Summary:

- Microsoft’s gaming division is often overlooked despite the gaming industry being larger than the movie and music industries combined.

- Xbox Game Pass is a major catalyst for growth, offering access to over 100 games for a monthly fee.

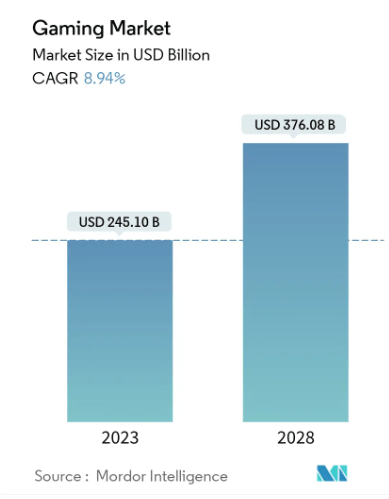

- The gaming industry as a whole is projected to grow at an annualized CAGR of 8.94%. MSFT is set to ride this upward trajectory.

ESOlex

As a gamer, I’ve been exposed to Microsoft (NASDAQ:MSFT) and their gaming related products for over two decades, dating back to the original Xbox console in 2001. In my analysis, I will focus on the items within Microsoft’s gaming related divisions and how this area of the business doesn’t seem to get enough of the spotlight.

A little fun fact is that the gaming industry as a whole is larger than both the movie and music industries combined! I fully expect that trend to continue as advancements in visual fidelity, hardware, and game development continue to be made.

I believe that Microsoft is a buy as the benefits and long term potential outweigh the short term risks.

Gaming Segment

Xbox Game Studios

Microsoft holds the responsibility for creating and releasing some of the most iconic and profitable franchises in history, including: Halo, Forza, Gears of War, The Elder Scrolls, DOOM, Age of Empires, Minecraft, Fallout, Microsoft Flight Simulator, and numerous others.

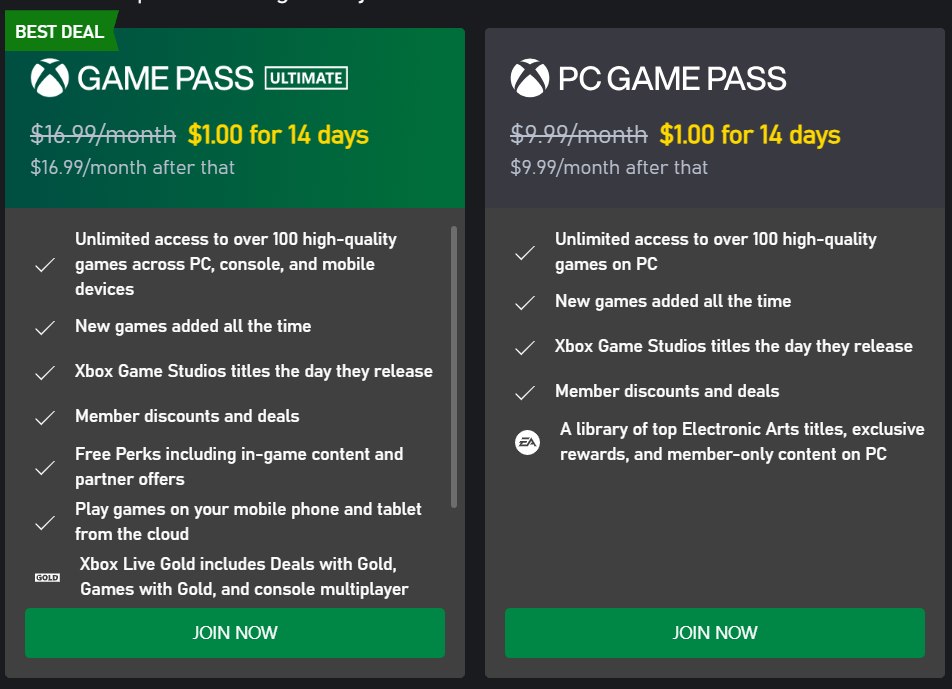

Game Pass

Microsoft’s subscription game service, Game Pass, grants players access to over 100 games for a monthly fee of $16.99 that aligns with many of the popular streaming services.

Xbox Game Pass

A nice bonus of Game Pass is that it comes packaged with a library of games published by Electronic Arts (EA). This is a great bonus as it also includes popular franchises such as:

- Battlefield

- Need For Speed

- FIFA

- Madden

- Sims

- Starwars

- UFC

Xbox Game Pass emerges as the primary catalyst for growth within Microsoft’s video game sector. Microsoft highlighted a 5% growth in Xbox content and services revenue. As of the recent Q4 report, Microsoft’s gaming revenues reached approximately $3.49 billion, marking the second-highest figure in the history of the Xbox division, trailing only behind the fourth quarter of the previous fiscal year.

Industry Growth – MSFT Will Follow The Trend

The gaming industry as a whole is projected to grow at an annualized CAGR of 8.94%. MSFT is set to ride this upward trajectory as they continue with strategic acquisitions and partnerships of different gaming developers and expand upon their library of products.

Mordor Intelligence

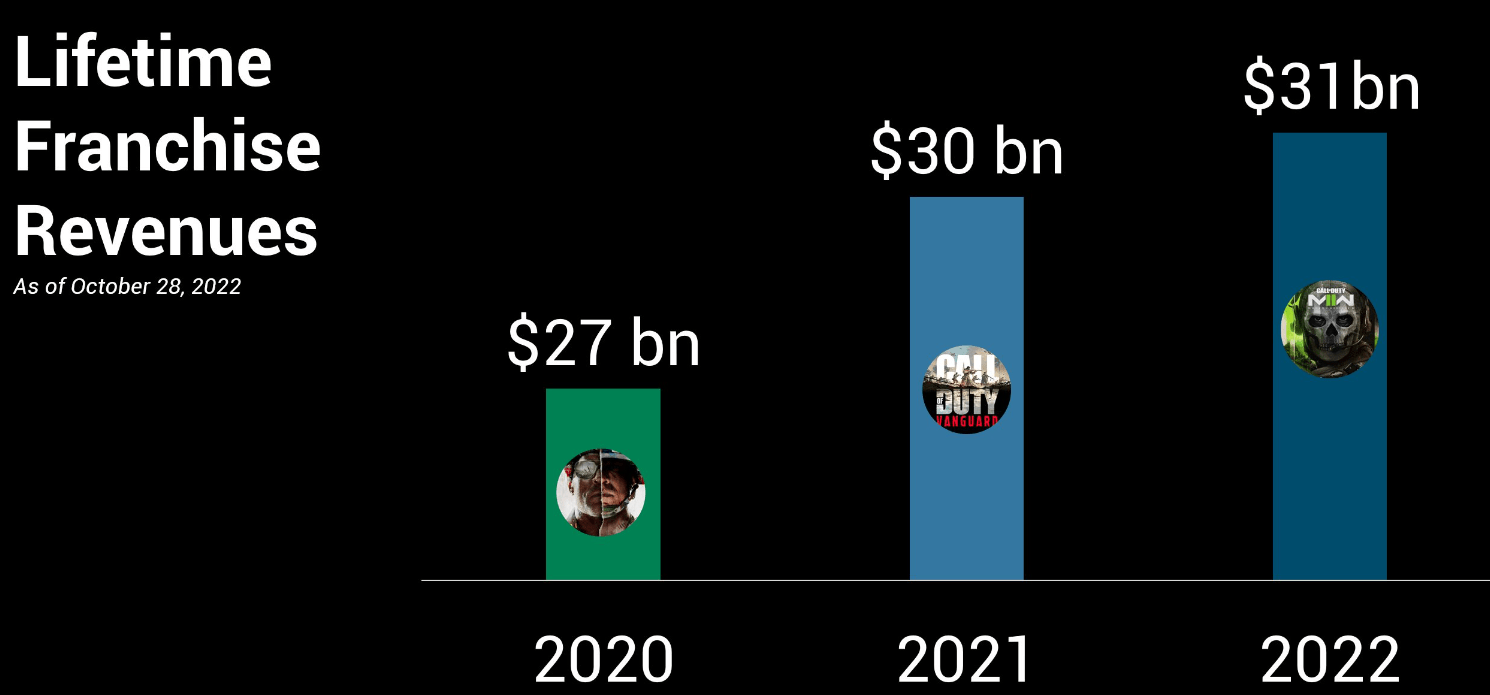

The most controversial, but also potentially most profitable, acquisition on the waitlist is the acquisition of Activision Blizzard (ATVI). If this is successful, MSFT would add about $70B worth of assets in value. ATVI publishes some iconic game series such as:

- Crash Bandicoot

- Call Of Duty

- Spyro

- Tony Hawk’s Pro Skater

- Candy Crush

The Call of Duty franchise alone is worth over $30B and rakes in $1B a quarter from in-game microtransactions. Microtransactions have been a genius way to make money from a franchise even past the sale of the game. These typically include cosmetic items such as clothing for your character, upgrades, weapons, and more within the game that you pay real money for. For example, in 2019, gamers willingly spent an average of $82 on microtransactions in Fortnite, a game that is completely free to play.

Essentially Sports

Forward looking, MSFT is strategically aligning their portfolio of game studios to have a lot of popular franchise names under their umbrella. I think the executives are doing a great job at identifying what developers and game titles would benefit them in the future.

Hardware sales have historically always been weak for Xbox, but I think Microsoft knows that. This is why they are putting in the effort to make their subscription service offer its customers lots of value.

Hardware sales were down 13% last quarter, but this short-term figure takes away from the long term vision. MSFT found a way to get customers without the need to sell a physical console by making their Game Pass service accessible to PC players as well.

AI – Elevating Games

Microsoft has recently unveiled an extended collaboration with OpenAI, marked by plans to invest $10 billion in the company. Text based AI and the relationship to gaming may seem like a reach, but you’re highly mistaken!

I mention AI because there are already indications that AI will transform gaming and increase profitability. The gaming landscape has witnessed a groundbreaking transformation driven by AI with more dynamic and interactive non-player characters (“NPCs”), the emergence of procedurally generated content, and the establishment of immersive gameplay scenarios.

Xbox Game Pass

One example of how this space can improve is to reference popular games that enable players to engage in lifelike conversations with NPCs – Titles such as the upcoming Starfield game that will release as part of Game Pass. RPGs (Role Playing Games) like this offer rich and dynamic dialogue interactions, allowing players to get immersed into real discussions with the game’s characters, each equipped with distinct personalities and responses. Similarly in the popular “Fallout” series, players can engage in realistic and immersive conversations with NPCs, enhancing the sense of realism within the game world.

Furthermore, the incorporation of AI-driven procedural content generation has redefined the way games are developed and experienced. Games like the upcoming “Starfield” utilize procedural algorithms to generate entire virtual universes, ensuring that each player’s exploration journey is unique and unpredictable. This approach allows for boundless opportunities for discovery, fostering a sense of excitement and unpredictability in the gaming environment.

I do believe that this is the natural next step in the evolution of games. This will bring more customers and reoccurring purchases alike. Therefore, increased profitability is likely.

Valuation

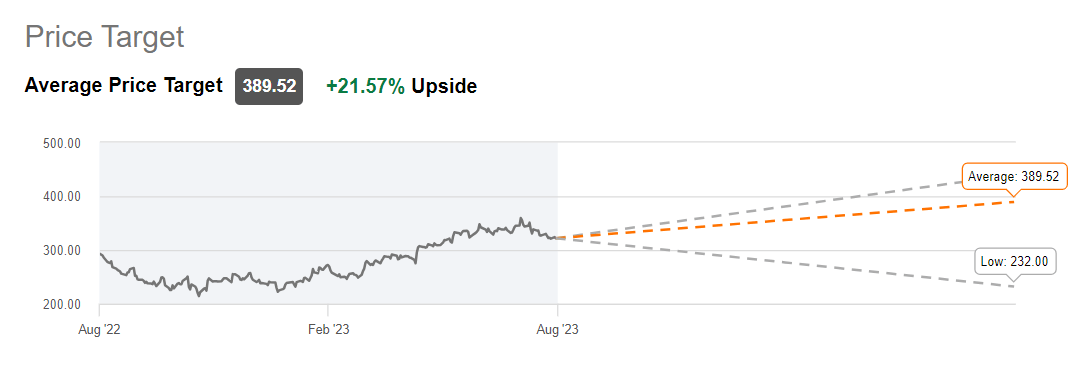

For reference, we can see the average price target for MSFT sits at $389/share. This represents a 21% upside from the current price level of $320. While gaming only represents a fraction of Microsoft’s business, it would be silly for me to give a valuation projection based on gaming data alone. So I will instead focus on how the upside potential through their gaming channel has not yet been captured.

Seeking Alpha

I suggest that investors contemplate taking advantage of the market downturn, considering Microsoft’s ongoing growth, particularly in the Cloud sector. In addition, MSFT has substantial free cash flow that can be directed toward buybacks or strategic acquisitions. Combined with the growth in the video game portion of the business opens plenty of possibility for future growth and I believe entry here would be beneficial to ride the momentum upward.

Tech4Gamers

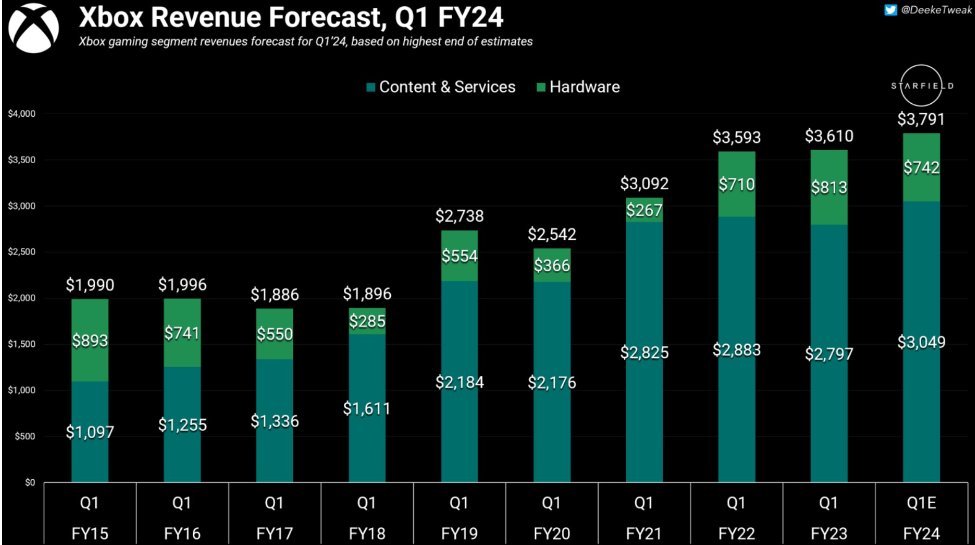

Projected to generate approximately $3.791 billion in revenue, Microsoft has set its sights on Starfield to once again secure a quarter of remarkable achievement, building on last year’s successes. The decision to establish the game as an exclusive title, MSFT is likely forecasting large sale figures and increased subscription revenue from Game Pass on Xbox.

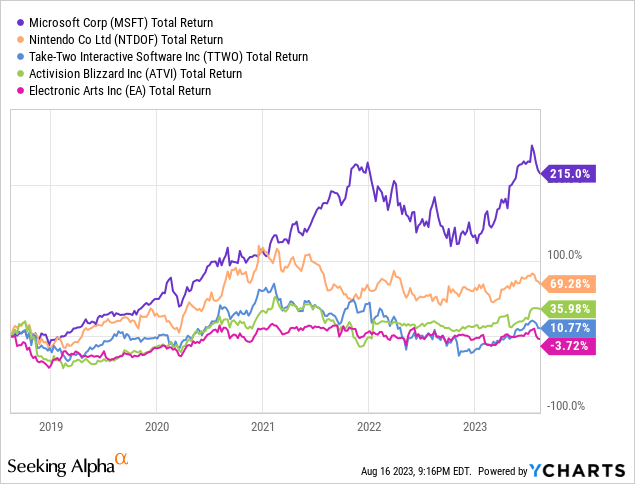

While I know the comparison may be unfair, we can see that MSFT has outperformed the pack. This isn’t surprising considering MSFT is extremely larger and has many more components to their business.

The point is, if I want some video game exposure in my portfolio, why would I invest in any of these individual gaming companies when MSFT has the video game exposure I like but also is already working alongside some of these companies. As previously mentioned, Xbox’s game pass comes with EA titles and simultaneously, MSFT is trying to acquire ATVI. The upward growth here is being hidden by the recent downward movement.

Risks

The primary concern here for me ultimately comes down to the success of Game Pass. If MSFT fails to continue the consistent subscriber growth, we will ultimately see revenue fall. Game Pass is the bread and butter of the gaming umbrella right now. As previously mentioned, hardware sales of Xbox consoles have continued to disappoint. While they are able to capture some subscriber revenue from PC users, the portfolio of streams within the gaming part of the business does not yet have a comfortable diversity of revenue streams.

I think this is all part of the calculated risk though. Short term growth is prioritized in the eyes of shareholders, but MSFT has always stood out by prioritizing substantial investments in its future. They are offering incredible value with Game Pass and as more titles are added, inevitable price increases will happen.

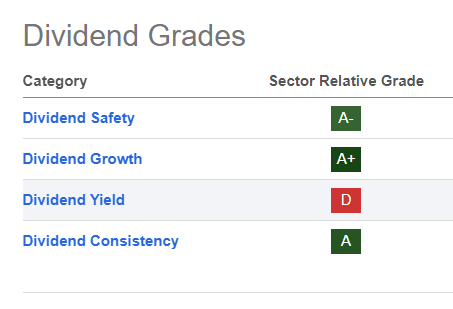

Dividend Growth

The dividend growth of MSFT has been top-notch. Although the starting yield is low around 0.85%, the consistent raises have certainly been impressive.

Seeking Alpha

With a 5-year dividend growth rate of 10.12% and 18 years of consecutive raises, the income provided is a nice bonus. For a company based in the tech sector, the growth is impressive and based on growing revenue and cash flow, I believe the dividend increases are very likely to continue. This is especially true when we see the ultra conservative payout ratio of 28%.

Conclusion

With iconic franchises like Halo, Forza, and The Elder Scrolls under its belt, Microsoft is strategically positioned to capitalize on the industry’s projected growth. The Game Pass offering, which includes titles from Electronic Arts and aims to incorporate Activision Blizzard, showcases a commitment to value and forward-looking expansion. While risks center on Game Pass subscriber growth, Microsoft’s strategic investments, cloud sector dominance, and diversified gaming approach make it an attractive choice for investors seeking long-term upside potential.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MSFT either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.