Summary:

- While many investors have been focused on how the AI revolution will benefit Azure and Bing, it will also boost Microsoft’s most profitable segment through Microsoft 365 advancements.

- 365 Copilot could indeed become a profitable revenue juggernaut for investors thanks to strong pricing power.

- However, competition from a powerful rival may undermine Microsoft’s opportunities.

jewhyte

Ever since Microsoft (NASDAQ:MSFT) struck gold with its investment in the ChatGPT creator, OpenAI, the AI deployment opportunities across Microsoft’s suite of products/ services have proven to be bountiful. The Redmond-based tech giant is perhaps best known for its suite of productivity tools, Microsoft 365, which includes apps like Microsoft Word, Excel and PowerPoint. The company has swiftly embedded chat-based AI capabilities into these offerings, and is signaling lucrative revenue prospects to investors by displaying strong pricing power. Nexus Research has a ‘buy’ rating on the stock.

Over the past several months, Microsoft has been touting the addition of ‘Copilot’ to its Microsoft 365 productivity suite. Copilot is a digital assistant that is powered by the same large language model that underpins ChatGPT. While this feature is still in preview, the company disclosed pricing for this service a few days ago:

Microsoft … said that its artificial intelligence tools for its Office software, known as 365 Copilot, will cost $30 per user per month, significantly raising the price of the software.

Unveiled at its virtual Inspire conference, Microsoft said the $30 per user per month cost will be for its E3, E5, Business Standard and Business Premium customers. These customers have monthly plans that range between $12.50 and $57 per user per month.

Current E3 users pay roughly $36 per user per month for Office 365, effectively making Copilot an 83% increase for that tier of customers.

Microsoft has been previewing Copilot for several months now with various enterprise customers, exploring how this feature can be effectively deployed within organizations, how well it can improve productivity, and what enterprises will likely be willing to pay for it. Given that Microsoft has decided to charge a $30 premium for Copilot signals enterprises are witnessing strong productivity improvements and that the $30 premium is commensurately justified, according to Microsoft.

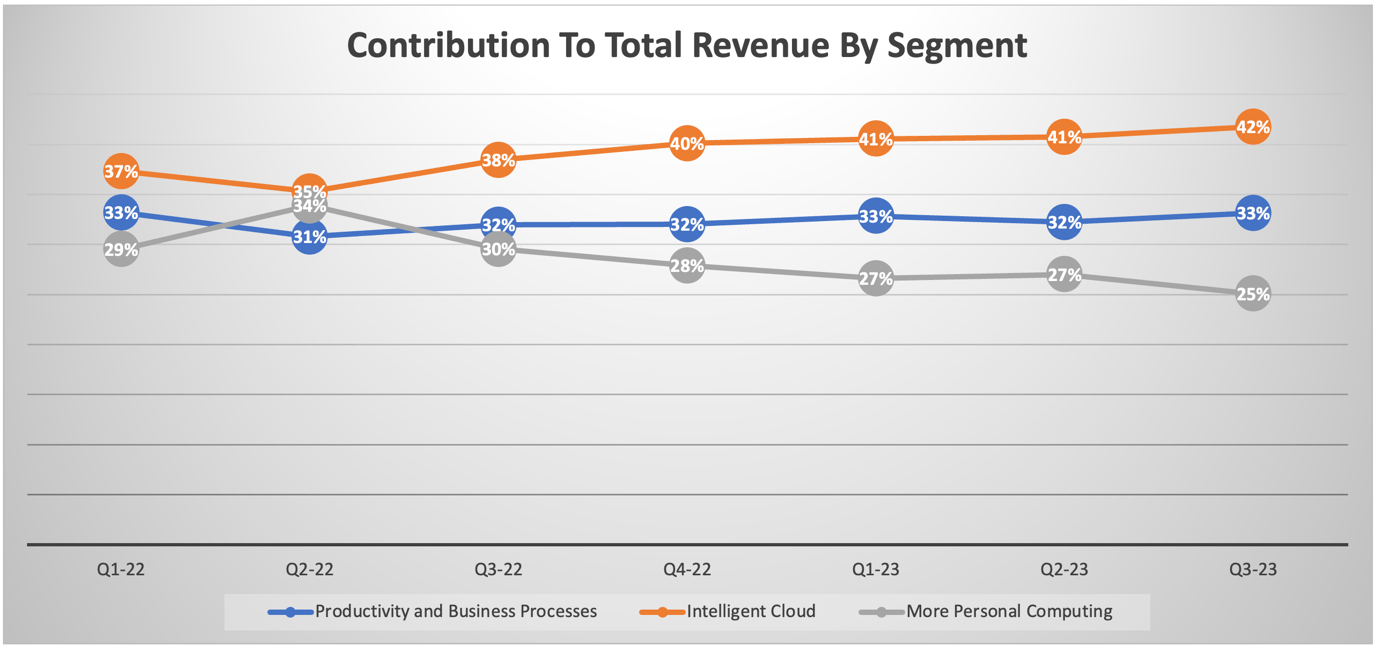

This pricing power indeed strengthens the bull case for the stock, as it bolsters the revenue prospects for its second-largest segment, ‘Productivity and Business Processes’. The segment contributed 33% to total revenue in Q3 2023.

Data compiled from company filings

Adding $30 on top of current subscription fees is indeed pricey, asking enterprises to stretch their budgets, with the promise of cost savings in the form of increased productivity. Wall Street is now eager to see whether Microsoft can actually command this pricing power, in other words, whether enterprise customers are willing to upgrade to 365 Copilot, once it rolls out publicly. Given the AI race across industries, enterprises are likely to invest in the most advanced AI-powered productivity tools to stay competitive. Hence, Nexus Research believes 365 Copilot could indeed become a revenue juggernaut for Microsoft.

The generative AI capabilities through 365 Copilot I think should not only boost productivity, but also make the Microsoft 365 suite stickier as users become increasingly accustomed to relying on Copilot for day-to-day activities. When Microsoft initially introduced the concept of Microsoft 365 Copilot, the company proclaimed that:

“Copilot doesn’t just supercharge individual productivity. It creates a new knowledge model for every organization — harnessing the massive reservoir of data and insights that lies largely inaccessible and untapped today.”

As Copilot gains a holistically comprehensive understanding of an organizations’ data, and becomes increasingly better at assisting users through regular tasks and processes, I think these enterprise customers are very unlikely to abandon their Copilot subscriptions for a competitor’s service given the inconvenient switching costs. This seems to foster the pricing power for Microsoft, conducive to strong recurring revenue for investors.

Furthermore, according to Microsoft:

“The average person uses only a handful of commands — such as “animate a slide” or “insert a table” — from the thousands available across Microsoft 365. Now, all that rich functionality is unlocked using just natural language.”

I think Copilot can help users more easily discover the wide-ranging capabilities of the Microsoft 365 apps that they didn’t know existed, inducing customers to better appreciate the value proposition of the productivity suite, further supporting Microsoft’s pricing power.

Though the opportunities don’t stop there. On the last earnings call, CEO Satya Nadella proclaimed that:

“Teams is also expanding our TAM [Total Addressable Market]. Nearly 60% of our enterprise Teams customers buy Teams Phone, Rooms or Premium. … Teams Premium meets enterprise demand for AI-powered features like intelligent recaps. Now generally available, it’s one of our fastest-growing Modern Work products ever with thousands of paid customers just two months in.”

Therefore, as the tech giant continues to advance the AI capabilities of not just Microsoft Teams, but also the add-on Teams products like Teams Premium, I think it will further fortify the company’s upselling opportunities, creating wider revenue opportunities for Microsoft shareholders.

While Copilot indeed promises to enhance enterprise productivity, competitors will strive to produce similar software functionalities that compete with Microsoft’s Copilot. Therefore, investors will want to see continuous innovation and advancements in Copilot’s versatility over time to sustain its competitiveness and pricing power.

I note that Microsoft has emphasized that Copilot is designed for protecting enterprises’ data privacy. Hence, enterprise usage data is not used to further train Copilot for future editions. While this helps win enterprises’ trust, it could impede Microsoft’s ability to advance the capabilities of Copilot to more intricately serve enterprises’ specific needs and subsequently improve pricing power.

However, while Copilot can’t be trained on data that enterprise users feed into it, it is in fact programmatically designed to learn new business processes as customers use it in new contexts, as Microsoft explained in its blog post:

“Copilot knows how to command apps (e.g., “animate this slide”) and work across apps, translating a Word document into a PowerPoint presentation. And Copilot is designed to learn new skills. For example, with Viva Sales, Copilot can learn how to connect to CRM systems of record to pull customer data — like interaction and order histories — into communications. As Copilot learns about new domains and processes, it will be able to perform even more sophisticated tasks and queries.”

Therefore, Copilot should become continuously better over time at serving the enterprise customers’ needs by being able to carry out company-specific processes and tasks more efficiently through self-learning. This self-learning feature also enables Microsoft Copilot to stay relevant and competitive in a self-reinforcing manner, mitigating the risk of becoming outdated in the face of upcoming rival solutions from competitors. I think this creates an incredibly powerful moat around Microsoft 365 Copilot, conducive to robust recurring revenue, advantaging Microsoft investors.

Increased use of Copilot for various organizational processes could also open up opportunities for Microsoft to encourage greater use of its new or under-used software solutions, over competitors’ solutions. Moreover, Copilot can be programmed to recommend a specific Microsoft app or tool for completing a task, subduing the chance of users looking for a solution from competitors. I think greater use of Microsoft’s own software solutions through Copilot further strengthens the revenue prospects of the ‘Productivity and Business Processes’ segment.

The advanced Microsoft 365 E3, E5, Business Standard, and Business Premium subscription plans will also come with a new feature called Bing Chat Enterprise. It offers office workers a new avenue for “researching industry insights, analyzing data, or looking for inspiration”.

This is a great strategy, in my opinion, to encourage more professional use of its search engine. Moreover, if Microsoft successfully induces more business users to utilize Bing Chat Enterprise over Google to look for various work-related solutions, it could indeed encourage more third-party companies (that provide B2B solutions) to list their websites on Bing and pay ad dollars to put their products/ services in front of Bing Chat Enterprise users. Therefore, this could generate more Bing advertising revenue for shareholders, which contributes to the ‘More personal computing’ segment of Microsoft.

Risks against Microsoft’s bull case

More productivity could mean fewer enterprise subscriptions required: Increased productivity through Copilot could mean fewer people are required to do the same amount of work, potentially leading to slower growth in the number of commercial seats using Microsoft 365 across enterprises, or even declines in the number of seats. The number of commercial seats across enterprises is a key metric used by Microsoft to convey financial performance to investors. For context, last quarter “Paid Office 365 commercial seats grew 11% year-over-year to over 382 million”. From my vInvestors should prepare for a slowdown in seats growth going forward, depending on just how well Copilot can improve work efficiency.

That being said, Microsoft has been previewing Copilot with various enterprise customers, and is cognizant of increased productivity through Copilot potentially leading to lower number of commercial seats going forward. Therefore, Microsoft is wise to charge a significant premium of $30 to compensate for the fewer commercial seats required going forward.

Though from an investment standpoint, simply recovering revenue lost through lower number of commercial seats with higher revenue per seat does not seem compelling to sustain the bull case. In order to continue delivering solid revenue growth, Microsoft will need to show investors that the higher revenue per seat outweighs the slowing growth in/ loss of commercial seats due to Copilot.

Competition from a powerful rival: Google is also offering its own version of Copilot by embedding its chatbot ‘Bard’ into Google Workspace apps, its own productivity suite. This could undermine Microsoft’s pricing power for Microsoft 365 Copilot.

Microsoft may be well positioned to encourage its existing customer base to upgrade to the Microsoft 365 Copilot subscription plan, given that Microsoft’s productivity suite is already well-ingrained into the enterprises’ massive datasets and activities. However, newly set-up businesses will deeply scrutinize and compare the cost implications between Microsoft 365 Copilot and Google Workspace. How Google will price Bard-powered Google Workspace subscriptions for enterprises remains unknown. Nonetheless, Microsoft will need to continuously add new, superior features to its subscription plans to justify its premium pricing.

Microsoft Financial Performance & Valuation

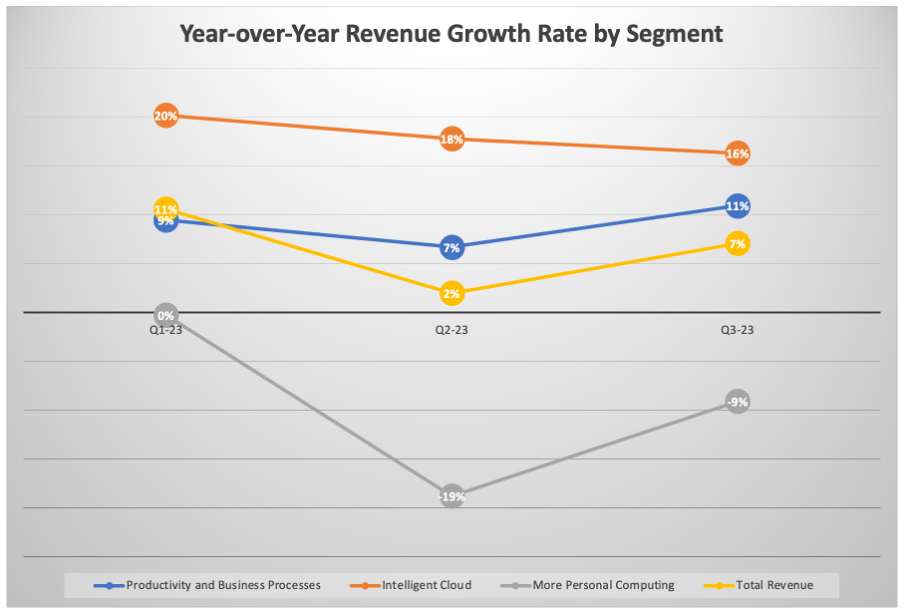

Relative to other segments, ‘Productivity and Business Processes’ has seen the most stability in terms of revenue growth over the last few quarters amid macroeconomic uncertainty.

Data compiled from company filings

The introduction of Copilot for Microsoft 365 enterprise subscription plans should help drive further revenue growth for the segment, but keep in mind that ‘Productivity and Business Processes’ also consists of other products/ services like Microsoft 365 Consumer subscriptions and LinkedIn, which will also impact revenue growth trends going forward.

As noted earlier, the $30 Copilot premium will be for its E3, E5, Business Standard and Business Premium subscription plans. In the table below, Nexus Research has compiled the current monthly price for each of these plans, what the price will be for these plans with the $30 Copilot premium added, and what the consequent price premium is in percentage terms, to get a better sense of Copilot’s impact on revenue.

Data compiled from company website

Microsoft does not disclose how much each subscription plan individually contributes to segment revenue. We could get more insights on the mix of subscription plans in terms of revenue on future earnings calls as Copilot officially launches. However, what we do know is that based on the price premiums, Microsoft stands to generate between 53% to 240% more revenue per user that upgrades to the Copilot subscription plan.

Keep in mind that, as mentioned earlier in the risks section, the improved productivity through Copilot could potentially lead to fewer number of seats going forward. That being said, Nexus Research believes that despite the expensive premium, Microsoft’s Copilot-powered productivity tools will be a necessity for enterprises as they strive to stay competitive in their respective industries, conducive to a lucrative upgrade cycle for Microsoft. This will boost revenue per user ranging from 53% to 240%, depending on which subscription plan they use, enabling Microsoft stock to command a higher valuation based on sales multiple. It currently trades at around 12.50x forward sales, nearly 32% above its 5-year average, given the AI-driven growth prospects.

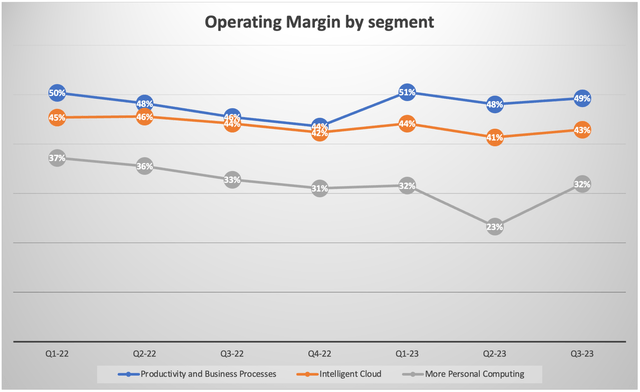

In terms of profitability, Microsoft’s ‘Productivity and Business Processes’ segment is currently Microsoft’s most profitable segment, delivering an operating margin of 49% last quarter.

Data compiled from company filings

Data compiled from company filings

The introduction of Copilot will inevitably increase the compute costs for its cloud-based Microsoft 365 productivity apps. We currently don’t know the exact cost implications and profit margin dynamics for the Copilot-powered subscription services, but should get more insights on the forthcoming earnings calls as Copilot officially launches publicly.

However, as discussed earlier in the article, I think Microsoft has strong pricing power potential through Copilot, given the promising productivity improvements and just how deeply embedded it will become into users’ daily activities. Therefore, I’m confident that Microsoft is well-positioned to pass on the AI-related costs to the consumers, sustaining the tech giant’s high profit margins, and thereby enabling Microsoft stock to command a high forward earnings multiple.

Now tying all this into Nexus Research’s broader perspective on Microsoft, in a previous article we laid out the bull case for Microsoft’s largest revenue segment, ‘Intelligent Cloud/ Azure’. Nexus Research is now re-affirming this bullishness given the Copilot-driven growth prospects of the ‘Productivity and Business Processes’ segment. The AI-driven growth opportunities for Microsoft seem indeed plentiful.

That being said, there’s no denying that Microsoft’s stock is expensive. According to Seeking Alpha data, it currently trades at around 37x forward earnings, 26% above its 5-year average. But here’s the deal, the stock has been expensive for a while now. As investors on the sideline continue to wait for a correction, the stock has continued to rise as the bull case keeps getting stronger amid new AI-related announcements. At the same time, Wall Street analysts keep raising the price target as they try to keep up with the AI rally.

The truth is, even Wall Street analysts are unclear about the exact revenue/ profitability potential relating to AI for stocks like Microsoft, leading to regular adjustments of price targets as they learn more about new company developments and the market keeps pushing the stock price higher.

So what should you do as an investor wanting exposure to Microsoft’s AI growth story?

Nexus Research is mindful of the fact that the current expensive valuation can be a tricky entry-point, as it is hard to determine whether 37x forward earnings is a fair valuation to pay while the full revenue/ profitability prospects remain uncertain. Though at the same time, it can be painful to sit on the sideline knowing that Microsoft will be a big beneficiary of AI over the long-term, especially as the company shows strong earnings growth prospects through impressive pricing power. I think if you’re looking to invest in Microsoft over the long-term, it is imperative to start building a position despite the expensive valuation, while keeping dry power on hand to buy more in case there is a dip in the stock price.

Therefore, to ease the pain of buying high, Nexus Research recommends a dollar-cost-averaging strategy to gradually build a position in the stock, and take advantage in case a correction does materialize. But make no mistake, Microsoft stock is a treasure worth owning for the long-term.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MSFT either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.