inflation, which puts pressure on consumers.

On the other hand, Home Depot has a strong track record of execution and has been gaining market share. The company has made strategic investments in various initiatives over the past few years, and these investments are starting to yield positive results.

In a previous article, I discussed how Home Depot’s investments in flatbed distribution centers, direct fulfillment centers, and market delivery operations for large and bulky goods are aiding the company in capturing market share among its larger professional (PRO) customers. Below is the relevant excerpt:

Previously, while the company had a good presence among the smaller professional customers, larger professionals mainly relied on Home Depot as a backup (not for planned purchases) due to the company’s inefficient delivery system for them. In recent years, the company has optimized its logistics system and invested in flatbed distribution centers, direct fulfillment centers, and market delivery operations for big and bulky goods like appliances. The company now has the capability to deliver large quantities of materials directly to the job site which should help it gain market share in the large PRO space from regional independents and nationwide building material suppliers.”

These investments in delivery operations also have improved Home Depot’s overall delivery speed and efficiency. Customers can now shop from a larger inventory and receive faster delivery directly from distribution centers, rather than relying solely on in-store availability. Consequently, store associates are relieved of additional responsibilities, such as dispatching, allowing them to focus more on providing a better in-store experience for customers.

Additionally, Home Depot’s acquisition of HD Supply in recent years has expanded its opportunities in the maintenance, repair, and operations – MRO – market within the PRO space. Previously, the company’s MRO-related business primarily focused on multifamily housing, but the acquisition of HD Supply opened up new verticals, including hospitality, healthcare, government, and university dorms.

So, there’s a good secular market share gain story for Home Depot.

In the previous quarter’s management commentary, Home Depot anticipated a low single-digit decline in end-markets for the year, which it aimed to offset through market share gains resulting from the aforementioned initiatives. So, management was expecting flat comp sales and total sales for the full year.

While Home Depot does not provide quarterly guidance, it’s expected that the benefits from these initiatives will continue to ramp up as the year progresses. Additionally, as the company faces easier year-over-year comparisons in the second half of the year (as it started to experience the impact of a consumer slowdown in the latter half of the previous fiscal year), the second half should show improvement compared to the first. Therefore, it’s reasonable to anticipate a year-over-year decline in sales for the first two quarters, followed by some improvement in the third and fourth quarters.

The sell-side analysts are currently expecting a -1.26% year-over-year decline in Home Depot’s Q1 sales. However, personally, I’m more conservative and believe that the company could experience an even worse decline. Besides challenging macroeconomic conditions, I see two additional factors that could impact Home Depot’s Q1 sales negatively.

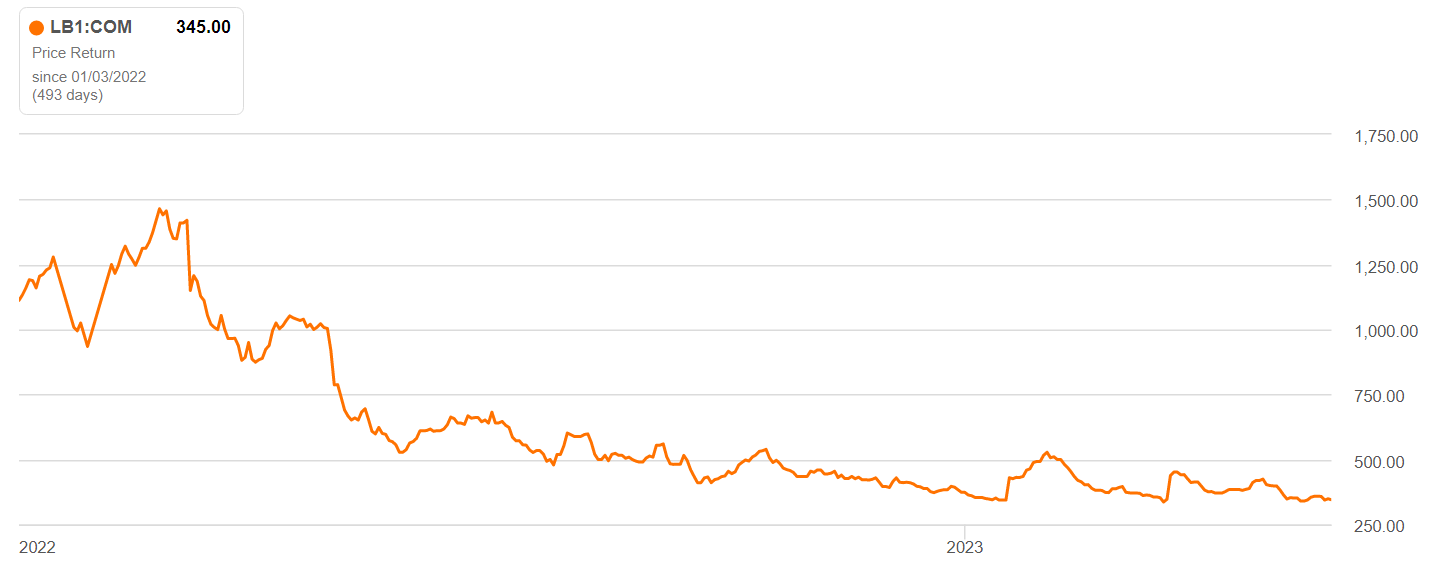

Firstly, lumber prices (LB1:COM) have undergone a significant correction since early 2022. This correction in prices may have an adverse effect on the company’s comparable sales in the first and second quarters, as the average selling prices of products containing lumber have decreased meaningfully Y/Y.

Lumber Future Price (Seeking Alpha)

Secondly, this year’s spring selling season has experienced a delayed start. Tractor Supply (TSCO) recently reported lower-than-expected earnings, attributing the miss to the delayed onset of the spring season. Home Depot may face a similar impact.

Therefore, Home Depot may encounter additional headwinds in Q1. However, I anticipate that management will maintain guidance, considering it’s just one quarter in the year, and some of the sales lost in Q1 due to the delayed spring season may shift to Q2.

Regarding operating margins, management already has taken a conservative approach and provided guidance for an operating margin of 14.5% in the current year, compared to approximately 15.3% in the previous fiscal year. I find this guidance conservative enough, and given the company’s track record of effective execution and the easing of supply chain challenges, I do not anticipate significant changes in that regard.

Even if the company slightly misses sales expectations in the current quarter, as long as it maintains its guidance, I do not expect a significantly negative response from investors. Long-term investors are eagerly awaiting the company’s investor conference on June 13, during which Home Depot is likely to highlight its initiatives to gain market share. The company has previously stated its target of achieving $200 billion in annual sales, a substantial increase from the current levels (with expected sales of ~$156.7 billion in the current fiscal year). Investors are seeking more visibility regarding the timeline and drivers behind this growth, which could be a key event to watch for.

Home Depot is currently trading at a price-to-earnings (P/E) ratio of 18.27x based on consensus EPS estimates for the current fiscal year and 17.23x based on consensus estimates for the next fiscal year. This represents a significant discount compared to its five-year average forward P/E ratio of 21.21x. Although investors may have concerns about near-term macroeconomic headwinds, I believe that the long-term story of Home Depot remains attractive. It’s often a wise strategy to purchase high-quality stocks at discounted valuations when the market is focused on short-term factors. Eventually, the business cycle will turn, and companies like Home Depot tend to emerge stronger on the other side. Moreover, investors can also benefit from an attractive dividend yield (FWD) of 2.9% while waiting for the stock’s potential upside. Therefore, I believe that Home Depot stock is a good buy at its current levels.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

This article is written by Ashish S.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.