Summary:

- Microsoft reported a double beat for Q4 FY-2024, but the stock tumbled over 6% in after-hours trading after an unexpected miss in Microsoft’s Azure Cloud business.

- While Azure Cloud growth is now decelerating, management guided for increased CAPEX spending for FY2025. The ROI on AI infrastructure spending remains an unanswered mystery.

- Microsoft stock is upgraded to a “Neutral/Hold” rating due to its expected 5-year CAGR return now exceeding treasury rates. However, Microsoft’s long-term risk/reward is nowhere close to justifying fresh capital.

juliannafunk

Introduction

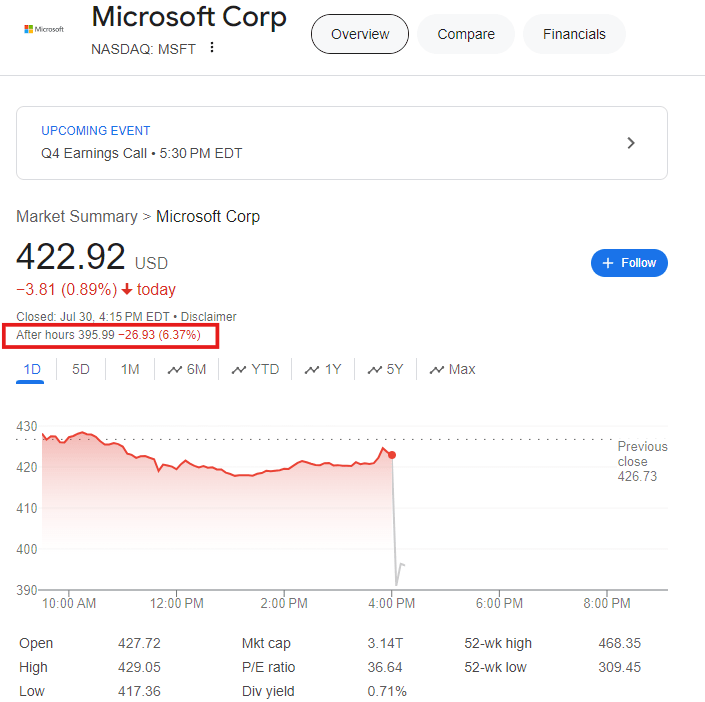

Despite reporting a double beat for Q4 FY-2024, Microsoft Corporation (NASDAQ:MSFT) stock has tumbled by more than -6% to $396 per share in the after-hours session.

GoogleFinance

Heading into today’s report, Microsoft was sitting 10% off of its highs, and so, we are firmly in the correction territory now. In this article, we shall investigate Microsoft’s Q4 FY2024 report and re-evaluate its long-term risk/reward to make an informed investment decision.

Brief Review of Microsoft’s Q4 FY2024 Report

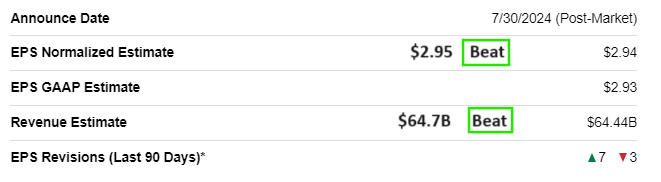

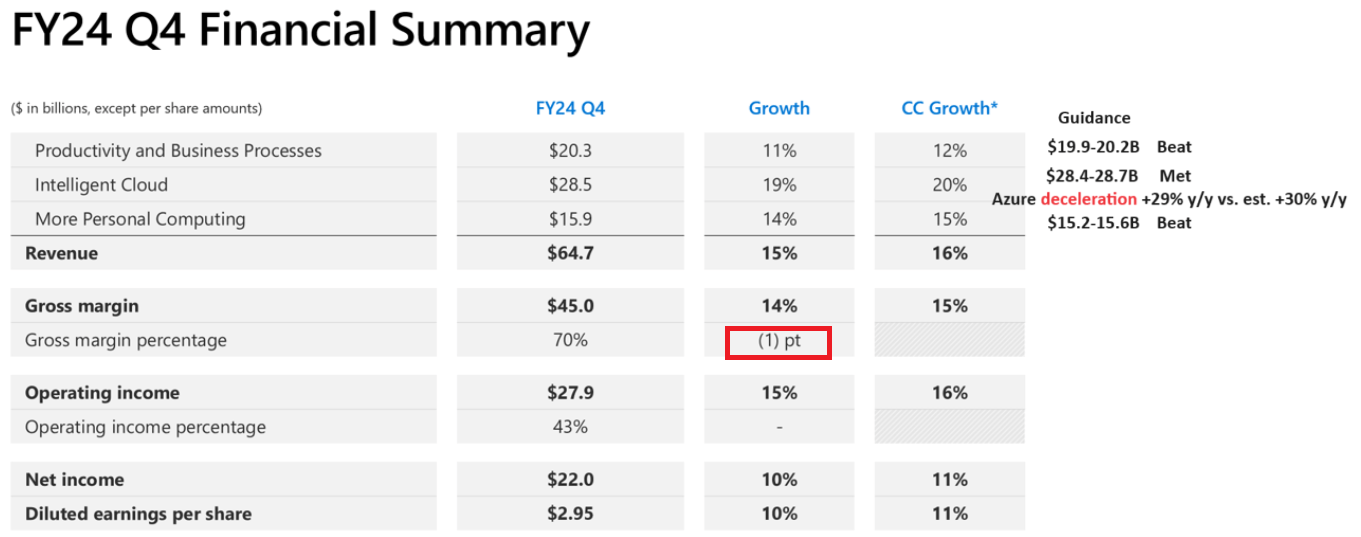

For Q4 FY2024, Microsoft reported a double beat, with total revenues of $64.7B (+15% y/y, vs. est. $64.4B) and diluted EPS of $2.95 (+10% y/y, vs. est. $2.94); however, the quantum of the beat was minuscule.

Author, SeekingAlpha Microsoft Investor Relations

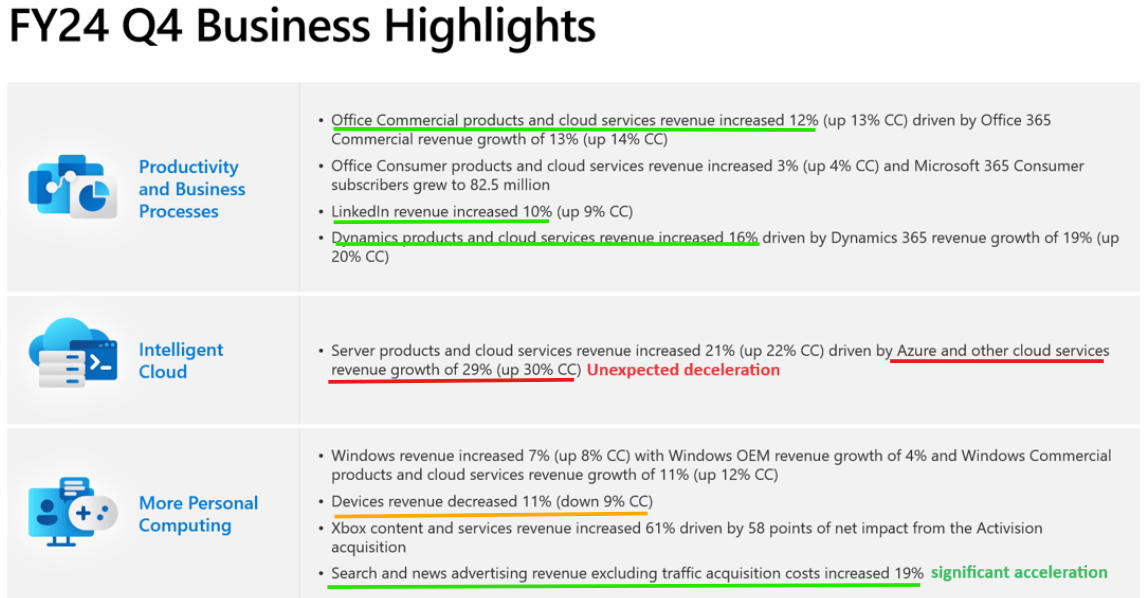

As you can see above, Microsoft’s Productivity & Business Processes [$19.6B, +12% y/y] and More Personal Computing [$15.6B, +17% y/y] segments exceeded management’s guidance range, the Intelligent Cloud business [$28.5B, +21% y/y] was closer to the lower end of management’s guided range of $28.4-28.7B, with deceleration in Azure Cloud growth rate from 31% y/y in Q3 to 29% y/y in Q4. Last week, Alphabet reported an acceleration in Google Cloud Platform revenues (from 28% y/y to 29% y/y); hence, the deceleration in Microsoft Azure is a real negative surprise!

Microsoft Investor Relations

While Azure numbers look disappointing, Microsoft’s Search and News Advertising revenues jumped +19% y/y, a significant acceleration from last quarter’s 12% y/y growth. Finally, AI-powered Bing showing some progress!

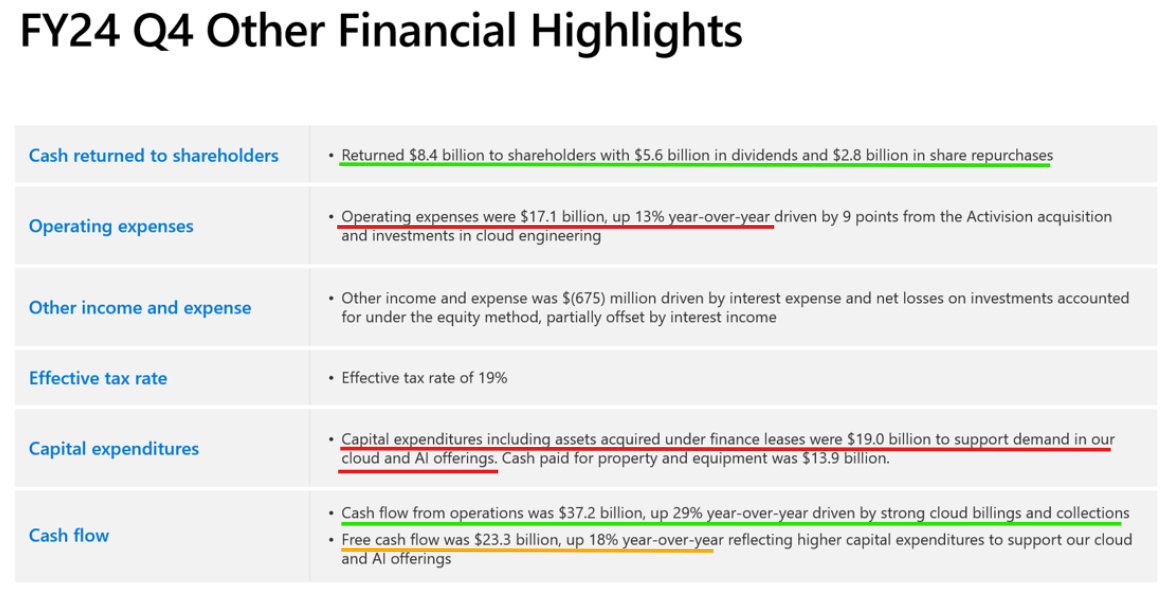

Now, during Q4 FY2024, Microsoft’s operating expenses grew by +13% y/y while the revenue growth rate moderated to +15% y/y. Consequently, Microsoft generated $37.2B in cash flow from operations (+29% y/y) and $23.3B in quarterly free cash flow (+18% y/y) in Q4. From these free cash flows, Microsoft returned $8.4B to its shareholders in the form of share repurchases ($2.8B) and dividends ($5.6B).

Microsoft Investor Relations

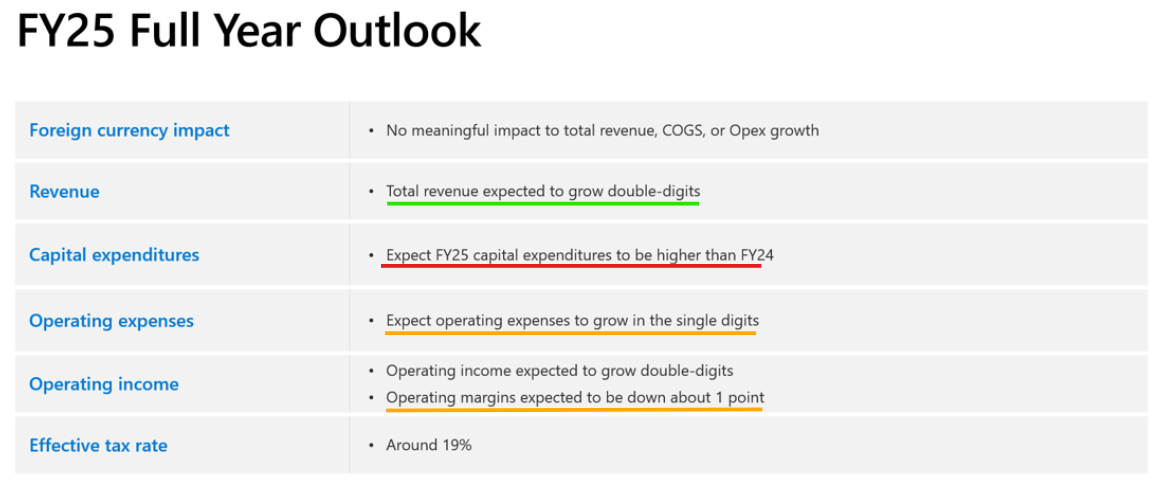

Microsoft is still a giant cash printing machine; however, with the gap in its revenue and operating expenses growth rates narrowing in recent quarters, concerns about Microsoft’s operating leverage (margin expansion) story hitting a snag have been rising. However, Microsoft’s FY2025 outlook calls for double-digit revenue growth and single-digit operating expenses growth:

Microsoft Investor Relations

Hence, I am no longer worried about Microsoft’s operating leverage.

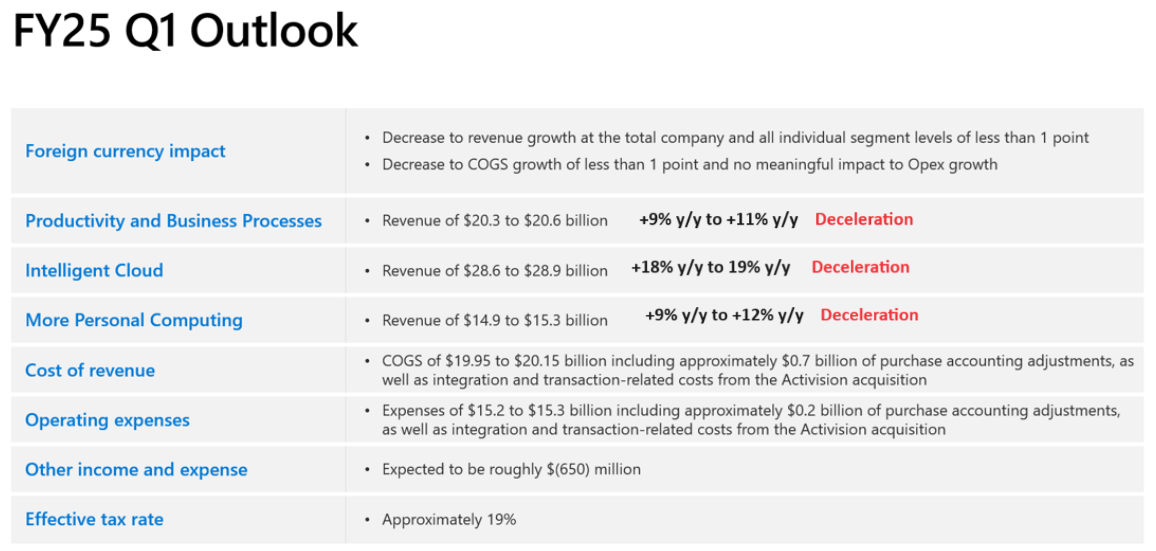

For Q1 FY2025, Microsoft’s management guided for deceleration across the business, with total revenues expected to come in at $64.3B at the midpoint of the guidance range, a figure that fell short of pre-Q4 consensus street estimates for Q1-FY2025 revenue of $65.45B.

Microsoft Investor Relations Microsoft Investor Relations

Furthermore, Microsoft’s leadership guided for increased CAPEX spending in FY2025, with Q1 FY2025 CAPEX set to rise sequentially from the $19B Microsoft spent in Q4 FY2025. With roughly half of this CAPEX spend going into real estate and infrastructure, Microsoft’s management sees this spending as a long-term asset that will be monetized over 15 years! Also, Microsoft’s leaders – Satya Nadella and Amy Hood – expressed a belief that Microsoft’s increased CAPEX spend is a sign of higher AI demand; however, while doing so, they mentioned architectural consistency between cloud and AI infrastructure, i.e., if Microsoft ends up overbuilding AI capacity, they will monetize the GPUs via cloud computing demand. This sort of language was utilized by Alphabet’s leadership, too. Unfortunately, both Nadella and Pichai failed to provide a real answer on the ROI (quantum and timeframe) of the ongoing AI infrastructure spending. Yes, it might be too early to make an assessment; however, with elevated CAPEX spending about to apply pressure on FCF generation, stock prices could get hurt in the near term if the return on investment remains uncertain.

Overall, Microsoft’s Q3 FY2024 report is mixed. While the company beat top and bottom-line estimates, it failed to meet lofty investor expectations. Despite increasing its AI CAPEX spending, Microsoft’s Azure Cloud revenue unexpectedly decelerated in Q4. This raises question marks over the future ROI on the ongoing CAPEX spending cycle and, in my view, puts a richly valued MSFT stock in the penalty box for the next quarter at the very least.

Let us now re-evaluate MSFT stock in light of these Q4 FY2024 numbers.

Microsoft Fair Value And Expected Returns

In Microsoft: Bubble, Bubble Toil, And Trouble, I shared detailed reasoning behind our model assumptions for Microsoft. For today’s evaluation, we’re sticking to all of our past assumptions, with the only change coming in the form of the model’s revenue base – TTM revenue now stands at $245.3B

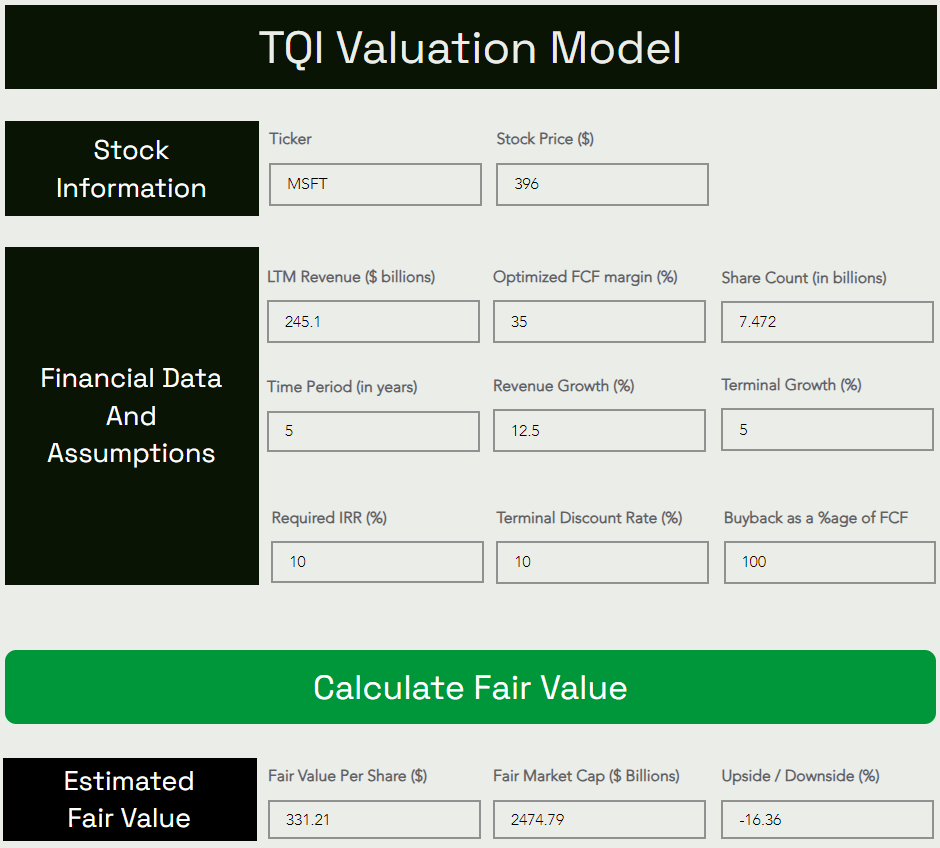

Now, despite using aggressive assumptions for long-term growth and steady-state margins, Microsoft continues to look overvalued, albeit the gap to fair value has narrowed to ~15% in light of the ongoing correction in MSFT stock:

TQI Valuation Model (Free to use at TQIG.org)

According to our valuation model, Microsoft’s fair value estimate is ~$331 per share (or ~$2.5T) [up from $320 per share or ~$2.4T at the last assessment]. With the stock trading at ~$396 per share, I now see a downside of -16% to fair value in MSFT stock.

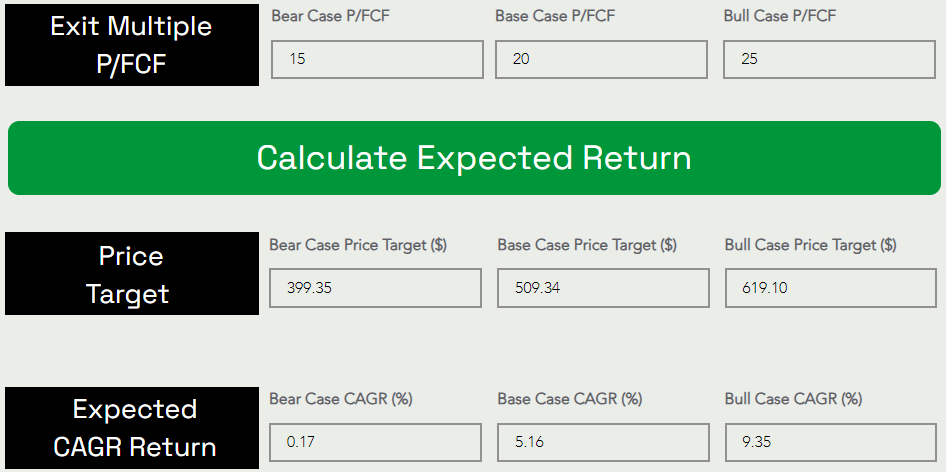

Predicting where a stock will trade in the short term is impossible; however, over the long run, a stock will track its business fundamentals and obey the immutable laws of money. If the interest rates were to return to artificially low levels (i.e., ZIRP), higher equity multiples would be justifiable. However, I work with the assumption that interest rates will eventually track the long-term average of ~5%. Inverting this number, we get a trading multiple of ~20x (P/FCF).

Assuming a base case exit multiple of 20x P/FCF, I see Microsoft stock rising from ~$396 to ~$509 per share in the next five years at a CAGR of 5.16%.

TQI Valuation Model (Free to use at TQIG.org)

Since MSFT’s expected return falls well short of our investment hurdle rate of 15%, I am still not a buyer here. While MSFT looks unattractive when compared to the S&P 500’s (SPY) long-term average return of ~8-10%, Microsoft’s 5-year expected return is now better than treasury yields [~4-5%]; hence, Microsoft is no longer “Sell” under our valuation process. Henceforth, I am upgrading MSFT stock to a “Neutral/Hold” rating.

Concluding Thoughts: Is Microsoft Stock A Buy, Sell, Or Hold Now?

Microsoft is one of the perennial “buy the dip” stocks, and so, most investors are likely chomping at the bit to buy the ongoing ~16%+ correction in MSFT stock. While I continue to think of Microsoft as an incredible company, its long-term risk/reward doesn’t justify the allocation of fresh capital just yet.

That said, Microsoft’s 5-year expected CAGR return now exceeds risk-free government treasury rates, and this is why I am upgrading MSFT stock to a “Hold/Neutral” rating.

As of Q4 FY2024, Microsoft is performing exceptionally well right now (despite the slight deceleration in Azure). In the event of a hard landing, we could see Microsoft retracing to its fair value (and who knows, it could probably overshoot to the downside, like in previous economic downturns). If the long-term risk/reward for MSFT stock improves beyond my investment hurdle rate of 15% CAGR through a time or price correction, I will happily turn bullish.

Key Takeaway: I rate Microsoft a tactical “Sell” in the $400s.

Thank you for reading, and happy investing! If you have any questions, thoughts, and/or concerns, please feel free to share them in the comments section below.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.