Summary:

- The year of efficiency has paid off many times over with revenue growth acceleration and significant expense reduction.

- The company has focused on using recommendation AI to drive engagement and ad impressions, resulting in a 7% increase in engagement and a 31% increase in ad impressions.

- While generative AI may be more hyped, recommendation AI is the driving force behind Meta Platforms’ success and financial health in 2023.

- Mark Zuckerberg plans on prioritizing AI in 2024 which will result in the Year Of Efficiency version 2.0.

Tero Vesalainen

Meta Platforms (NASDAQ:META) announced 2023 would be its Year of Efficiency after growing its headcount rapidly in the preceding years. Several rounds of layoffs have led to expenses shrinking while revenue growth accelerates. But this efficiency wasn’t merely laying off a good portion of its workforce; it was an alignment toward growing its AI strategy to replace the jobs of those laid off and gain better technology and business results. The Year of Efficiency has seen strong use of AI, which is only getting started as CEO Mark Zuckerberg has set the stage for the Year of AI in 2024. The execution of the combined leaning of its corporate structure while pushing headlong into AI makes Meta Platforms one of the best AI-in-action investments of the decade.

How The Year Of Efficiency Has Done It All

Typically, when a company conducts mass layoffs, its ability to operate is hampered at some level. Expenses decrease, but investments in the company’s business and its market tend to take a hit as well. After all, with fewer employees, the end result means productivity drops. It’s hard to operate with less and do more.

However, when a company lives on, innovates with, and produces technology, there are options for automation. Now, AI obviously doesn’t stand for automated intelligence, but AI at its core is complex automation. Software engineers, configuration engineers, and many other software engineering-related professionals seek ways to automate their daily work lives. This is exactly what Meta Platforms set out to do. It may have started with content moderation – replacing people looking and deciding on content with machine learning abilities to do the same – but it’s only the beginning. Meta doesn’t make a living moderating content; it makes a living providing ad agency services.

Therefore, to do more with less, something more than human intervention in its core competency – which was happening last year in the wake of iOS privacy signal issues, according to the now-resigned COO – needed to occur. And that’s where AI came in.

And Meta has rallied around this solution.

While generative AI gets all the nerds’ pants in a bunch, it’s not what’s directly helping Meta drive ads and recommendations. There’s a different AI aspect doing this called recommendation AI.

…there is also a different set of sophisticated recommendation AI systems that powers our feeds, Reels, ads, and integrity systems. And this technology has less hype right now than Generative AI, but it’s also improving very quickly.

AI-driven feed recommendations continue to grow their impact on incremental engagement. This year alone, we’ve seen a 7% increase in time spent on Facebook and a 6% increase on Instagram as a result of recommendation improvements.

– Mark Zuckerberg, CEO, Q3 ’23 Earnings Call

Mark understands it’s not as sexy as generative AI, but it’s what’s driving his company forward and crushing its competitors’ AI efforts. Notice how it’s used across all planes of the business: content feeds and moderation, but also ads. This all-encompassing solution is, in no small part, how the company drove a 31% ad impression increase year-over-year in Q3.

It’s almost like a central recommendation system works for all its very critical business areas. Yes, generative AI plays a role in some of its new ad creative products, but the financial health of the company relies on its ability to recommend content and ads.

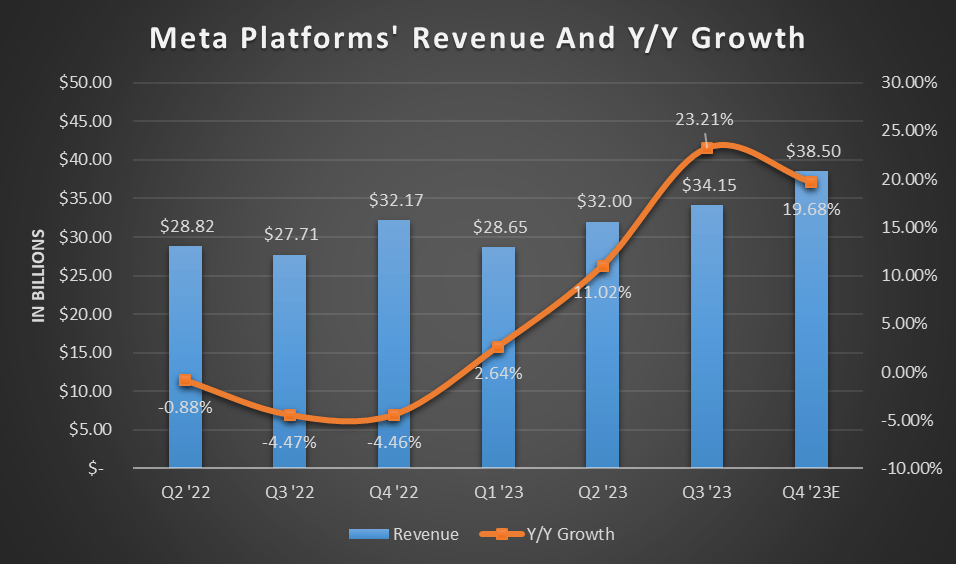

This is how the company produced accelerating revenue growth throughout this year, digging out of its hole of negative revenue growth from last year.

Chart mine, data from company press releases

But it’s also what’s allowed it to lay off tens of thousands of employees and reduce expenses. For Q3, expenses were $20.4B, down 7% from $22.05B in 2022. Moreover, at the midpoint of its full-year guide, Q4 expenses will likely come in at $23.58B versus 2022’s Q4 of $25.77B, down 8.5% year-over-year.

It goes without saying growing revenue and lowering expenses expand margins and provide a larger bottom line. It also works to provide a heftier cash flow margin. Throughout 2023, free cash flow has grown enormously even as Meta spends $28B on AI-based CapEx. The return to hefty free cash flow is a stark contrast to a very rough 2022.

| FCF | Q1 | Q2 | Q3 | Q4 |

| FY23 | $6.91B | $10.96B | $13.64B | $14.2BE |

| FY22 | $8.53B | $4.45B | $0.17B | $5.29B |

I can’t say the year of efficiency isn’t working. Revenue growth plus reduced expenses plus the return of enormous cash cow-like free cash flow says “mission well underway.” If there’s one thing CEO Mark Zuckerberg is good at, it’s achieving the goals he sets for the company. Yes, he’s had to course correct once, twice, maybe even three times, depending on how you look at it, but he manages to put the company back on the map every time. Love him or hate him, the financial improvements and results each time prove his abilities.

The Year Of AI Has Tailwinds

On that note, the next mission Zuckerberg has is what 2024’s priorities are. And you might have guessed it: AI.

…in terms of investment priorities, AI will be our biggest investment area in 2024, both in engineering and compute resources.

– Mark Zuckerberg, CEO, Q3 ’23 Earnings Call

It’s hard to imagine Meta investing even more heavily in AI than it already has in 2023, but this is the exact strategy to have. While AI continues to bake in the commercial business world, there will be a lot of breakthroughs in use cases and abilities to push what has been achieved to the next level. If you’re not one of those companies pushing the edge of this frontier further, you’ll be left behind – and quickly.

The AI strategy from a headcount perspective is playing out exactly like I said it would when I talked about Meta’s AI capabilities in June of 2022, allowing it to slow headcount growth and then cut employees. The idea was AI would be a tailwind in the face of a recession, one so far not seen as a country but certainly for online advertising. This was months before the company announced any layoffs, but I was already foreshadowing their coming:

Meta Platforms…would love to replace the massive amount of content moderators it hired over the last several years [with AI]. Naturally, it would cut down substantially on human resource costs and employee benefits (read: stock-based compensation).

And with the results it has seen in 2023, why stop?

A focus within 2024’s AI approach is business AI. This encompasses business messaging and e-commerce.

Today, most commerce and messaging is in countries where the cost of labor is low enough that it makes sense for businesses to have people corresponding with customers over text…But in lots of parts of the world, the cost of labor is too expensive for this to be viable. But with business AIs, we have the opportunity to bring down that cost and expand commerce and messaging into larger economies across the world. So making business AIs work for more businesses is going to be an important focus for us into 2024.

– Mark Zuckerberg, CEO, Q3 ’23 Earnings Call

Why is this important? Two reasons: first, it’s differentiation from advertising; it’s a pay-to-message system, and second, it provides easy monetization for an underserved aspect of e-commerce. With AI, it becomes not only scalable but learns through the success and failures of direct sales. As machine learning, well, learns, it builds on itself.

…as we are able to roll out the business AIs, I think that, that can really unlock and grow the business – messaging business in a big way…

– Mark Zuckerberg, CEO, Q3 ’23 Earnings Call Q&A

For Meta, this can explode if done properly and wouldn’t rely on economic advertising cycles to work. While AI messaging isn’t free either, it could be an easy win-win scenario, much like injury attorneys: no settlement, no fee. So, even in difficult economic times, you only pay for the lead if you close a sale. This differs significantly from advertising with a low or zero follow-through rate; nothing’s guaranteed when spending money on ads. But this messaging and e-commerce AI approach aligns with the seller’s and Meta’s interests and can provide an economically resilient product from Meta.

But this focus on business AIs isn’t in a vacuum.

Add together continued improvements with AI in the areas I touched on earlier, and it begins to snowball in 2024.

For example, Reels turned from a headwind to neutral to ad revenue quicker than expected. This could only have been done with the recommendation AI improvements over this year and the culmination of those efforts coming into this year.

[We] are now at a level where Reels is neutral to overall revenue…it has now become part of the core experience on Instagram and Facebook. As such, we don’t anticipate quantifying the net revenue contribution from Reels going forward. We will still work to further improve Reels ads performance through ranking improvements and making Reels ads increasingly interactive, while also growing supply to give businesses more opportunities to get in front of people. We anticipate this ongoing work will help Reels be a modest tailwind to revenue in 2024 while we continue to strike the right balance between engagement and revenue growth.

– Susan Li, CFO, Q3 ’23 Earnings Call

Expect Reels to go from lagging to leading as the company refines and hardens its AI systems.

What 2024 really becomes is the ‘Year of Efficiency v2.0’. Since the way to get there is through AI improvements and progress, efficiency becomes a by-product of the effort. This is why I called out AI as being one of the most necessary aspects of a company in 2022. It’s because 2023, 2024, and the many years ahead will require companies to do more with less headcount. A weaker and more volatile macro environment will necessitate less overhead to operate with decent margins. But this transition simultaneously allows for doing more, not just maintaining the status quo financially.

The Price Of AI In Action

While I don’t expect continued acceleration of revenue growth into 2024 as the company will begin lapping its better 2023 performance, it doesn’t negate the continued profit growth from the new efficiencies. This is why I outlined the cash flow and how it has created breathing room for the company, allowing it to return capital to shareholders and invest at a level necessary to remain a leader in the industry.

But this also drops the valuation from an earnings standpoint and brings value back to the stock. I’ve modeled 2024 EPS of $17.97 (consensus is currently $17.27) using an average net margin of 31% (Q3 ’23 was 34%) as the company plans on backfilling some headcount with AI-priority positions. I’ve more or less maintained the share count to amount for net-zero effect buybacks to stock-based compensation. At Friday’s close of $314.60, this is a forward P/E of 17.5.

If 2023 ends with an EPS of $14.45, 2024 is set to grow just shy of 24.5%. The math works out for paying under fair value for growth. If Reels, the ad market, or messenger AI outperforms in any way, the upside potential pushes EPS estimates toward $18.50. This means the P/E drops to 17 even. Comparatively, Google (GOOG)(GOOGL) trades at a forward P/E of 19. Even if I boost analyst consensus for Google (much like I did with Meta), growth is expected to be 18%. Not enough to warrant a higher P/E.

With Meta’s strategy of implementing AI providing superior revenue and net profit returns, Meta winds up being the less risky investment.

The Year Of AI Continues The Legacy Of The Year Of Efficiency

It’s clear 2023’s quest for efficiency has paid off on all the levels it should have: reduced workforce, reduced expenses, better product performance, and better user experience as seen through higher engagement. This has translated to accelerated revenue growth, expanded margins, and former glory free cash flow.

The idea 2024 will be all about AI is another way of saying it’s the Year Of Efficiency version 2.0. It’s because of this focus Zuckerberg and team will continue to drive growth, reduce costs, and find ways to fund its long-term investments without hampering near-term returns. And because of the efficiencies found in 2023, it has rendered the valuation below its growth and below its nearest competitor. Meta continues to perform, as seen in Q3, but it expects the improvements to continue much like the chapter it already started in 2023.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Join My Tech Investing Group For More

Do two things to further your tech portfolio. First, click the ‘Follow’ button below next to my name and then sign up to be a free member of my investing group. You’ll get more free content from me. Then step up to being a paid subscriber to get the chart analysis and trade strategy from this article. I also provide four times more content (earnings, best ideas, trades, etc.) each month than what you read for free here. Plus, you’ll get ongoing discussions among intelligent investors and traders in my chat room.