Summary:

- Microsoft remains attractively valued with robust long-term prospects, due to its ability to monetize the PC refresh cycle and generative AI/ cloud boom.

- This has been observed in the expanding operating margins, growing cloud market share, increasing multi-year backlog, and promising H2’25 commentary.

- If anything, we expect MSFT’s strategic partnership with OpenAI to pay off handsomely, given the potentially hefty equity stake the former may command moving forward.

- Even so, the stock’s relatively expensive FWD PEG non-GAAP ratio implies further sideways trading in the near-term, before any catalysts occur.

Galeanu Mihai

MSFT Is Inherently Undervalued – Offering Opportunistic Investors With Dual Pronged Returns

We previously covered Microsoft Corporation (NASDAQ:MSFT) (NEOE:MSFT:CA) in August 2024, discussing the stock’s pullback attributed to the ‘blue screen of death’ snafus and the supposedly slower AI monetization. This was on top of the massive capex reported in FY2024 and the guidance of higher spending in FY2025.

Even so, we had maintained our optimism surrounding its long-term prospects, attributed to the still robust cloud market share, growing backlog despite the capacity constraints, rich Free Cash Flow generation, and a healthy balance sheet, resulting in our reiterated Buy rating then.

MSFT YTD Stock Price

TradingView

Since then, MSFT has mostly traded sideways at +2.8%, with it appearing to be the new laggard of the Magnificent 7 stocks, as Tesla (TSLA) quickly rallied post US elections.

Even so, we believe that MSFT has continued to execute well, as observed in its ability to monetize the ongoing PC refresh cycle and the generative AI boom.

Firstly, MSFT reported growing Productivity and Business Processes revenues of $28.31B (+54.7% QoQ/ +12.2% YoY) and More Personal Computing revenues of $13.17B (-5.2% QoQ/ +16.2% YoY).

This is on top of the expansion of the segments’ respective operating margins to 58.3% (+8.9 points QoQ/ +1.7 YoY) and 26.8% (-6.7 points QoQ/ -5.9 YoY) – with the impacted Personal Computing results attributed to the lumpy Windows OEM and Devices sales.

Even so, the robust Consumer/ Commercial/ Enterprise demand for MSFT’s well-diversified SaaS/ Cloud offerings cannot be denied indeed, as observed in the growing multi-year Remaining Performance Obligation [RPO] of $266B (-3.2% QoQ/ +23.1% YoY) in the latest quarter, with it offering robust insights to its long-term top/ bottom-line performance.

Secondly, the biggest question in most readers’ minds may be the management’s monetization during the ongoing generative AI boom.

Well, MSFT has already highlighted that “AI-related products are now on track to contribute about $10 billion to the company’s annual revenue, the fastest business in our history to reach this milestone.”

The same may be observed in the Microsoft Cloud sales of $38.9B (+10.5% QoQ/ +22.3% YoY) along with Intelligent cloud’s richer LTM operating margins of 46.7% (+2.5 points sequentially).

When compared to its direct peers, including Amazon AWS (AMZN) at LTM operating margins of 35.3% (+9.5 points sequentially) and Google Cloud (GOOG) at 10.8% (+10.84 points sequentially), MSFT’s robust pricing power and operational efficiency cannot be denied indeed, despite the supposedly hefty costs related to AI training.

If anything, MSFT’s Azure Arc continues to win new adoptions with increased customer count by +85.7% YoY, with it also contributing to the expanding cloud market share to 20% by Q3’24 (inline QoQ/ +2 YoY).

This is compared to AMZN’s stable AWS share at 33% (inline QoQ/ YoY) and Google Cloud’s slower expansion to 10% (inline QoQ/ +1 YoY).

At the same time, MSFT has guided FQ2’25 Azure revenue growth by +31.5% YoY in constant currency, with H2’25 “Azure growth to accelerate from H1 as our capital investments create an increase in available AI capacity to serve more of the growing demand,” likely attributed to NVIDIA’s (NVDA) ongoing production ramp for Blackwell.

This is also why we believe its partnership with OpenAI and the intensified data center capex efforts worth $49.48B over the LTM (+55.8% sequentially) have been highly strategic to its next phase of growth, especially since the management aims to utilize these assets “over the next 15 years and beyond.”

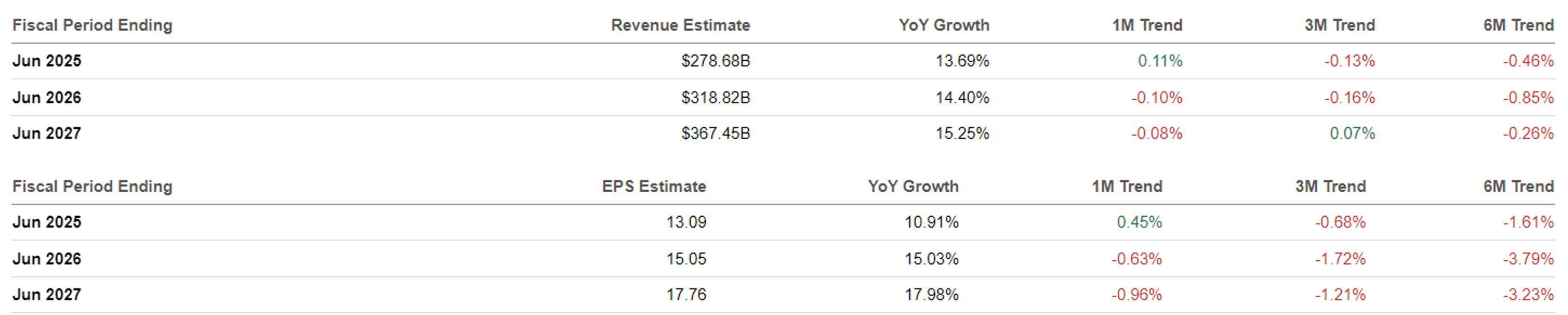

The Consensus Forward Estimates

Seeking Alpha

These reasons are also why the consensus forward estimates remain promising, with MSFT still expected to generate an excellent top/ bottom-line growth at a CAGR of +14.4%/ +14.6% through FY2027.

This is compared to the original estimates of +13.2%/ +12.8%, while building upon the historical growth at +14.3%/ +20% between FY2019 and FY2024, respectively.

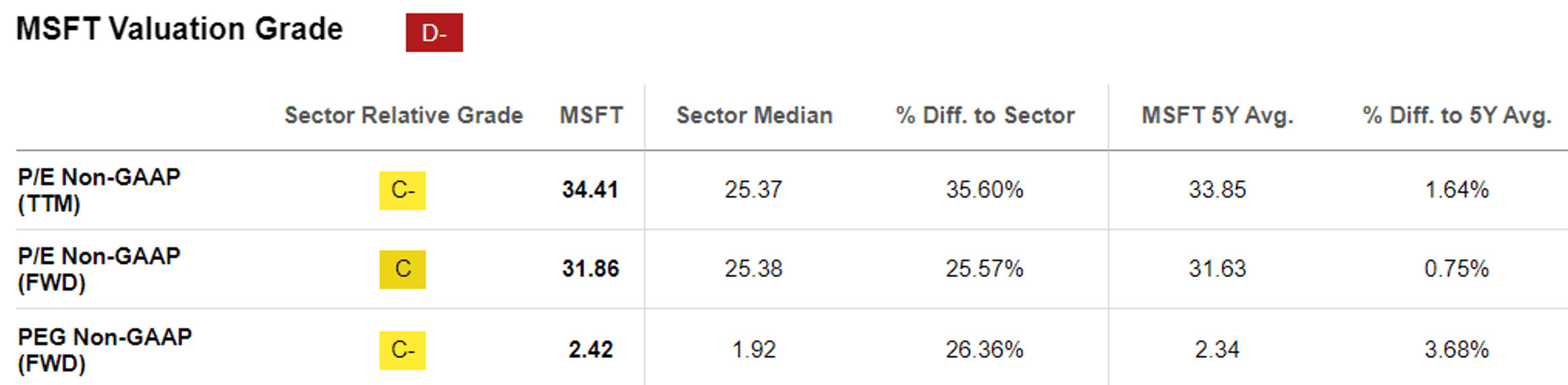

MSFT Valuations

Seeking Alpha

On the one hand, MSFT continues to trade at reasonable FWD P/E non-GAAP valuations of 31.86x, relatively in-line with its 1Y mean of 33.27x and the 5Y mean of 31.63x.

On the other hand, when we use the FWD PEG non-GAAP ratio of 2.42x, it appears that the stock is trading somewhat at a premium compared to the 1Y mean of 1.63x and the 5Y mean of 2.34x.

Even when we compare MSFT to its Magnificent 7 peers, including AMZN at 1.66x, GOOG at 1.26x, Meta (META) at 1.32x, and NVDA at 1.28x, it goes without saying that the former is on the expensive side here, aside from Tesla (TSLA) at 17.26x and Apple (AAPL) at 3.26x.

Perhaps part of the premium may be attributed to MSFT’s highly strategic investments in OpenAI, at an estimated sum of $13.75B against the latter’s last reported valuation of $157B.

With OpenAI now seeking to “restructure itself into a for-profit public benefit company,” we may see MSFT’s investments pay off handsomely indeed, given the potentially hefty equity stake the latter may command on one of the most important AI companies moving forward.

So, Is MSFT Stock A Buy, Sell, or Hold?

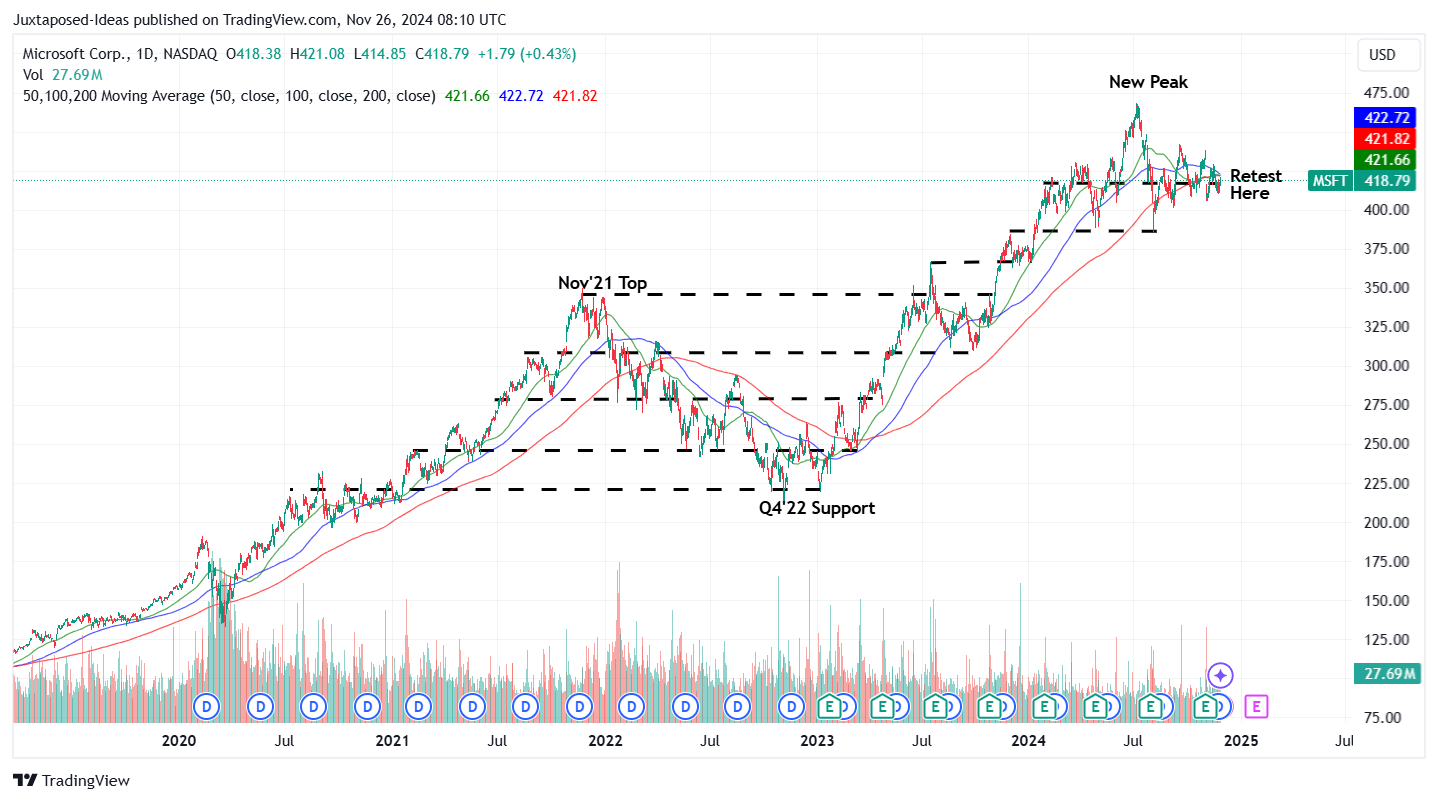

MSFT 5Y Stock Price

TradingView

For now, MSFT continues to trade sideways in 2024 after failing to break out of the 2024 peak of $468s, with it seemingly growing into its premium valuations.

For context, we had offered a fair value estimate of $369.30 in our last article, based on the FY2024 adj EPS of $11.80 (+20.2% YoY) and the 5Y P/E mean of 31.3x.

Based on the LTM adj EPS of $12.12 ending FQ1’25 (+15.9% sequentially), it is apparent that MSFT has run away (yet again) from our updated fair value estimates of $379.30, despite the recent pullback and the sideways YTD trading.

On the other hand, based on the consensus FY2027 adj EPS estimates of $17.76, there remains an excellent upside potential of +32.7% to our updated long-term price target of $555.80.

If anything, based on MSFT’s YTD trading pattern, we are likely to see the stock consolidate here before any catalyst materializes prior to the next earnings call in January 2025 – with the established resistance/ support levels offering interested investors with an excellent margin of safety.

As a result, while we continue to reiterate our Buy rating, there is no specific recommended entry point since it depends on individual investor’s dollar cost averages.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of NVDA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The analysis is provided exclusively for informational purposes and should not be considered professional investment advice. Before investing, please conduct personal in-depth research and utmost due diligence, as there are many risks associated with the trade, including capital loss.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.