Summary:

- Lucid Group announced a $3 billion offering to address production issues, causing a 24% drop in stock price, which may be an overreaction.

- With $6 billion in liquid assets after the offering, Lucid can scale production, and the backing of the Saudi Arabian Public Investment Fund (PIF) indicates support for the company’s growth.

- Despite potential risks such as cash burn and demand concerns, I believe the capital raise is a positive step for Lucid’s long-term prospects.

Michael H/DigitalVision via Getty Images

Inadequate production is the root of all of Lucid Group, Inc.’s (NASDAQ:LCID) problems. In order to remedy this issue LCID announced a $3 billion offering, which will cause a 20% dilutive effect. As a result, shareholders expressed their frustrations causing the stock to fall 21% since the announcement. Despite the understandable frustration of LCID’s long-suffering shareholders, I believe this is an overreaction since dilution is necessary for LCID to secure its future. That said, I believe LCID is a buy at the current dip price once its offering closes. Now that LCID has enough funds to scale production, its production woes could soon be behind it.

Production

Despite CEO Rawlinson’s statement during its Q4 earnings call that LCID has “solved production”, I remain unconvinced.

During 2022 LCID cut its production guidance twice and only produced 7,180 EVs that year. For reference, Polestar (PSNY) produced 21,000 EVs in the last quarter of 2022 alone. These reductions caused LCID to extend its waiting period for EV reservations, causing demand to plummet as customers sought out EV manufacturers with shorter waiting periods.

Previously, production was a two-pronged issue for LCID. The first prong was supply chain issues and the second was production capacity. The first issue is mostly resolved due to waning COVID restrictions in China, and LCID’s deal with Panasonic for batteries. Now LCID needs to shift its attention toward increasing production capacity.

As is, LCID is planning to increase its Arizona plant’s production capacity to 365 thousand EVs annually. Additionally, its Saudi Arabian facility is projected to produce 155 thousand EVs annually in 2025. Together, these facilities should notably improve its production capacity, but funding is necessary.

Funds for Production

To raise the capital for improving its production capacity, LCID recently announced a $3 billion offering consisting of a $1.2 billion public offering totaling 173.5 million shares, and a $1.8 billion private placement of 256.6 million shares with its majority shareholder the PIF. Although this capital raise will significantly dilute shareholders, these funds are critical for LCID to scale production – benefiting the share price over the long term.

Currently, LCID has a $900 million cash balance and $2 billion in short-term investments. Once the $3 billion from this offering are factored in, LCID will have around $6 billion in liquefiable funds which is unprecedented for an EV startup. I believe these funds are enough for LCID to increase its production leading to more demand as the wait time decreases.

PIF Backing

This is not the first time the PIF came to LCID’s aid. In late 2022, the PIF contributed $915 million in capital to LCID and provided LCID with a 100 thousand vehicle purchase order from the Saudi government. It is clear through its actions that the PIF views LCID as an important part of its Saudi Vision 2030 and as such the PIF will likely continue supporting LCID.

Saudi Arabia’s 2030 Vision plan is chiefly focused on creating a diversified economy no longer reliant on fossil fuels. To achieve this, the country is pushing more of its labor force toward the private sector, and the EV market plays an important role in those plans.

After their attempts to enter the traditional ICE market failed in the past, it seems the EV market is a second chance for the country. Lucid’s new EV factory in Saudi Arabia will be completed by 2025-26 and together with KSA’s own EV brand – Ceer – they are expected to produce 500 thousand EVs annually starting in 2030.

The government of Saudi Arabia is also promoting Lucid’s vehicles since it has agreed to purchase 100,000 vehicles from LCID over the next 10 years for use by government-related employees. This will help promote Lucid’s image in the region.

With this level of production in the region, I believe Lucid will begin exporting to developed countries in the Gulf. The UAE is already primed for EV adoption and could become a promising market for LCID moving forward.

TSLA: A Tale About Dilution

While Lucid’s future looks promising thanks to its production plans in Saudi Arabia, this latest round of dilution has shaken investors’ confidence in the company. However, it’s important to note that all EV startups dilute.

The most prominent example of this is Tesla, Inc. (TSLA). Without dilution, TSLA would never have obtained the capital required to scale production. When TSLA went public it had 110 million shares outstanding, now that figure is 3.1 billion.

Through dilution, TSLA was able to scale production and develop new vehicles which allowed TSLA to become the EV industry leader it is now.

I believe LCID is now at a point where dilution is a necessity to scale which is why I believe the offering is a positive more than a negative. If LCID is able to maximize its production as a result, then it will be the right decision for the long-term despite the short-term pain.

Entering China

LCID appears to be taking another page from TSLA’s book now that its head of China operations, Zhu Jiang, has announced the company’s intention to enter the Chinese market. LCID is expected to sell imported cars while it considers local production in China. By entering the world’s largest EV market, LCID has a golden opportunity to increase its sales significantly given the high demand for EVs in China.

It’s worth noting that TSLA’s decision to manufacture vehicles in China, helped it achieve profitability in 2020 when the company began delivering these vehicles. Therefore, this decision marks another promising opportunity for Lucid – likely made possible by the company’s recent capital raise.

Technical Analysis

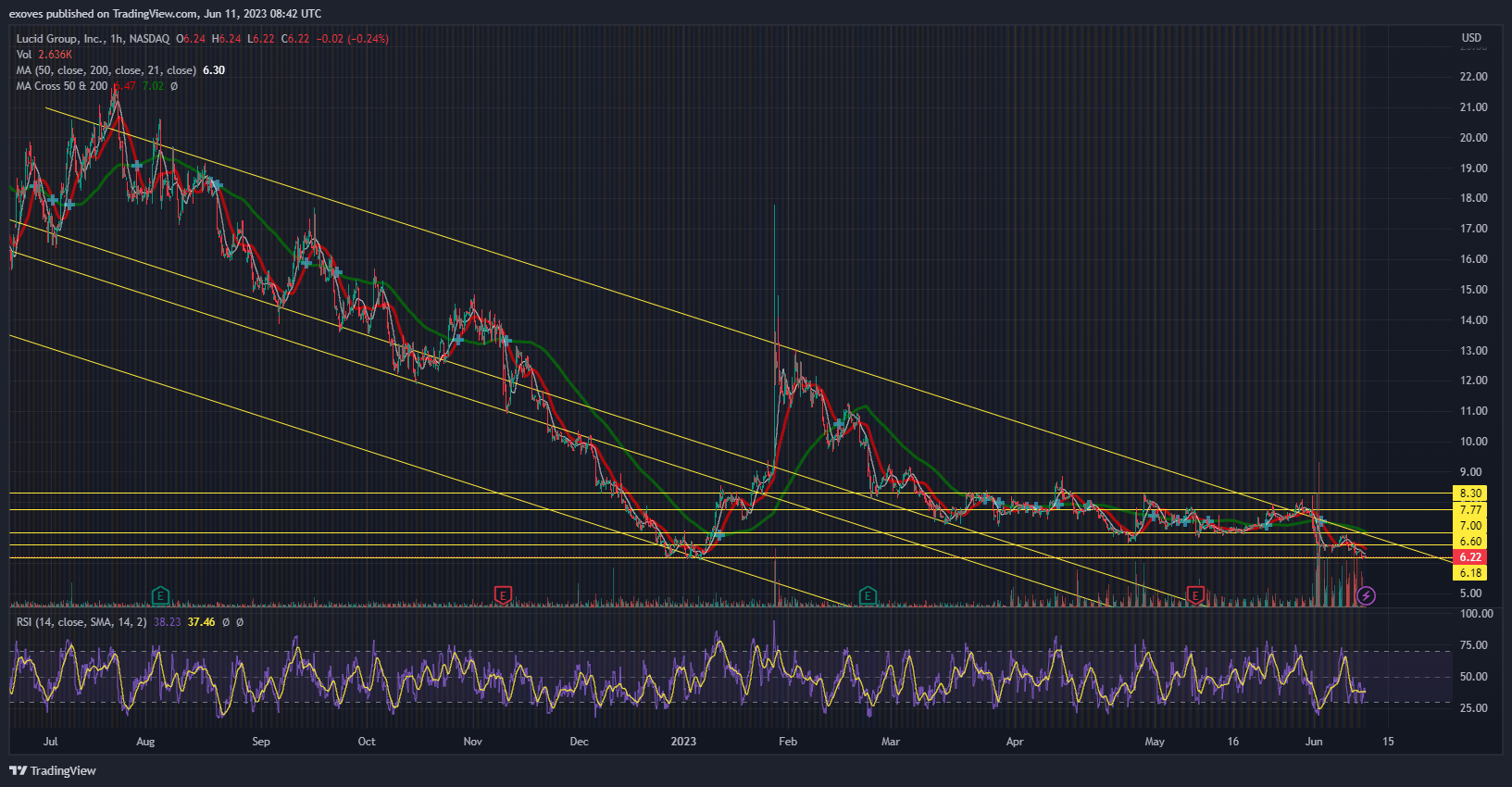

Tradingview

LCID has been trading in a downwards channel on the hourly timeframe, but a sideways channel may form. Looking at the indicators, LCID is trading below the 200, 50. and 21 MAs and the RSI is at 38.

Right now, LCID is testing a support formed in January 2023 when LCID formed a new all-time low. After consolidating at this level in January it ran more than 95%. While this run-up was fueled by a number of factors, it does highlight LCID’s ability to recover from this low if the new capital is used to trigger growth over the next quarters.

Therefore, I see upside for the stock in the long-term now that the company has nearly $6 billion in highly liquid assets, to improve its production capabilities and scale production. While I believe LCID is a buy, I urge investors to wait and see if the support level holds before taking a new position or averaging down.

Risks

Despite the progress LCID is making, its cash burn is a risk that investors should consider. Even with $6 billion in liquid assets, as LCID scales production, the company’s cash burn rate could increase exponentially from the $921.5 million it reported in Q1 2023.

As is, LCID’s gross profit margin is concerning. In Q1, LCID realized $149.4 million in revenues, however, its cost of revenue was a staggering $500.5 million – leading to a gross profit margin of -2.35.

If LCID is not able to control its ballooning costs then it might burn through a huge chunk of its recently raised cash over the coming quarters. For example, if LCID sells double the 1,406 vehicles it sold in Q1 as a result of its expected increase in production, its cost of revenue could exceed $1 billion – meaning the company may need to raise more cash in the future.

A second risk is demand. The company laid off 18% of its workforce in March – a sign that demand is potentially weakening. Additionally, of the 2,314 vehicles produced in Q1 2023, only 1,406 vehicles were delivered. This may be a sign that LCID is finding it difficult to convert reservations into orders. Resolving delays in deliveries may help demand recover, but there is no assurance that this is the only problem facing demand.

Conclusion

After dropping 24% since announcing the $3 billion capital raise, I believe LCID is a dip buy opportunity. Following this capital raise, LCID will have $6 billion in liquid assets that will be used to scale production and add value to the company in the long term.

At the same time, I see the PIF’s participation in the capital raise as a bullish sign since the PIF has shown its commitment to helping LCID grow. This combined with its entrance into China’s EV market are reasons to be bullish on the stock which is why I believe LCID is a buy at its current price.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.