Summary:

- Since my last writing, a critical development surrounding INTC stock is the potential spinoff of its foundry division.

- Finding a suitable buyer at a reasonable price seems to me unlikely under current conditions.

- Even if the spinoff materializes, it is only a way to cut losses.

- I expect the company to continue to have trouble competing with fabless rivals such as ADM and NVDA.

duoogle

INTC stock: previous thesis and new developments

My last article on Intel Corporation (NASDAQ:INTC) was titled “Intel’s Q2 Earnings Release Taught Me 3 Lessons About Its Turnaround.” As seen from the screenshot below, it was published on August 7. As the title suggests, the focus was on its Q2 earnings report and how it has influenced my assessment of its turnaround plan. Quote:

Intel Corporation’s Q2 earnings report has led me to reassess the odds of the success of its turnaround plan. A successful turnaround requires sound fundamental economics and financial resources. Intel’s Q2 results and, more importantly, FWD guidance have led me to question both. Credit downgrades can further increase its future borrowing costs and limit its financial resources.

Seeking Alpha

Since that writing, there have been a few new developments surrounding the company. The most important one on my list is the possibility for the company to spin off its foundry division. Given the pivotal role of the foundry dividing in its turnaround plan, this possibility merits a closer look and motivated this follow-up article. For readers unfamiliar with the background, recently, INTC has been reported to be in talks with investment banks to spin off its foundry business. Leading analysts also argued for such a spin-off as you can see from the quotes below.

Tech PowerUp (August 30, 2024): According to a recent report from Bloomberg, Intel is in talks with investment banks about a possible spin-out of its foundry business, as well as scraping some existing expansion plans to cut losses. As the report highlights, sources close to Intel noted that the company is exploring various ways to deal with the recent Q2 2024 earnings report… CEO Pat Gelsinger is now exploring various ways to control these losses and make the 56-year-old giant profitable again. Goldman Sachs and Morgan Stanley are reportedly advising Intel about its future moves regarding the foundry business and overall operations.

Seeking Alpha news (Sept 5, 2024): While management has bet the company’s future on its foundry business, Citi believes it should get out while it still can. “While in our view Intel manufacturing for CPUs is on track, we continue to believe it should exit the foundry business in the best interest of shareholders,” Citi analyst Christopher Danely said in a note to clients.

In the remainder of this article, I will explain why A) I consider it unlikely that INTC can find a suitable buyer for its foundry business under current conditions (at a reasonable price anyway), and B) thus I consequently expect the ongoing selling pressure to persist.

INTC stock: foundry in focus

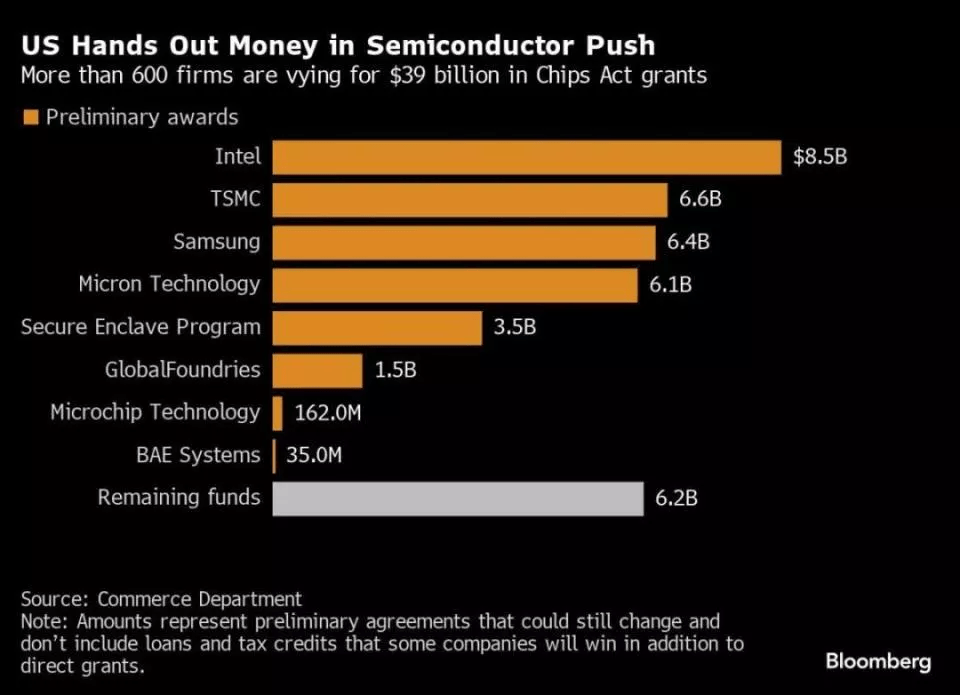

INTC’s foundry initiative and the support provided by the US government for this initiative were key factors in my earlier bullish thesis on the stock. As an example, the chart below shows the preliminary awards the US has made under the CHIPS Act. The total amount allocated is $39 billion and is distributed across a handful of companies. Intel has secured the largest share of the funding as seen, with a preliminary award of $8.5 billion. Following closely are TSMC and Samsung, each receiving $6.6 billion and $6.4 billion, respectively.

Bloomberg

With the setbacks the company suffered, I had to reassess my thinking and have to admit that I misjudged the impact of the US support, badly. The challenges faced by INTC (and other recipients of the CHIPS awards too) are far beyond financial. Almost all the recipients listed on the chart above, both domestic and foreign, face various substantial challenges in building manufacturing facilities in the United States, despite the incentives provided by the CHIPS Act. These challenges include difficulties in adapting to the local environment, labor issues, high operational costs, etc. Even sector leader Taiwan Semiconductor Manufacturing Company Limited (TSM) is experiencing difficulties and delays with its Arizona factory. TSM announced plans in 2020 to build a chip manufacturing facility near Phoenix. Four years have passed and TSM has yet to start selling semiconductors made in Arizona.

Out of the many issues, the top one – an almost insurmountable issue in my mind – is the issue of skilled technicians and engineers. TSMC is successful for its hiring standards and rigorous work pace, which is what the precision of chip manufacturing requires and the crucial ingredients in its success in my view. TSM can send highly skilled and experienced local (i.e., Taiwanese) engineers to Arizona (at the cost of higher operating expenses) and yet still cannot overcome the issue entirely due to a range of reasons (cultural, language, etc.). INTC does not have a reservoir of experienced engineers like TSM to start with and is probably facing more restrictions in terms of hiring as it is more limited to local talents (and the US unions could further add to the limitations).

Given these issues and the current limbo status of INTC’s many foundry projects, I think it is very unlikely for INTC to find a buyer. Even if it does, I don’t think the price would be in favor of shareholders.

INTC stock: sell pressure likely to persist

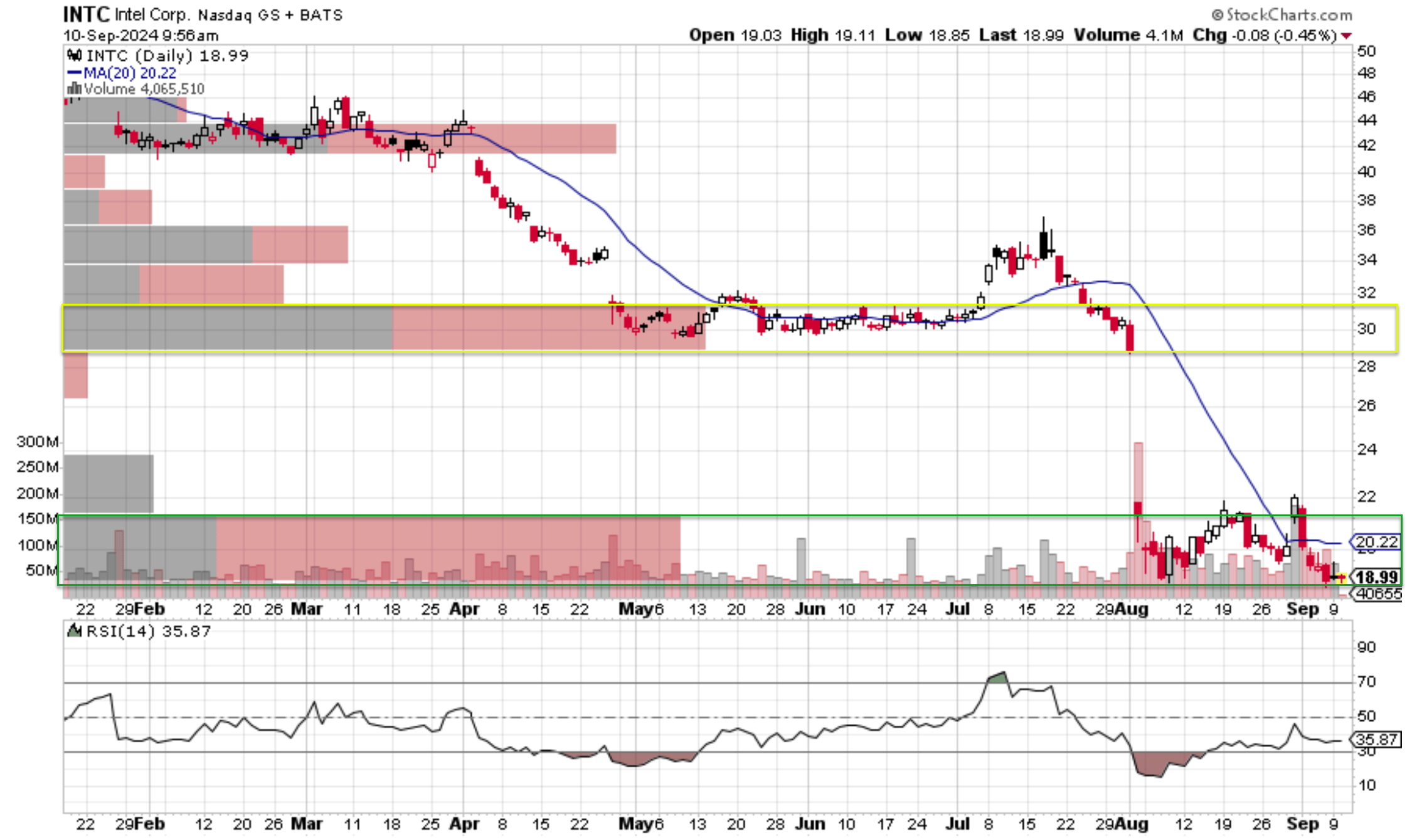

As a reflection of my above pessimism, the stock continued to face selling pressure shortly after the news of the spinoff possibility. As you can see from the chart below, the stock price enjoyed a sizable rebound immediately after the news of a potential spinoff broke. However, the selling pressure shortly took over and pulled the stock prices to be even lower than before the news. Judging by the technical trading pattern, I think the selling pressure facing INTC stock is likely to persist. More specifically, the top panel of the chart below describes the price-volume trading information of INTC with its 20-day moving average.

As seen, INTC stock prices have now declined to be well below its 20-day moving average of $20.22. This negative divergence is a classical sign that selling pressure outweighs buying interest. Also, note that the trading range (around $19 to $21) highlighted by the green box represents the range with the largest cumulated volume in the past 6 months. Given the high volume, I consider this to be a key support range. INTC prices currently are near the bottom of this range and are likely to fall through. On the upward direction, the closest resistant level is around $30 as highlighted by the yellow box judging by the sizable volume in this range. The current price is too far away from this level and I do not expect it to challenge it anytime soon given the negative fundamentals. Lastly, the Relative Strength Index (RSI) furthers the bearish outlook. The RSI currently sits around 36, borderline the oversold regime (30 is typically considered the threshold).

Source: StockCharts.com

INTC stock: upside risks and final thoughts

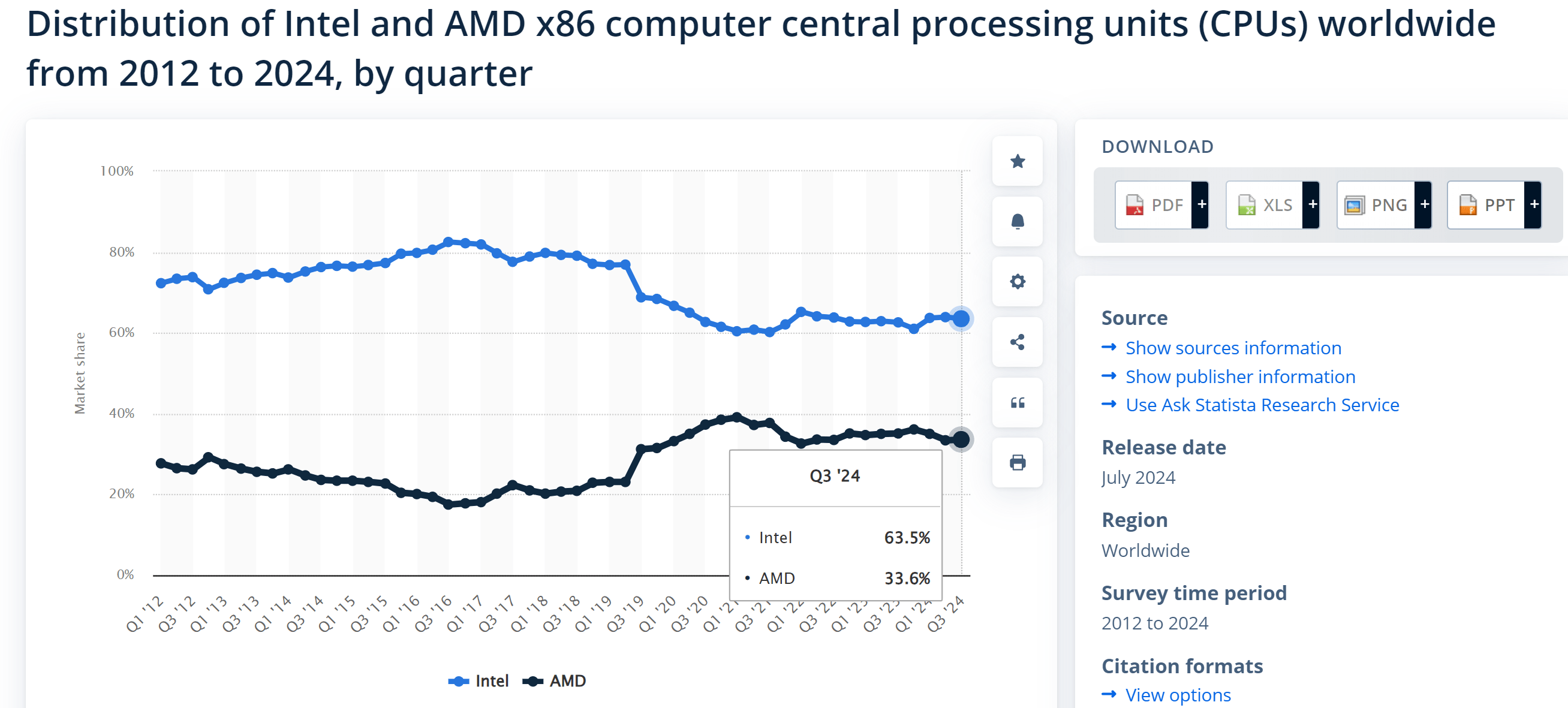

In terms of upside risks, a strong PC market recovery or update cycle could help INTC. The company has been losing its PC market share (and lagging competitors on the AI front) in the past few years. However, in recent quarters, the company’s PC market share seems to be stabilizing or even slightly improving as you can see from the chart below. This chart provides a comparison of INTC and AMD’s market share in the x86 computer CPU market from 2012 to 2024. Intel has maintained a dominant position in the market before 2017~2018, with its market share peaking above 80%. The market share quickly dropped since then due to competition from AMD. Its market share dropped to as low as ~60% recently and has recovered slightly to the current level of 63.5% as of the latest quarter.

To sum up, I see an overall bearish picture surrounding the stock. Fundamentally, I do not see INTC having the resources – both in terms of talent and money – to simultaneously compete on both the chip and manufacturing fronts. On the foundry front, pure-play rivals such as TSM are too far ahead. Thus, I do consider the spinoff of its foundry division as a viable option. Although it is only an option to cut losses in my view. In the case the spinoff indeed materializes (and I have my doubts as argued), I expect INTC to still be in a tough position to compete with fabless chip rivals such as AMD and NVDA.

Statistica

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.