Summary:

- Meta Q1 results beat estimates, and Q2 guidance was strong.

- Year of efficiency is certainly paying off.

- Shares hit a new 52-week high in after hours.

Kira-Yan

After the bell on Wednesday, we received first quarter results from social media giant Meta Platforms (NASDAQ:META). The stock has been one of the market’s best performers recently, rallying more than 67% into earnings so far in 2023, as the company has looked to cut costs and get revenues growing again. The Q1 report was certainly better than expected, helping shares hit a new 52-week high and recover some of last year’s losses.

For Q1, revenues came in $28.65 billion, handily beating street estimates by nearly a billion dollars. While the 2.7% top line growth number doesn’t look impressive if you consider the company’s history, analysts were actually looking for revenues to decline by nearly 1%. Ad impressions delivered across the company’s family of apps increased by 26% year-over-year and the average price per ad decreased by 17% year-over-year.

Perhaps even more impressive for Q1 was the company’s expense structure. Meta is looking to get its operating expenses down quite a bit, and Q1 showed some pretty good progress. Total costs were up just 10% to $21.4 billion, a growth rate that was less than half of what was seen in Q4 2022, and the March 2023 period included over a billion dollars in restructuring charges. Headcount also is down 1% year over year. When you add in the ongoing help from the company’s share repurchase plan, which topped $9 billion in the first quarter, earnings per share of $2.20 smashed estimates for $1.95.

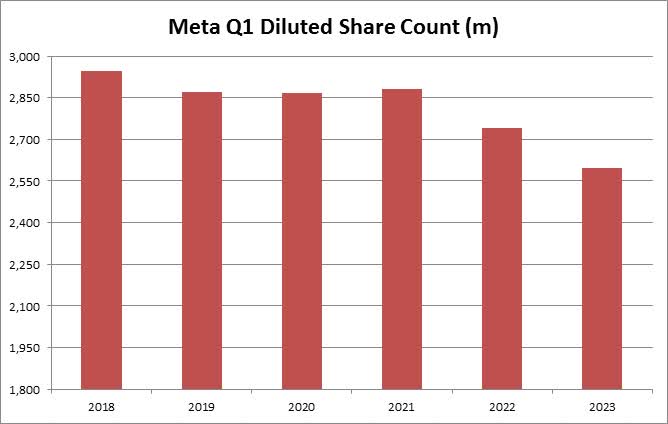

Like many large cap tech giants, Meta is in a great financial position. Cash totaled more than $37 billion at the end of Q1, against just $10 billion in debt. Free cash flow was more than $7 billion for the quarter, which at times can be the weakest period of the year due to seasonality. The ongoing buyback has lowered the share count nicely, with the diluted count used for the EPS calculation declining by almost 12% in the past five years to under 2.6 billion as the chart below shows. At the end of Q1, more than $41.7 billion remained authorized for future share repurchases.

Meta Q1 Diluted Share Count (Company Earnings reports)

As great as the Q1 results were, guidance for the current period was even stronger. Management guided to revenues of $29.5-$32.0 billion, with the low end of that range being above the street’s expectation for $29.47 billion. Revenue growth could be back into the double digits by early 2024, or perhaps earlier if this near term strength continues. More importantly, however, was that this year’s total expense forecast was lowered on the top end by $2 billion. The new $86 billion to $90 billion range, which includes $3 billion to $5 billion in restructuring costs, is down significantly from the original range of $96-$101 billion that included $2 billion in facilities charges.

Going into Wednesday’s report, the average price target on the street was just under $229. Given the Q1 double beat, the strong revenue guidance, and the lowered expense forecast, I expect we’ll see a number of analysts hiking their valuations in the coming days. If the company can do $11 in earnings this year, as compared to the $9.78 annual estimate going in, I think a valuation of about 24.5 times earnings is justified. That’s basically the average of what tech giants Microsoft (MSFT), Apple (AAPL) and Alphabet (GOOG) (GOOGL) currently trade for.

That gives us a price target of about $270, or more than 15% upside from where Meta is in the after-hours session. As the chart below shows, the stock has rebounded very nicely from its multi-year low of $88, although it is still quite a bit off its all-time high. Investors looking to buy may want to wait to see if we get a little pullback in the coming weeks, however, especially if the market pulls back on another Fed interest rate hike.

META Last 2 Years (Yahoo! Finance)

In the end, Meta delivered another very strong quarterly report. The company beat street estimates by a billion dollars on the top line and crushed analyst expectations for earnings per share. Q2 guidance was tremendous, showing that revenues are starting to grow again and by more than just a token amount. As the company continues to get its expense base in check, earnings per share upside is definitely possible, especially thanks to the ongoing share repurchase plan. I do see some nice upside for the name moving forward, but it’s a little hard to recommend jumping in right now with the stock up double digits in the after-hours session and a Fed meeting looming for next week.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.