Summary:

- Meta Platforms (formerly Facebook) has experienced a significant increase in market value, with its stock rising +240% in the past 11 months.

- META’s revenue growth has rebounded after three consecutive quarters of decline, and expenses are slowing down.

- Meta’s operating profit growth is back in the black, and its operating margin is estimated to be above 30% for 2023.

Kelly Sullivan

The following segment was excerpted from this fund letter.

Meta Platforms (NASDAQ:META) – A deep dive into what is driving the optimism for the stock

It’s been exactly 11 months since we published an article: “Does a $750 billion decline in Meta’s market cap make sense?” META is up +240% since then compared to the S&P 500 advance of +13.5% over the same time period. We will examine what drove this abnormal return. But first, we can’t help but wonder: How is it possible for a trillion-dollar company to first drop -75% to $268 billion in market cap and then skyrocket +250% to over $800 billion in market cap all in just less than 2 years. We are not talking about some micro-cap company here. META is the 7th largest company in the world. It is very well-known to everybody and is covered by 45+ analysts.

Are the markets really efficient when you witness this kind of a phenomenon?

Our belief is that the markets have actually become a lot less efficient over the short term with the proliferation of the internet, smart-phones, social media and effortless access to information. This is counterintuitive to what the academics teach us, but that is the way it has worked in reality. We will spare you further discussion on the efficiency of the markets as the purpose of this note was to discuss our investment in META. We wanted to share this observation and be clear that we are not exactly complaining here. Part of our job as fund managers is to exploit these market inefficiencies and drive value to the Rowan portfolio over the long run. And over the long run, the markets do a pretty good job in valuing companies.

What changed since last November that spurred such a drastic increase in the market value of META?

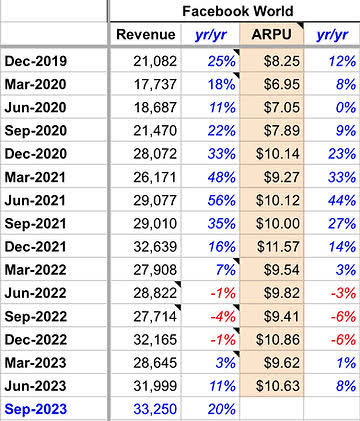

After 3 consecutive quarters of year-over-year revenue declines, which was a first in META’s history, their revenues are growing again, posting $32 billion in Q3 ‘23 (+11% growth) with management guiding to 20% growth in Q3 (see chart below):

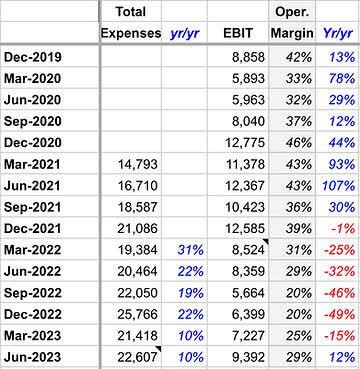

Their total expense growth, which was a major pain-point for investors in 2022, is slowing down considerably as you can see below:

After growing at a crazy pace in comparison to negative revenue growth, expenses now look in check, growing only 10% yr/yr (the latest $22.6 billion in expenses includes $1.87 billion in accrued legal expenses and $780 million in restructuring charges). The year of efficiency so far is working out quite well as META’s operating profit growth is back in the black after more than 5 quarters of significant year-over-year declines (refer to chart above). Operating margin was 29% in the latest quarter, significantly above 20% all-time lows in Q3 and Q4 of 2022. Operating margin is estimated to be above 30% again for 2023. Please note that META is able to generate these incredible operating margins despite their heavy investment in Reality Labs that caused them to lose over $15 billion in that operating unit. That is how solid META’s core Family of Apps business really is! It generates north of 40% operating margins and brought home over $44 billion in operating profits. There aren’t very many businesses in the world that can consistently generate these kinds of operating margins.

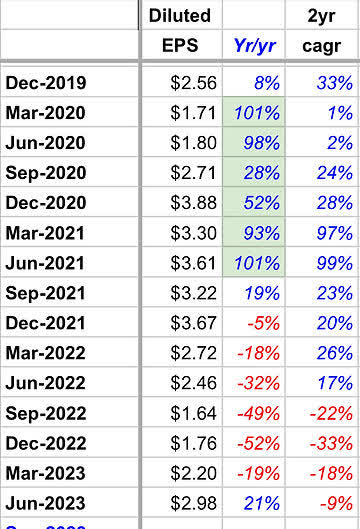

On the earnings per share (EPS) front, they delivered 21% yr/yr growth after 6 consecutive quarters of yr/yr declines. In the table below, notice the astounding growth rates in EPS back during the COVID time (2020 and 1H 2021), which fueled investor excitement and pushed their market cap to over $1 trillion. If we look at the 2 years EPS CAGR, it is still in the negative territory as we are comparing to peak Q2 ‘21 EPS of $3.61.

All of this was music to investors’ ears, and it’s astounding how quickly they went from the maximum point of pessimism in November of 2022 to lots and lots of excitement about META’s future prospects.

Let’s take a look at how the valuations have changed

In our November note, we wrote:

“Current valuations of Meta makes no sense to us”:

“Meta is estimated to make close to $120 billion in revenues this year. Gross profits are still around 80%. The core Family of Apps business generated $48 billion in operating profits over the past 12 months, and the entire market cap is currently $240 billion (5x core operating profits). Free cash flow over the past 12 months netted at $26 billion, even after the heavy capital expenditures we described above.

Since 2017, Meta had invested $210 billion into R&D and Capex — close to the current market cap. In 2022 alone, they are investing $65 billion into R&D and Capex (in comparison, Apple is doing about half of that). Is Zuck just burning through piles of cash? Given his incredible track record, his unique ability to see where the world and technology is headed over the next 10-15 years and to execute against his vision, we would not bet against him.”

Meta is now estimated to have close to $135 billion in revenues in 2023. Gross profits are estimated to top $100 billion. We estimate that operating profits in 2023 could come close to $45 billion, a significant improvement (>50% growth) from 2022 operating profits of $28.9 billion, but still shy of $46.8 billion in peak operating profits in 2021. The core Family of Apps business generated $44 billion in operating profits over the past 12 months. With the market cap currently at $810 billion, they are now trading at 18.4x core operating profits (a 3.7x jump from the November ‘22 multiple). If we adjust for $53 billion in cash they have on the balance sheet, Meta is now trading at 21.6x 2023 EPS and 17.4X 2024 estimated EPS. Although no longer “dirt-cheap” as it was a year ago, in our opinion, this seems like a very reasonable multiple to pay for a high quality franchise like META and the long term growth opportunities of this investment. If we take a look at its mega cap tech peers (Apple, Microsoft, Alphabet, Amazon), they are all trading above that multiple. We expect Meta to now generate over $32 billion in free cash flow in 2023, even after a massive $28 billion in Capex. This represents about 4.4% free cash flow yield, which we believe should grow at double-digit rates over the next decade. Compare that to the current 10-year treasury yield of 4.6%, which is guaranteed not to grow.

In our November note, we talked about the three pressing issues that Zuck & Co. have been dealing with:

-

Competitive threats from TikTok

-

Signal loss from Apple’s iOS changes

-

Economic downturn that is having a broad impact on digital advertising business

Let’s see how Zuck has addressed these issues thus far. First off, many don’t realize that despite all the competitive threats and numerous rumors that “no one uses Facebook anymore”, Facebook continues to grow globally and engagement remains strong. In 2023, for the first time, they crossed 3 billion monthly active users (MAU); daily active users (DAU) were 2.1 billion, up 5% year-over-year.

On the first two issues above, the investments that Meta made over the years in AI, including billions of dollars they’ve spent on AI infrastructure, are clearly paying off across their ranking and recommendation systems and improving engagement and monetization. Here is what Zuck said on the Q2 ‘23 call:

“AI-recommended content from accounts you don’t follow is now the fastest growing category of content on Facebook’s feed. Since introducing these recommendations, they have driven a 7% increase in overall time spent on the platform. This improves the experience because you can now discover things that you might not have otherwise followed or come across.

Reels is a key part of this Discovery Engine, and Reels plays exceed 200 billion per day across Facebook and Instagram. We’re seeing good progress on Reels monetization as well, with the annual revenue run-rate across our apps now exceeding $10 billion, up from $3 billion last fall.

Beyond Reels, AI is driving results across our monetization tools through our automated ads products, which we call Meta Advantage. Almost all our advertisers are using at least one of our AI-driven products. We’ve also deployed Meta Lattice, a new model architecture that learns to predict an ad’s performance across a variety of datasets and optimization goals. And we introduced AI Sandbox, a testing playground for generative AI-powered tools like automatic text variation, background generation, and image outcropping.

AI is quickly becoming another driver of growth for META

Barclays analyst has recently pointed out that “Meta Platforms may be poised for a new tipping point as it relates to artificial intelligence… Users may have a new ‘interaction layer’ to access information and transact via Meta’s four mega-apps: Whats App, Messenger, Instagram and Facebook.”

At the Meta Connect 2023 Event last month, the company announced new AI tools, including personal AI assistants with 28 AI personality characters, which can help users with tasks such as finding information, controlling devices, and translating languages. Meta is also developing AI-powered tools for creators, such as AI dubbing tools and AI background generators. These new products and services have the potential to revolutionize the way people interact with technology and with each other.

What’s even more exciting for us as investors is that after spending the past five years as a wartime CEO, Zuckerberg is finally getting back to exactly what he thrives at, which is innovation and creating amazing products. As he put it in one of his recent interviews: “For the next wave of my life and for the company — I define my life at this point more in terms of getting to work on awesome things with great people who I like working with.”

A few words on the Metaverse

A majority of investors have been very skeptical and critical of Zuck’s efforts on the Metaverse as the losses for Reality Labs have been substantial. However, our hat is off to Zuck for continuing to persevere on his vision on the next computing platform that he wholeheartedly believes in. That’s the benefit of being a founder/CEO that owns the majority of the voting shares. A “hired gun” CEO would never pursue such a vision and risk his career. Please take a look at this presentation — it will blow your mind!

Looks like the Metaverse is no longer just a dream that is too far off into the future — it’s officially real!

Thank you for your confidence and trust in our investment discipline. Despite a meaningful rebound in our portfolio in 2023, we see a continued opportunity to intelligently deploy capital and to deliver long-term value to our investors.

As always, should you have any questions or comments, we would be very happy to hear from you. We look forward to reporting to you again at the end of the year.

DisclosureThe information contained in this letter is provided for informational purposes only, is not complete, and does not contain certain material information about our Fund, including important disclosures relating to the risks, fees, expenses, liquidity restrictions and other terms of investing, and is subject to change without notice. The information contained herein does not take into account the particular investment objective or financial or other circumstances of any individual investor. An investment in our fund is suitable only for qualified investors that fully understand the risks of such an investment. An investor should review thoroughly with his or her adviser the funds definitive private placement memorandum before making an investment determination. Rowan Street is not acting as an investment adviser or otherwise making any recommendation as to an investor’s decision to invest in our funds. This document does not constitute an offer of investment advisory services by Rowan Street, nor an offering of limited partnership interests our fund; any such offering will be made solely pursuant to the fund’s private placement memorandum. An investment in our fund will be subject to a variety of risks (which are described in the fund’s definitive private placement memorandum), and there can be no assurance that the fund’s investment objective will be met or that the fund will achieve results comparable to those described in this letter, or that the fund will make any profit or will be able to avoid incurring losses. As with any investment vehicle, past performance cannot assure any level of future results. IF applicable, fund performance information gives effect to any investments made by the fund in certain public offerings, participation in which may be restricted with respect to certain investors. As a result, performance for the specified periods with respect to any such restricted investors may differ materially from the performance of the fund. All performance information for the fund is stated net of all fees and expenses, reinvestment of interest and dividends and include allocation for incentive interest and have not been audited (except for certain year end numbers). The methodology used to determine the top 5 performers is the best performing stocks for the quarter. The top 5 do not reflect all fund positions. The top 5 can and will vary at any given point and there is no guarantee the top 5 will continue to perform and, more generally, there is no guarantee the fund will meet any particular performance level. S&P 500 performance information is included as relative market performance for the periods indicated and not as a standard of comparison, as it depicts a basket of securities and is an unmanaged, broadly based index which differs in numerous respects from the portfolio composition of the fund. It is not a performance benchmark, but is being used to illustrate the concept of “absolute” performance during periods of weakness in the equity markets. Index performance numbers reflected in this letter reflect reinvestment of dividends and interest (as applicable). Index information was compiled from sources that we believe to be reliable; however, we make no representations or guarantees with respect to the accuracy or completeness of such data. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.