Summary:

- Johnson & Johnson is entering the surgical robotics market with the Ottava surgical system, potentially gaining a strong market position.

- Ottava’s design offers competitive advantages over the dominant da Vinci system, including a smaller footprint and potential cost savings for healthcare organizations.

- The global surgical robotics market is expected to grow rapidly providing a significant growth opportunity for JNJ, which is well-positioned with its established capabilities and brand reputation.

FatCamera

When looking for dividend stocks, I’m as concerned about capital growth as I am about compounding safe income.

The issue is that companies that pay dividends (unless required by law) often do so because it’s the most efficient use of cash to return value to shareholders. But this often comes at the expense of company growth.

But I don’t think this entirely holds for Johnson & Johnson (NYSE:JNJ). In addition to paying out excellent dividends, it’s also using that excess cash to make a bold leap into robotics to accelerate its growth trajectory, notably with its Ottava surgical robot.

JNJ has been planning to enter the robotics market for some time, which it has accomplished through acquisitions. It acquired Orthotaxy, a developer of software-enabled robotic technology for surgery, in 2018 and Auris Health, another robotics technology company, a year later.

Framing this effort is that JNJ has fallen far behind its peers in the robotics market, as its presence is nonexistent from a commercial standpoint. Ottava is an emerging pipeline product that’s still under research and development.

JNJ’s late start in this area is partly because the system has been continually delayed. Initially expected to be used in human surgeries by the end of 2022, technical issues and COVID-19 have postponed these plans. The company intends to seek FDA approval for clinical studies in the latter half of 2024. Some analysts have speculated that the robot could be released between late 2026 and early 2027.

Despite initial setbacks, I think JNJ’s delayed entry into the surgical robotics market might work in its favor. The slow adoption of robotics in surgery, primarily due to surgeons’ objections, is directly addressed by Ottava’s specific design features and speculated price point. The expected timing of J&J’s entry around 2027 also coincides with predictions of substantial growth in the robotics market. This may position the company to see an accelerated return on its venture due to the significant pent-up demand for JNJ’s entry.

Robotics synergizes exceptionally well with the company’s brand reputation and existing product portfolio. If any company can successfully bridge the gap between traditional surgical methods and the advanced capabilities of robotics, it’s Johnson & Johnson. For this reason, I’m giving this company a “Buy” recommendation and will quantify how I believe Ottava will affect JNJ’s financials.

Ottava Surgical System Overview

Johnson & Johnson’s Ottava is a surgical robot developed for soft-tissue procedures. This includes procedures such as hernia repairs, organ resections, and various other general surgeries.

Robots like Ottava are utilized in these procedures primarily for their precision and control capabilities. They enable surgeons to perform complex tasks more accurately than possible by hand.

Ottava is equipped with robotic arms and high-definition 3D cameras. Combining these features with the surgeon’s expertise may facilitate minimally invasive procedures, resulting in smaller incisions, reduced scarring, and potentially faster patient recovery times.

JNJ’s Monarch robotic surgical platform is a key component of its digital surgery ecosystem, designed to integrate with its surgical and robotic technologies, including the Ottava system. Monarch, which already has FDA clearance for certain medical procedures, is being developed further by JNJ for cancer diagnosis.

Ottava’s competitive positioning

J&J’s Ottava system will join a family of surgical robots upon release. The table below provides a breakdown of current and upcoming surgical robots. This high degree of specialization is a feature that was not present until recently.

| Brand & Model Name |

Unique Feature Description |

| Johnson & Johnson’s Ottava |

Features a smaller footprint with retractable arms for space efficiency. |

| Intuitive Surgical’s da Vinci Systems (Xi, X) |

Widely adopted, versatile for various surgeries. |

| Medtronic’s Hugo Robotic-Assisted Surgery System |

Completed first procedure in 2022, advanced features, aiming for high flexibility in surgery. |

| Stryker’s Mako Robotic-Arm |

Specialized in orthopedic surgeries for knee and hip replacements. |

| Zimmer Biomet’s ROSA Robot |

Precision-focused for neurosurgical and spine procedures. |

| Globus Medical’s ExcelsiusGPS |

Integrates robotics with navigation and imaging for spine surgeries. |

| Smith & Nephew’s NAVIO Surgical System |

Orthopedic focus, especially knee replacements, without CT scans. |

| CMR Surgical’s Versius Surgical Robotic System |

Compact and mobile for a variety of laparoscopic surgeries. |

| Auris Health’s Monarch Platform |

Designed for lung condition procedures using a flexible robotic endoscope. |

| TransEnterix’s Senhance Surgical System |

Emphasizes digital laparoscopy with hand-mimicking instruments. |

This analysis will focus primarily on Ottava’s competitive advantages over Intuitive Surgical’s da Vinci system. J&J must overcome this competitor if it intends to become the market leader.

One of Ottava’s main advantages is its smaller footprint. On the surface, this may seem like a minor advantage, but I feel it’s highly significant in practice. For context, a standard model like the da Vinci Xi has a footprint roughly the size of a small car when the robotic arms are fully extended.

da Vinci X Cheyenne Regional Medical Center

On the other hand, Ottava is designed to be more efficient in smaller spaces. Its retractable arms, for example, can fold completely under the operating table when not in use. The arms are built into the surgical bed, so there’s no need for a separate tower or cart, unlike the da Vinci system.

Ottava’s smaller size means it can potentially reduce costs for healthcare organizations. Since its size is smaller, it can be used by clinics and hospitals with more limited floor space. This means these organizations can save on expensive construction projects by not having to build new rooms and may help reduce the need for larger operating theatres altogether.

Costs were found to be a key objection that stands in the way of clinics adopting robot-assisted surgery, according to a study from 2011. Another problem the study found was that payments for these surgeries are the same as for standard laparoscopic procedures. Said differently, without additional financial incentives, justifying the higher price of advanced robotic systems becomes challenging for healthcare providers, as they do not generate additional revenue to offset these higher costs.

Therefore, reducing these systems’ prices indirectly via eliminating the need for larger floor space and directly with a lower sticker price is critical. To put some of these costs into context, the da Vinci-S system starts at around $1.5 million for a standard model, which doesn’t include servicing or training expenses. The servicing contract is around $112,000 per year. Ottava’s price point is currently unknown. However, given its smaller size and objective to take market share from its peers, a lower upfront investment may be part of J&J’s pricing strategy.

Its design also offers functional benefits. The retractable arms save space and help minimize setup times in surgical environments. The four arms also move in unison with the operating table; this is expected to help shorten procedure times. Another indirect benefit of its design is that staff have more room to navigate the surgical space, improving health and safety and simplifying complex workflows.

Therefore, I’m bullish on Ottava’s prospects for the above reasons. It addresses major objections healthcare organizations raised about why they haven’t embraced robot-assisted surgeries. Therefore, its combination of strengths gives it a sharp spear to go out and claim market share from its competitors.

However, Ottava’s entry into the market is considerably complex. Analysts project Ottava to compete with Medtronic’s Hugo system rather than immediately challenging the widely installed da Vinci surgical robot.

Again, one of the main obstacles in Ottava’s way is cost, but also da Vinci’s deep penetration into the market. Da Vinci has an enormous installed base of over 6,700 systems worldwide. Surgeons and hospitals have invested heavily in the da Vinci platform and associated instrumentation and training. There would be high switching costs to adopt a new system.

Furthermore, JNJ is expected to have a specific initial customer segmentation strategy for Ottava, with J.P. Morgan analysts writing, “[Ottava] could compete well against Hugo in new surgical accounts and particularly in [ambulatory surgery centers (ASCs)].” This means it would not initially seek to replace da Vinci systems in large hospitals with an established foothold.

The da Vinci system continues to see strong procedure and revenue growth globally. To me, this suggests that there is room for alternatives like Ottava to gain a share in specific segments rather than outright displace the leader in the foreseeable future.

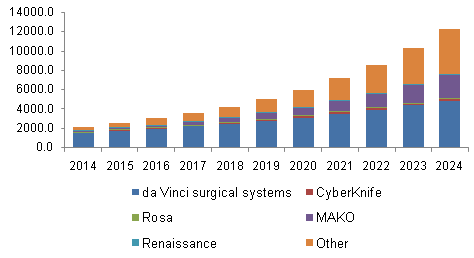

Another boon is that the competitive market structure moving forward is panned to be favorable for new entrants like the Ottava. According to a report by Grandview Research, the da Vinci system has the largest market share by a considerable margin. However, given each model’s high degree of specialization, the market is far from a monopoly, with the “Other” category growing in prominence each year. This data suggests that the market is steadily moving from a consolidated one in 2014 to a far more diverse one in 2024. Ottava’s delayed release may be seen as a blessing in disguise as it rides on the coattails of the industry’s trends in growth and diversification.

Grandview Research

Market and Financial Analysis

Since Ottava is still considerably far away from its release date, management has been coy about its specific impact on its Ottava system in terms of top-and-bottom-line growth. Guidance on these figures is expected as Ottava nears its release date. However, given its growing total addressable market and low global penetration rate, we can surmise it will likely be significant over the long term.

For some context, Intuitive Surgical, the da Vinci surgical robot maker, has an estimated global market share of around 57% at the time of writing. Furthermore, the use of robotic surgeries in general surgery procedures rose from 1.8% in 2012 to 17% in 2022. J.P. Morgan analysts have forecasted a 17% CAGR for using robotics in soft tissue procedures into 2026.

This appears to be another case of favorable timing for JNJ, as the rise in robot-assisted surgeries is anticipated to reach a critical inflection point coinciding with the projected release of Ottava. Additionally, there’s an expected sharp increase in the prominence of Ambulatory Surgery Centers [ASCs] over time. This trend is particularly noteworthy since Ottava is primarily intended for use in ASCs rather than in hospitals, where a significant portion of the surgical industry’s growth is expected. Some of the reasons why ASCs are expected to grow over hospital is due their lower comparative costs for patients as well as being able to serve a wider geographical area.

Underling this, Surgical Information Systems also suggests that numerous soft-tissue procedures are anticipated to transition from hospital outpatient facilities to ASCs. Among those, some can be performed using the Ottava surgical robot:

Procedures likely to move from Hospital Outpatient to ASCs:The 2023 Impact Change Forecast calls out likely procedures to shift to ASCS between now and 2033. They indicate high shift potential for Upper GI Endoscopy, Hammertoe, and First Ray (Foot) procedures and medium shift potential for Colonoscopy, Neurostimulator, Rotator Cuff Repair, and Lumpectomy/Mastectomy procedures.

Often constrained by smaller budgets and facility sizes, these centers present an ideal opportunity for the sleeker Ottava system to gain a foothold in an expanding market.

To gauge the financial impact of the Ottava robot on JNJ’s finances, we will begin with specific initial premises and then proceed using informed assumptions. Note that we will use Intuitive Surgical’s financials. This company has three reportable operating segments (Instruments & Accessories, Products, and Services), but all relate to the sale or service of their robots, so I believe using the total revenue contribution of this segments will give us an accurate baseline.

Some of the premises are as follows:

- Intuitive Surgical has a global market share of around 57% for robot-assisted surgeries.

- Intuitive Surgical’s full-year revenue for 2022 was $6.22 billion.

- This then implies a total addressable market of $10.91 billion in 2022.

- JP Morgan forecasts a 17% CAGR in robotic soft tissue procedure growth, which brings the projected TAM to be approximately $12.77 billion in 2026.

Considering the expansion of ASCs, the projected pricing and features of Ottava, and the expected shift of certain soft-tissue procedures from hospitals to ASCs, I suggest a conservative estimate for Ottava’s peak market share to be around 15% in the foreseeable future.

If we assume that Ottava will begin selling in 2026 as analysts speculate, and that it will follow an S-curve adoption model, I believe that the following revenue projections are a reasonable starting point. Note that these projections were smoothed by me.

| Year | Estimated Market Share (%) | Revenue with 17% market CAGR growth (Billion $) | Revenue with 10% market CAGR growth (Billion $) | Average Revenue (Billion $) |

|---|---|---|---|---|

| 2026 | 0.10 | 0.01 | 0.01 | 0.01 |

| 2027 | 0.30 | 0.04 | 0.04 | 0.04 |

| 2028 | 0.88 | 0.15 | 0.14 | 0.14 |

| 2029 | 2.38 | 0.49 | 0.41 | 0.45 |

| 2030 | 5.47 | 1.31 | 1.02 | 1.17 |

| 2031 | 9.53 | 2.67 | 1.96 | 2.31 |

| 2032 | 12.62 | 4.13 | 2.85 | 3.49 |

| 2033 | 14.12 | 5.41 | 3.51 | 4.46 |

| 2034 | 14.70 | 6.59 | 4.02 | 5.31 |

| 2035 | 14.90 | 7.82 | 4.49 | 6.15 |

Ottava could then make up a significant portion of JNJ’s MedTech revenue, as well as give it a strong recurring revenue base from servicing, training, and accessories as inferred from Intuitive’s financial reports.

I also see some potential catalysts that could accelerate the adoption of the Ottava robot. Most importantly, it can integrate with the advanced instruments surgeons already use and prefer from JNJ’s Ethicon business. This interoperability could accelerate Ottava’s adoption. The reasoning is simple: Surgeons are likelier to adopt new technologies that seamlessly work with their preferred, familiar tools. It helps to reduce the learning curve of using the technology, as well as other integration challenges. Furthermore, it smooths over the long-term transition from traditional surgical practices to robotics.

JNJ CEO Joaquin Duato appeared considerably bullish on the adoption of its robot in its most recent earnings call, citing Ethicon as the responsible catalyst:

They are rooting for Johnson & Johnson to come into the robotic surgical space. They want to have the service and the support with our Ethicon business and they also want to be able to utilize the advanced instruments with whom they have grown [familiar with]. So what I see in the surgical space is that the surgeons want to have alternatives and they are all looking forward to having Johnson & Johnson play an important role in robotic surgery.

Quarterly Financials & Valuation

Framing Ottava’s predicted entry into the market is JNJ’s overall positive and improving financial health. Notably, sales grew 6.8% operationally to $21.4 billion for Q3 2023, driven by 10.9% growth in pharmaceuticals and 10.4% growth in medical devices. It also posted $4.3 billion in earnings from continuing operations.

As for some downside risks, what stands out to me is that JNJ maintains an accrual of approximately $9 billion as its best estimate of probable loss for the talc litigation. This is a significant liability on the balance sheet. However, the reserve is payable over 25 years, reducing near-term liquidity impact. The total nominal amount is approximately $12 billion. But there’s still uncertainty regarding final resolution of the talc claims, which could require additional accruals.

The company has approximately $23.51 billion in cash on its balance sheet with $29.92 billion in debt. This gives it a net cash position of -$6.41 billion or -$2.66 per share. It’s also important to note that JNJ also generates a huge amount of free cash flow. Over twelve months it generated $15.74 billion in FCF. So, while the lawsuits are substantial threats to JNJ’s business, it’s more than capable of absorbing the losses. On the other hand, JNJ does face a steep opportunity cost since those same funds could be better deployed elsewhere, but this cost is hypothetical in nature.

I think this Kenvue separation has muddied the waters in terms of JNJ’s valuation, and the market has not priced in JNJ’s fair value. This can be seen from an EPS basis of JNJ’s share barely moving at all despite EPS from continuing operations growing by 4.3% year-over-year and management guided to further progression in 2024. JNJ reported a total EPS of $10.21, of this, $8.52 came from discontinued operations, which includes the gain on the Kenvue separation.

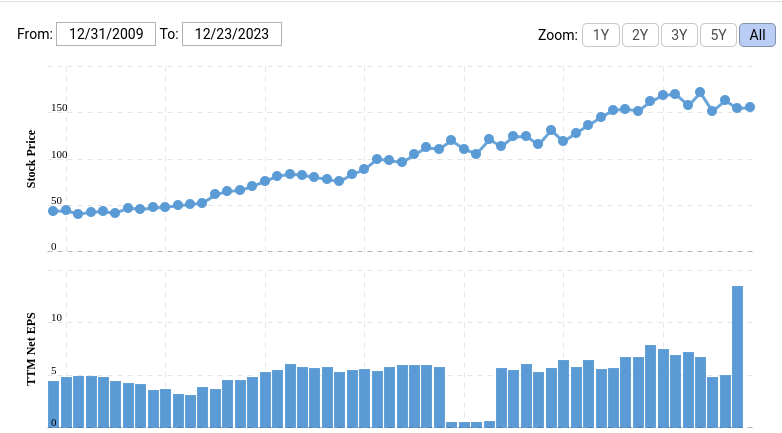

Author supplied

JNJ trades at a forward P/E of ~14x compared to its 5-year average multiple of ~24x. The valuation discount seems unwarranted given expected EPS growth. $5 billion in share repurchases were also completed in the quarter, demonstrating commitment to return capital to shareholders. The risks from the talc payments also seem contained from its 25-year payment term.

And if we see the expected fall in interest rates next year, Dividend Kings could also see a boost in valuation as investors return to equities in search of yield. Defensive stocks like JNJ may also become an appealing hedge while investors take on more risk elsewhere.

All these factors indicate that JNJ’s is currently undervalued, and that a further upside for the company is to be had in the near-term.

Risks

The most significant risk is that development setbacks or delays could push back Ottava’s commercial launch. While Johnson & Johnson targets seeking regulatory approval in 2024 and analysts predict possible market entry around 2026-2027, Ottava remains an early stage pipeline asset that still faces technical and testing hurdles. Any safety issues or need for design modifications found during development could postpone the launch timeline.

Additionally, gaining surgeon and hospital acceptance once launched poses challenges. The surgical robotics market has substantial barriers to entry given the entrenched position of Intuitive’s da Vinci system and its expansive installed base. While Ottava aims to differentiate through pricing and integration with existing J&J surgical tools, convincing healthcare organizations to adopt a new platform still requires significant education and coaching. Execution missteps like lacking sufficient sales support during rollout could hinder traction. And since much of the bull case depends on Ottava fueling above-market growth tailwinds, sputtering commercial adoption would dampen the investment case.

Conclusion

JNJ’s foray into the surgical robotics market with the Ottava system and the Monarch platform represents a significant stride in MedTech.

The Ottava system’s unique design features, like its smaller footprint and retractable arms, address key market barriers. As the surgical robotics market continues to diversify and grow, J&J’s entry with Ottava, although later than its competitors, may align well with market readiness and demand.

If investors were on the fence about JNJ’s shares, I feel that this, along with it being more broadly undervalued, may give them the extra push they need to open a position.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.