Intel Corporation’s Q2 earnings report has led me to reassess the odds of the success of its turnaround plan.

A successful turnaround requires sound fundamental economics and financial resources.

Intel’s Q2 results and, more importantly, FWD guidance have led me to question both.

Credit downgrades can further increase its future borrowing costs and limit its financial resources.

Prostock-Studio

INTC Stock: Q2 recap

Readers familiar with my writings would notice that my investment approach has a strong contrarian flavor. In particular, I like to invest in turnaround stocks (and have had winning success rates so far). In the case of Intel Corporation (NASDAQ:INTC) stock, I have been betting on its turnaround plan in the past 1~2 years. As an example, my last article on the stock was titled “Intel Stock: Why I Keep Betting Against Wall Street (Technical Analysis).” In that article, I argued that:

Wall Street has become overly sensitive to its setbacks, especially those surrounding the foundry business. Intel Corporation’s foundry business is a long-term investment to start with. The market’s overreaction to quarterly updates only offers superb entry points for long-term investors.

Seeking Alpha

Since then, INTC has released its FY Q2 earnings report (“ER”). The results have led me to reassess my thesis, which is the focus of this follow-up article. The remainder of this article will explain why now I have a much gloomier view of the odds of its turnaround plan.

By this time, the ER has been critiqued by many Seeking Alpha authors and I assume readers are well aware of the negatives (weak financials, 15% layoff plan, plan to halt dividends, etc.). Therefore, in this article, I will focus on three aspects less discussed so far. And I will present these aspects in the form of 3 painful turnaround lessons I’ve learned from the stock: the fundamental economics of the business, the financial resources available, and the feedback from market sentiment.

Intel stock Q2: margin pressure

If you have invested in turnaround stocks, you would surely know the top 2 requirements for a successful turnaround are effective leadership and fundamentally sound business economics. To limit the scope of this article to more objective aspects, I will leave the leadership requirement in this article and directly move on to the fundamental economics of its business. In a nutshell, its Q2 results and forward guidance have led me to question the economics underlying INTC’s business operations.

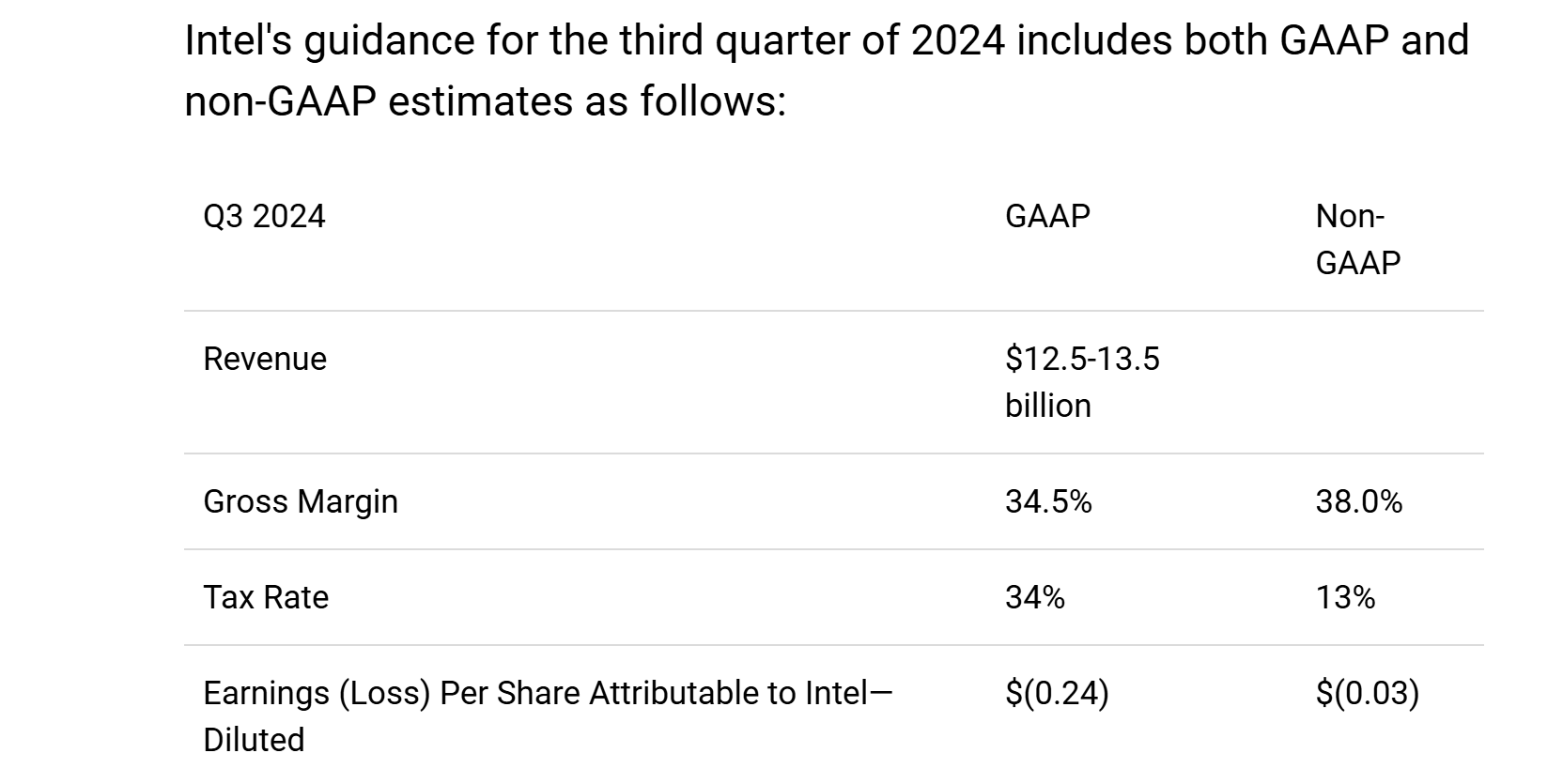

To wit, the chart below shows the earnings guidance INTC issued for its Q3 2024. As seen, Intel expects revenue to fall within the range of $12.5 billion to $13.5 billion. More importantly, it expects A) its gross margin to be 34.5% under the Generally Accepted Accounting Principles (GAAP) and 38.0% on a non-GAAP basis, and B) its net profits to be negative both on a GAAP basis and a non-GAAP basis. Earnings per share (EPS) are expected to be a loss of $0.24 per share and a loss of $0.03 on these bases, respectively.

Seeking Alpha

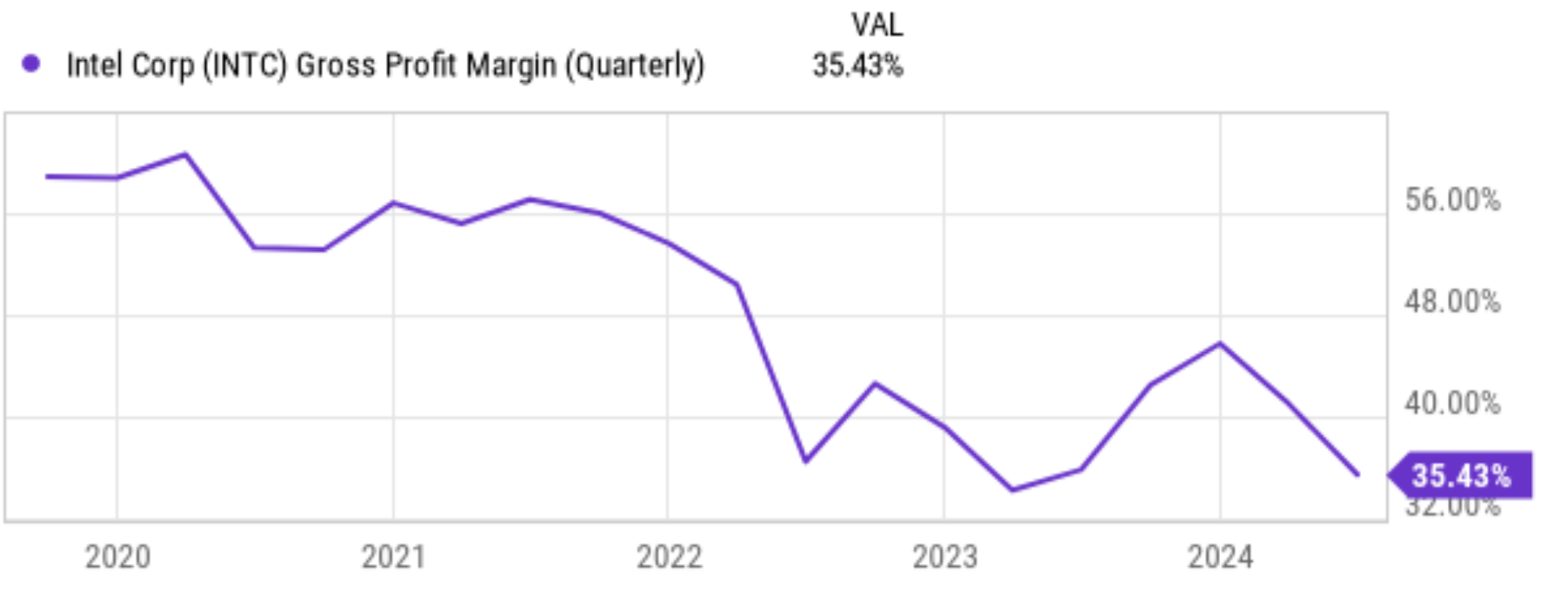

I view such margin guidance as a concerning sign of its underlying economics in both absolute and relative terms. For example, the chart below shows the gross profit margin for INTC stock in the past 5 years to better contextualize things. As seen, despite some fluctuations, the trend is overall downward. The margin started in early 2020 at around 60% and declined to the current level of 35.4% only. My concern is even more heightened when its margin is benchmarked against key rivals.

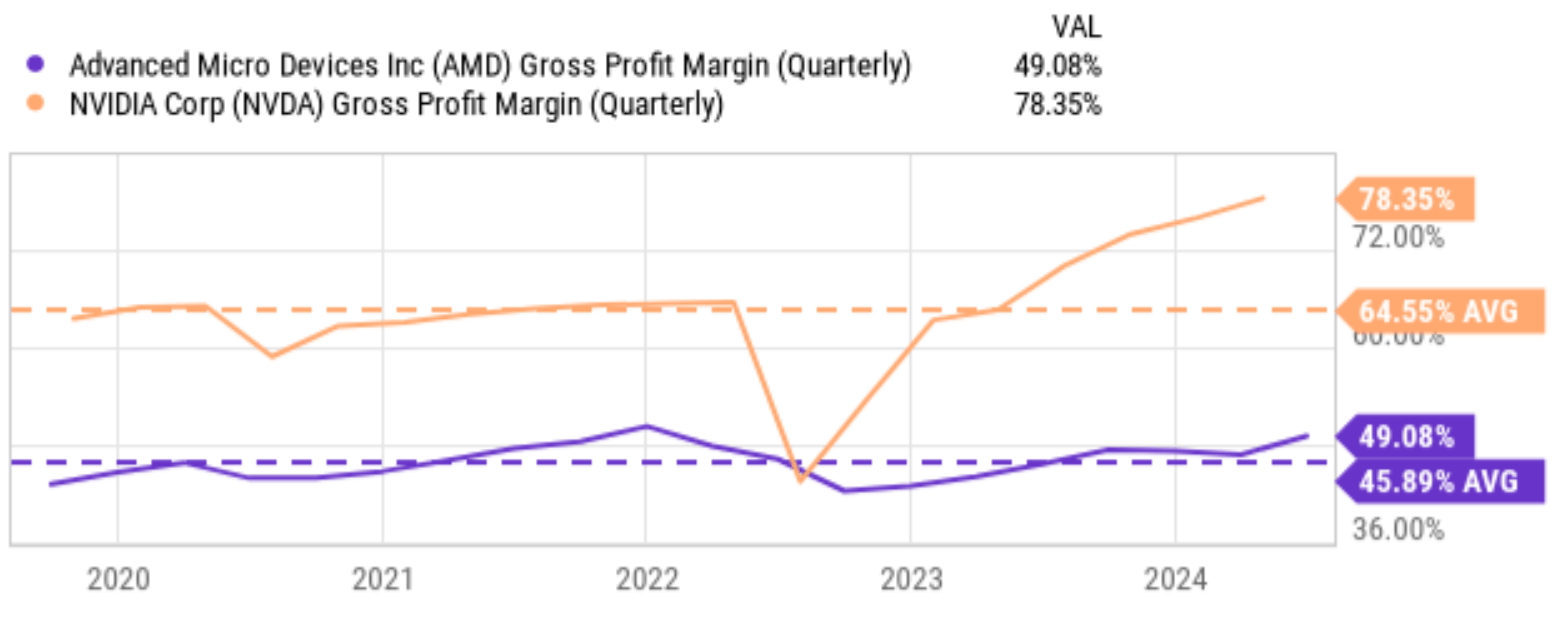

As an example, the second chart below shows the gross profit margins of Advanced Micro Devices (AMD) and Nvidia Corporation (NVDA) during the same period. As seen, Nvidia consistently outperforms both INTC and AMD with a significantly higher gross profit margin averaging 64.5%. Moreover, Nvidia’s margin has been trending upward, and as argued in my recent article, I expect NVDA’s superb profitability to persist in the near term, judging by the inventory data and LLM demand for advanced chips. AMD’s margin has fluctuated more and has not enjoyed the kind of expansion NVDA enjoyed. However, AMD’s margin stays consistently at a respectable level, with an average gross profit margin of 45% as seen.

To further compound my concern, INTC’s future earnings guidance also began to raise questions in my mind about whether it has the financial resources to keep supporting its turnaround plan, as detailed next.

Seeking Alpha

Seeking Alpha

INTC stock: financial resources

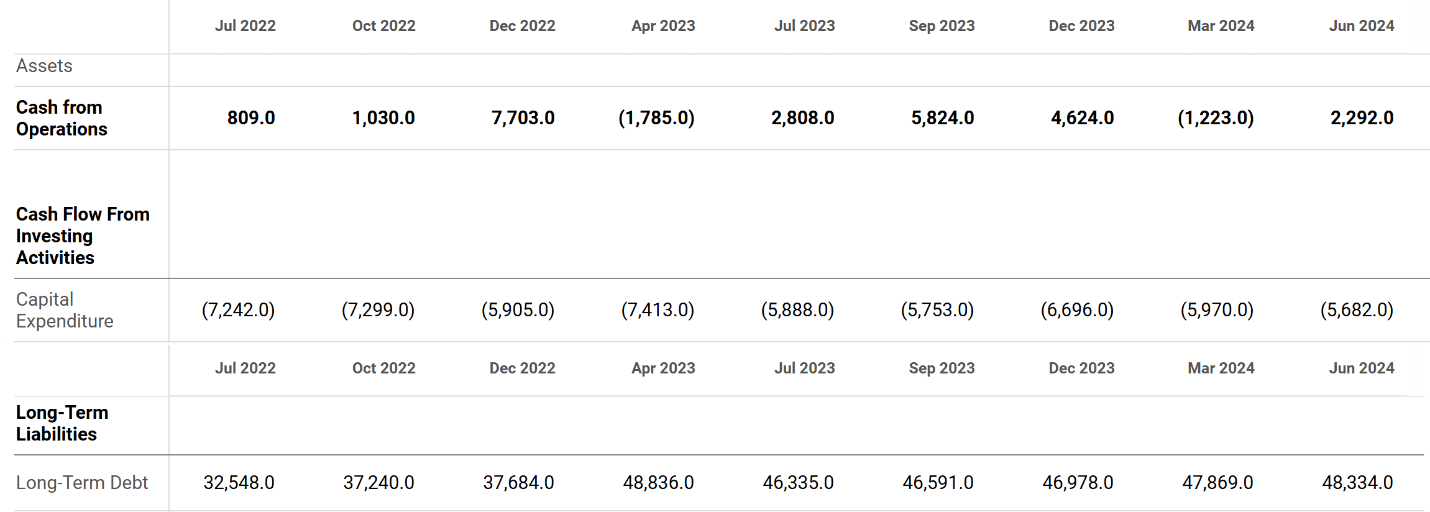

Besides effective leadership and fundamental sound economics, the next requirement for a successful turnaround is plenty of financial resources. I am not certain if INTC can meet this requirement anymore after its Q2 results and forward guidance. As an example, the chart below shows the operating cash, capital expenditures, and long-term debt of INTC stock in recent quarters. As seen, its operating cash flow has been volatile in recent quarters and dialed in $2.29 billion for Q2. Meanwhile, capital expenditures have remained consistently higher than operating cash flow, with its investment in the fab capability as a key driver. The average CAPEX has been around $6 billion per quarter in the past ~2 years or so and was $5.68B for Q2, far exceeding the operating cash flow. As a result, even after the company has halted its dividend payouts entirely, I don’t see the financial resources that can support it turnaround plan sustainably.

The company has been increasingly relying on debt financing as a result. To wit, as illustrated by the chart below, long-term debt has increased substantially in the past few years. In the past 2 years alone, it increased from $32.5 billion in 2022 to the current level of $48.3 billion.

Seeking Alpha

Other risks and final thoughts

The company’s increasing reliance on debt financing leads me to the final lesson: the feedback of the market’s view on the company’s business operations. The starting point of investing (or at least fundamental-driven investing) is that a good business leads to good market sentiment and thus higher stock prices. However, market sentiment can in turn impact business fundamentals, especially in the case of turnaround stocks when the stock prices are more sensitive to market sentiments (and INTC’s stock price movements after the Q2 ER serve as an illustrative example here).

Negative sentiment can cause/amplify a negative feedback loop. For example, negative sentiment makes it hard for the company to raise capital (both in the equity and debt market) and motivate/retain its employees financially, which in turn leads to stronger negative sentiment. As an additional illustration of such a feedback mechanism, you can see from the quotes below that major credit agencies have lowered their credit rating. This potentially increases its future borrowing costs and further limits the financial resources available for it to continue working on the turnaround.

Fitch Downgrades Intel’s Ratings to ‘BBB+’; Affirms Short-Term Ratings at ‘F2’; Outlook Stable on 01 Jul, 2024…. the successful execution on Intel’s strategy to regain process technology leadership and build the leading foundry services business in the U.S. and Europe could support a return to the A-category. However, Fitch does not expect this to be apparent in the next few years.

S&P Global lowered Intel Corp’s Rating To ‘A-’ On Weaker-Than-Expected Growth While Capital Intensity Stays High; Outlook Negative. We expect Santa Clara, Calif.-based semiconductor manufacturer Intel Corp.’s revenue to be weaker than previously forecasted given recent personal computer (PC) and data center end market recovery trends for 2024.

In terms of upside risks, turnaround stocks generically offer high-payoff potential, together with the high risks involved. Besides such generic characteristics, another key upside risk for INTC is government support. Advanced chip manufacturing capability is considered not only as a business interest but also an interest of importance to national security – for good reasons. One of the key factors that led me to bet on its turnaround plan was that I expected INTC to receive substantial government support along the way. This has indeed been the case thus far, in my view. For example, the company has recently been granted up to $8.5 Billion from the Biden administration under the CHIPS & Science Act to build its semiconductor facilities.

To reiterate, developments reported in Intel Corporation’s Q2 ER have led me to reassess the odds of its turnaround. Experience has demonstrated to me that two of the traits – that is, besides effective leadership – of successful turnarounds are fundamentally sound profitability and plenty of financial resources. I begin to question both following INTC’s Q2 ER.

Furthermore, the prevailing negative market sentiment can also feed back to its business fundamentals and make it even harder for INTC to turn around. With these considerations, I am lowering my rating to HOLD from my earlier BUY rating and would only suggest you consider it unless you truly have a very high level of risk tolerance.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of INTC either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If you share this investment style, check out Envision Early Retirement. It provides at least 1x in-depth articles per week on such ideas.

We have helped our members not only to beat the S&P 500 but also avoid heavy drawdowns despite the extreme volatilities in BOTH the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too.