Summary:

- Meta Platforms’ stock has been rallying over the past year due to strong advertising revenue growth and efficiency measures.

- Although the company faces a growing risk that undermines Meta stock’s appeal as a long-term investment.

- Nexus is downgrading Meta stock to a ‘hold’.

LIONEL BONAVENTURE/AFP via Getty Images

Meta Platforms’ (NASDAQ:META) (META:CA) stock has been on a bull run over the past year, as it delivered strong advertising revenue growth, and the company’s ‘Year of Efficiency’ paid off.

In the previous article, we discussed how Meta’s AI initiatives are promising sources of growth, with the company benefitting from extensive user datasets that can now be leveraged to train and deploy AI models.

Although recently the social media giant has once again come under scrutiny for how it manages the alleged harmful impacts of its platform on society, specifically relating to the U.S. Senate hearing on ‘Protecting Children Online’. And this isn’t the first time that the company has come under pressure for the perceived negative influences of its apps.

The repetitive nature of these allegations and Meta’s inadequacy at inhibiting these plights from taking place on its platform reflects a growing problem that could undermine the company’s growth and financial performance in the future. Nexus is downgrading Meta stock to a ‘hold’.

On the Q4 2023 Meta Platforms Earnings Call, CFO Susan Li announced:

“we will no longer report Facebook daily and monthly active users or family monthly active people. In Q1, we will instead begin reporting year-over-year changes in ad impressions and the average price per ad at the regional level while continuing to report family daily active people.”

So let’s first understand what drives growth in these two key metrics that Meta will be focusing on going forward.

Number of ad impressions growth will be driven by more people using the Family of Apps (Facebook, Instagram, Messenger, WhatsApp, Threads) and spending more time on those apps, which would enable Meta to show more ads to these users.

Average price per ad growth will result from improving conversion rates for ads, i.e. Meta being able to show more relevant ads to the right target audiences. To achieve higher conversion rates for advertisers, Meta will need to be able to collect more and more valuable data on its users for more accurate targeting. Advancements in advertising tools that enable advertisers to better measure their ad performances could also help drive growth in average price per ad.

Now the growing allegations against Meta relating to controversial content and negative experiences on its suite of apps could hinder the company’s ability to drive growth in both these metrics.

For many years, Meta has been criticized for making its apps too addictive using its algorithms, so that the company can show more ads to them. Whistleblowers like Frances Haugen have alleged that the company has turned a blind eye to the alleged negative impacts its app can have on the mental health of teenagers.

And more recently, the U.S. Senate hearings on ‘Protecting Children Online’ revealed serious concerns around Meta’s obliviousness towards child sexual exploitation on its platform.

Regulators are concerned that despite Meta trying to resolve these issues by investing billions on safety, the company is still hesitant to make necessary changes in order to avoid hurting its growth and engagement metrics.

The fact that these problems have been recurring issues does raise questions over whether Meta is truly doing all that it can to prevent such things from happening on its suite of apps, even if it means fewer ad impressions.

Nexus believes that ongoing issues surrounding mental health impacts and child safety concerns could catch up to Meta over the long run.

Let’s consider these issues from a shareholder’s perspective.

Firstly, calls for regulating social media platforms more rigorously are growing. In fact, on the Q4 2023 Meta Platforms Earnings Call, CFO Susan Li noted that:

“we continue to monitor the active regulatory landscape, including the increasing legal and regulatory headwinds in the EU and the U.S. that could significantly impact our business and our financial results. Of note, the FTC is seeking to substantially modify our existing consent order and impose additional restrictions on our ability to operate. We are contesting this matter, but if we are unsuccessful, it would have an adverse impact on our business.”

The Federal Trade Commission (FTC) case she is referring to is the allegation that Meta misguided parents over the level of control they have over who could contact their children in the Messenger Kids app. Now the FTC is seeking to ban the social media giant from being able to utilize the data of users aged under 18 for monetization purposes in the U.S.

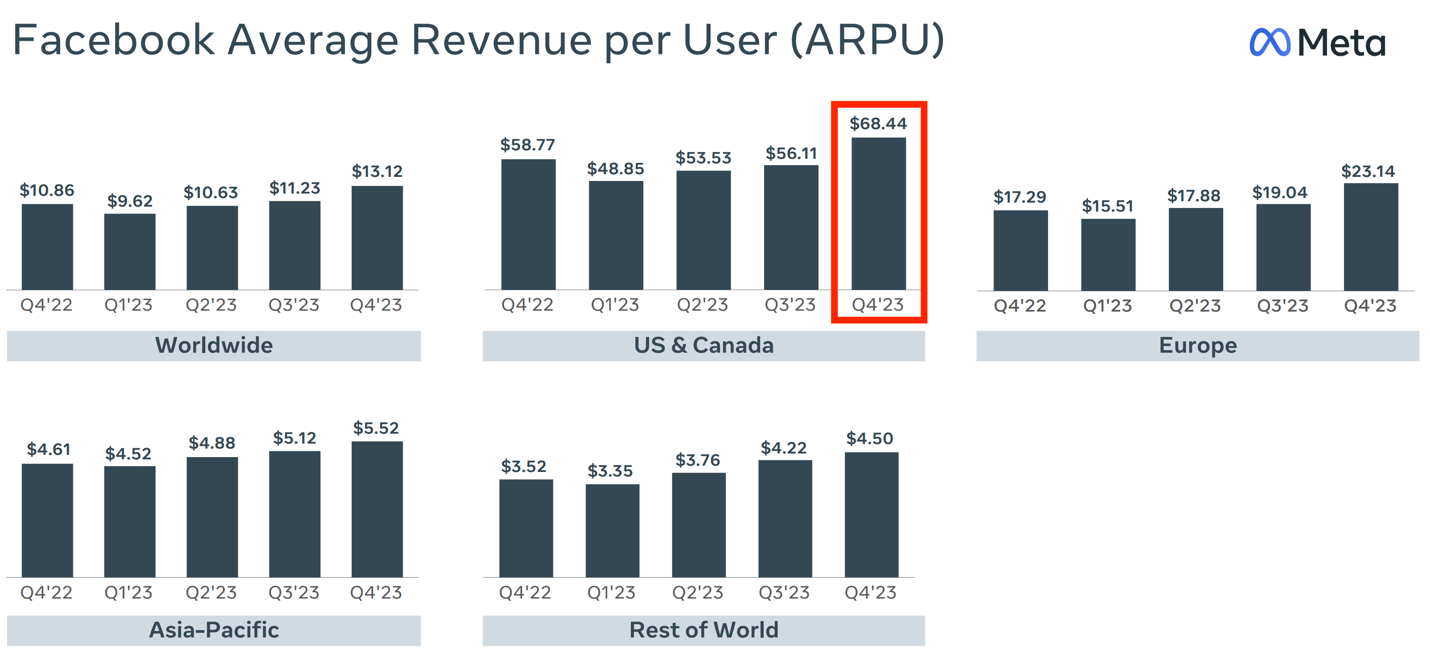

This inability to show more targeted advertising to Americans under 18 years-old indeed poses a significant threat to Meta’s revenue and profits. While Meta does not disclose user and revenue statistics by age group, we do know that the ‘US & Canada’ is the geographical region with the highest Average Revenue Per User (ARPU), with Facebook’s ARPU at $68.44 in Q4 2023. For context, ‘US & Canada’ accounted for 46% of revenue last quarter.

Meta Platforms

Additionally, lawmakers are also considering new bills such as the Stop CSAM Act, enabling victims to sue social media platforms, and the Kids Online Safety Act, which entails greater parental controls and annual audits.

Such measures could indeed drive costs higher for Meta, as well as undermine its ad-based monetization strategies. Although from a moral perspective, such acts would be welcome to subdue the ill impacts of social media on society.

That being said, while this may seem like a bipartisan issue that both U.S. parties can agree upon and pass legislation swiftly, there remain disagreements over how to modify certain types of content, which is delaying such bills from becoming law, and therefore delaying the impacts of such Acts on Meta platforms’ financial performance.

Nonetheless, investors should beware of how such regulatory developments, both in the U.S. and internationally, unfold and impact Meta’s future growth prospects.

Aside from intensifying regulatory risks, we must also consider the potential impacts on user engagement going forward.

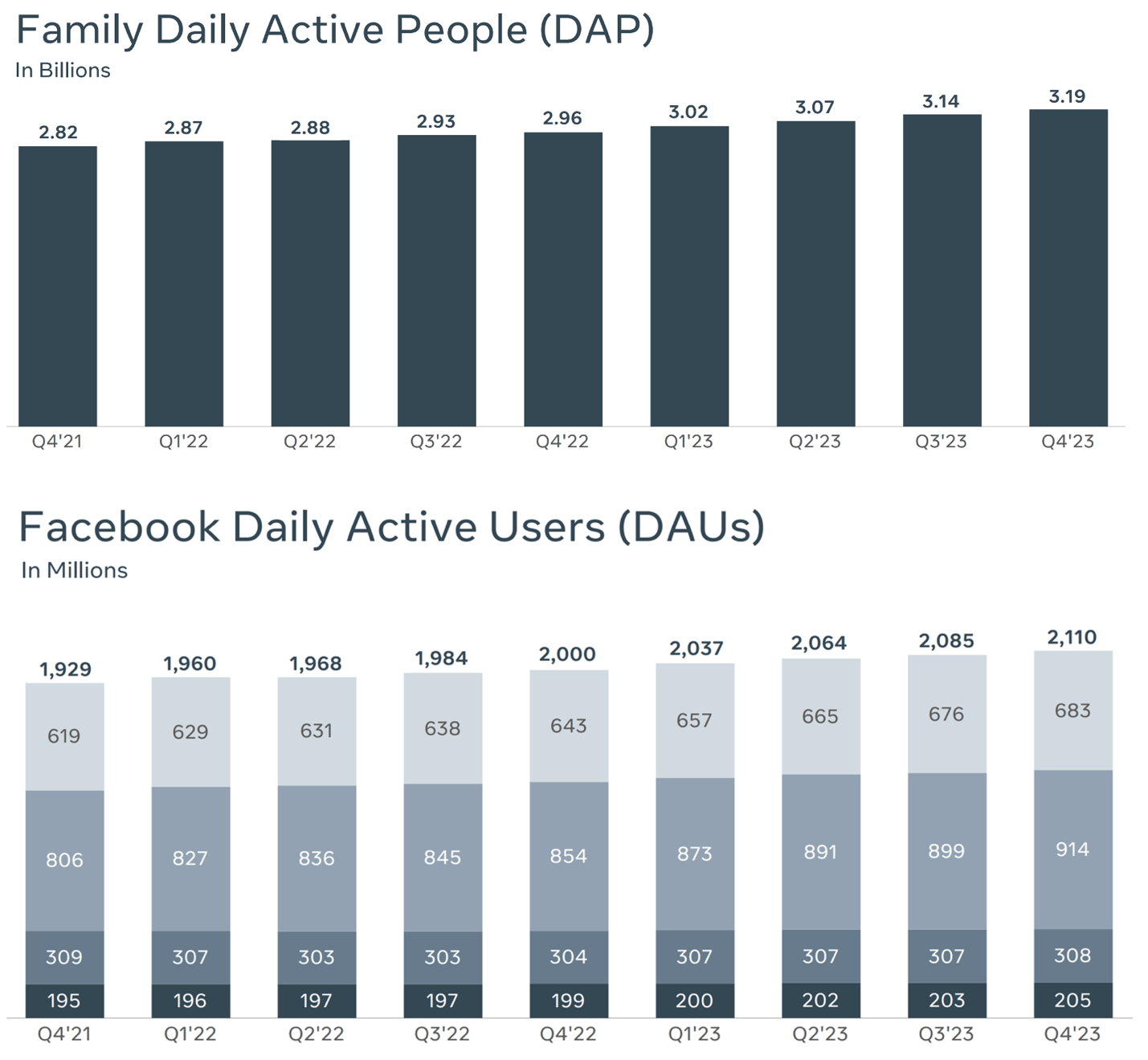

Up until Q4 2023, Meta has disclosed usage trends for the Facebook app and Family of Apps in aggregate. Despite the issues surrounding mental health and child safety, the Daily Active People (DAP) for both of these segments have continued to rise.

Meta Platforms

Although the company does not break out the DAP/DAU statistics for Instagram, to which many of the mental health and child abuse allegations relate to. And so the aggregate Family of Apps statistics could be obscuring alterations in usage trends for such apps individually.

Nevertheless, so far, these issues haven’t seemed to deter growth in advertising revenue for the social media giant.

Although if these issues continue to worsen, they could impede Meta’s growth prospects over the long run. People may spend less time on these apps, or not use them altogether.

The generative AI revolution is likely to give rise to new social media apps that we haven’t even heard of yet, which could take away from the time spent on Meta’s Family of Apps, especially if they offer more positive user experiences, in which case ad dollars could follow.

Hence, in order to stay more competitive against the potential rise of new competitors, it is imperative for Meta to resolve these mental health/ child safety concerns to encourage user loyalty towards its Family of Apps.

Furthermore, any negative user experiences and controversial content could also raise brand safety concerns, whereby advertisers don’t want their ads to be shown in places and at such times when users are encountering a negative experience on the apps.

In fact, back in 2020, major brands like The North Face and Unilever had pulled their advertising on Facebook, citing the social media giant’s inadequacy at controlling “hate speech”.

If Meta wants to successfully achieve long-term growth in its ‘average price per ad’ metric, it will need to step up its efforts to mitigate controversial content and negative experiences on its apps, in order to help protect both users and brands.

Businesses will be willing to pay more per ad if the place and timing are positively relevant, with users having a pleasant experience on the platform when encountering the ad, which would in turn drive growth in the average price per ad metric, conducive to revenue and profit growth.

Meta Financial Performance and Valuation

Meta delivered solid advertising revenue growth over the past few quarters, thanks to increased ad spending from the ‘online commerce’ segment (particularly Chinese e-commerce apps Temu and Shein).

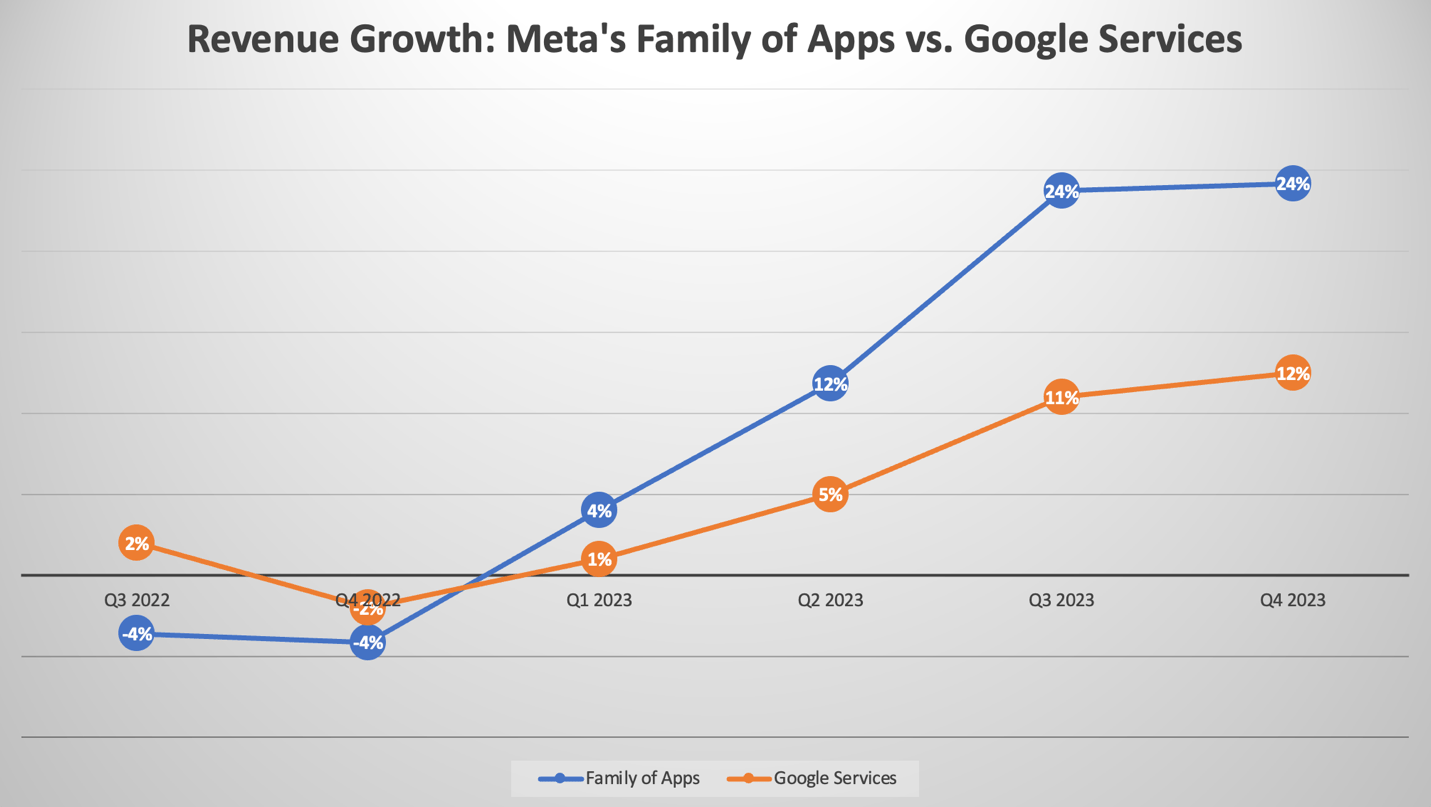

In fact, in 2023 Meta’s revenue growth for its ‘Family of Apps’ segment consistently outpaced the comparable ‘Google Services’ segment (which also derives majority of its revenue from digital advertising).

Nexus, data compiled from company filings

The consistent outperformance in ad revenue growth suggests to the market that Meta is better deploying AI than Google when it comes to targeted advertising.

Though it is also worth noting that in 2022 Meta’s ad revenue was particularly badly hit by Apple’s ‘App Tracking Transparency’ policy changes, easing the year-over-year comparable growth for the social media giant relative to Google.

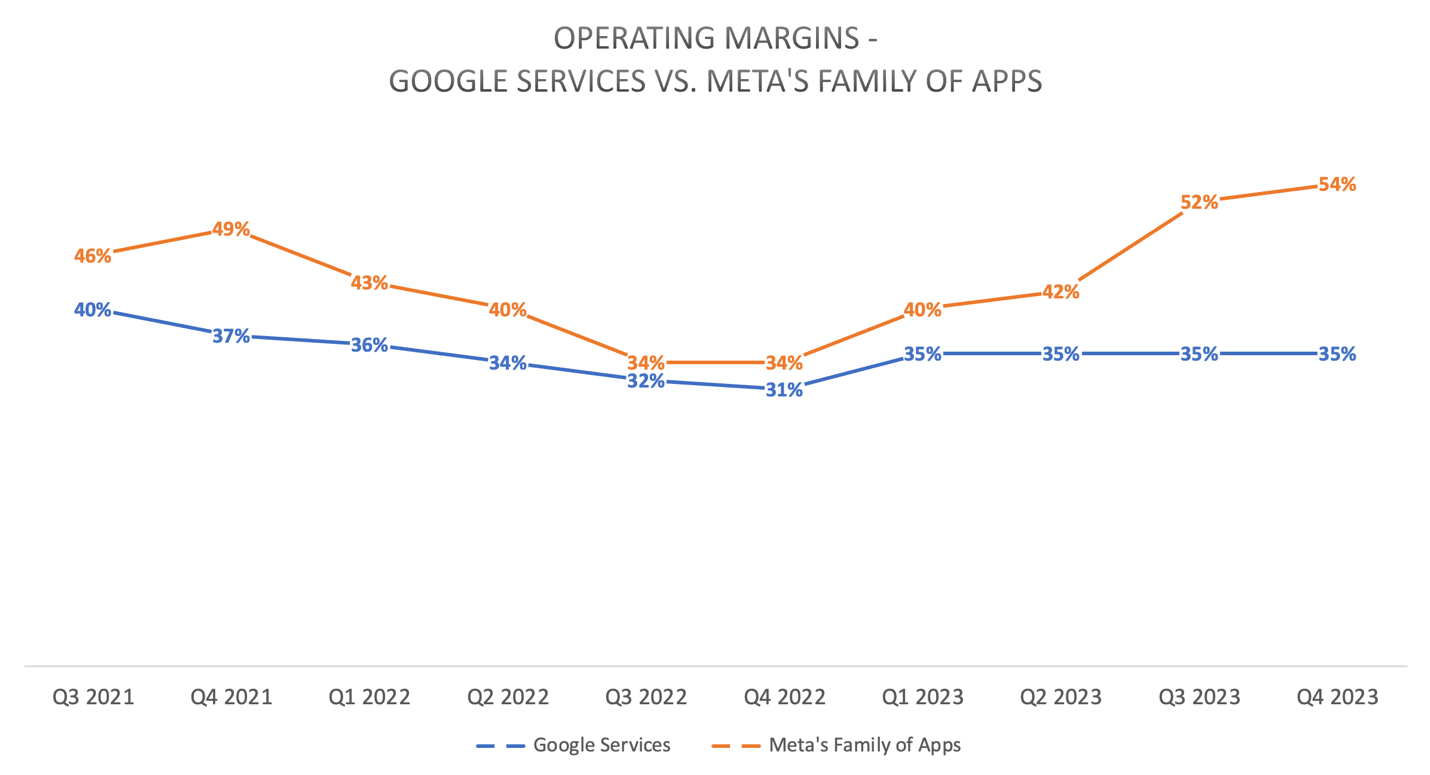

Nonetheless, Meta is not only outperforming its key advertising rival in terms of top-line revenue growth, but also when it comes to operating profitability.

Nexus, data compiled from company filings

Meta’s ‘Year of Efficiency’ in 2023 has clearly paid off as it drove operating margin expansions towards 54% for its key ‘Family of Apps’ segment, while Google Services’ operating margin remained flat at 35%.

The combination of strong top-line growth and operating margin expansion paved the way for an incredible rally of over 184% over the past year.

Although that being said, going forward there are several headwinds facing Meta’s financial performance.

Firstly, on the earnings call, CFO Susan Li had shared that:

“In 2023, revenue from China-based advertisers represented 10% of our overall revenue and contributed 5 percentage points to total worldwide revenue growth.”

The massive ad budgets of Temu and Shein proved to be a great tailwind for Meta’s advertising revenue last year, which may not necessarily repeat again this year.

Furthermore, Meta will also be accelerating its investments into AI infrastructure this year, as Susan Li outlines on the call:

“We anticipate our full year 2024 capital expenditures will be in the range of $30 billion to $37 billion, a $2 billion increase of the high end of our prior range. We expect growth will be driven by investments in servers, including both AI and non-AI hardware, and data centers as we ramp up construction on sites with our previously announced new data center architecture.

…

we expect higher infrastructure-related costs this year. Given our increased capital investments in recent years, we expect depreciation expenses in 2024 to increase by a larger amount than in 2023. We also expect to incur higher operating costs from running a larger infrastructure footprint.”

And the rise in AI-related expenses will not be the only factor putting pressure on profit margins going forward.

As discussed earlier, the recurring allegations of Meta’s suite of apps having negative impacts on people’s mental health and society have led to growing regulatory risks.

Intensifying regulation could not only increase operating expenses to comply with the new laws, but may also impair Meta’s ad-based monetization strategies as regulators push the company to prioritize user safety over user engagement. This could indeed deter Meta’s performance in terms of the ‘number of ad impressions’ and ‘average price per ad’ metrics, undermining future revenue growth and profitability.

Additionally, the FTC case cited earlier poses a significant threat to Meta’s U.S. advertising revenue if the company is indeed banned from using data of users under age 18 for targeted advertising purposes.

And aside from the U.S. regulatory landscape, laws in other countries aimed at mitigating the negative societal impacts of social media are also a key risk facing Meta’s future financial performance.

Now in terms of Meta’s valuation, the stock currently trades at a forward P/E of 24.33x, which is above its 5-year average of 22.97x. The company’s improved profitability over the past year and AI-driven growth prospects help justify its valuation being above historical averages.

At 24.33x, the stock is also more expensive than key advertising rival Google, which trades at 21.5x forward earnings. The market perceives Google’s core search advertising business to be at high risk of disruption, fearing that it will lose its monopolistic market dominance amid the AI revolution. Google has also not engaged in the level of cost cutting measures as Meta to deliver profit margin expansions.

Hence from this perspective, it makes sense for META stock to be trading at a higher valuation multiple than GOOG stock.

Although the growing risk of tighter regulations to subdue social media’s alleged societal harms cannot be underestimated. While any laws restricting social media companies’ activities would also impact Google via YouTube, which made up 11% of the tech giant’s total revenue last quarter, they would have a more pronounced impact on Meta, given that the ‘Family of Apps’ segment contributed 97.3% to company-wide revenue last quarter.

Furthermore, as discussed earlier, there is also the growing risk of diminishing user engagement over time if these issues persist or become worse, especially as new social media apps rise amid the generative AI revolution. And if users flock to alternative platforms, ad dollars would follow.

Nexus Research advises on long-term investment opportunities only. Therefore, despite Meta’s encouraging AI-driven growth prospects over the near-term, Nexus does not believe META is a worthwhile long-term investment with this dark cloud hanging over the company, both from a growth and moral perspective.

Nexus downgrades META stock to a ‘hold’.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.