Summary:

- Merck’s reduced profit guidance is primarily due to recent acquisitions, but the company remains strong with potential for future growth, especially in 2024.

- Keytruda continues to be a key revenue driver, contributing 45% of Merck’s total revenue, with potential for sustained double-digit growth.

- Strategic acquisitions, like Acceleron, are broadening Merck’s pipeline, with new drugs like Winrevair showing promising revenue growth.

- Merck’s stock decline appears to have found support, making it likely to appreciate, especially as it approaches key moving averages.

JHVEPhoto

Merck (NYSE:MRK) has been a strong performer within the Pharma space over the last several years, but is down this summer, following earnings and full-year profit guidance cut. Despite this, Merck remains one of the stronger performers among large healthcare equities, and is likely to return to all-time highs within the next several quarters, and potentially within 2024.

There are multiple reasons for the reduced profit guidance, including the slowing growth seen by versions Gardasil, its Human Papillomavirus vaccine, and a near halving of revenue from Merck’s COVID-19 therapy Lagevrio. Nonetheless, it appears that the key driver behind the change to profit guidance was the one-time impact from recent buyout deals, which Merck anticipates will reduce full-year earnings by $0.77 per share.

Other recent concerns may include the large cut to Medicare pricing for Januvia, Merck’s diabetes drug. Among the ten drugs for which the U.S. negotiated lower pricing, Januvia sustained the largest percentage reduction, with a 79% price cut from the 2023 list price.

Despite that reduced profit guidance, Merck also raised its full-year revenue guidance to $63.4-$64.4 billion from $63.1-$64.3 billion. Also, if we look at Merck’s actual reduction to its 2024 profit guidance, it lowered the full-year earnings outlook to $7.94-8.04 from $8.53-8.65. This reduction is actually less than the impact from recent acquisitions, indicating that continuing operations are continuing to perform in line with expectations, and would likely prior beat full-year guidance if those acquisitions were not made.

Another way of looking at this is that if we remove the $0.77 reduction in acquisition costs from Merck’s profit outlook, the company may have increased its full-year profit guidance. This is also less than a ten percent change to Merck’s full-year profit guidance, and those acquisitions may result in meaningful additions in coming years. After all, Merck does need to broaden its drug portfolio in order to reduce concentration risk.

The key product within Merck’s portfolio of drugs continues to be Keytruda, which brought in approximately $7.3 billion in sales during the second quarter of 2024. Keytruda quarterly revenue grew by about 16% year-over-year and beat expectations by roughly $100 million. Keytruda made up roughly 45% of Merck’s total quarterly revenue, which came in at about $16.1 billion. This also represented year-over-year revenue growth of about seven percent.

It should also be noted that, Winrevair is starting to hit Merck’s results after its FDA approval for pulmonary arterial hypertension this March. Winrevair was acquired along with Merck’s 2021 buying of Acceleron Pharma, In its first full quarter of selling Winrevair, the drug brought in about $70 million in revenue, and this is likely to increase in coming quarters. Winrevair’s growth may not be apparent within the second half of 2024, as it is possible that this first quarter’s numbers were partially helped by the initial stocking of inventory.

While I anticipate that Keytruda growth should eventually slow due to the significant size it has already reached, as well as eventual patent expiration, the drug continues to be approved for additional indications, including for earlier lines of therapy. By broadening the lines of applicable usage, it is entirely possible that Keytruda could sustain double-digit revenue growth for the next several years. Further, Merck is working on a subcutaneous formulation of the drug that may be applicable for about half of current Keytruda indications. This advancement could extend patent protection into the late 2030s. The subcutaneous formulation is currently in Phase 3 development.

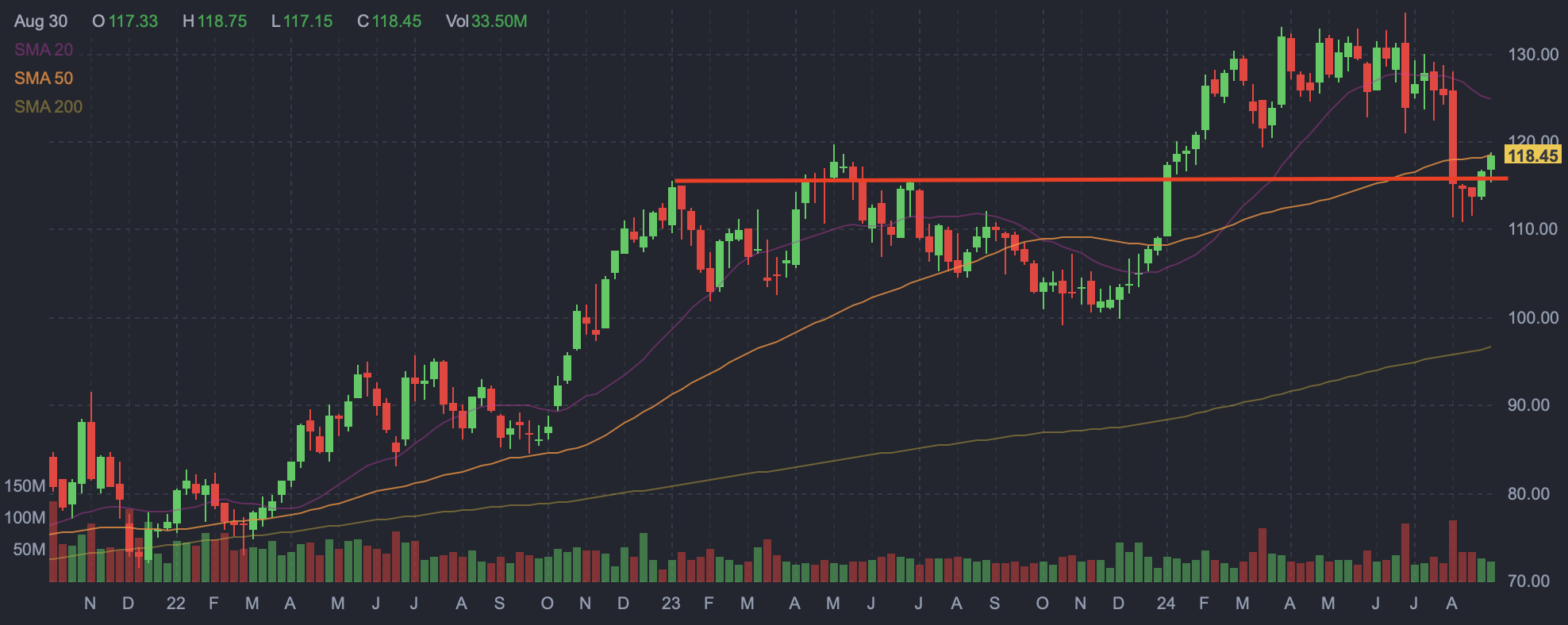

Merck’s chart also looks supportive at current levels. The decline in late July and early August took Merck shares down to pricing that acted as resistance throughout the first half of 2023. Merck performed poorly during the end of 2023, but the gapped up at the start of the year, when it quickly returned to that level, after which it continued to appreciate towards new all-time highs.

Merck weekly candlestick chart (Finviz.com with red line by Zvi Bar)

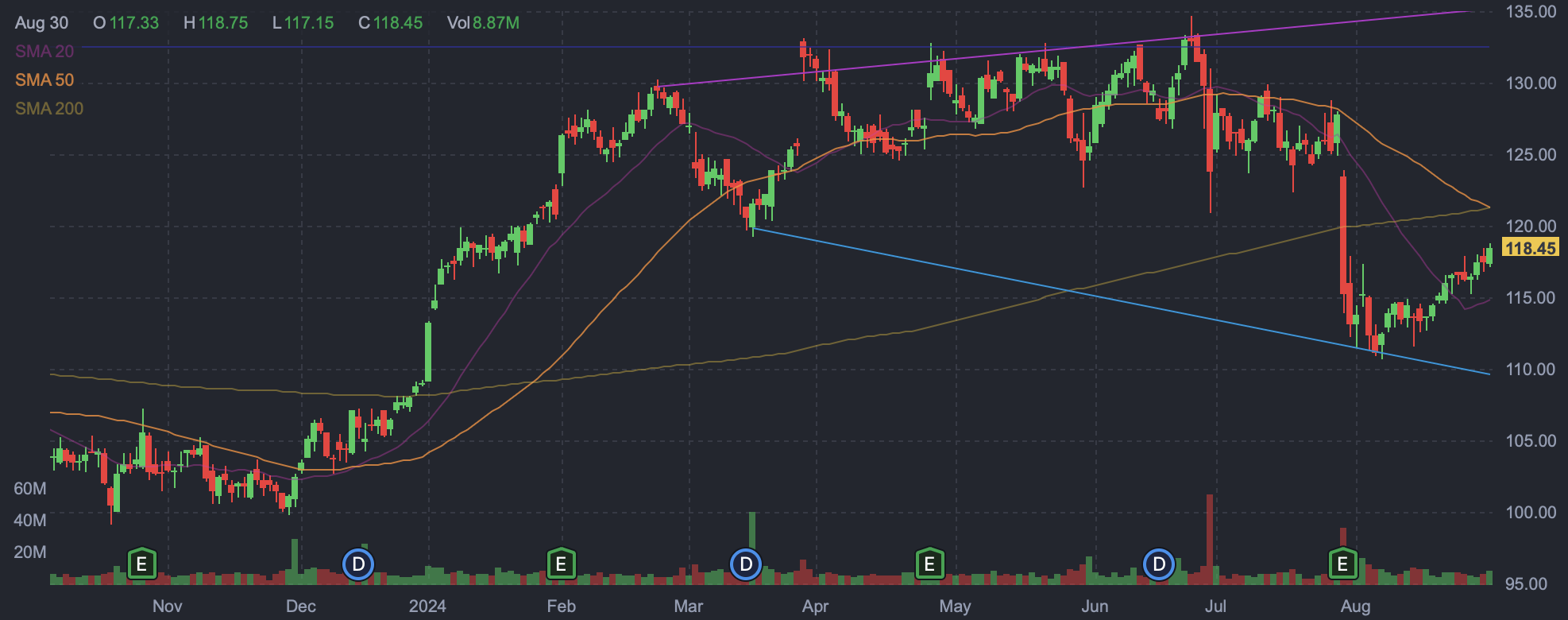

Therefore, I believe that Merck’s recent gap down took Merck shares to what is now apparent support, and that this level is likely to continue to be supportive here of another move up the charts. Merch shares are also approaching their 50 and 200-day moving averages in the low $120s, and appear likely to reach them in the coming weeks, and potentially days. A move through that level would also be supportive of a sustained climb higher.

Merck daily candlestick chart (Finviz.com)

Risks to Merck include its dependence upon Keytruda, which contributed nearly half of the company’s revenue. It is entirely possible that a competing medication will be approved, and that this competitive threat will reduce prescribing of Keytruda. It could also result in reduced pricing and related margin pressure. Further, Keytruda faces patent expiration in 2028, and this should also result in margin pressure. While Merck is working on a subcutaneous formulation that could extend that patent protection by another decade, that formulation would only apply to about half of Merck’s Keytruda prescriptions.

Other concerns include potential poor results from clinical trials. Such trials could affect the prospects of new drugs as well as the broadening of existing ones. For example, Merck recently discontinued two Phase 3 Keytruda trials due to poor benefit/risk profiles. One, KEYNOTE-867, was evaluating Keytruda plus stereotactic radiotherapy in patients with stage I or II non-small cell lung cancer, and the other, KEYNOTE-630, was evaluating Keytruda for the adjuvant treatment of patients with high-risk locally advanced cutaneous squamous cell carcinoma following surgery and radiation. Similarly, Merck stopped another Keytruda late-stage for its use as a first-line treatment of patients with extensive-stage small cell lung cancer.

Merck is also in the habit of making acquisitions, and may well need to do so in order to reduce its dependence upon Keytruda. It is possible that Merck will make additional purchases in the near term, and that such acquisitions will reduce profit guidance and/or be poorly received by the market. It is also often the case that pharmaceutical companies and actually healthcare equities more broadly sustain heightened volatility in the months prior to presidential elections.

Conclusion

Merck continues to perform well, largely due to its blockbuster drug Keytruda. While Merck does have some concentration risk, with Keytruda making up about 45% of the company’s revenue last quarter, Merck has been making strategic acquisitions that are broadening its pipeline. Further, Merck’s acquisition of Acceleron is now bringing in revenue from Winrevair, which was recently approved for pulmonary arterial hypertension and which is likely to grow over time.

Merck’s reduced profit guidance was largely due to recent acquisitions, and the market’s concern over it appears to be an over-reaction that may soon be resolved. Further, Merck’s decline appears to have bounced off of levels that were upside resistance in 2023 and which now appear to be a reasonable level of support. Therefore, shares seem likely to appreciate from here.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in MRK over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.