Summary:

- McDonald’s management team announces a 25% hike in royalties from franchisees, but it will only apply to new locations in the US and Canada.

- The increase in royalties is part of McDonald’s long-term strategy to create additional value for shareholders.

- The company is focusing on digital initiatives, delivery services, and automated stores to stay ahead in the competitive fast-food industry.

Jeff J Mitchell/Getty Images News

On September 22nd, the management team at McDonald’s (NYSE:MCD) made a surprise announcement that, for the first time in 30 years, McDonald’s will raise its royalty fees. The hike from 4% royalties to 5% might sound fantastic for some and scary for others, depending on whether you are a shareholder or a franchisee. When you really dig into the announcement and apply it to the bigger picture, you start to see that, in the near term, this will not change the investment outlook of the company. However, it is yet one more sign that management is forward-thinking and is planning for the long haul. Down the road, this will result in additional value for shareholders, as will other long-term initiatives that management has implemented in recent years. And for those who are already bullish on the company, this is yet one more reason to be a fan.

Setting the record straight

From my experience, headline news can often be deceiving. This is because there is an incentive to sound sensationalistic about developments for the sake of drawing additional readers or viewers to the content in question. No doubt, many shareholders and market watchers probably had a very specific interpretation of management’s announcement. After all, a significant portion of the company’s revenue and profits comes from the royalties that it charges franchisees. So to see a 25% hike from 4% to 5% sounds like it could bring in tremendous amounts of additional cash each year. Likewise, for those who are franchisees, it can signal additional costs in a highly competitive and low margin business.

McDonald’s McDonald’s

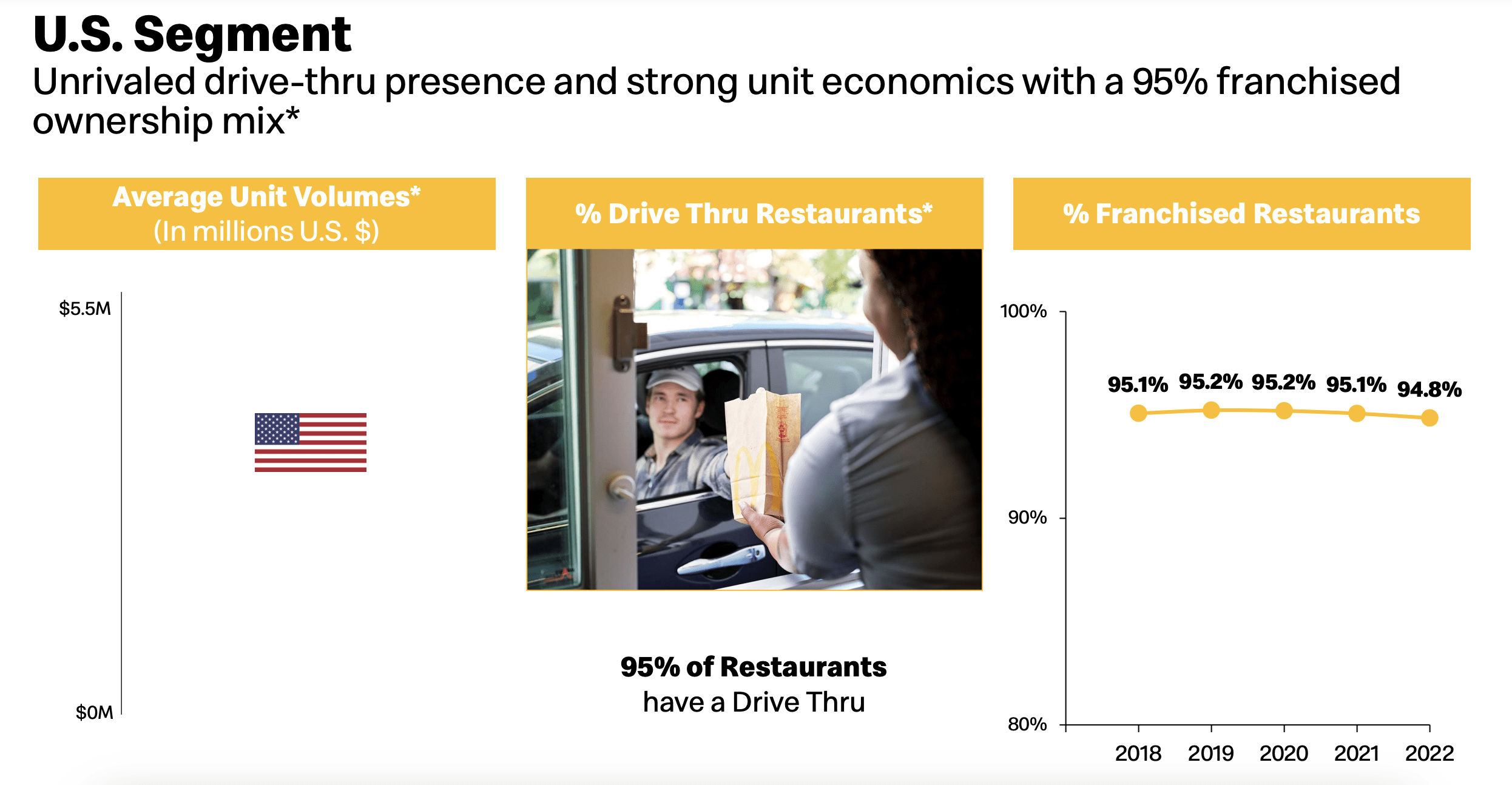

To be very clear, the 5% royalty rate that the company is going to start charging as of January 1st of next year will only apply under certain circumstances. In the two sections of text shown above, you can see the specifics of how this hike will work and who it will impact. Most notably, it will mostly impact owners of new locations. Globally, McDonald’s already charges 5% to its franchisees. The exceptions to this for franchised locations involve the restaurants located in the US and Canada. So the hike really does just apply to these two countries.

McDonald’s

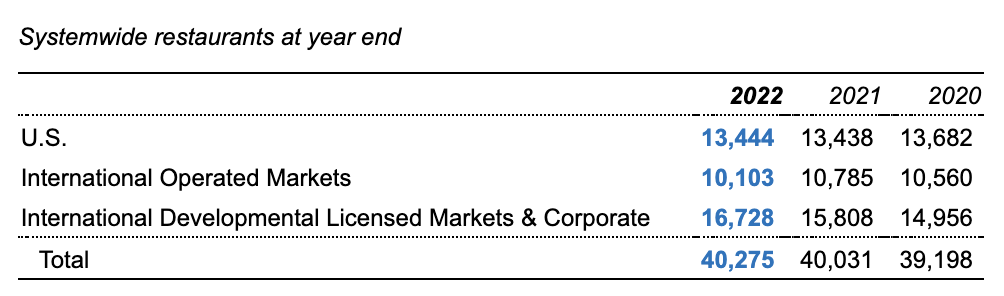

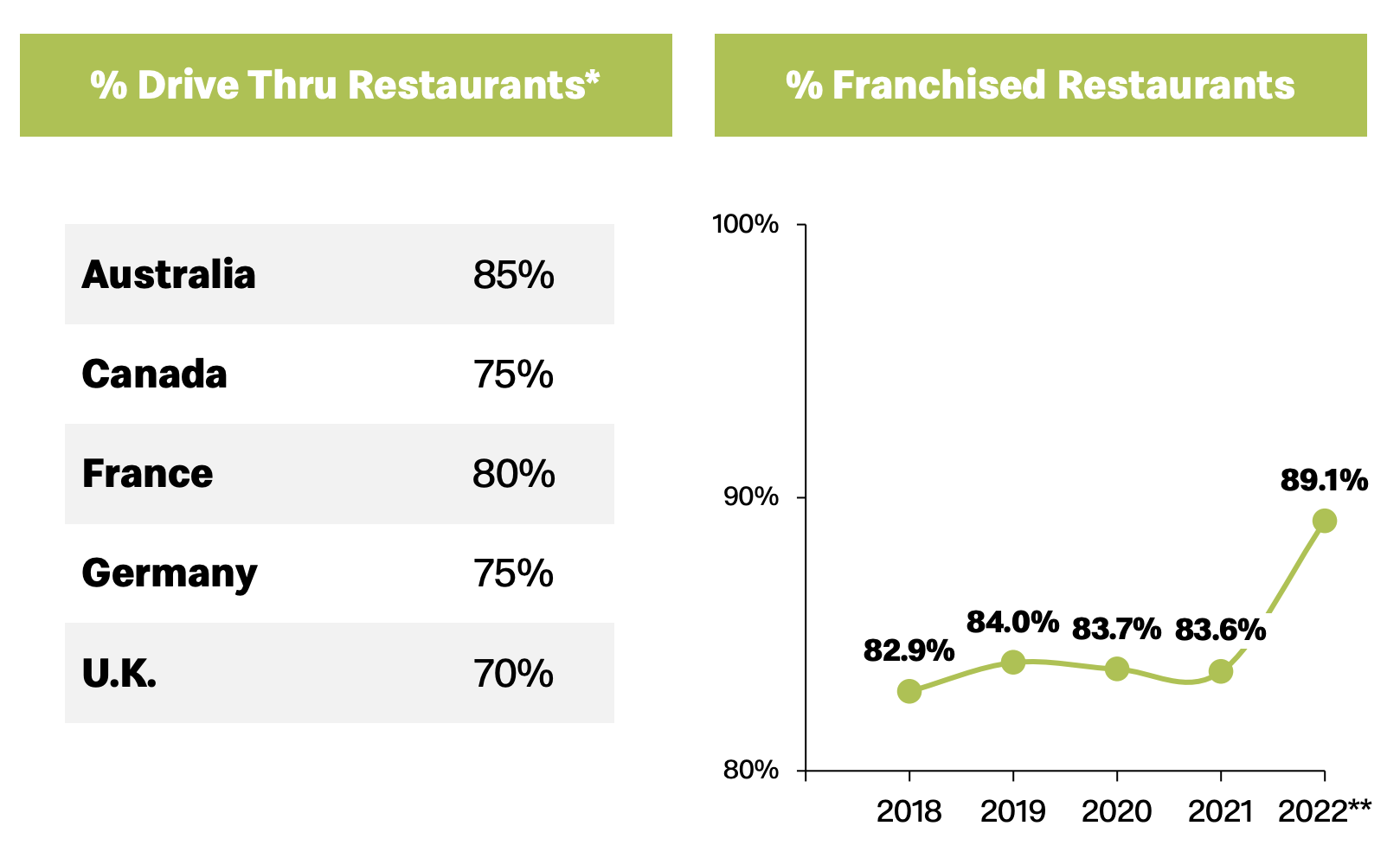

Across the globe, as of the end of the 2022 fiscal year, McDonald’s had 40,275 restaurants. The US market consisted of 13,444, while Canada was home to 1,462. We do know that, in the US, 94.8% of the company’s restaurants were franchised at the end of last year. We don’t actually know what this number is for its locations in Canada. And this is because those locations are grouped together with Australia, France, Germany, and the UK. Prior to the company selling off its operations in Russia, that country was also included in the group. And that sale illustrates just how varied the franchise rate can be from country to country. In 2021, 83.6% of the restaurants in this group were franchised. But after the operations in Russia were sold in the second quarter of 2022 because of the conflict in Ukraine, that number spiked to 89.1%. Regardless, it is clear that the majority of the restaurants in Canada are also franchised out.

McDonald’s

Anybody looking at the data over the span of a few years might initially think that the increase in the franchise rate is all for show. After all, the number of locations in the US actually shrank from 13,682 in 2020 to 13,444 this year. But that decline is deceptive. I say this because, in 2022 alone, across all of its markets, McDonald’s opened 1,576 restaurants and closed 1,332. And again, any new locations that end up being opened will be impacted. Management did say that, this year alone, it plans to open over 400 restaurants in the US and in its International Operated Markets segment, on top of another 1,500 that will be opened under developmental licenses. In any given year, the firm said that hundreds of locations will ultimately be affected.

McDonald’s

On its own right now, I don’t believe that we are likely to see a significant impact on the business given this particular change. As an example, if this were to apply to 400 restaurants, and based on an average revenue per restaurant of $3.41 million per year, it would translate to roughly $13.7 million in additional revenue for the company, almost all of which would be pure pre-tax profit. But if the company opens 400 new restaurants each year that are affected by this, then we would be looking at over $900 million in cumulative pretax profits that the company otherwise wouldn’t have seen over the span of 10 years. And that excludes any increases in revenue that the stores will see between now and then.

Author – SEC EDGAR Data

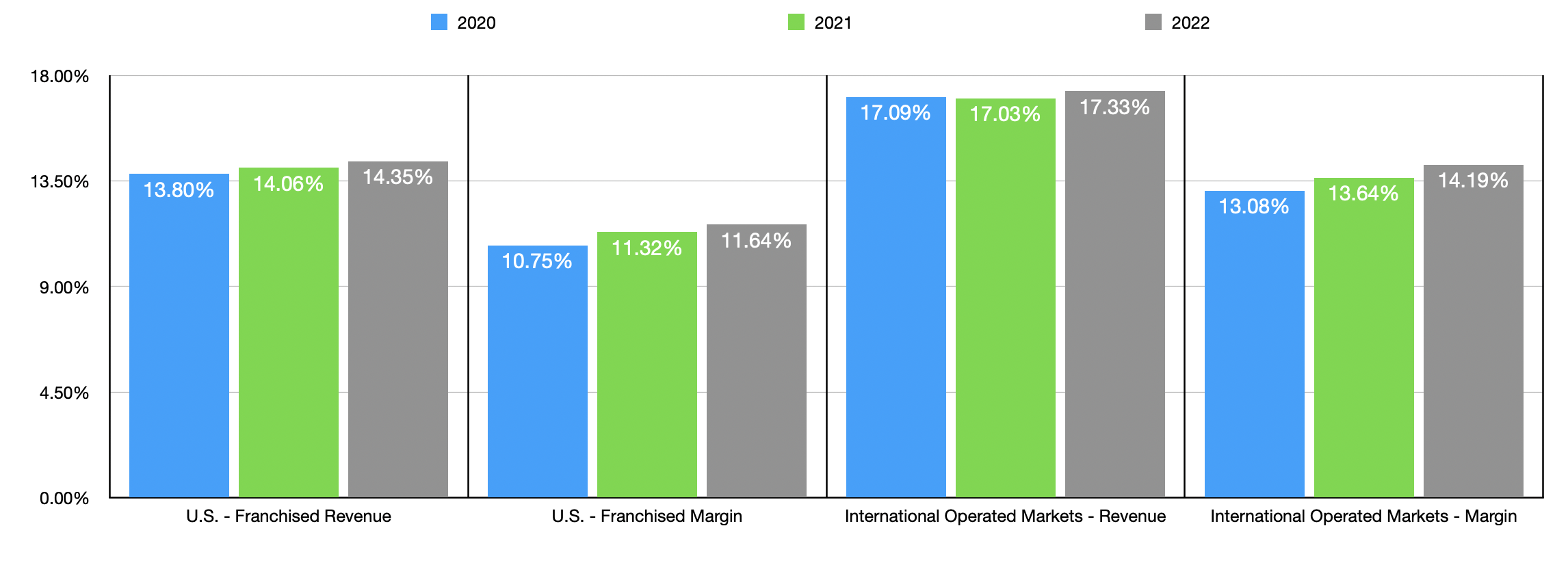

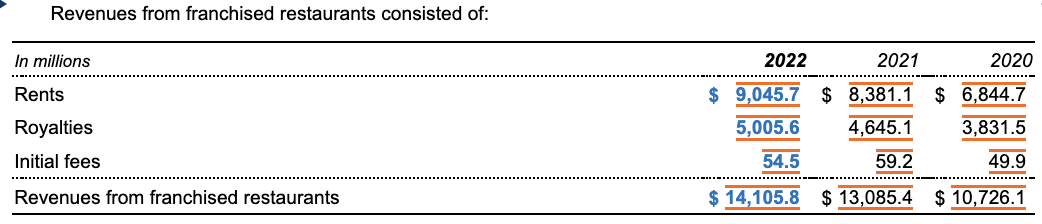

Of course, this is not the only driver that the company has for creating additional shareholder value. Over the past three years, the firm has seen its profit margins associated with its US franchised operations climb from 10.75% to 11.64%. A small portion of this increase came from actual franchise revenue. But the lion’s share was driven by higher rents that the company was able to extract from its partners. Owners of franchised restaurants went from paying $6.84 billion in rents to the company in 2020 to $9.05 billion last year. In the U.S. market, this was responsible for pushing total franchise revenue that the company collected from $5.26 billion to $6.59 billion, with the take relative to total franchised systems revenue growing from 13.80% to 14.35%.

McDonald’s

It’s all about the long haul

Regardless of what your perception might be of the food that McDonald’s serves and the experience that it offers its guests, at corporate, management seems to be incredibly focused on the long run. The decision to hike franchise fees, for instance, is something that will play a role in the company’s future, but it will not have any real impact today. There are other decisions management has made in recent years that have solidified my view that management is very forward-looking.

For instance, in recent years, a transition from picking up your food at a restaurant to having your food delivered to you has been occurring. According to one source, in 2020, food delivery revenue surpassed $26 billion. And by 2025, it’s expected to grow to $43 billion. Already, McDonald’s offers delivery in around 100 of its markets, representing 85% of all of its restaurants. While the company does have long term partnerships with the major food delivery platforms, it has also integrated delivery service into its app. In fact, management is adamant about focusing more and more on all things digital. 40% of its systemwide revenue in its top six markets last year came from digital means. And this has been energized by the company’s massive loyalty program that operates in 50 different markets. In just the top six markets that it has a presence in for its loyalty program, there are over 50 million active MyMcDonald’s Rewards members.

Late last year, the company even went so far as to open up a test concept in Texas that is automated to a large extent. In theory, a fully automated location would be cheaper to run, physically smaller in size (thereby making it cheaper to build and maintain), and it would be more efficient. Though management has not connected the dots publicly, I would also argue that the firm’s decision to get rid of self-service beverage machines across the US by 2032 might also be connected with this since the shift toward delivery and digital, combined with automated stores, would render the demand for self-service beverages much lower than if the company maintained the status quo.

McDonald’s

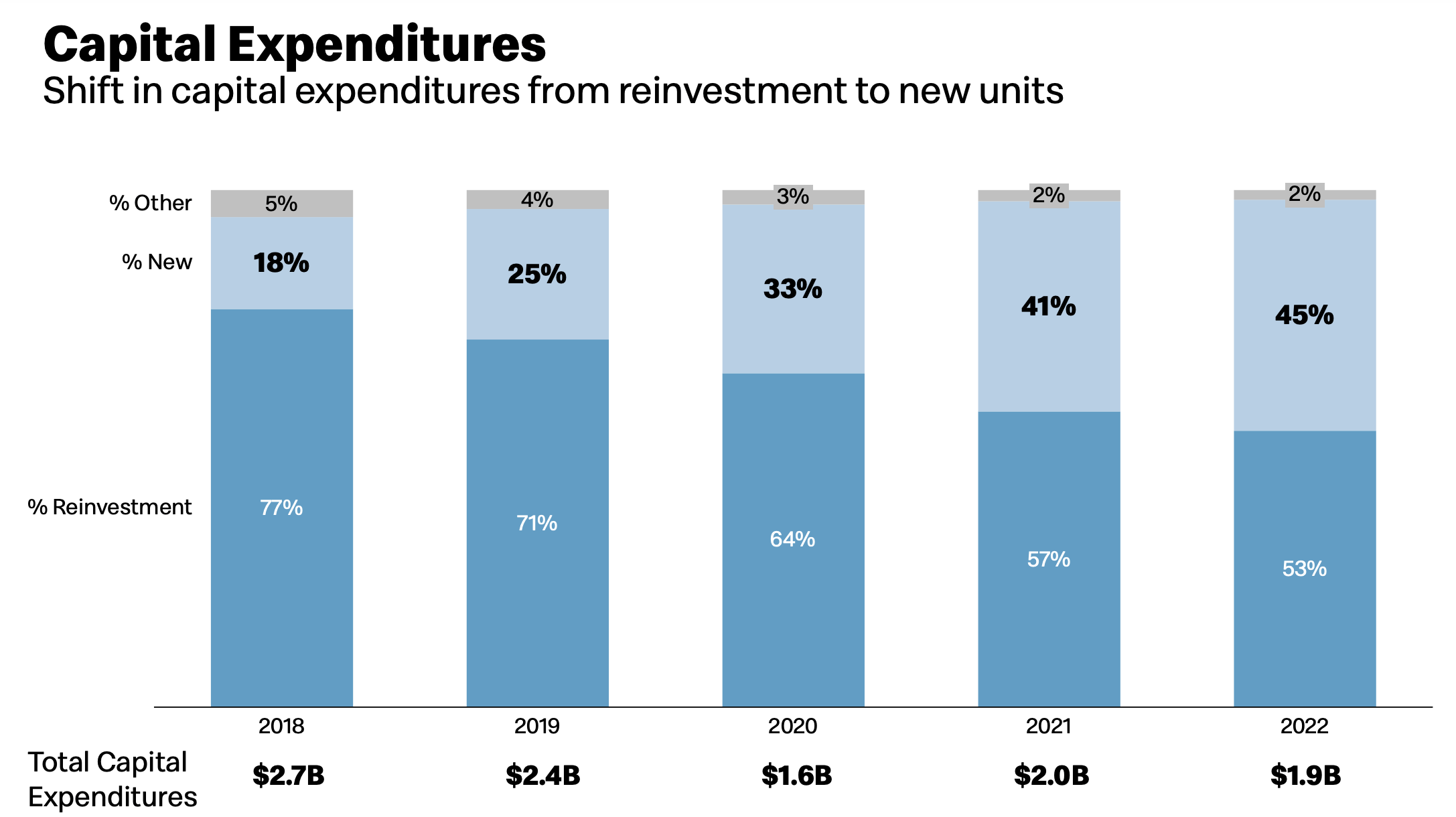

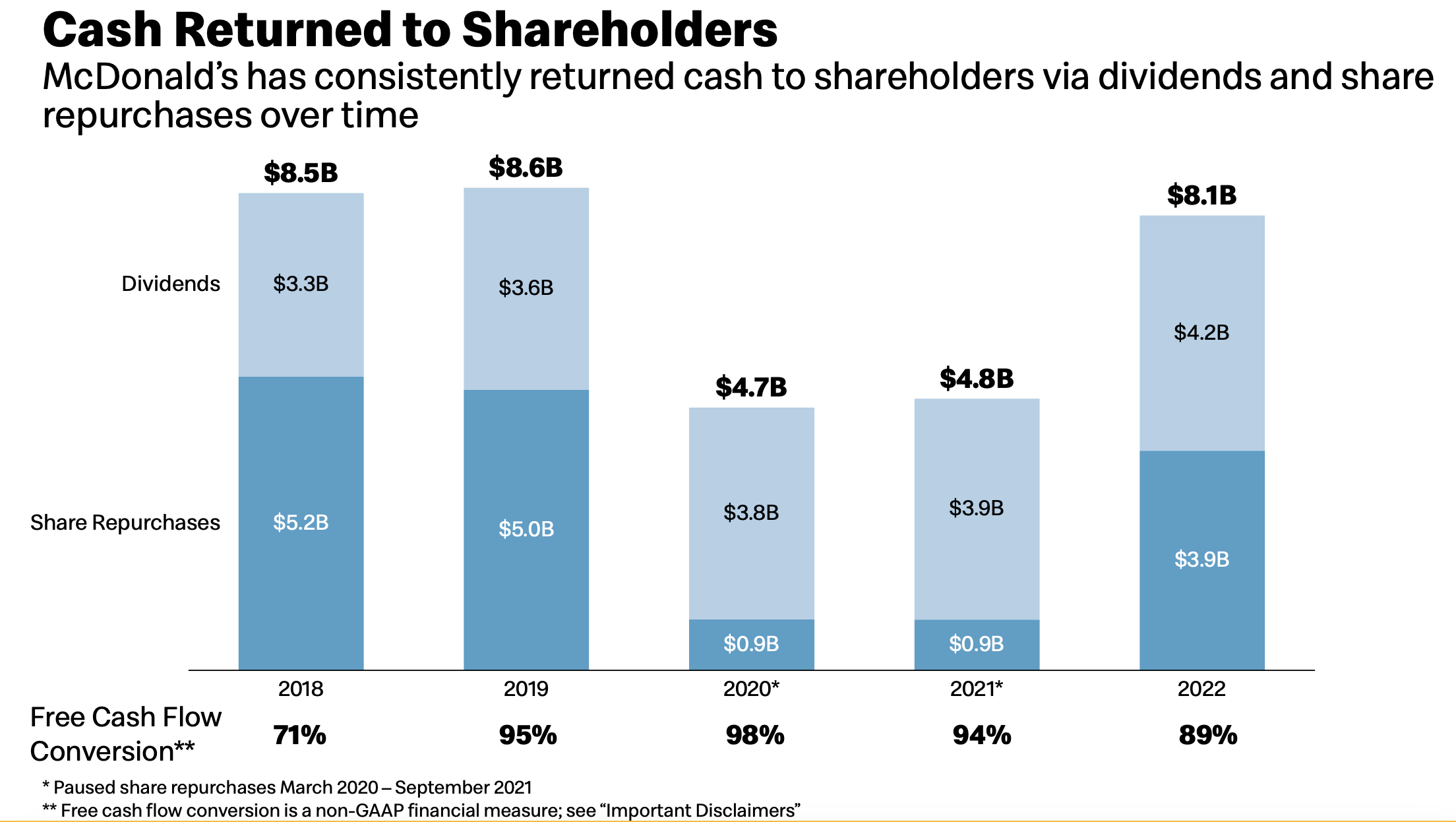

All of this comes at a good time for the company because it is quickly pulling back on years of costly investments aimed at existing locations. Back in 2018, for instance, McDonald’s spent $2.7 billion on capital projects. 77% of that funding went into existing locations. By comparison, only 18% went toward new stores. Last year, the company spent $1.9 billion, with only 53% going toward existing locations and 45% allocated toward the construction of new units. As I mentioned already, this year, the company expects to open 1,900 locations. This represents a sizable increase over the 1,092 restaurants opened last year and the paltry 503 locations that were opened in 2020. And because of how much cash the company generates as a whole, yeah it continues to pay out significant amounts of capital toward dividends and to further share repurchases. In 2022, for instance, the company allocated $4.2 billion toward dividends, on top of another $3.9 billion that went for share repurchases.

McDonald’s

Takeaway

Even though McDonald’s is a controversial company because of a number of reasons, it is a firm that is making some interesting moves. The latest, which is the decision to increase the royalties it charges franchisees, is not a play on today. Rather, it is setting up the company for the long run. Along the way, the company continues to make other interesting maneuvers with the purpose of increasing shareholder value. We are transitioning away from reinvesting in existing locations to building new ones for the purpose of growing revenue. The company has already been successful in generating even more revenue from the rents that it charges its franchisees. It’s making interesting investments in digital concepts and delivery, while simultaneously testing out new restaurant formats that could put it at an even greater competitive advantage compared to similar quick service restaurants. All combined, I see these as good reasons to be bullish about the company and its prospects in the long run.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!